Chapter 11 – Decision Making with a Strategic Emphasis

11–16

11–26 Sell or Process Further; Product Mix (30-40 min)

1. The key is to identify the relevant costs and revenues associated with

any GR37 diverted for production of SilPol (silver polish).

Incremental Fixed Costs (SilPol) = $5,600

Incremental Contribution Margin/Unit Sold:

Selling price per unit = $4.00

Less: Relevant Costs:

Opportunity cost: lost revenue from GR37:

GR37 selling price/pound = $2.00

$0.70 per unit = 8,000units of SilPol.

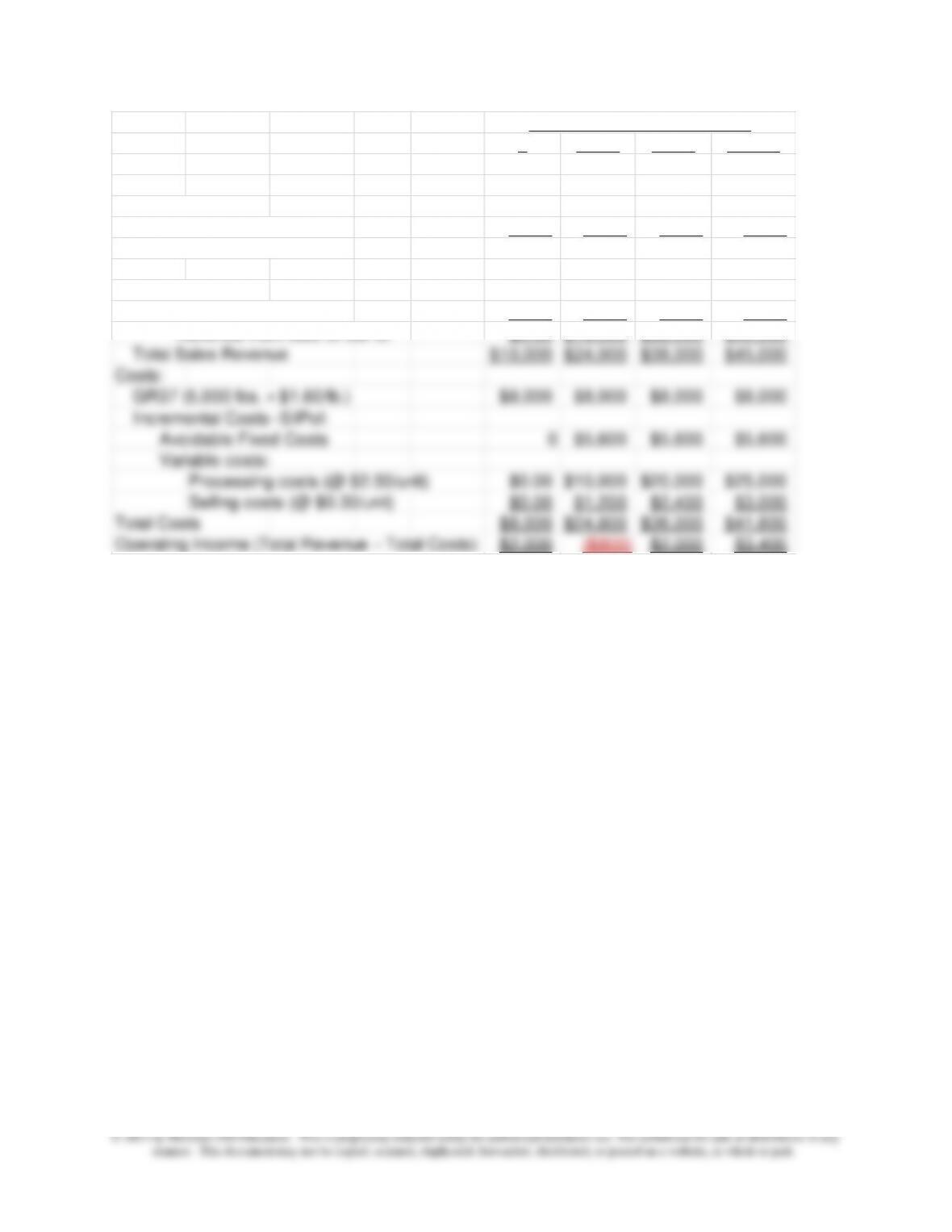

2. Comparative Income Statements —Three Different Product Mixes

Chapter 11 – Decision Making with a Strategic Emphasis

04,000 8,000 10,000

Sales:

GR37:

Pounds 5,000 4,000 3,000 2,500

Selling price per pound $2.00 $2.00 $2.00 $2.00

Revenue from GR37 $10,000 $8,000 $6,000 $5,000

SilPol:

Units 0 4,000 8,000 10,000

Selling price per unit $4.00 $4.00 $4.00 $4.00

Revenue from Sale of SilPol $0.00 $16,000 $32,000 $40,000

Total Sales Revenue $10,000 $24,000 $38,000 $45,000

Costs:

GR37 (5,000 lbs. × $1.60/lb.) $8,000 $8,000 $8,000 $8,000

Incremental Costs–SilPol:

Avoidable Fixed Costs 0 $5,600 $5,600 $5,600

Variable costs:

Processing costs (@ $2.50/unit) $0.00 $10,000 $20,000 $25,000

Selling costs (@ $0.30/unit) $0.00 $1,200 $2,400 $3,000

Total Costs $8,000 $24,800 $36,000 $41,600

Operating Income (Total Revenue − Total Costs) $2,000 ($800) $2,000 $3,400

Units of SilPol Produced/Sold

11-26 (Continued)

Note that at volume levels below 8,000 units, it is not worthwhile to incur

the additional fixed processing costs of $5,600. The breakeven volume, as

indicated by the answer to #1 above, is 8,000 units of SilPol.

Chapter 11 – Decision Making with a Strategic Emphasis

11–27 Product Profitability Analysis (20-25 min)

Note that variable selling and administrative costs should be included in

calculating contribution margin, so that the contribution margin

presented in the problem is incorrect and requires this adjustment.

1. T-1

Last year’s contribution = $200,000 − $70,000 − $20,000 = $110,000

Last year’s contribution margin ratio = $110,000 ÷ $200,000 = 55%

T-2

Last year’s contribution = $260,000 − $130,000 − $50,000 = $80,000

Last year’s contribution margin ratio = $80,000 ÷ $260,000 = 30.77%

2. Required % increase in sales of T-1 to compensate for lost margin from

T-2:

Loss of CM, T-2 = Gain in CM, T-1

3. Required % increase in sales from T-1 to compensate for lost margin

from T-2 if total fixed costs can be reduced by $45,000.

11–19

1. Gross profit calculations, by product, and per square yard

Commercial Residential

Sales (@ $16, $25) $480,000 $200,000

Less: CGS:

Variable (@ $10, $15) $300,000 $120,000

Fixed (@$1.50, $2.25) $45,000 $18,000

Gross profit (margin) $135,000 $62,000

Gross profit per square yard

$4.50 $7.75

Product

11-27 (Continued)

Check:

Last year’s total operating income = $168,000

Projected = $168,000*

4. The following strategic factors should be considered.

• What will be the effect on the firm’s image if T-2 is dropped?

products or in some other value-creating activity?

11-28 Product-Mix Analysis (30-40 minutes)

11–20

3. Optimum product mix, given labor-hour constraint and demand constraints

Commercial Residential

Contribution margin per square yard

$6.00 $10.00

Labor hours per square yard 0.12 0.18

Contribution margin per labor hour $50.00 $55.56

Product

relate to the relevant demands of the two products in terms of the scare

resource (labor hours).

Chapter 11 – Decision Making with a Strategic Emphasis

11–21

11-28 (Continued)

4. Conceptual Lesson

The primary conceptual lesson is that neither of the profit measures

reported in 1 or 2 are useful for determining the short-term optimum

product mix in the presence of resource constraints (labor hours in the

present example). For this purpose it is necessary to allocate available

labor hours on the basis of the contribution margins expressed on a per–

labor-hour basis. In the present case, the residential-grade carpet is the

decisions solely on these alternative profitability figures could lead to a

suboptimal deployment of available capacity.

5. Primary Role of the Management Accountant

The primary role of the management accountant in this context is to

develop accurate estimates of the contribution margins for each product

Optimum Mix:

Residential Grade Carpet: Hours Sq. Yards

Total demand = 8,000 sq yds. × 0.18 hr./sq. yd. = 1,440 8,000

Commercial Grade Carpet (balance of production):

4,600 hours − 1,440 hours = 3,160 hours ÷ 0.12 hour/sq. yd

3,160 17,556

4,600

Chapter 11 – Decision Making with a Strategic Emphasis

11–22

11–29 Solar Panels: Lease or Purchase? (45-60 minutes)

1. Relevant Costs—Leasing vs. Purchasing: Solar Panels

a. Purchase:

(1) original cost, including installation

(2) annual maintenance contract?

(3) annual maintenance expense?

v. loan guarantee programs

(in short, there is an almost bewildering array of financial

incentive programs available at both the government [federal

and state] level and at the level of the local utility provider)

b. Lease:

(1) Lease terms:

i. fixed payment plan per month

ii. Variable-cost payment plan (also known as “Power

Purchase Agreements” or PPAs)—generally, these are

Chapter 11 – Decision Making with a Strategic Emphasis

11–23

11-29 (Continued-1)

(3) Price escalation:

installation

2. Other considerations:

a. Individual

i. Risk—by leasing, the basic risk is that the cost of (purchasing)

solar panels would fall in the future and/or the level of

government subsidy for such would increase significantly

(which effectively reduces the cost): with the lease, the lessee

would be a worthwhile first step prior to installing solar energy

panels

v. Solar energy could conceivably be used in the future to charge

electric cars

Chapter 11 – Decision Making with a Strategic Emphasis

11–24

b. Businesses

1. use of solar-generated power may make businesses more

11-29 (Continued-2)

4. use of solar (i.e., renewable) energy could help the business

5. Image—are the customers more likely to buy from a business

that is viewed as more “environmentally responsible”?

c. Society:

i. Cleaner air/lower levels of pollutants/reduction in level of

Chapter 11 – Decision Making with a Strategic Emphasis

11–25

11–30 Relevant Cost Exercises (60-75 minutes)

a. Make or Buy:

The relevant cost for producing the product is as follows:

Cost Per Unit

Direct Materials $28

Direct Labor 18

Variable Overhead 16

Total $62

($62/unit × 2,000 units) = $124,000

Qualitative Considerations:

a. How does the quality of product compare, insourcing vs.

outsourcing?

b. Reliability (i.e., on-time delivery performance)?

c. Financial condition of the supplier? (With the supplier be in

costs: increased payroll taxes; negative goodwill.

Chapter 11 – Decision Making with a Strategic Emphasis

11–26

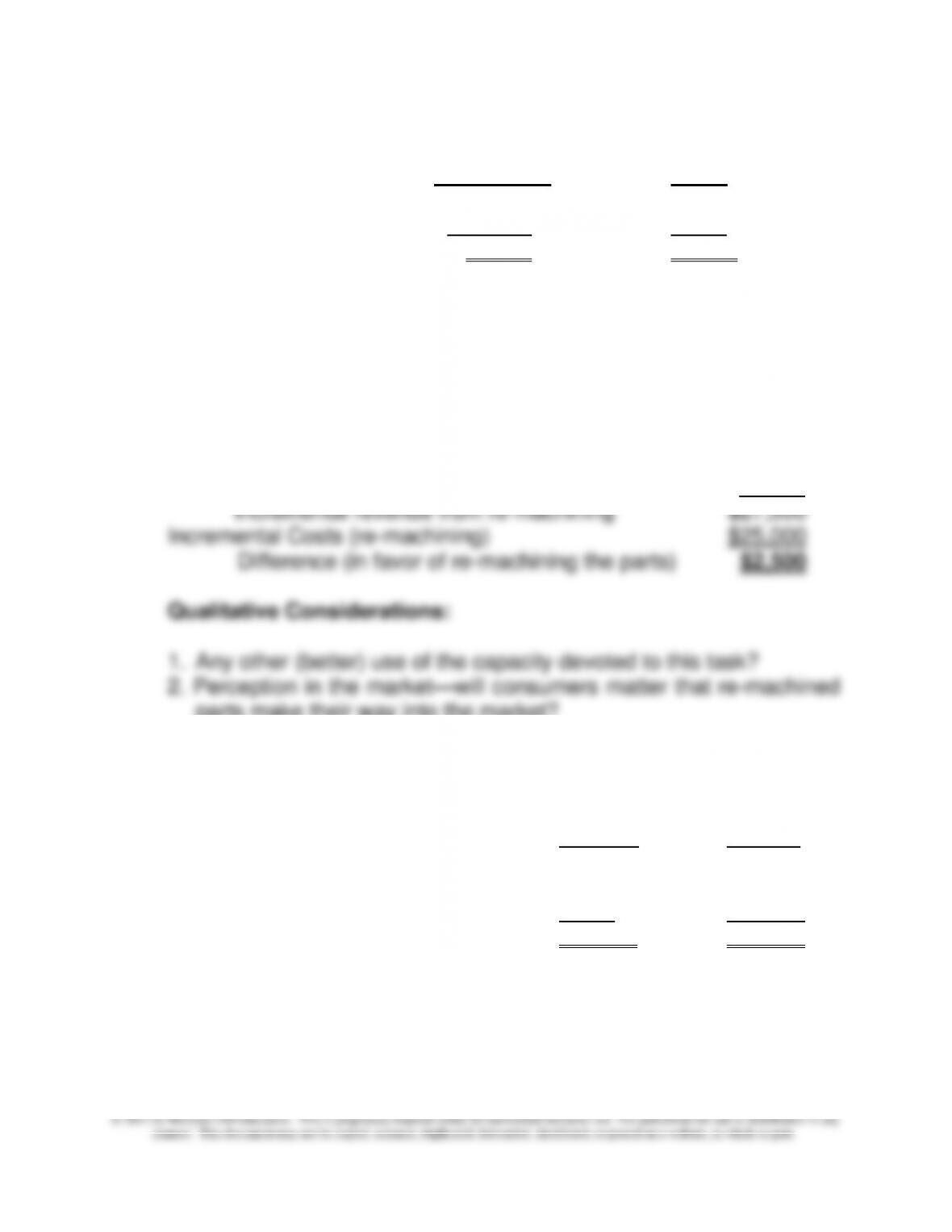

b. Disposal of Assets

Re–machine Scrap

Future Revenues $30,000 $2,500

Deduct future costs 25,000

Difference $5,000 $2,500

11-30 (Continued-1)

The difference is in favor of re-machining. The $50,000 inventory cost

is irrelevant.

Alternative presentation format:

Incremental Revenues from Further Processing:

Estimated sales value of re-machined parts $30,000

Current disposal value of parts $2,500

parts make their way into the market?

3. Reliability/quality of re-machined parts (in the minds of the

consumer)?

c. Replacement of an Asset

Replace Rebuild

New boat $92,000 –

Deduct current disposal price $ 9,000

Rebuild of existing boat $75,000

Margin $83,000 $75,000

The difference is in favor of rebuilding. The $90,000 original purchase

cost is irrelevant as it is a “sunk cost.”

Chapter 11 – Decision Making with a Strategic Emphasis

11–27

Alternative presentation format:

Cost to buy a replacement boat = $92,000

Total cost of refurbishing:

Out–of-pocket cost = $75,000

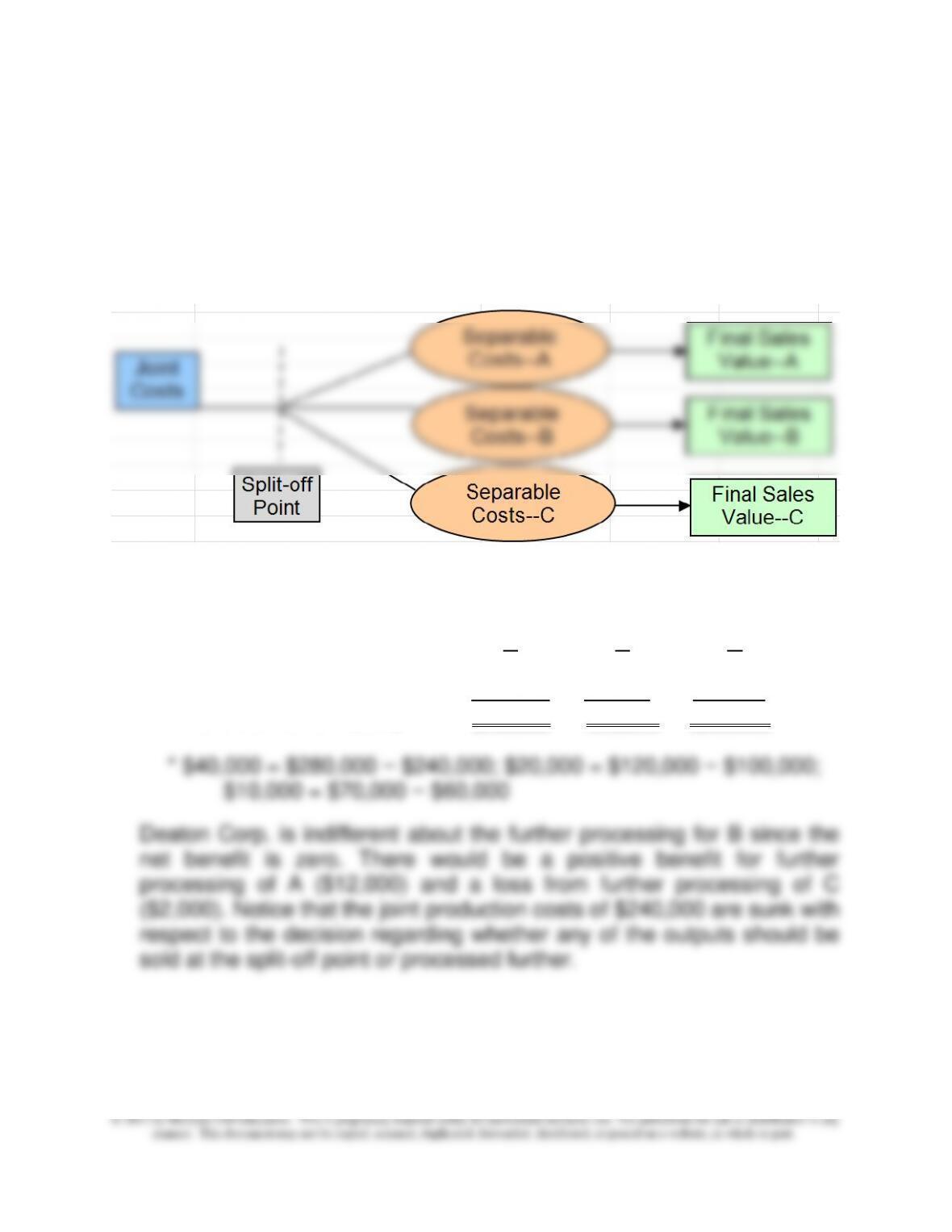

d. Profit from Processing Further (“Sell or Process Further”)

The main point of this exercise is that joint costs should be ignored when

addressing the “sell–or–process further” decision (see also coverage of

this point in Chapter 7).

1. Definitions:

a. joint production process: process in which more than output

emerges from a common resource input (e.g., barrel of crude oil)

b. joint costs: in a joint production process, these are costs incurred

before the split-off point; that is, these costs are joint or common to

the outputs; since these costs are non-traceable, they must be

allocated to outputs

Chapter 11 – Decision Making with a Strategic Emphasis

11–28

d. split-off point: point in a joint production process where products

with individual identities emerge; cost incurred prior to the split-off

point are called joint costs, while those incurred after the split-off

point are called separable processing costs

The situation for Deaton Corporation is depicted in the diagram that

follows.

2. Which products, if any, should be processed further (rather than being

sold at the split-off point)?

A B C

Addt’l costs of further process $28,000 20,000 12,000

Increase in sales value * 40,000 20,000 10,000

Differential benefit (loss) $12,000 $0 ($2,000)

Chapter 11 – Decision Making with a Strategic Emphasis

11–29

3. For financial reporting and tax purposes, accountants need to value

inventory on a “full cost” basis. Thus, in the present case for income-

statement preparation purposes and for purposes of preparing an end–

of-period balance sheet, a portion of the joint production cost of

$240,000 must be assigned to each unit sold during the period and each

unit on hand at the end of the period. There are alternative ways to

allocate joint production costs to outputs. Regardless of how these costs

are handled for financial reporting and tax purposes, they are irrelevant

to the sell-or-process further decision.

e. Make or Buy (sourcing decision)

The relevant fixed overhead is $12 per unit ($20 × 60%) because that

amount could be avoided by buying the part from McMillan. All variable

Nonfinancial Factors that Might Be Relevant

a. Are there alternative (better) uses for the available capacity?

b. Quality of the supplier’s product: how does it compare to the quality of

internal production?

c. Reliability—on-time delivery performance of the supplier?

d. Future price trends: is the supplier price likely to be lower (or greater)

in the long run?

f. Selection of More Profitable Product

1. The comment “Flash and Clash are processed through the same

production departments” can be taken to mean that capacity-related

Chapter 11 – Decision Making with a Strategic Emphasis

11–30

2. Selection of the more profitable product:

Flash Clash

Selling price per unit $250.00 $140.00

Variable cost per unit* 200.00 100.00

Contribution margin per unit $ 50.00 $ 40.00

most profitable product with the labor constraint. The measure,

operating profit, is not used because it includes the sunk fixed costs.

In sum, Clash returns the highest amount per DLH, the scare

resource. Therefore, the optimum short-term product mix would

consist of producing Clash up to external demand. Any remaining

DLHs would then be devoted to the production of Flash.

g. Special-Order Pricing

The total cost of each meal is variable plus fixed cost or $2.00 per

meal + ($1,200 ÷ 600 meals) = $4.00 per meal. This is a reasonable

cost basis for long-term pricing, and Barry is getting a $1.00 margin

on each meal. However, in a special-order situation the fixed costs