Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–31

20–39 (continued -1)

2. [Operating Income – (.06 x Invested Assets)] x .10 = Bonus

Amount

The total bonuses for each division and in total are determined as

follows:

Total Bonus

Consumer

Electronics

Office

Supplies

Computers Total

2011 1,167,700 75,000 106,300 1,349,000

2012 407,300 102,600 29,700 539,600

2013 94,300 108,000 128,900 331,200

And given the number of executives:

Number of Executives

Consumer

Electronics

Office

Supplies

Computers Total

2011 300 40 120 460

2012 350 40 140 530

2013 375 37 175 587

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–32

20-39 (continued –2)

3.

When bonuses are determined on a division-based method, the

results are as follows:

Division-based Bonus

per Executive

Consumer

Electronics

Office

Supplies

Computers

2011 3,892$ 1,875$ 886$

2012 1,164 2,565 212

2013 251 2,919 737

Bonuses per executive were largest for consumer electronics in 2011

because this division, the largest, generated the largest amount of

Bonuses in the Computer division followed the returns in this division,

down in 2012 and up again in 2013; overall the bonuses are smallest

in this division because of the relatively large, and increasing number

of executives in this division.

4.

Comparing the results for the three divisions in parts 2 and 3, it is

clear that the consumer electronics division managers would benefit

from the division-based plan based in 2012, while the Office Supplies

division would benefit in 2012 and 2013.

The contrast between the firm-wide and division-based bonus plans

work to make the opportunities for cross-division profit clear.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–33

20–39 (continued -3)

Pros: The company-wide bonus plan promotes the sharing of

corporate-wide assets. The bonus plan also helps to keep talented

20–34

20-40 Compensation; Strategy (25 min)

For companies with substantial growth opportunities or long

product life cycles, bonus plans based on short-term decisions may

not adequately reflect long-term consequences of managerial

decisions.

options to be paid off.

MBI may want to consider granting stock options where the

exercise price is adjusted with the appreciation of an industry index.

This will allow MBI to reward executives for an increase in the value

of their stock relative to that of companies facing similar risks.

future. This would minimize the chance that executives would

increase current performance measures at the expense of damaging

future performance.

Developing effective compensation plans is more difficult for

multinational companies such as MBI because foreign currency

frequently managers of foreign SBUs are able to protect their unit

from unfavorable currency fluctuations by carefully chosen

purchasing, sales, and financing practices.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–35

20-41 Executive Compensation; Teams; Strategy; Ethics (30

min)

1. Universal should use the new measures to improve product

quality and customer satisfaction.

a. At least three customer value-added measures for Universal Air

Inc. include the following:

• Availability of products to meet customer needs on a timely

basis.

b. At least three process-efficiency measures for Universal include

the following:

• New product development time and introduction time to market.

activities.

2. At least three types of employee behavior that Universal Air Inc.

can expect by having middle management participate in the

development of the second set of new performance measures include

the following:

• Increased job satisfaction and morale, as well as a feeling of

3. To ensure that the cross-functional teams are effective, the

executive management at Universal Air Inc. needs to provide:

• the necessary resources, including people and money

•

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–36

20–41 (continued –1)

functional managers and team members, and support for the

implementation of team-suggested changes.

4. Referring to the specific standards (competence, confidentiality,

integrity, and credibility) in the Institute of Management Accountants

Statement on Ethical Professional Practice, John Brogan’s behavior

is unethical for the following reasons:

Competence

• Brogan is undermining the preparation of complete and clear

reports.

Confidentiality

Credibility

Brogan did not:

• communicate information fairly and objectively disclose fully

all relevant information.

20–37

20-42 Executive Compensation (30 min)

1. a. The benefits to Jensen Corporation of a profit participation

incentive plan for the Hobbit Hole’s restaurant unit managers include

the following:

• Increased employee interest in, and motivation toward the

economic success of the company, leading to goal congruence

between the managers and Jensen. This could include improved

b. The negative behavioral problems that could occur with the

profit participation incentive plan for Hobbit Hole restaurant unit

managers include the following:

• Greater emphasis placed on short-term rather than long-term

objectives. This could have a negative impact on the company in

the long term if items such as capital expenditures are delayed to

problems.

2. a. The advantages to Jensen Corporation from having the motel

unit managers of Cruise and Snooze Inns participate in an incentive

plan based on goal attainment include the following:

• Improved employee motivation and ownership of the goals could

result since the unit managers have participated in establishing the

20–38

20–42 (continued -1)

b. The disadvantages to Jensen Corporation from having an incentive

plan based on goal attainment for the motel unit managers of Cruise and

Snooze Inns include the following:

• There may be a perceived lack of management objectivity or fairness

if goals are not consistent among individuals. Employees could

reach the goals.

3. a. The behavioral problems that could arise for Jensen Corporation

by having two different types of incentive plans for Hobbit Hole and

Cruise and Snooze Inns may be that unit managers may complain and

ask why their bonuses cannot be calculated like the other division’s. For

example, Hobbit Hole managers may request to be evaluated on items

other than just profitability.

b. The rationale that Jensen Corporation can give to the unit

managers of Hobbit Hole and Cruise and Snooze Inns to justify having

different incentive plans for the two divisions include the following:

• The goals of the two businesses may be different, and therefore

should be measured on different criteria in order to maintain goal

• The two divisions may have different incentive plans that are each an

accepted practice in their own industry.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–39

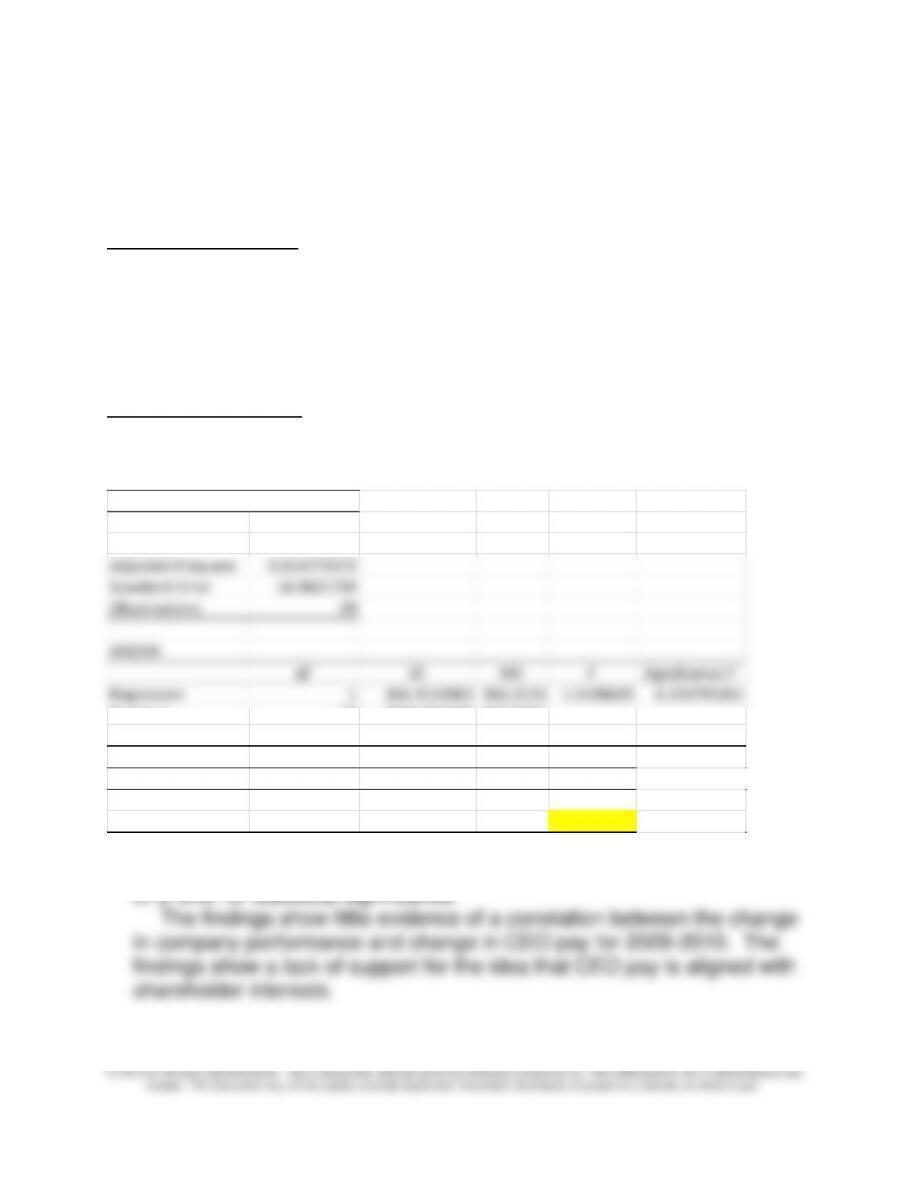

20-43 Compensation; Regression Analysis (40 min)

The results are shown below:

Correlation Analysis:

Correlation between executive pay and company performance is .223518

which is not statistically significant at the .10 level. While the direction of

the correlation is in the expected positive direction, there is no indication

from this data that there is a significant relationship between pay and

performance.

Regression Analysis:

A regression analysis with company performance (measured by stock

return) as the dependent variable and CEO pay as the independent

variable produce the following results:

Regression Statistics

Multiple R 0.223517854

R Square 0.049960231

Adjusted R Square 0.014773573

Standard Error 16.0621739

Observations 29

ANOVA

df SS MS F Significance F

Regression 1 366.3153062 366.3153 1.4198629 0.243795201

Residual 27 6965.822625 257.9934

Total 28 7332.137931

Coefficients Standard Error t Stat P-value

L

Intercept 19.17308552 3.422222448 5.602525 6.066E-06

Compensation 0.05103919 0.042833204 1.19158 0.24380

The above regression results confirm the correlation results shown

above. The p-value for the compensation variable is .2438, well short

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–40

Source: Pradnya Joshi, A Rich Year and More to Come,” The New York

Times, April 10, 2011, p. B7.

20-44 Compensation; Regression Analysis (20 min)

1. Given the available information, the most reliable regression appears to

be regression one, as it has the highest R squared. Regression three is

next best, and regression two is poor, an R squared of only 11%

2. The regressions have some common patterns:

• return on assets (ROA) is not a significant predictor of CEO pay for

any of the dependent variables.

• stock price volatility is significant at the lower level of reliability (.05) in

consistent with the expectation that lower levels of ownership require

stronger incentives, and thus higher CEO pay.

There are mixed results for the remaining variables, passenger load,

CEO tenure, and book to market value. These variables are not

significant in at least one of the regressions, indicating there is

potentially some relationship there but the nature of the relationship

depends on the dependent variable chosen, and that further analysis

would be necessary to understand the nature of the relationships

between these variables and CEO pay.

3. The principal goal of the study was to identify a potential relationship

between non-financial performance, as measured by passenger load, and

note that since many of the carriers included in the study were in financial

20–41

20–44 (continued -1)

distress at the time of the study, the presence of this distress may have

influenced the overall results.

4. The answers here could vary widely. One observation is that the

information is applicable only to the airline industry, and the results might

not be generalizable to other industries. Clearly the results indicate that

464.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-42

20-45 Business Analysis (45 min)

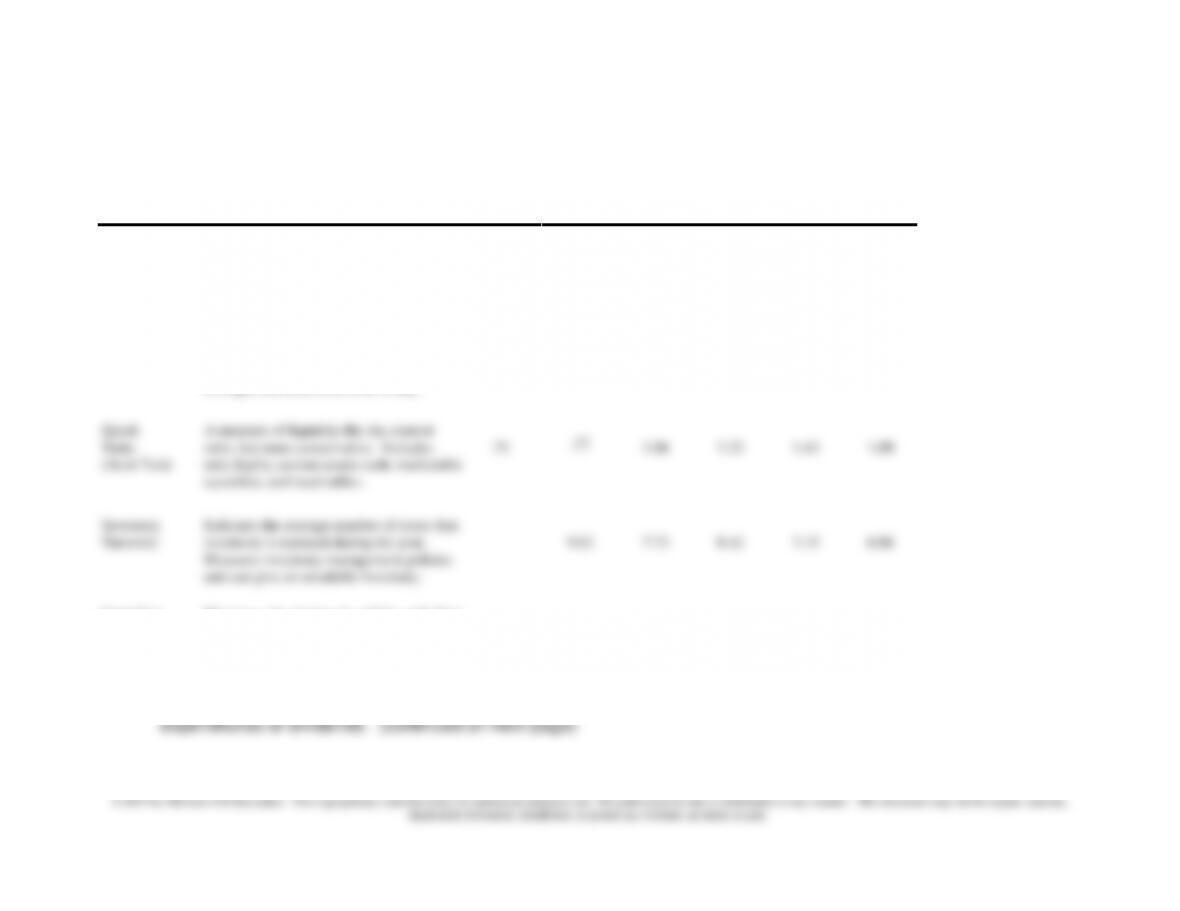

The following shows the ratios and an interpretation for each ratio.

a. Liquidity

Ratios

Relevance

2008

2009

2010

2011

2012

2013

A/R

Turnover

The average number of times per yr. net

receivables turn into cash. Indicates

effectiveness of credit policy and

collections. Should be compared to prior

years and to industry averages.

7.48

7.44

8.09

6.92

7.88

Current

Ratio

An important measure of liquidity. Should

be compared to prior years, industry

averages and debt restriction, if any.

1.01

1.23

1.66

1.92

2.23

1.90

Quick

Ratio

(Acid Test)

A measure of liquidity like the current

ratio, but more conservative. Includes

only highly current assets-cash, marketable

securities, and receivables.

.71

.77

1.06

1.23

1.43

1.09

Inventory

Turnover

Indicates the average number of times that

inventory is replaced during the year.

Measures inventory management policies

and can give an unsalable inventory.

9.62

7.73

8.42

7.15

6.86

Cash flow

ratio

Measures the degree to which cash flow

from operations covers the amount of

current liabilities

.11

.25

.61

.42

.53

Note: The free cash flow ratio is not calculated because information is not provided in the problem re: capital