Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-31

5-42 (continued-1)

Calculation for general administration allocated to branches:

Total direct labor dollar: $382,413 + $317,086 + $317,188 = $1,016,687

Allocation of general administration based on direct labor dollar:

Proportion Allocated Amount

2. Contribution of each branch:

Columbus

Cincinnati

Dayton

Total

Sales

$1,500

$1,419

$1,067

$3,986

Less: Direct labor

382

317

317

1,016

Direct materials

281

421

185

887

Direct overhead

180

270

177

627

Contribution margin

$657

$411

$388

$1,456

3. Profitability of each branch using activity-based costing:

Columbus

Cincinnati

Dayton

Total

Sales

$1,500

$1,419

$1,067

$3,986

Less: Direct labor

382

317

317

1,016

Direct materials

281

421

185

887

Direct overhead

180

270

177

627

Contribution margin

$657

$411

$388

$1,456

Activity-based overhead

529

453

278

1,261

Operating income

$128

($42)

$110

$195

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-32

5-42 (continued-2)

4. Evaluating management concerns:

Overhead costs are usually aggregated in pools and allocated to

products and other cost objects based on volume measures such as

direct labor dollars or machine hours. The cost object, therefore,

supposedly shares proportionally in those costs necessary for its

production or existence. If however, overhead varies in accordance with

addition, existing marketing strategy may be promoting the wrong

location and strategic planning may be based on spurious assumptions

concerning relative profitability.

This case also illustrates that ABC is applicable to service organizations

as well as to manufacturing and that cost objects can consist of projects,

locations, customers, etc., as well as products. In essence, the better

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-33

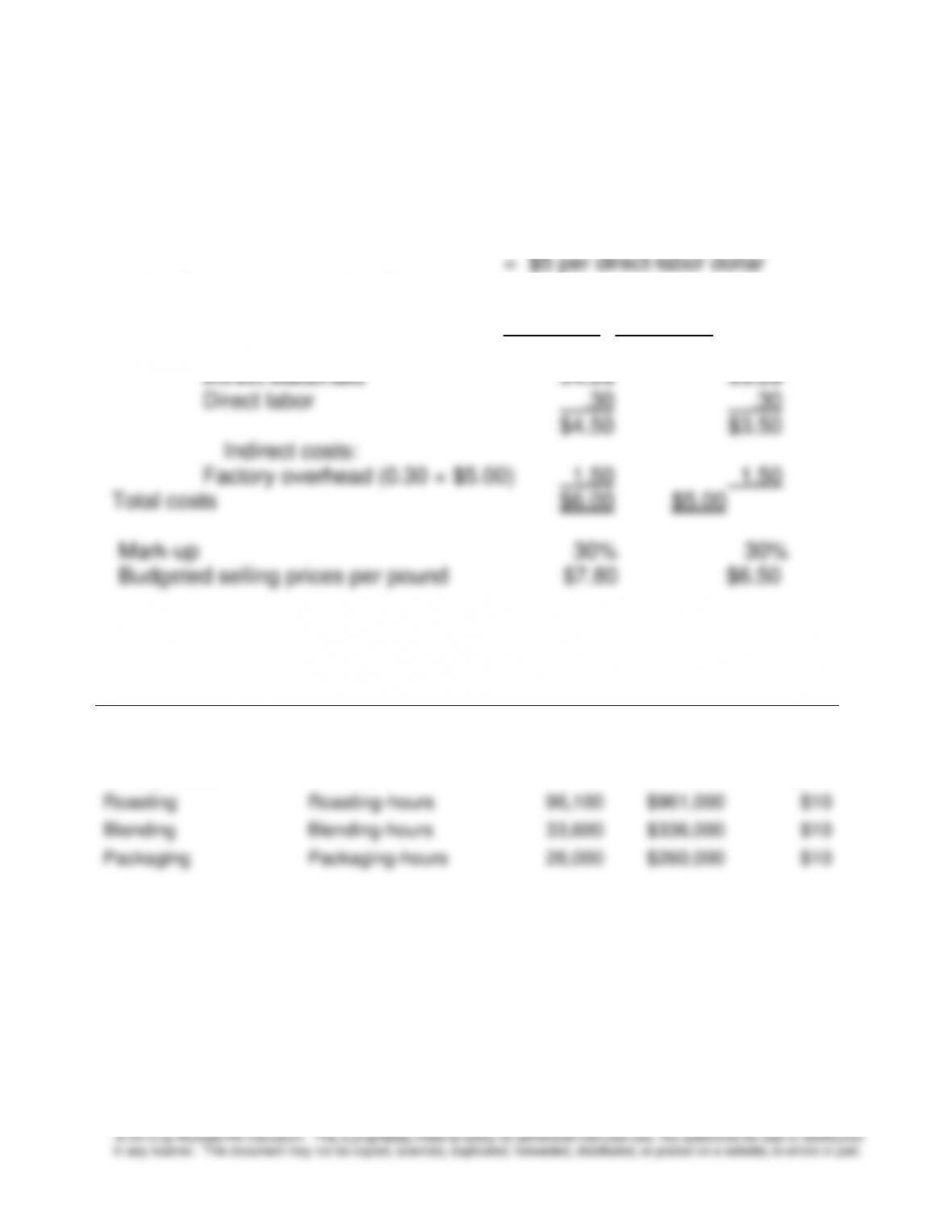

5-43 Volume-based Costing Versus ABC (40 min)

1. a. Predetermined factory overhead rate = $3,000,000 ÷ $600,000

= $5 per direct-labor dollar

b. Product costs and selling prices

Product Costs Mona Loa Malaysian

Direct costs:

2. The cost per driver unit is:

Activity

Cost Driver

Budgeted

Activity

Budgeted

Cost

Cost per

Unit

Purchasing

Purchase orders

1,158

$579,000

$500

Materials handling

Setups

1,800

$720,000

$400

Quality control

Batches

720

$144,000

$200

Roasting

Roasting-hours

96,100

$961,000

$10

Blending

Blending-hours

33,600

$336,000

$10

Packaging

Packaging-hours

26,000

$260,000

$10

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-34

5-43 (continued-1)

The budgeted unit costs per pound are:

Mona Loa Coffee Malaysian Coffee

Direct unit costs:

Direct materials $4.20 $3.20

Direct labor 0.30 $4.50 0.30 $3.50

Indirect unit costs:

Purchasing 0.02 1.00

(4 orders × $500 ÷ 100,000 lbs.) (4 orders × $500 ÷ 2,000 lbs.)

Material handling 0.12 2.40

(30 setups × $400 ÷ 100,000 lbs.) (12 setups × $400 ÷ 2,000 lbs.)

Quality control 0.02 0.40

The comparative cost numbers are:

Mona Loa

Malaysian

Requirement 1

$6.00

$5.00

Requirement 2

4.82

7.46

The ABC system in requirement 2 reports a decreased cost for the high–

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-35

5-43 (continued-2)

3. Three of the indirect cost items can be classified as output-unit driven:

Mona Loa

Coffee

Malaysian

Coffee

Roasting

$0.10

$0.10

Blending

0.05

0.05

Packaging

0.01

0.01

Total output-unit overhead

$0.16

$0.16

The other three indirect cost items are batch-level driven:

Mona Loa

Coffee

Malaysian

Coffee

Purchasing

$0.02

$1.00

Material handling

0.12

2.40

Quality control

0.02

0.40

Total batch-level overhead

$0.16

$3.80

Malaysian coffee has a greater number of setups per output unit than

does Mona Loa coffee. The result is that the unit cost of the lower–

volume Malaysian coffee is much higher than that of the higher-volume

coffee, even though its cost of direct materials is lower.

With the current costing system, the high-volume Mona Loa is

overcosted, while the low-volume Malaysian is undercosted. Pricing of

Mona Loa can be reduced to make it more competitive. In contrast,

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-36

5-43 (continued-3)

ABC cost data also point out that the reason for the Malaysian

coffee to have a higher unit cost is not because of high-priced

ingredients. In fact, Malaysian coffee has a lower cost of direct

materials than that of Mona Loa coffee. The costs of roasting,

5-44 Cost of Capacity; Continuation of 5-43 (25 min)

1. The calculation of the new activity rates and the cost of unused capacity is

determined below.

Activity

Budgeted

Activity

Budgeted

Cost

Usage

Based

Rate

Practical

Capacity at

current

spending

Usage

%

Practical

Capacity

Rate

Unused

Capacity

Cost of

Unused

Capacity

Purchasing

1,158

$579,000

$500

1,400

83%

$413.57

242

$100,084

Materials

handling

1,800

$720,000

$400

2,400

75%

$300.00

600

$180,000

Quality

control

720

$144,000

$200

1,200

60%

$120.00

480

$57,600

Roasting

96,100

$961,000

$10

100,000

96%

$9.61

3,900

$37,479

Blending

33,600

$336,000

$10

36,000

93%

$9.33

2,400

$22,400

Packaging

26,000

$260,000

$10

30,000

87%

$8.67

4,000

$34,667

$3,000,000

$432,230

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-37

2. The information on cost of capacity can alert management to the total cost

of unused capacity, in this case $432,230 or approximately 14% of total

overhead cost. This information can be used to identify activities where there

3. The analysis below shows the number of employees “unused” in column

4. The analysis assumes that each employee (or machine) contributes an

equal share to the work of the activity. Note that the materials handling

activity appears to have as many as 5 unused employees.

1

2

3

4

5

6

7

8

Driver

Usage

Cost

Capacity

at Current

Spending

Step:

Number of

Employees

or Machines

Unused

Capacity

Cost per Step

=(2)÷(4)

Step Size

=(3)÷(4)

Steps

Not

Used

Purchasing

1,158

$579,000

1,400

8

242

$ 72,375

175

1.38

Materials

Handling

1,800

720,000

2,400

20

600

36,000

120

5.00

Quality

Control

720

144,000

1,200

4

480

36,000

300

1.60

Roasting

96,100

961,000

100,000

10

3,900

96,100

10,000

0.39

Blending

33,000

336,000

36,000

10

3,000

33,600

3,600

0.83

Packaging

26,000

260,000

30,000

3

4,000

86,667

10,000

0.40

5-45 Ethics, Cost System Selection (5 min)

Unfortunately, there are a number of reasons why ABC costing systems are

studied by firms and then not adopted. In some cases the reason is to protect

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-38

In the case of Aero Dynamics, the reason has to do with an ethical issue, that

is, the use of cost allocation to improperly charge a cost-plus customer (the

federal government) for overhead costs. The management accountant should

keep the professional ethics code in mind. First, he or she should try to

persuade other ABC pilot project members and the company controller to

strongly recommend that top management adopt the more accurate ABC

method. If the company top management still would not listen, then the

management accountant should report the situation to the company’s audit

committee. Because of the management accountant’s responsibility for

confidentiality, he or she should not report the matter outside the firm. (See

the Institute of Management Accountant’s Code of Ethics in Exhibit 1-10).

An interesting footnote to the case is that the Government Accounting Office,

to assist the Dept of Defense, in part due to issues of this nature, developed in

the 1970s a series of cost accounting standards. These standards apply

generally to companies contracting with the federal government, especially the

DOD. See http://www.gao.gov/casb1.htm for the CASB website. Also, the

Federal Government in 1990 created the Federal Accounting Standards

Advisory Board (www.fasab.gov) which sets standards for financial and

managerial reporting within the federal government. The FASAB web site is

an interesting place to see the progress/continuing issues of accounting at the

federal government.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-39

5-46 Time-Driven Activity-Based Costing (TDABC) in a Call Center

(20min)

1. The TDABC rate per minute for MSI is determined as follows:

Total Projected Costs ÷ Practical Capacity

2. The total time for each type of loan is determined as follows:

Total Calls

Answered

Avg. No. of

Minutes/C

all

Total Time (minutes)

Inquiries

Autos

Trucks

Inquire re: Rates and Terms

Autos

96,000

5

480,000

Trucks

32,000

7

224,000

Inquire re: Loan App Status

Autos

37,500

6

225,000

Trucks

6,750

11

74,250

Inquire re: Payment Status

Autos

39,000

3

117,000

Trucks

12,000

4

48,000

Inquire re: Other Matter

Autos

29,000

11

319,000

Trucks

8,500

15

127,500

Total

1,141,000

473,750

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-40

5-46 (continued)

The revised proposal would show:

Cost for Autos (1,141,000 x $.78)

$889,980

Cost for Trucks (473,750 x $.78)

$369,525

Total Cost

$1,259,505

Time markup

1.25

Total Charge for Engagement

$1,574,381

Note: For further information on TDABC and call centers, see Robert S.

Kaplan and Steven R. Anderson, Time-Driven Activity-Based Costing, Harvard

Business School Press, 2007; and Bilbert Y. Uang and Roger C Wu,

“Strategic Costing & ABC,” Management Accounting, May 1993, pp 33-37.

5-41

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution

in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

5-47 TDABC; Continuation of Problem 5-46 (20 min)

1. The amount of unused capacity is determined as follows.

Total Calls

Answered

Avg. No. of

Minutes/Call

Total

Platinum Regional Bank

234,000

6.0

1,404,000

Healthwise Software Inc.

66,788

5.0

333,940

Johnson Manufacturing

122,665

4.0

490,660

Lesco Online Shopping

233,756

6.0

1,402,536

Babcock Insurance Service

55,455

5.5

305,003

Garcia Electric Supply and Service

38,956

3.4

132,450

Gilbert’s Online Garden Supplies

145,902

4.0

583,608

Financial Planning Services Inc.

68,993

11.0

758,923

Porter’s Camera and Optical

198,440

6.0

1,190,640

Jordan Auto World Inc.

965,887

3.0

2,897,661

Total

9,499,421

Unused Capacity

2,545,579

Call Center Practical Capacity

12,045,000

Total minutes used with the AS engagement (9,499,421

+ 1,614,750)

11,114,171

Unused capacity with the AS engagement

930,829

which would reduce unused capacity to 7.7%, a substantial improvement.

Also, it points to the need to examine staffing levels to bring down the cost of

unused capacity. Alternatively, MSI can use the unused time to provide staff

training in order to improve their performance and to make MSI’s services

more attractive to other potential clients.