Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-1

CHAPTER 15: OPERATIONAL PERFORMANCE MEASUREMENT:

INDIRECT-COST VARIANCES AND RESOURCE-CAPACITY

MANAGEMENT

QUESTIONS

15-1 The total factory overhead can be the same as the standard amount allowed for the

current period’s output while one or more of the components of the total factory

overhead have significant variances. For example, a firm can have a substantial

unfavorable overhead flexible-budget variance of a period may continue into the

future with the consequence that the organization continues to suffer from

unfavorable flexible-budget variances.

15-2 This question pertains to text Exhibits 15.1 and 15.3. As indicated in Exhibit 15.1, the

amount of variable overhead applied to production for a period (product-costing

purpose) is exactly equal to the amount of variable overhead in the flexible budget

15-3 Possible contributing factors to a variable overhead spending variance include:

▪ Prices paid to acquire one or more variable overhead items differ from those

specified as standard prices.

overhead.

15-4 Because an alternative activity measure usually is used as the basis for applying

manufacturing overhead to production, a variable overhead efficiency variance can

variable overhead cost of efficiency or inefficiency in the use of the activity measure

used to construct the flexible-budget.

15-5 A fixed overhead spending variance is defined as the difference between the actual

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-2

example:

▪ A factory manager was given a bonus or raise that was not in the original

budget.

▪ Additional salaried employees, not envisioned when the original budget was

prepared, were added during the period.

15-6 A production volume variance results when actual output differs from the output level

assumed when the fixed overhead application rate was developed. Among reasons

for this discrepancy are:

▪ Unexpected stoppage or slowdown of operations because of unscheduled

equipment maintenance, strike, or workers’ slow-down.

▪ Choice of denominator activity level (e.g., if budgeted activity, rather than

practical capacity, is used, the amount of the production volume variance will

likely be smaller—in the extreme, it would be zero).

15-7 Even though the denominator level a firm selected determined the fixed overhead

application rate, the selected denominator level has no effect on either the amount

or the direction of the fixed overhead flexible-budget variance for the operation. The

the production volume variance is directly a function of the selected denominator

level assumed when the application rate was developed. A high denominator level

increases an otherwise unfavorable production volume variance (or decreases an

otherwise favorable volume variance). On the other hand, a low denominator level

increases an otherwise favorable production volume variance (or decreases an

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-3

otherwise unfavorable production volume variance).

15-8 The “denominator activity level” refers to the size of the denominator when

determining the standard fixed overhead application rate for product-costing

purposes. Various options for the volume of the denominator are possible, including

budgeted volume, practical capacity, and theoretical capacity. Most writers today

recommend the use of practical capacity for at least two reasons:

▪ Logical consistency between the numerator and denominator in the

(i.e., overhead items).

15-9 Among reasons that a firm may use a 2-variance instead of 3-variance or 4-variance

analysis of overhead variances are:

▪ Information provided by the simpler 2-variance analysis is thought to meet the

needs of management, that is, the information is thought to be “good

analysis.

▪ A more detailed analysis confuses users of accounting reports.

▪ Total overhead costs are not significant in a relative sense

However, as indicated in Exhibit 15.3, the amount of fixed overhead in the flexible

budget is likely to be different from the amount of fixed overhead assigned to

production for the period. The flexible budget for fixed overhead includes a “lump–

the period. In short, when dealing with fixed overhead, the (“lump–sum”) amount

used for control purposes and the amount applied to production will be identical only

if the actual output of the period exactly equals the denominator activity level.

15–10 If a standard cost system is used, variances related to overhead costs can be

recorded formally in the accounting records. Such variances, however, are

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-4

considered “temporary accounts,” which at the end of the year must be closed out.

There are two primary methods for doing this at the end of the year:

(1) Closing the net variance to cost of goods sold (for example, if the net

overhead variance is favorable, then the CGS account would be decreased,

that is credited, at the end of the year). This practice can be defended for

several reasons. One, it is the most expedient (and therefore least costly)

standard overhead costs contained in the end–of-period balance in these

accounts. Note that when we expand the analysis to include direct materials,

any price variance that occurs during the period should be allocated to the

materials inventory account, the materials quantity (efficiency) variance, the

WIP Inventory account, the Finished Goods Inventory account, and CGS.

Similarly, any fixed overhead spending variance should, in theory, be partially

allocated to the production volume variance for the period. The proration

a different end-of-year allocation of the net manufacturing cost variance for the

year compared to the conceptually correct method noted above.

We note here that both financial reporting and income tax considerations are

associated with the end-of-period variance disposition question:

(1) For external reporting purposes, accountants need to follow the provisions of

generally accepted accounting principles (FASB ASC 330–10–30-6 and -7,

www.fasb.org, which specify that abnormal amounts of idle facility expense

should be recognized as current-period charges and not capitalized as part of

inventory cost. One implication of this reporting requirement is that the amount of

fixed overhead allocated to each unit of production is not increased as a

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-5

consequence of abnormally low production or an idle plant.

result in “reasonable” allocations across outputs. Additional guidance for income–

tax purposes regarding the use of alternative denominator-volume levels for

determining income under the absorption-costing approach is given in Treasury

Regulation § 1.471-11: Inventories of Manufacturers.

15–11 For external reporting purposes, accountants need to follow the provisions of

generally accepted accounting principles (FASB ASC 330–10–30 -6 and -7,

previously, Statement of Financial Standards No. 151:Inventory Costs—An

Amendment of ARB No. 43, Chapter 4, available at www.fasb.org) regarding the

setting of overhead allocation rates and the end–of-period disposition of any volume

15–12 Factors that need be considered include:

15–13 Any significant variance, be it favorable or unfavorable, should be investigated. It

might be argued that significant favorable variances should not be investigated since

such variances serve to increase operating income for the period. Nonetheless, an

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-6

BRIEF EXERCISES

15–14 The budgeted supervisory salary per month is:

$360,000 ÷ 12 months = $30,000 per month

Thus, the flexible-budget variance for the production supervisory salaries in

August is:

15–15 Standard indirect labor cost per unit:

= $144,000/year ÷ (5,000 units/month × 12 months/year)

= $2.40/unit

15–16 Fixed overhead variances for the year:

(a) Spending Variance = Actual fixed overhead costs – Budgeted fixed overhead

= $245,000–$250,000 = $5,000F

(b) Production Volume Variance = Budgeted fixed overhead – Applied fixed

overhead

= $250,000 – (20,000 units × 2 hrs./unit × $5/hr.)

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-7

15–17 Variable overhead variances for the year:

(a) Spending variance = Actual variable overhead − Flexible budget based on

Inputs

= ($3.90/unit × 20,000 units) − (41,000 hours. × $2.00/hr.)

(b) Efficiency variance = Flexible-budget based on Inputs– Flexible budget based

on output

= $82,000 − (20,000 units × 2 hrs./unit × $2.00/hr.)

= $82,000 − $80,000

15–18 Summary journal entries for the year:

Actual Overhead Costs:

Dr. Factory (or, Manufacturing) Overhead 323,000

Cr. Accumulated Depreciation—Factory 150,000

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-8

15–19 To Record Factory Overhead Variances:

Dr. Production Volume Variance 50,000

Dr. Variable Overhead Efficiency Variance 2,000

Cr. Variable Overhead Spending Variance 4,000

Cr. Fixed Overhead Spending Variance 5,000

Cr. Factory (or, Manufacturing) Overhead 43,000

To Close the Net Overhead Variance to CGS at Year-End:

Dr. CGS 43,000

Dr. Variable Overhead Spending Variance 4,000

Dr. Fixed Overhead Spending Variance 5,000

Cr. Production Volume Variance 50,000

Cr. Variable Overhead Efficiency Variance 2,000

15–20 To Allocate the Net Factory Overhead Variance at Year-End

Dr. WIP Inventory (10% of $43,000) 4,300

Dr. Finished Goods Inventory (20% of $43,000) 8,600

Dr. CGS (70% × $43,000) 30,100

15–21 Factory Overhead Variance: Two-Variance Decomposition

(a) Total Overhead Variance = actual overhead − overhead applied to production

= $323,000 − (20,000 units × 2 hrs./unit × $7.00/hr.)

= $323,000 − $280,000

= $43,000U

(b) Total Flexible-Budget Variance = Actual overhead – Flexible-budget for

Overhead based on Output

= $323,000 − [($2/hr.× 2hrs./unit × 20,000 units) +

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15-9

15–21 (Continued)

(c) Production Volume variance = budgeted fixed overhead − applied fixed

overhead

= $250,000 − (20,000 units × 2 hrs./unit × $5.00/hr.)

$50,000 during the year)

15–22 Summary Journal Entries:

(a) Actual Overhead Costs

Dr. Factory (or, Manufacturing) Overhead 323,000

Cr. Accumulated Depreciation—Factory 150,000

Cr. Salaries Payable 95,000

(b) To Record Overhead Variances Using a Two-Variance Approach:

Dr. Production Volume Variance 50,000

15–23 End-of-Year Journal Entry to Close Out Variance Accounts:

(a) Net Variance Closed to CGS:

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–10

(b) Net Variance Allocated to Ending Inventories and CGS:

Dr. WIP Inventory (10% × $43,000) 4,300

Dr. Finished Goods Inventory (20% × $43,000) 8,600

EXERCISES

15–24 Flexible Overhead Budgets for Control; Spreadsheet Application (40–45

minutes)

Note: An Excel spreadsheet solution file for this assignment is embedded below. You

can open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

this Word document.

Ex. 15-24.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–11

15–25 Journal Entries for Factory Overhead Costs and Standard Cost Variances;

Spreadsheet Application (50–60 minutes)

Note: An Excel spreadsheet solution file for this assignment is embedded below. You

can open this “object” by doing the following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

this Word document.

Ex. 15-25.xlsx

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–12

15–26 Graphical Analysis—Variable Overhead Variances (20–25 minutes)

Solution:

(A) = Variable Overhead Costs per Machine Hour (label)

(B) = Machine Hours (i.e., the activity measure used to apply variable overhead

(G) = Variable overhead spending variance = AQ × (AP − SP)

(H) = Standard variable overhead cost applied to production = Flexible budget for

variable overhead based on units produced (i.e., based on standard allowed

machine hours) = SQ × SP

(B)

(A)

(C)

(D)

(E)

(F)

Area (G)

Area (H)

Area (I)

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–13

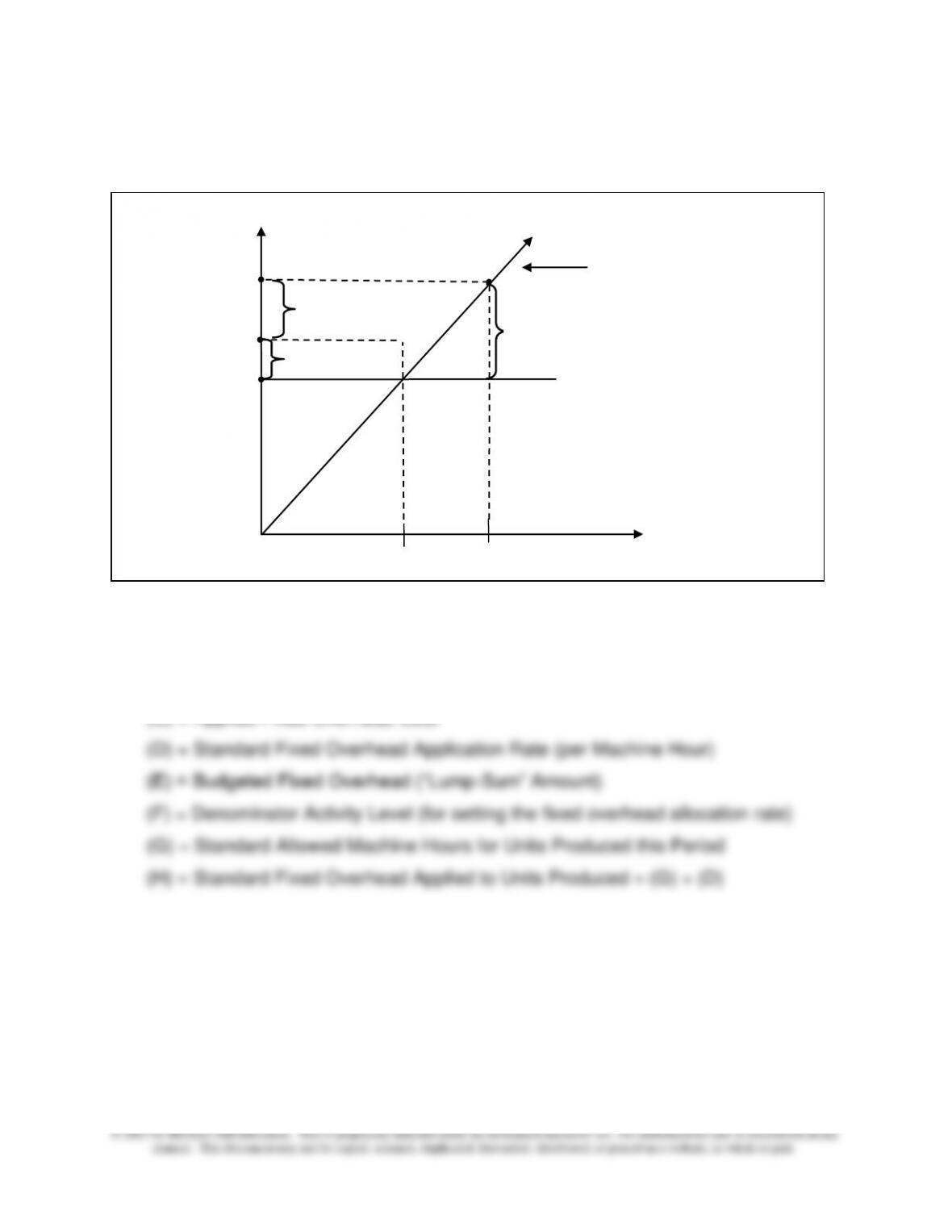

15–27 Graphical Analysis—Fixed Overhead Variances (30–40 minutes)

Solution:

(A) = Fixed Overhead Cost (label)

(B) = Machine Hours = Activity Measure for Applying Fixed Overhead Cost (label)

(C) = Applied Fixed Overhead Cost

(I) = Actual Fixed Overhead Costs Incurred During the Period

(J) = Fixed Overhead Production Volume Variance (= D × (G − F))

(K) = Total Fixed Overhead Variance = (J) + (L)

(L) = Fixed Overhead Spending (Budget) Variance = (I) − (E)

(L)

(K)

(I)

(H)

(A)

(C)

(B)

(F) (G)

Slope of Line = (D)

(E)

(J)

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–14

15–28 Flexible Budget and Variances for Depreciation (20 minutes)

1. Budgeted depreciation, factory equipment for September:

$360,000 12 = $30,000

2. Spending Variance—Equipment Depreciation Expense:

Actual depreciation for the month $28,000

3. Production Volume Variance—Portion Pertaining to Depreciation:

Budgeted depreciation for the month $30,000

Total standard depreciation expense applied:

Total chargeable hours for the month = 9,000

Interpretation: Because chargeable hours (i.e., “activity” or “volume”) were less

than anticipated, a portion of the budgeted depreciation expense for equipment

did not get charged to the output of the period.

4. Reasons for the favorable spending variance regarding equipment depreciation

expense include:

▪ The company disposed of some of its equipment during the period

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–15

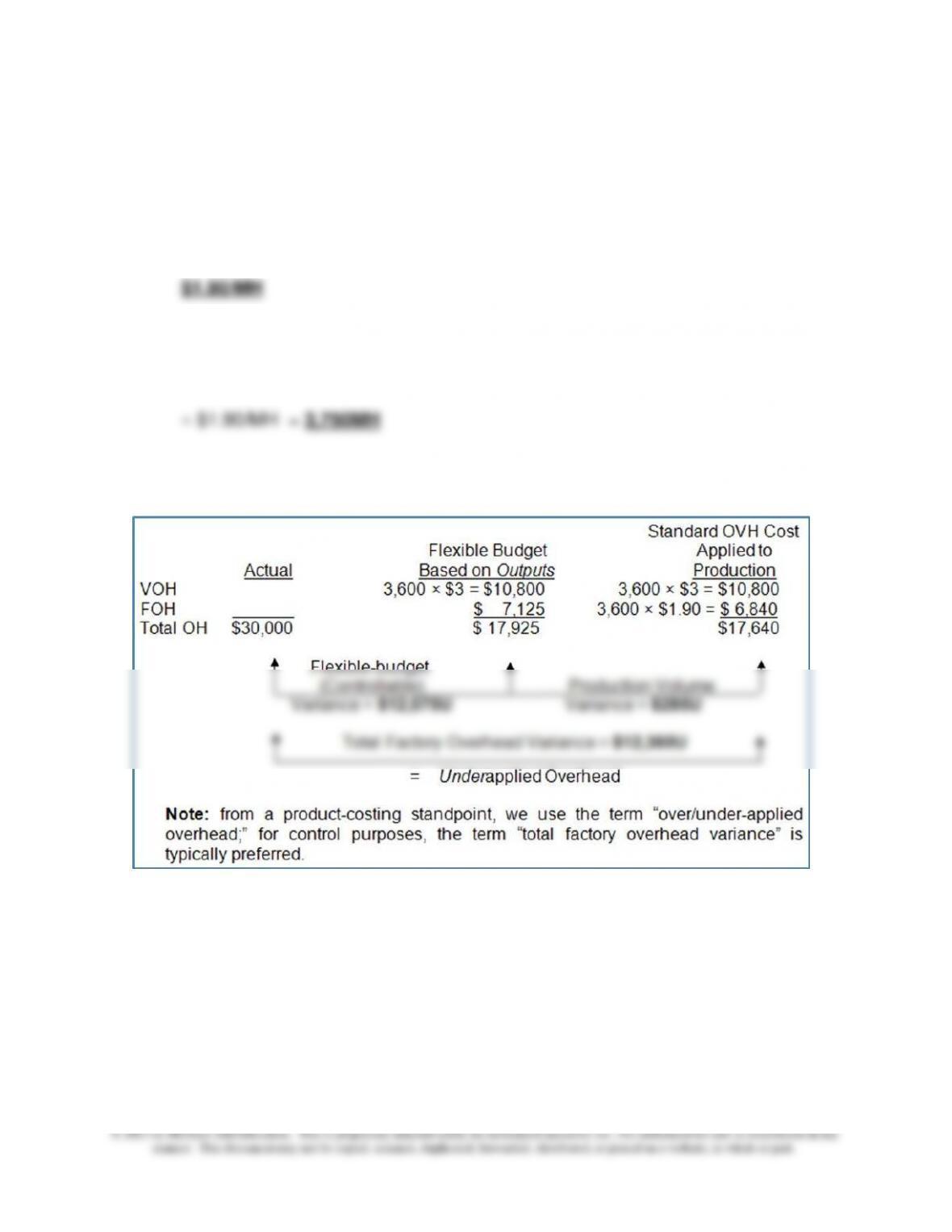

15–29 Fixed Overhead Rate, Denominator Level, and 2-Variance Analysis of Fixed

Overhead Variance (20-25 minutes)

1. Standard fixed factory overhead rate = budgeted total overhead cost per machine

hour − budgeted variable overhead cost per machine hour = $4.90 − $3.00 =

2. Denominator activity level (used to set the standard fixed overhead allocation rate)

= Budgeted Fixed OverheadFixed Overhead Allocation Rate per MH = $7,125

3. Two-Way Analysis (Breakdown) of Total Overhead Variance