Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–16

benefit.

Cumulative Goodwill Amortization. Goodwill arises when the acquisition of another firm is

recorded as a purchase and there is an excess of cost over the fair value of the net assets acquired. The

amount of the goodwill recorded can be amortized against earnings over a period not to exceed 40 years.

To make this non-cash, non-tax-deductible item the non-issue it really is, the amortized amount should be

added back to reported earnings. And, to be consistent, the cumulative goodwill that has been amortized

must be added back to equity capital and to goodwill remaining on the books. By un-amortizing goodwill

in this way, the rate of return will properly reflect the true cash-on-cash yield that is of interest to

shareholders. Action(s) to be taken:

Add to Capital: Amount of the cumulative goodwill amortization

Add to NOPAT: The amount of increase in goodwill amortization

An Overview of the Process Involved in Calculating EVA

The solution of the OSI case is in the attached Exhibits that have been prepared for OSI (TN-1

through TN-3).

The following is a list of the steps to be completed in calculating OSI’s EVA amounts:

1. Obtain a Balance Sheet and Income Statement for 2013

2. Obtain the footnotes to those financial statements;

3. Analyze the footnotes for information on equity equivalent adjustments;

4. Obtain information on the firm’s stock, debt and interest rates;

5. Determine equity equivalent adjustment amounts by analyzing the footnotes;

6. Calculate the firm’s weighted average cost of capital;

7. Prepare worksheets of EVA statements

8. Prepare final statements of EVA showing amounts calculated for RONA (Return on Net

Assets), and EVA

Calculating EVA

EVA calculations for OSI in 2013 using the Financing Approach are detailed in Exhibit TN-3.

Refer to Exhibits TN-1 and TN-2 for relevant information on the WACC and the equity equivalent

adjustment amounts involved in these calculations.

Note: This case situation focused primarily on EVA, but other valuation-based performance

metrics exist such as NPV, CFROI, and RI. CFROI (cash flow return on investment) is a rate of return

measure calculated by dividing inflation-adjusted cash flow from the investment by the inflation-adjusted

amount of the cash investment. While CFROI does adjust for inflation, it fails to account for risk and the

appropriate required return on the project. In a sense, CFROI is similar to the internal rate of return (IRR)

⎯ after including the EE adjustments, hence it measures the investment’s return as opposed to the wealth

created or destroyed by the investment.

2. Benefits / Advantages and Disadvantages of EVA

All managers basically have the same objective ⎯ putting scarce capital to its most promising

uses. To increase their company’s stock price, managers must perform better than those with whom they

compete for capital. Then, once they get the capital, they must earn rates of return on it that exceed the

return offered by other, equally risky seekers of capital funds. If they accomplish this, value will have

been added to the capital their firm’s investors placed at their disposal. If they don’t accomplish that goal,

there will be a misallocation of capital, and the company’s stock will sell at a price that discounts the sum

total of the resources employed.

EVA is a financial management system that is well adapted to this kind of a situation since it

focuses on creating shareholder value. In using the system, managers and employees focus on how capital

is used and on the cash flow generated from it. It runs counter to the notion that long-term stock

appreciation comes from earnings.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–17

Focusing on EVA growth provides two benefits: 1) management’s attention is focused more

toward its primary responsibility ⎯ increasing investor wealth; and, 2) distortions caused by using

historical cost accounting data are reduced, or eliminated. As a result, managers spend their time finding

ways to increase EVA rather than debating the intricacies of the fluctuations in the earnings reported in

their traditional accounting statements.

EVA measures the amount of value a firm creates during a defined period through operating

decisions it makes to increase margins, improve working capital management, efficiently using its

production facilities, redeploying underutilized assets, etc. Thus, EVA can be used to hold management

accountable for all economic outlays, whether they appear in the income statement, on the balance sheet

or in the financial statement‘s footnotes. EVA creates one financial statement that includes all the costs of

being in business, including the carrying cost of capital. The EVA financial statement gives managers a

complete picture of the connections among capital, margin and EVA. It makes managers conscious of

every dollar they spend, whether that dollar is spent on or off the income statement, or on operating costs

or the carrying cost of working capital and fixed assets.

Another very subtle benefit for a firm that adopts EVA is that it creates a common language for

making decisions, especially long-term decisions, resolving budgeting issues, evaluating the performance

of its organizational units and their managers, and measuring the value-creating potential of its strategic

options. An outgrowth of such an environment is that the quality of management also improves as

managers begin to think like owners and adopt a longer horizon view.

3. To this point, the emphasis has been on how focusing on EVA may help managers increase shareholder

wealth. However, for the metric to help in creating shareholder wealth, managers must behave in a

manner consistent with wealth creation. One powerful way to align managers’ interests with those of the

shareholders is to tie their compensation to output from the EVA metric. In fact, it is not just for

managers, but may be used for all employees. When implemented correctly, the basic notion of increasing

shareholder value will permeate the entire organization, and employees at all levels will then begin to act

in concert with upper levels of management.

Implementing an EVA-based incentive plan is fundamentally a process of empowerment ⎯

getting employees to be entrepreneurial, to think and act as owners, getting them to run the business as if

they owned it, and giving them a stake in the results they achieve.

The overall, firm-wide objective is to generate a persistent increase in EVA. To achieve that,

employees must understand the role they play in increasing a firm’s EVA. A key factor in sustaining a

continuing interest in EVA and in making it work is to revise the compensation system to focus on

creating value. It has been shown that one of the critical components in successfully using EVA to

improve a company’s MVA is tying it to bonuses and pay schemes. Designing an incentive compensation

system that pays people for sustainable improvements in EVA, in concert with an understanding of what

drives EVA, and what drives economic returns, is what transforms behavior within a company.

A good way to get started quickly is to increase insider ownership of the firm’s stock. One way to

do this is to turn old profit-sharing plans into employee stock-ownership plans.

If an incentive system is to work, it must have certain distinctive properties:

1. An objective measure of performance, which cannot be manipulated by one of the parties who

may benefit. For example, in many existing plans, the budget is a commonly used target for

performance, but the manager being evaluated is usually heavily involved in negotiating that

budget.

2. It must be simple so that even employees far down in the organization will understand how EVA

is tied to economic value and can follow it well.

3. Bonus amounts have to be significant enough in amount for employees to alter their behaviors.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–18

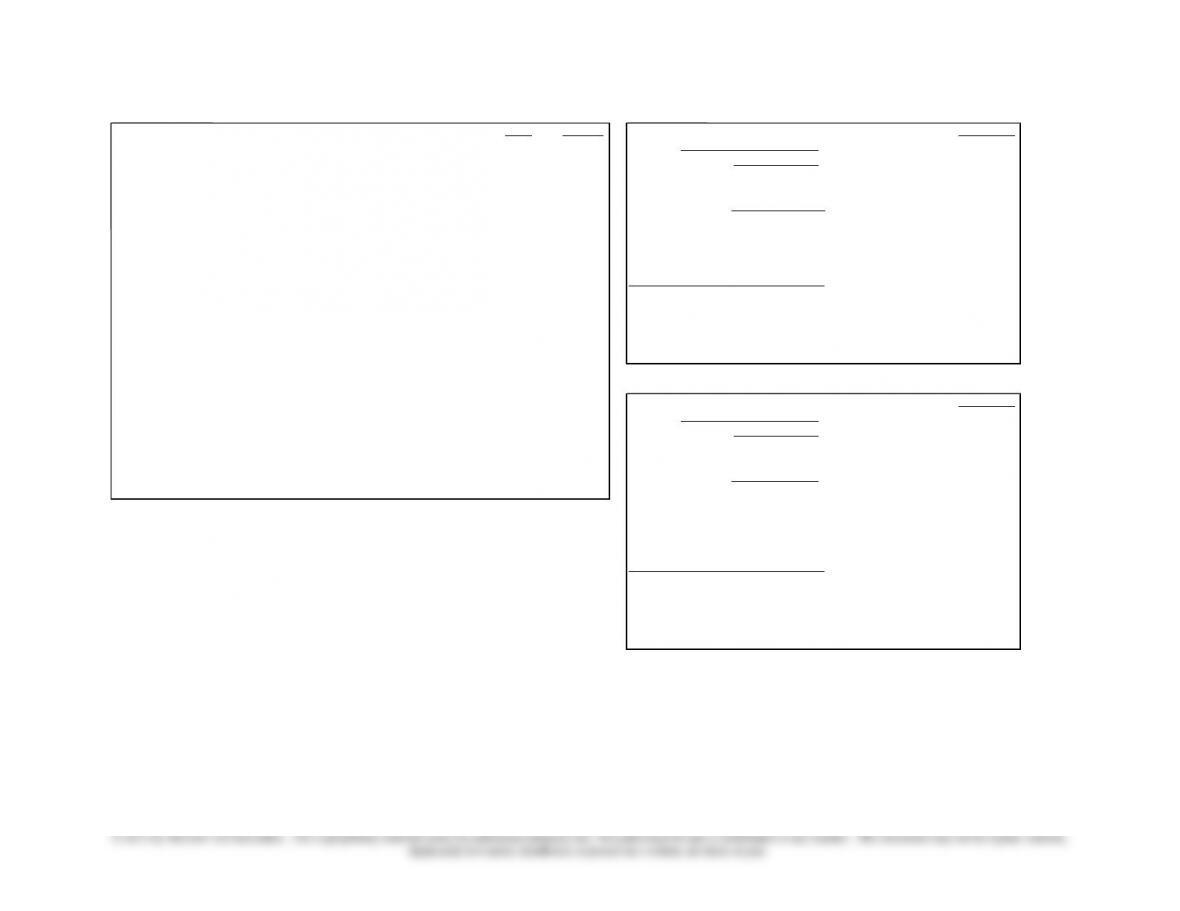

Exhibit TN-1

Financial Data Input and Calculation of Interest Rates/Expense:

Calculate Weighted Ave. Cost of Capital – Based on Market:

Rate

Interest

Weights:

Pct of Total

Short-term Debt:

$8,889

8.00%

$711

Long-term Note Payable

$117,155

17.8%

Long-term Debt: Current portion

$18,411

10.00%

$1,841

Preferred Stock

Long-term Debt: Long-term portion

$98,744

10.00%

$9,874

Shares o/s

1,000

$117,155

Interest paid=

$12,427

Par value

$100

$100,000

15.2%

Common Stock

Risk-free rate (90 day T-bills)=

5.0%

Shares o/s

219,884

Return on the Market=

12.5%

Market value

$2.00

$439,768

66.9%

Beta Value of common stock=

1.2

———

Tax Rate=

35.0%

$656,923

Price per share of common stock=

$2.00

Weighted Average Cost of Capital

For Debt=

1.159%

Calculated Cost of Equity Capital:

14.0%

For Preferred Stock=

1.674%

Common stock dividend/share paid last year=

0.111

per share

Common Stock=

9.372%

Total common stock dividend paid last year=

$24,429

——-

Calculated current dividend yield (last year)=

5.555%

12.206%

Expected growth rate of dividends=

8.000%

Future dividend yield (next year)=

5.999%

Calculate Weighted Ave. Cost of Capital – Based on Book Value:

Common stk dividend/sh. expected-next year=

0.120

Weights:

Pct of Total

Total common stock dividend to pay next year=

$26,383

Long-term Note Payable

$117,155

22.1%

Check: Calculated Future dividend yield (next year)=

5.999%

Preferred Stock

Preferred stock dividend/share paid last year=

$11.00

per share

Shares o/s

1,000

Total preferred stock dividend paid last year=

$11,000

Par value

$100

$100,000

18.9%

Total preferred stock dividend for next year=

$11,000

Common Stock

Share Book Value

$219,884

Paid-in capital

$32,056

59.0%

Retained earnings

$61,125

$313,065

————

$530,220

Weighted Average Cost of Capital

For Debt=

1.436%

For Preferred Stock=

2.075%

Common Stock=

8.266%

——-

11.777%

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–19

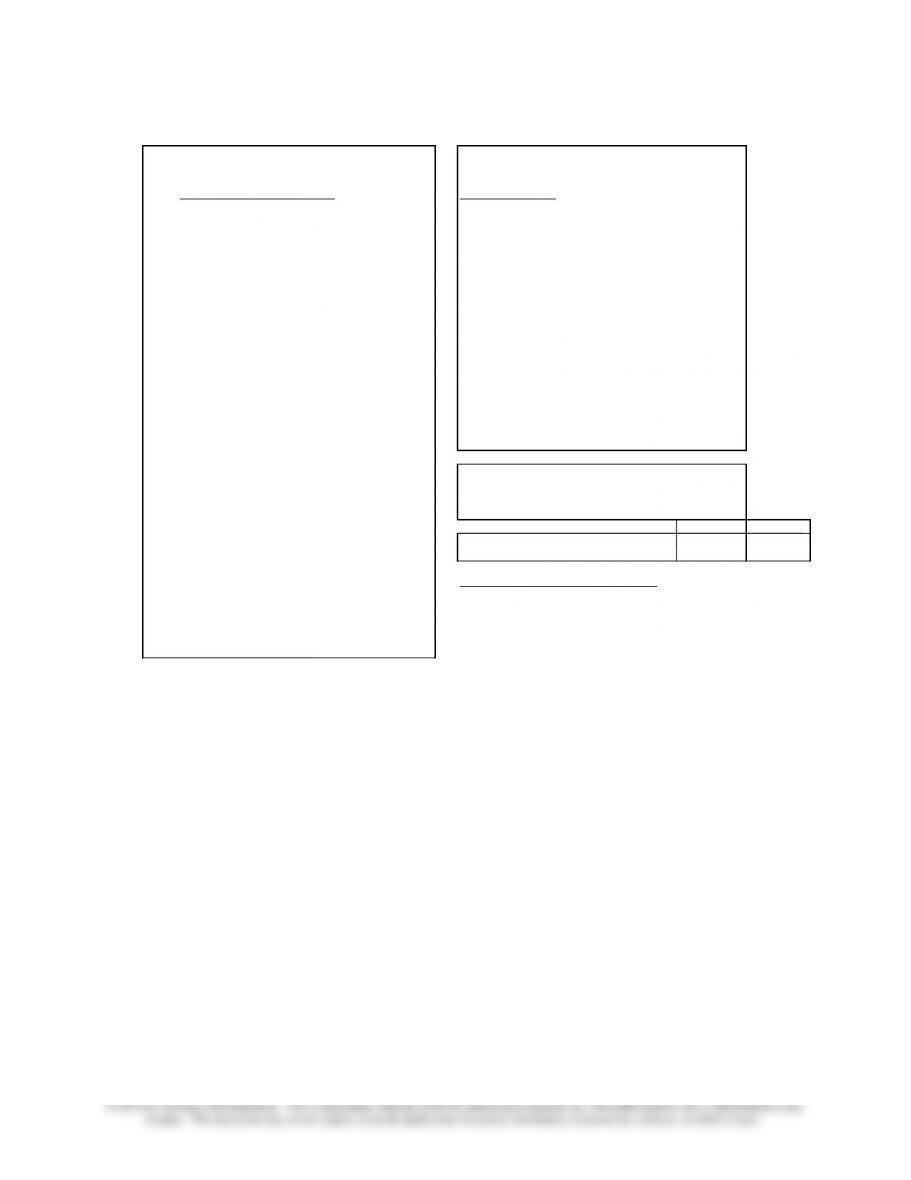

Exhibit TN-2

OutSource, Inc.

Pertinent Information Extracted from the Footnotes to the Annual Report

Footnote

A.

Inventories are stated principally at cost (last-in, first-out), which

is not in excess of market. Replacement cost would be $2,796 greater

than in 2012 and $3,613 greater in 2013.

$3,613

Add to Inventory and Capital: Amount of the LIFO reserve

$817

Add to NOPAT: The amount of increase in the LIFO reserve

B.

Deferred tax expense results from timing differences in recognizing

revenue and expense for tax and reporting purposes.

$6,784

Include as Capital: Amount of the Deferred tax reserve

$1,934

Add to NOPAT: The amount of increase in the deferred tax reserve

C.

On July 1, 2011, the Company acquired CompuPay. The acquisition has been

accounted for as a purchase, and the excess of cost over the fair value of net

assets acquired was $109,200, which is being amortized on a straight-line basis

over12 years. One-half year of amortization was taken in 1993.

$21,000

Include as Capital: Cumulative amount of goodwill that has

been amortized to date.

$8,400

Add to NOPAT: The amount of increase in Goodwill amortization

D.

Research and development costs related to software development are expensed as

incurred. Software development costs are capitalized from the point in time when

the technological feasibility of a piece of software has been determined until it is

ready to be put on line to process customer data. The cost of purchased software,

which is ready for service, is capitalized. Software development and purchased

software costs are amortized using the straight-line method over periods ranging

from three to seven years. A history of software development cost items follows:

Expensed

Capitalized

Amortized

2011

$166,430

$9,585

$0

2012

$211,852

$5,362

$4,511

2013

$89,089

$18,813

$5,111

———

———

———

$467,371

33,760

$9,622

$9,622

Include as Capital: Cumulative amount of software development

costs that have been amortized to date.

$467,371

Include as Capital: Cumulative amount of software development

costs that have been expensed to date.

$5,111

Add to NOPAT: The amount of increase in Goodwill amortization

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–20

Exhibit TN-3

OutSource, Inc.

OutSource, Inc.

EVA Capital via Financing Approach

EVA NOPAT via Financing Approach

Balance Sheet, December 31,

2013

Income Statement

2013

LIABILITIES & NET WORTH

Current liabilities

Income Available to Common

$40,616

Short-term debt and current portion

of long-term note

$27,300

Deferred Taxes (Increased)

1,934

(B)

Long-term debt less current portion

98,744

Lifo Reserve (Increased)

817

(A)

————

Goodwill Amortization

8,400

(C)

Total Debt

126,044

Software Dev. Costs Amortization

5,111

(D)

Software Dev. Costs Expensed

89,089

(D)

Equity Equivalents

————

Deferred income taxes

6,784

(B)

Increase in Equity Equivalents

105,351

LIFO Reserve

3,613

(A)

Accum Goodwill Amortization

21,000

(C)

Adjusted Income Available to Common

$145,967

Accum Software Dev. costs Amortization

9,622

(D)

Capitalize amounts of Software dev.

Add: Adjusted Interest Expense

12,427

costs that have been expensed.

467,371

(D)

Less: Tax Benefit of Interest Expense

(4,349)

————

Interest Expense After Taxes

8,077

Total Equity Equivalents

508,390

EVA NOPAT via Financing Approach

$154,044

Shareholders’ Equity:

Cumulative Convertible Exchangeable

Return on Net Assets (RONA) = NOPAT / Capital

Preferred Stock, $100 par value, authorized

EVA NOPAT via Financing Approach =

$154,044

5,000 shares, 1,000 shares issued and

EVA Capital via Financing Approach =

$1,047,499

outstanding

100,000

RONA =

14.71%

Shareholders’ Equity:

Calculate EVA – Based on:

Market Value

Book Value

authorized; 219,884 shares issued

Weighted Ave. Cost of Capital (WACC) =

12.21%

11.78%

and outstanding

219,884

EVA = (RONA – WACC) * Capital =

$26,189

$30,680

Addtl Paid in Capital

32,056

Retained Earnings

61,125

————

Adjusted Shareholders’ Equity

413,065

————

EVA Capital via Financing Approach

$1,047,499

=========

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–21

20-4 John Deere Case

Question 1: As discussed in the case, performance-evaluation and reward systems play a fundamental

role in guiding employees’ actions and, optimally, such systems should induce employees to engage in

organizationally desirable behaviors. When entering into labor contracts, employees and employers likely

have differing objectives. On the one hand, employees want to maximize the benefits they extract from

their relationship with the organization. Employees likely desire to maximize their compensation,

minimize their effort, and perform tasks that provide the most intrinsic enjoyment (and future

compensation). Employers (owners), on the other hand, hire employees to increase an organization’s

value. They want employees to exert high levels of effort towards projects with the greatest expected

payoffs for the lowest possible cost.

Performance-evaluation and reward systems should dampen, if not mitigate, the conflicts of interest

between employees and employers. To this end, performance-evaluation and reward systems serve many

vital functions in an organization (most of these are directly or indirectly discussed in the case). First,

such systems serve a motivational role whereby employees are enticed to exert high levels of effort

(duration and intensity) on organizational endeavors. In this regard, such systems not only need to

production quantity or quality. Additionally, employees can choose to perform more routine, day-to-day

activities, or engage in thinking about innovative ways to improve the process. Moreover, performance–

evaluation and reward systems should make it profitable for employees to apportion their work effort to

the tasks and activities with the highest expected returns to the organization.

Third, performance-evaluation and reward systems serve an extracting role. Employees typically know

and efficiency of the production process, thereby reducing the cost, improving the speed, and/or

increasing the quality of production. Performance-evaluation and reward systems should make it

profitable for employees to share their private information with other members of the organization.

Finally, performance-evaluation and reward systems serve an attracting role. Such systems should entice

employees with the requisite abilities and skills desired by the organization to seek employment with the

facilities of John Deere. Indeed, just about every organization, be it private, public, or not-for-profit, has a

performance-evaluation and reward system in place. For example, sales persons frequently are evaluated,

and receive a large part of their compensation, based on sales. Such compensation systems are used to: (1)

motivate sales persons to spend their time selling units; (2) focus sales persons’ attention on selling and

sales-related activities; (3) get sales persons to use their knowledge about the product and their customers

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–22

to sell more units (in turn, the company finds out which products are selling best, which customers are

buying, and where/when customers are buying); and (4) attract people who are skilled at sales and/or

motivated to sell. For similar reasons, a waiter or waitress’ compensation is linked to tips, a middle

manager’s compensation is linked to divisional performance, and an executive’s compensation is linked

to his/her company’s stock price and/or net income.

More generally, just about everyone’s performance is routinely evaluated and rewarded (or punished) by

person. For example, an instructor uses examinations to both motivate and direct student effort. This same

instructor may use student peer evaluation forms to extract information about the relative effort levels of

group members. Finally, instructors’ course policies and grading procedures are publicly available,

serving to attract students interested in the subject matter and work requirements.

Question 2:

2.a. Using formulas 1-3 from the case text, the machinist’s compensation for the week is (notice that Oa

> Os; i.e., 180 > 133.33 (40/0.3))

2.b. If 185 deck kits are fabricated, then the machinist’s compensation for the week is:

Notice that compared to question 2.a (when 180 deck kits were fabricated), the machinist’s

compensation is higher. When standards are held constant, fabricating more deck kits (by either

exerting greater effort or implementing process improvements) leads to greater compensation.

Thus, under the standard-hour plan, the machinist should be motivated to increase his/her

productivity.

As described in the case text and illustrated in this problem, however, standards under the standard-

probability of an audit, the machinist’s expected two–week compensation (again using formulas 1-3

in the case text) for the three scenarios presented in Table 2 is calculated below:

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–23

Choice

Wp (period 1)1

Wp (period 2)

Expected2

Total

Expected Pay

A

$955.80

$955.80

$1,911.60

B

$971.73

$958.77

$1,930.50

C

$982.35

$923.41

$1,905.76

1: Wp1 (A, B, C) = (# deck kits completed) × 0.30 × (20 × 0.885)

2: E[Wp2] (A, B, C) = (# deck kits completed) × 0.30 × (20 × 0.885) × (1 – paudit)

+ (# deck kits completed) × (revised standard) × (20 × 0.885) × paudit

E[Wp2] (A) = 180 × 0.30 × (20 × 0.885) = $955.80

E[Wp2] (B) = [(183×0.30×20×0.885) × 0.80] + [(183×0.28×20×0.885) × 0.20] =

$958.77

E[Wp2] (C) = [(185×0.30×20×0.885) × 0.10] + [(185×0.28×20×0.885) × 0.90] =

$923.41

Choice B maximizes the machinist’s expected two-week compensation. Notice that even though

output is highest under choice C, the machinist’s second-period (and beyond) compensation is

expected to be lower than choices A and B because of the likely increase in the standard – i.e., John

Deere is likely to ratchet-up the employee’s standard and extract some of the first-period

compensation. John Deere, on the other hand, clearly prefers choice C because production per labor

hour is highest and cost per unit of production is lowest.

This problem illustrates the inherent tradeoff faced by employees evaluated under the standard-

hour plan. Specifically, when deciding whether to increase their productivity levels, employees

must trade-off the benefits of higher current period compensation with the potential (uncertain)

2.c. Using equation (1) from the case text, the machinist’s production wages for 100/180 deck kits are:

Wp (100) = 100 × 0.30 × (20 × 0.885) = $531.00

Wp (180) = 180 × 0.30 × (20 × 0.885) = $955.80

Using equation (2) from the case text, the machinist’s non-production wages for 100/180 deck kits

are:

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–24

Using equation (3) from the case text, the machinist’s total wages for 100/180 deck kits are:

produce, thereby generating excess inventory (in this case deck kits). This is costly to John Deere

on several fronts: (1) increased inventory holding costs – in this case an extra $80 per week; (2)

potential for spoilage, damage, costly rework, and/or obsolescence due to holding inventory; (3)

muted incentives for employees to engage in any activity other than production such as training

new employees or helping co-workers.

2.d. Employee A – compensation under John Deere’s contract and the competitor’s contract:

Wp (JD) = 180 × 0.30 × ($20 × 0.885) = $955.80

Wp (competitor) = 40 × $20 = $800.00

Employee B – compensation under John Deere’s contract and the competitor’s contract:

Wp (JD) = 100 × 0.30 × ($20 × 0.885) = $531.00

Wp (competitor) = 40 × $20 = $800.00

Employee A maximizes her weekly compensation by choosing to work for John Deere while

Employee B maximizes his compensation by choosing to work for John Deere’s competitor. This

example illustrates that incentive-based compensation contracts can serve as useful sorting

(screening) mechanisms, thereby attracting employees with the highest levels of ability and

motivation.

2.e. As illustrated in questions 2.a and 2.b, the standard-hour plan can motivate employees to work hard.

In the absence of standard adjustments, employee compensation strictly increases as production

increases. Unfortunately, substantial increases in productivity can also trigger audits and standard

increases – thus, employees may withhold effort in certain situations (as shown in question 2.b). As

illustrated in question 2.d, the standard-hour plan also can attract employees with high levels of

skill and motivation.

As illustrated in question 2.c, the standard-hour plan does not always direct employees to activities

that provide John Deere the most value. Under the standard-hour plan, employees do not have

strong incentives to cooperate with, or assist, co-workers. Additionally, the standard-hour plan can

encourage overproduction. Finally, as illustrated in question 2.b, the standard-hour plan likely

penalizes employees for sharing production-related information. Moreover, employees’ private

information regarding the production process is likely to lead to large increases in performance – in

turn, large increases in performance are likely to lead to large increases in standards. Thus,

employees can find themselves being penalized for sharing their private information – i.e., they

could be working harder for less pay.

All in all, the goals of John Deere and its manufacturing employees are not perfectly aligned under

the standard-hour plan.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–25

Question 3:

Organizations can reap many benefits by moving from an individual-based to a team-based

performance-evaluation and reward system. First, team-based compensation schemes allow

performance measures to be collected at a more aggregate level. The use of aggregate information

is especially advantageous when it is costly to collect information at the individual level. This can

generate tremendous cost savings – for example, by moving to a team-based compensation plan,

John Deere no longer needed to employ a large number of industrial engineers to monitor

individual performance (as stated in the case text, this alone saved John Deere over $32 million per

year).

A second advantage to organizations is that team-based plans can foster a cooperative atmosphere

among employees. Performance evaluation and reward systems based on group performance

monitor each other’s performance. Since each individual’s compensation is tied to the collective

efforts of the group, there are incentives to ensure that every team member is contributing at a high

level.

There are, of course, possible costs to organizations associated with moving from individual-based

to team-based compensation arrangements. First, while individuals can encourage and monitor the

effort levels of fellow employees under team-based plans, this influence might be used to enforce

Another cost to organizations of team-based plans is that they can provide incentives to employees

to free-ride off the effort of others. Because individuals only receive a portion of the benefit for

each unit of effort (1 the number of team members), individuals under team based performance-

evaluation and reward systems frequently have an incentive to shirk and rely on other members to

accomplish the team’s objectives. This can lead to a classic public-goods dilemma and low levels

of production.

around each member’s strengths and weaknesses (promoting collaboration and effort-sharing).

Another benefit to employees is that team-based plans allow risks inherent in manufacturing

environments to be shared across all team members. That is, under a group-based plan, lost

compensation attributable to a “bad” event that is outside the control of the team (such as a

machine breakdown) is equally shared by all. Under an individual-based compensation plan,

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–26

Despite the potential benefits of using group-based plans to evaluate and reward performance,

these plans also can impose costs on employees. Because group-based plans make individual

compensation highly dependent upon the actions of others, group members would be motivated to

impose harsh penalties on employees not contributing at a high level to the team. For example, at

John Deere individuals have been subject to “parking lot diplomacy” and other forms of negative

group recourse since CIPP’s inception. Moreover, team-based plans have the potential to create an

environment that breeds distrust and conflict among employees.

Finally, group-based plans can raise equity concerns among team-members. Specifically, under a

group-based plan, the compensation of highly skilled and/or hard working employees could be

reduced by lower skilled and/or effort-averse employees (and vice-versa). That is, group-based

plans may under-compensate hard-working and/or highly skilled employees and over-compensate

lesser skilled, or more effort-averse, employees. Such equity issues could lead to employees being

less satisfied with team-based, rather than individual-based, compensation.

Question 4:

4.a. Using equation (4) in the case text, the adjustment factor, A, for the team is calculated as follows:

Team input hours = 30 employees × 40 hours per employee = 1,200 hours

Team standard output hours = 180 units × 6.5 hours per unit = 1,170 hours

Ea (actual team efficiency) = 1,170 1,200 = 0.975

employees). As mentioned in the teaching note to question (3), this could lead to equity concerns

among employees. That is, the machinist could feel s/he is working just as hard under CIPP as

under the standard-hour plan. However, since pay is linked to the productivity of others, his/her

compensation might actually decrease under CIPP.

4.b. The Machinist’s Weekly Compensation—185 Mowers Produced

Using equation (4) from the case text, the adjustment factor, A, for the team is calculated as

follows:

Team input hours = 30 employees × 40 hours per employee = 1,200 hours

Using equation (5) from the case text, the machinist’s compensation for the week is:

Wt = 40 × 20 × 1.201 = $960.80

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–27

Notice that compared to question 4.a (when the team produced 180 mowers), the machinist’s

compensation is higher. When team benchmarks are held constant, producing more mowers (by

either working harder or implementing process improvements) leads to higher compensation. Thus,

similar to the standard-hour plan, CIPP should motivate employees to increase their productivity.

The Machinist’s Compensation over the next two Bi-annual Periods – 180 Mowers Produced

If the team chooses to keep production stable at 180 mowers per week, then the machinist would

earn $943.20 per week (calculated in 4.a above). Thus, the machinist’s compensation over the next

two bi-annual periods (one year) would be:

Ea (actual team efficiency) = 1,202.5 1,200 ≈ 1.002

Eb (benchmark efficiency) = 0.94

So, A = {([(1.002 – 0.94) 0.94] × 0.67) + 1} × 1.15 ≈ 1.201

In turn, using equation (5) the machinist’s compensation for the week is:

Wt = 40 × 20 × 1.20 = $960.80

Thus, the machinist’s compensation for bi-annual period 1 (before the bonus) would be:

Bi-annual Period 2 Compensation

Since the team exceeded the standard by over 6.49 percent (the adjustment was over 120 percent),

the new benchmark for the team will be approximately 1.001 (0.94 × 1.0649).

Using this new benchmark and equation (4) from the case text, the adjustment factor, A, for the

team is calculated as follows:

Team input hours = 30 employees × 40 hours per employee = 1,200 hours

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–28

The machinist’s compensation for the week is:

Wt = 40 × 20 × 1.151 = $920.80

Thus, the machinist’s compensation for bi-annual period 2 would be:

Wbi-annual period 2 = $920.80 × 26 weeks per bi-annual period = $23,940.80

Total Compensation Over the Two Bi-annual Periods

mowers) because of the one-time bonus paid for exceeding the benchmark by 6.49 percent.

More generally, when deciding whether to implement an innovation, teams evaluated and rewarded

under CIPP continue to face a tradeoff between the benefits of higher current period compensation

and the cost of being evaluated and rewarded under a higher benchmark in the future. As illustrated

in question 2.b, this is very similar to the tradeoff faced by employees under the standard-hour

plan. However, there are two fundamental differences between the tradeoff faced by employees

production efficiency. As illustrated in this question, the bonus attempts to mitigate the tradeoff

faced by manufacturing teams when deciding whether to make their production processes more

efficient.

The Labor Savings to John Deere

The reduction in the machinist’s bi-annual compensation would be $1,040 ($24,980.80 before the

benchmark increase – $23,940.80 after the benchmark increase). Thus, John Deere rewards a one-

company pays a lump sum in the present to reap permanent increases in production efficiency.

4.c. By spending non-production hours training the two newly hired employees, the machinist could

increase the productivity of these two group-members. Further, increasing the productivity of these

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–29

two group members would ultimately enhance the efficiency of the F725 Front Mower team. Since

the machinist’s compensation depends upon the efficiency of his or her team, the machinist would

have financial incentives to spend non-production hours training the two newly hired employees.

Thus, by linking individual compensation to team performance, CIPP rewards group-member’s

Although the standard-hour plan provides financial incentives for cooperative efforts, it is unclear

whether it is in the machinist’s best interest to train the newly hired employees. Specifically, the

machinist would have to bear the full cost of the effort required to train the newly hired employees,

but the benefit that results from this effort would be shared equally by all team members. As

described in the teaching note to questions (3) and 4.a, the machinist could feel s/he is being

inequitably rewarded for this effort.

4.d. CIPP continues to reward high skills and high effort levels since performance and pay, ceteris

paribus, strictly increase as these variables increase. Under CIPP, however, compensation levels

not only depend on individual performance but also depend on the performance of other team

members. This dependence on other team members can alter the incentives of both high-skilled and

low-skilled employees to seek employment with John Deere. High-skilled employees would likely

members. Thus, lower-skilled employees might face negative group recourse (stress) and peer

pressure to perform at levels beyond their capabilities.

4.e. Overall, CIPP appears to make improvements over the standard-hour plan in motivating effort,

extracting production information, and appropriately directing the attentions of its manufacturing

employees. To achieve these gains, John Deere likely trades-off its ability to attract the most highly

skilled employees. In the remainder of this section, we discuss some of these improvements and

tradeoffs of CIPP when compared to the standard-hour plan as well as present actual performance

results from the plan. Finally, we discuss improvements that John Deere management would like to

make to CIPP in the upcoming contract negotiations.

Motivating and Extracting Roles

Because employees know ex ante exactly when and how their standards will increase (i.e. they no

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–30

Specifically, Figure 1 presents the average team benchmarks for John Deere’s manufacturing

employees for the first eight bi–annual periods (four years) following CIPP’s implementation. This

figure shows that, on average, team benchmarks increased from their initial level of 0.79 to 0.92 by

benefit of the one time 5 to 10 percent bonus for the costs of higher future standards.

Instead, manufacturing teams began to produce just shy of the 120 percent adjustment level. Figure

2 presents the distribution of actual bi-annual team performance at John Deere for the past five

years. Figure 2 clearly demonstrates a discontinuity in the distribution just short of the 120 percent

benchmark adjustment level. This behavior represents a rational economic response to the

mechanistic ratchet imposed under CIPP. That is, by producing just shy of the 120 percent

adjustment level, manufacturing teams maximize their compensation without incurring an

increased future benchmark.

Thus, in the first three years following the implementation of CIPP, the plan seems to have

successfully created a “win–win” situation for the manufacturing employees and John Deere as a

whole. Employees received larger compensation in the form of one time bonuses for increasing

UAW, Caterpillar (John Deere’s primary competitor) was replacing striking UAW

employees with non-union employees. Thus, the UAW was under a tremendous amount of

pressure to complete the contract with John Deere without a strike.

Consequently, the fear of job loss or plant closures could have induced employees to agree

to wage concessions and/or standard increases that were not necessarily in their best

interest. Moreover, companies have used the threat of job loss and/or plant closures to

induce employees to agree to compensation contracts with terms more favorable to the

organization (see Arnold (1998) for a vivid example of this strategy at Caterpillar).