Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–31

16–46 Direct Labor Variances, Productivity Measures, and Standard

Costs (30 min)

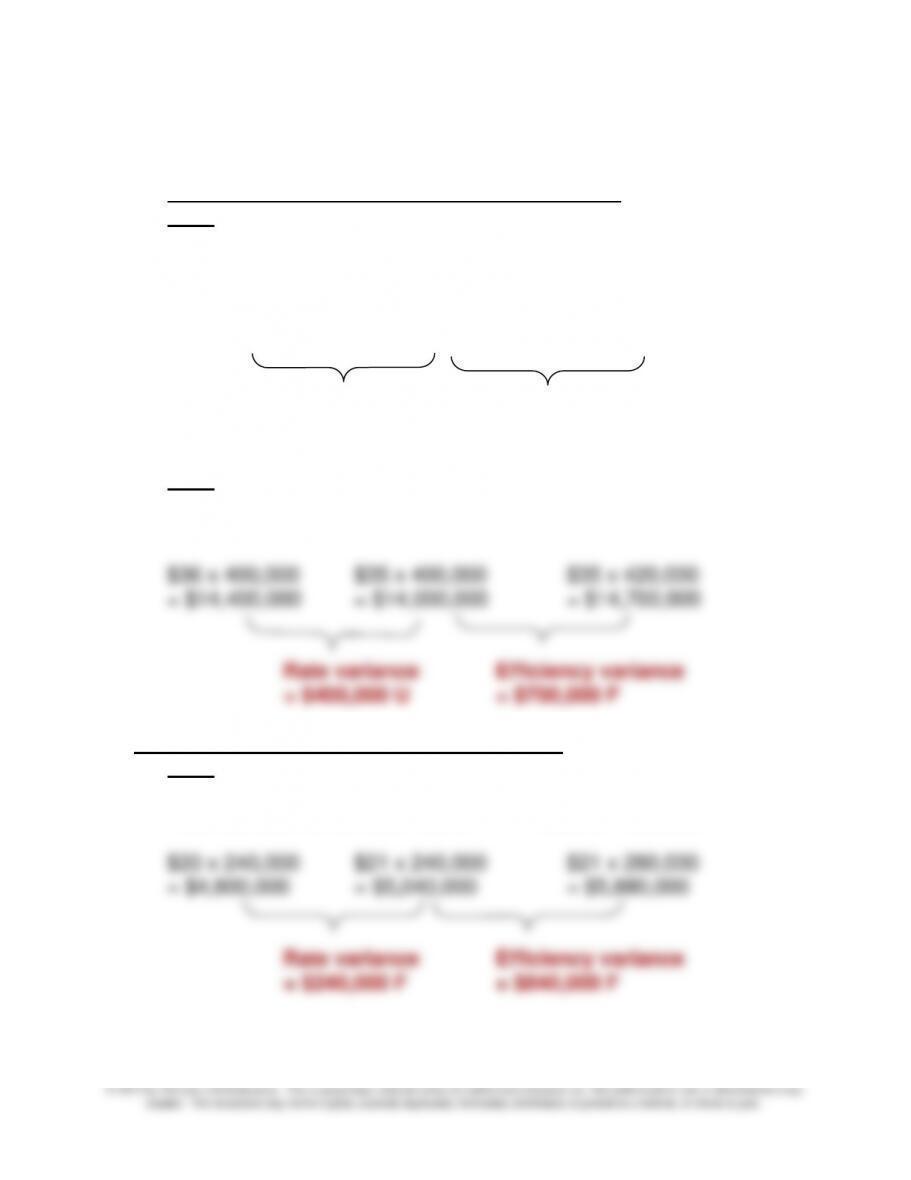

1. Assembly Department Direct Labor Variances

2012:

Total actual direct labor hours: 25 x 20,000 = 500,000

Total standard direct labor hours: 24 x 20,000 = 480,000

$30 x 500,000 $28 x 500,000 $28 x 480,000

= $15,000,000 = $14,000,000 = $13,440,000

Rate variance Efficiency variance

= $1,000,000 U = $560,000 U

2013:

Total actual direct labor hours: 20 x 20,000 = 400,000

Total standard direct labor hours: 21 x 20,000 = 420,000

Testing Department Direct Labor Variances

2012:

Total actual direct labor hours: 12 x 20,000 = 240,000

Total standard direct labor hours: 14 x 20,000 = 280,000

16–32

16-46 (continued –1)

Testing Department Direct Labor Variances (continued)

2013:

Total actual direct labor hours: 10 x 20,000 = 200,000

Total standard direct labor hours: 11 x 20,000 = 220,000

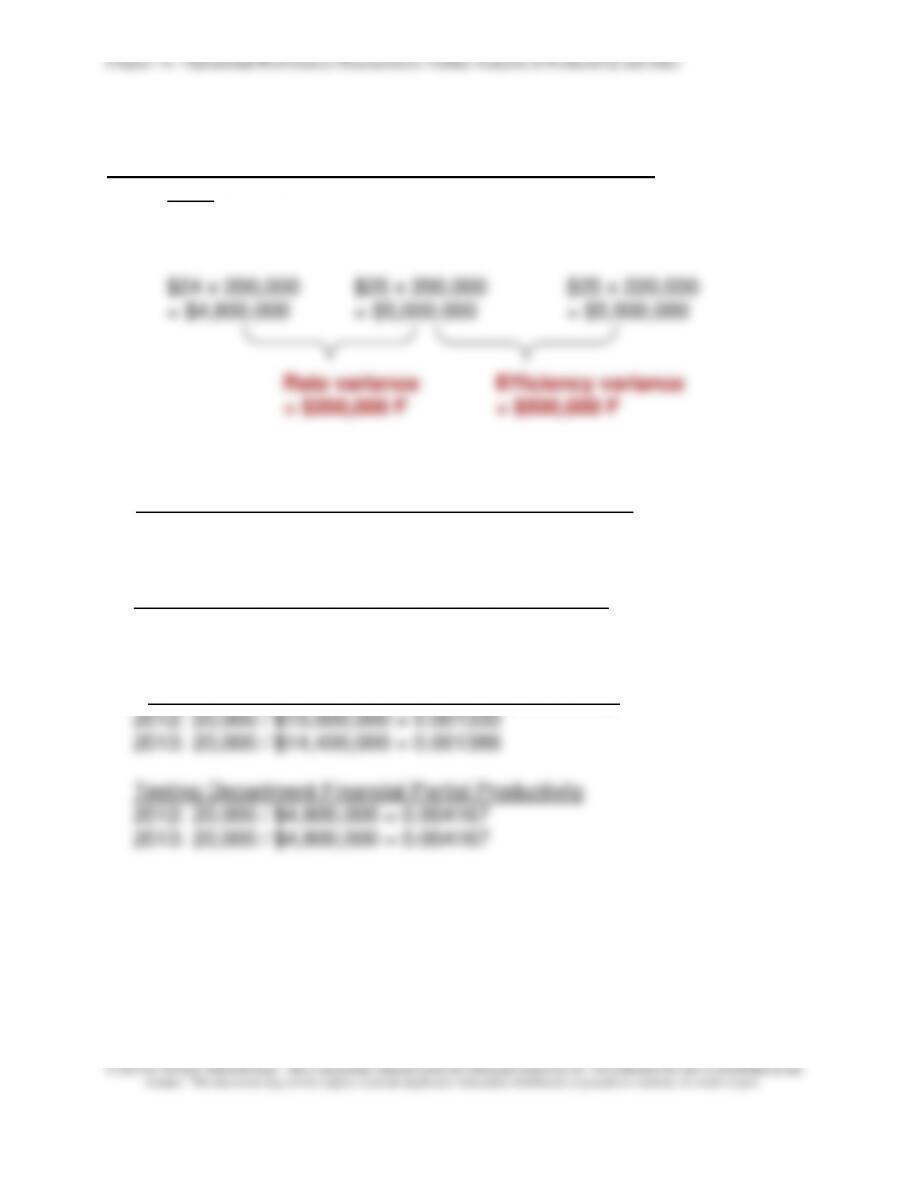

2. Assembly Department Operational Partial Productivity

2012: 20,000 / 500,000 = 0.04

2013: 20,000 / 400,000 = 0.05

Testing Department Operational Partial Productivity

2012: 20,000 / 240,000 = 0.083333

2013: 20,000 / 200,000 = 0.1

3. Assembly Department Financial Partial Productivity

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–33

16-46 (continued –2)

4. Recap:

Operational partial productivity

2012 2013 Change

Assembly 0.04 0.05 0.01 F

2012 to 2013. The financial partial productivity in the Assembly also

improved while the Testing remained unchanged.

5. The standards in a standard costing system often are determined

independently and incorporate changes in operating factors. The

standard for the operation of a year may change because of changes in,

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–34

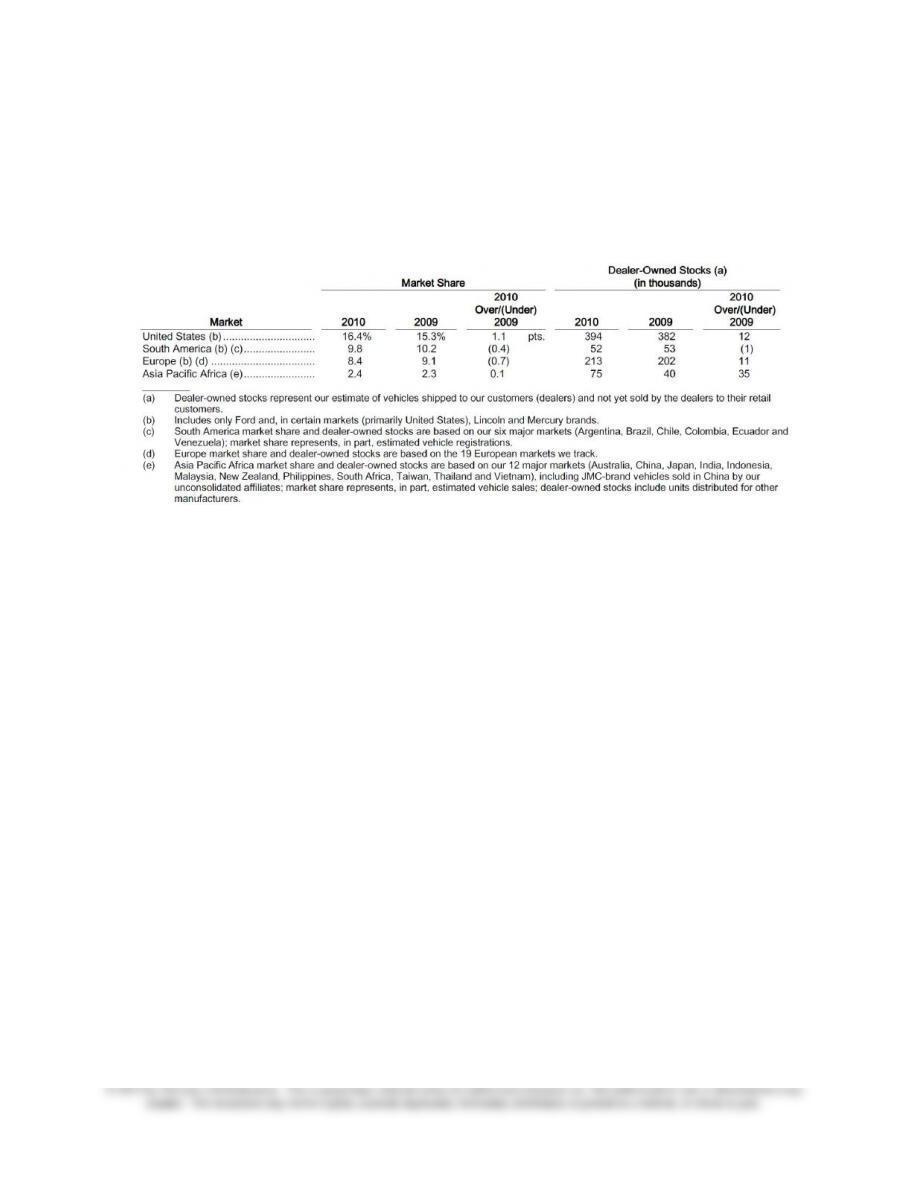

16-47 Productivity and Market Share in the Auto Industry; Internet

Exercise (20 min)

1.

The total productivity for the auto makers is shown below for 2010, the

most recent year at the time the question was prepared in October 2011.

Also, while not required, the results for 2007 and 2005 are also shown for

comparison.

12/31/2010 12/31/2010

Ford GM

Sales 128,954$ 135,592$

Cost of Goods Sold 122,296 130,508

Cost of Goods Sold x 80% 97,837 104,406

Total Productivity 1.32 1.30

For contrast, the productivity calculations for the two companies in 2007

and 2005 are as follows:

12/31/07 12/31/07

Ford GM

Sales 154,379$ 178,199$

Cost of Goods Sold 142,589 166,239

Cost of Goods Sold x 80% 114,071 132,991

Total Productivity 1.35 1.34

12/31/05 12/31/05

Ford GM

Sales 153,503$ 158,221$

Cost of Goods Sold 144,944 162,173

Cost of Goods Sold x 80% 115,955 129,738

Total Productivity 1.32 1.22

The objective of this question is to make the students aware that total

productivity can be at least approximated for a company the student is

interested in by obtaining basic financial data from the firm’s annual report.

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–35

16-47 (continued –1)

Note there are no significant differences between the auto makers or

between the productivity measures for 2005, 2007, and 2010. Note that this

is in contrast to the Harbour Report data on auto firm productivity in 2008,

cited in Problem 16-35, which reports an increase in productivity

(measured as labor hours per vehicle) for Ford. The two measures of

productivity do not measure the same thing, so that these differences arise.

While the measures computed here are limited by the amount of

information available, they can provide a starting point for looking at other

measures of performance, and looking for more detailed information about

From Ford’s 2010 Annual Report:

“…Total costs and expenses for our Automotive sector for 2010 and 2009

was $113.5 billion and $107.2 billion,respectively, a difference of $6.3

billion. An explanation of the change is shown below (in billions):

2010(Over)/Under2009

Explanation of Change:

Volume and Mix, and Exchange (11.6)

Material Costs Excluding Commodity Costs 1.1

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–36

16-47 (continued -2)

Ford’s 2005 Annual Report has a similar analysis

Increase (decrease)

Supplier related cost $1

Pension and health care .8

Warranty costs .4

Depreciation and amortization (investments

2. This requirement can be assigned for class discussion, and answers will

likely vary, depending on what portion of the financial statement is used

and which year’s annual report is used. The discussion here can focus on

some of the following (all these points are based on the 2010, 2007 and

2005 annual reports of GM and Ford)

Alternatively, the instructor can assign requirement 1 only, and then

discuss some of the observations about requirement 2, as noted below.

• some firms will be improving market share in some markets and

losing in others; for example Ford lost market share in the Europe

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–37

16-47 (continued -3)

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–38

16–48 Productivity and Ethics (15 min)

1. The operational partial productivity deteriorates slightly from

0.0051 in 2012 (500/99,000) to 0.005 in 2013 (560/112,000).

2. Kim Tomas should not follow the order without following a

consistent accounting method. If the firm believes that certain

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–39

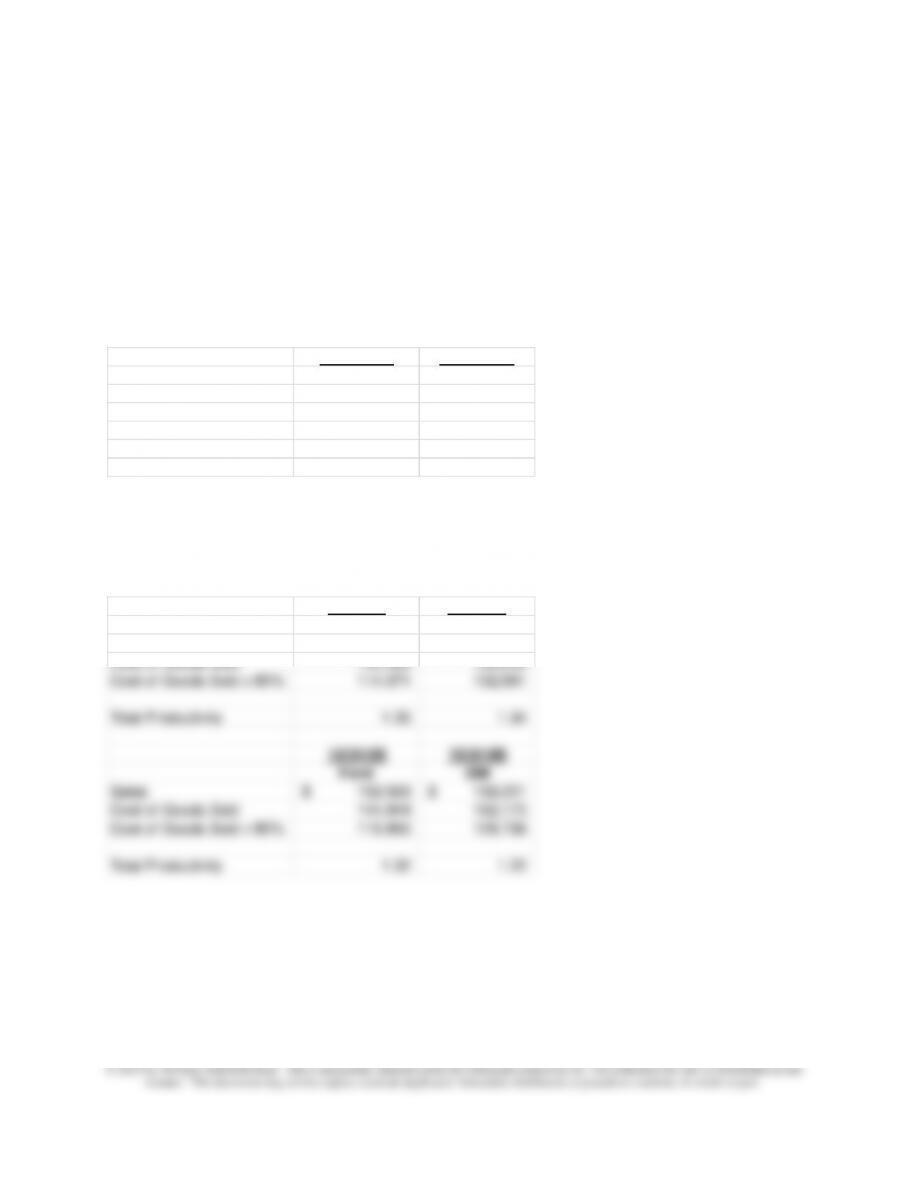

16–49 Partial Operational and Financial Productivity; Medical Practice (45 min)

1.,2. Partial operational and financial productivity and separation of partial financial productivity:

2013 2012

Patient visits 30,000 26,000

Nursing hours used 18,675 17,800

Administrative hours used 12,225 12,225

Cost of nursing support per hour $39.00 $38.00

Cost of administrative suppor per hour $25.56 $24.00

Total Nursing Cost $728,325 =18,675 x $39 $676,400

Total Administrative Cost $312,471 =12,225 x $25.56 $293,400

Financial Partial Productivity

Nursing 0.041190 =30,000/728,325 0.038439

Administrative 0.096009 =30,000/312,471 0.088616

Operational Partial Productivity

Nursing 1.60643 =30,000/18,675 1.460674

Administrative 2.45399 =30,000/12,225 2.126789

Output 30,000 30,000 30,000 26,000

Input Amount

Nursing 18,675 20,538 20,538 17,800

Administrative 12,225 14,106 14,106 12,225

Cost per unit of input

Nursing $39 $39 $38 $38

Administrative $26 $26 $24 $24

Nursing 0.041190 0.003737 0.037453 (0.000986) 0.038439 – 0.038439 0.002752

Administrative 0.096009 0.012801 0.083208 (0.005409) 0.088616 – 0.088616 0.007393

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–40

16–49 (continued –1)

3.

MEMO

TO: Rajat Patel, Integrated Medical Care

FROM: Joseph Marin, Marin & Associates

I have calculated the financial partial productivity measure for IMC for

the current and prior year and the supporting documentation is attached.

Nursing productivity improved by 0.003737 over the prior year, while

administrative productivity improved by 0.012801. I attribute this to the

greater than 15% increase in patient demand, with only modest increases in

nursing hours, and no increase in administrative hours. These figures show

that the practice is managed very effectively.

There was a small decline in the pricing component of productivity,

since average wages increased in both nursing and administrative support;

overall, taking both the change in wages and change in hours into account,

the financial productivity of both nursing and administrative support improved

has productivity of 0.096 in the current year relative to the industry average of

1.12. The good news, as noted above, is that the productivity of the

administrative support area is improving relative to the prior year, and these

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–41

16-49 (continued –2)

Medical practices are under pressure in recent years as Medicare

reimbursements have fallen and technology and labor costs have

increased. Many practices have looked for increased productivity and

profitability through:

1. Cross-training employees so that overall staff positions can be

reduced as employee are able to perform a variety of tasks

trend is for the single-doctor practice to be declining in numbers, as

more and more medical practices consolidate.

Source: Katherine Reynolds Lewis, “Medical Practices Work on Ways to

Serve Patients and Bottom Line,” The New York Times, September 8,

2011, p. B10.

4.

16–50 Flexible Budget, Sales Volume, Sales Mix, and Sales Quantity

Variances (40 min)

1.

Total per unit or % Total per unit or %

Sales

Product A 180,400$ 110.00$ 240,000$ 120.00$

Product B 341,120 52.00 300,000 50.00

Total 521,520$ 540,000$

Sales Units

Product A 1,640$ 20.00% 2,000$ 25.00%

Product B 6,560 80.00% 6,000 75.00%

Total 8,200$ 8,000$

Variable Cost

Product A 106,600$ 65.00$ 140,000$ 70.00$

Product B 216,480 33.00 180,000 30.00

Total 323,080$ 320,000$

Contribution Margin

Product A 73,800$ 45$ 100,000$ 50.00$

Product B 124,640 19.00 120,000 20.00

Total 198,440$ 220,000$

Fixed cost

Product A 80,000$ 80,000$

Product B 40,000 40,000

Total 120,000$ 120,000$

Contribution Income Statement

Sales Price Flexible Sales Volume

Sales

Actual Variance Budget Variance Budget

Product A 180,400$ (16,400) $196,800 (43,200) 240,000$

Product B 341,120

13,120 328,000 28,000

300,000

Operating Income 78,440$ 100,000$

ABC=A+B

Sales Mix Sales Quantity Volume

Variance Variance Variance

Product A

(20,500)$ =(.20-.25)x8200x50 2,500$ =(8200-8000)x.25×50 (18,000)$

Product B

8,200$ =(.80-.75)x8200x20 3,000$ =(8200-8000)x.75×20 11,200

(12,300)$ 5,500$ (6,800)$

Actual

Budget

Summary of Variances, as calculated above in contribution margin

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–43

Product A Product B

Flexible Budget Variance (8,200)$ (6,560)$

Sales Volume Variance (18,000) 11,200

Sales Quantity Variance 2,500 3,000

Sales Mix Variance (20,500) 8,200

16-50 (continued –1)

2.

The reconciliation of the selling price, variable cost, and flexible cost

variances is as follows. The variances are in the solution shown in part 1.

A negative selling price variance means an unfavorable variance and a

positive is favorable. A negative variable cost variance means a favorable

variance and a positive is unfavorable.

Product A Product B

Selling Price Variance (16,400)$ 13,120$

Less: Variable Cost Variance (8,200) 19,680

Flexible Budget Variance (8,200)$ (6,560)$

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–51 Flexible Budget, Sales Volume, Sales Mix, and Sales Quantity

Variances (30 min)

1.

T10 S40 T10 S40 Actual Budget

Units sold 1,200 1,500 1,000 1,000 2,700 2,000

Sales Dollars 126,000$ 58,500$ 100,000$ 40,000$ 184,500$ 140,000$

Sales Price 105.00$ 39.00$ 100.00$ 40.00$

Variable Cost 61,200$ 34,500$ 50,000$ 25,000$ 95,700$ 75,000$

Unit Variable Cost 51.00$ 23.00$ 50.00$ 25.00$

Total per unit or % Total per unit or %

Sales

T10 126,000$ 105.00$ 100,000$ 100.00$

S40 58,500 39.00 40,000 40.00

Total 184,500$ 140,000$

Sales Units

T10 1,200 44.44% 1,000 50.00%

S40 1,500 55.56% 1,000 50.00%

Total 2,700 2,000

Variable Cost

T10 61,200$ 51.00$ 50,000$ 50.00$

S40 34,500 23.00 25,000 25.00

Total 95,700$ 75,000$

Contribution Margin

T10 64,800$ 54.00$ 50,000$ 50.00$

S40 24,000 16.00 15,000 15.00

Total 88,800$ 65,000$

Fixed cost

T10 10,000$ 10,000$

S40 10,000 10,000

Total Variable Costs 95,700$ (1,800)$ 97,500$ 22,500$ 75,000$

Contribution

T10 64,800$ 4,800$ 60,000$ 10,000$ 50,000$

S40 24,000

1,500 22,500 7,500 15,000

Total Contribution 88,800$ 65,000$

Less Fixed Costs 20,000

20,000

Operating Income 68,800$ 45,000$

A B C=A+B

Sales Mix Sales Quantity Volume

Variance Variance Variance

T10 (7,500)$ =(.4444-.50)x2700x50 17,500$ =(2700-2000)x.5x50 10,000$

S40 2,250$ =(.5555-.5)x2700x15 5,250$ =(2700-2000)x.5x15 7,500

(5,250)$ 22,750$ 17,500$

Actual

Budget

Contribution Income Statement

Total

Chapter 16 – Operational Performance Measurement: Further Analysis of Productivity and Sales

16–45

16–51 (continued -1)

The solution is summarized below, and the calculations are shown above

(a negative is unfavorable and a positive is favorable):

T10 S40 Total

Flexible Budget Variance 4,800$ 1,500$ 6,300$

Sales Volume Variance 10,000 7,500 17,500

Sales Quantity Variance 17,500 5,250 22,750

Sales Mix Variance (7,500) 2,250 (5,250)

2.

MEMO

TO: Jay Banning, CEO

FROM: I M Student

RE: Banning Inc. Variance Analysis

The following information describes the results of variances

calculated on the attached spreadsheet (see requirement 1) with regard

to what was planned for 2013 and the actual results reported.

The firm has a favorable sales volume variance for both T10 and S40

due to increase sales volumes over budget for both products. The total

sales quantity of the firm for both products has increased significantly.

variance.

The flexible budget variance is favorable for both S40 and T10

because T10’s increase in price was greater than its small increase in

unit variable cost; for S40, the small decrease in price was more than

recovered by the substantial decrease in unit cost for S40.

Please contact me for further discussion.