Chapter 12 – Strategy and the Analysis of Capital Investments

12–16

12–30 Future and Present Values Using Excel (30 minutes)

A. To calculate future values, use the following Excel function:

FV(rate,nper,pmt, pv,type)

1. Between January 1, 1701 and December 31, 2012 there are 624 six-month

periods (nper). (624 = ([2012 – 1701] +1) × 2.) Thus, at the end of year 2012,

at an annual interest rate of 6% compounded semiannually, the $24.00 would

have grown to $2,458,325,906, as follows:

FV(0.06/2,624,0,-24,0)

2. FV(0.08/2,624,0,-24,0) = $1,020,974,662,039

B. To calculate present values, use the following Excel function:

PV(rate,nper,pmt,fv,type)

1. For a stream of ten (10) end-of-year payments of $25,200,000 (ordinary

annuity) and a discount rate of 12%, we have:

PV(0.12,10,-25200000,0,0) = $142,385,620

2. If the first payment is received the day the contract is assigned (annuity due),

we have:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–17

12–31 Cash Receipts Frequency and Present-Value Consequences (20 minutes)

1. Periodic cash receipts, to earn a 12% return, if payments are received from the

purchaser for each of the listed situations. NOTE: the PMT function in Excel was

used to generate the periodic cash payment/receipt for each of the following

cases.

PMT(rate,nper,pv,fv,type)

Rate is the interest rate for the loan, nper is the total number of payments, pv is

the present value (i.e., the total amount that a series of future payments is worth

now; also known as the principal), fv is the future value (or a cash balance you

want to attain after the last payment is made; if fv is omitted, it is assumed to be 0

(zero)), and type is the number 0 (zero) or 1 and indicates when payments are

due (if omitted, or 1 is chosen, it is assumed that payments occur at the end of

each period).

Input Data:

Sales Price (present value, pv) = $500,000

Required Pre-tax Return = 12.00%

Financing Period, years = 20

# Weekly payments per year = 52

# Monthly payments per year = 12

For quarterly payments = 0.12 ÷ 4

For annual payments = 0.12 ÷ 1

Periodic Cash

Receipt

Total per

Year

Total Over 20-

Year Period

a. Weekly Payments

$1,269

$66,004

$1,320,087

b. Monthly Payments

$5,505

$66,065

$1,321,303

c. Quarterly Payments

$16,556

$66,223

$1,324,470

d. Annual Payments

$66,939

$66,939

$1,338,788

12–18

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

12-31 (Continued)

2. What general conclusion can you draw based on the calculations above in (1)?

Money has a time value. As such, cash received earlier (e.g., on a quarterly basis

rather than an annual basis) has a greater value to the recipient (who, for example,

could invest those receipts). Therefore, when payments are made more frequently, a

lower annual amount will occur. As seen from the data above, total cash

Chapter 12 – Strategy and the Analysis of Capital Investments

12–19

12–32 Value of Accelerated Depreciation (25-30 minutes)

1. The incremental PV of using SYD depreciation rather than SL depreciation, at a

discount rate of 8%, is $1,272, as follows:

PV

Depreciation Method Difference Factor PV of

Year SYD S-L Amount Tax Effect at 8% Tax Effect

1 $40,000 $25,000 $15,000 $6,000 0.926 $5,556

2 30,000 25,000 5,000 2,000 0.857 1,714

3 20,000 25,000 (5,000) (2,000) 0.794 (1,588)

2. The incremental PV of using DDB depreciation rather than SL depreciation, at a

discount rate of 8%, is $1,615, as follows:

PV

Depreciation Method Difference Factor PV of

Year DDB S-L Amount Tax Effect at 8% Tax Effect

1 $50,000 $25,000 $25,000 $10,000 0.926 $9,260

2 25,000 25,000 – 0 – – 0 – 0.857 -0-

3 12,500 25,000 (12,500) (5,000) 0.794 (3,970)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–20

12–32 (Continued)

3. The incremental PV of using MACRS depreciation, rather than SL depreciation, at

a discount rate of 8%, is $1,345, as follows:

PV

Depreciation Method Difference Factor PV of

Year MACRS S-L Amount Tax Effect at 8% Tax Effect

1 $33,3301 $25,000 $8,330 $3,332 0.926 $3,085

2 44,4502 25,000 19,450 7,780 0.857 6,667

3 14,8103 25,000 (10,190) (4,076) 0.794 (3,236)

Notes:

1 $100,000 × 33.33%

2 $100,000 × 44.45%

Chapter 12 – Strategy and the Analysis of Capital Investments

12–21

12–33 Weighted-Average Cost of Capital (WACC) (20-25 minutes)

a. Bond interest expense before tax = $5,000,000 × 9% = $450,000

Income tax savings on bond interest expense = $450,000 × 30% = 135,000

After-tax bond interest expense = $315,000

b. After-tax cost of preferred stock = dividend per share/market price per share

= $3 ÷ $30 = 10.00%

c. Using weights based on the current market values of debt and equity, the

estimated WACC for this firm is 13.08%, as follows:

Interest After-tax

or Rate or Current Cost of

Dividend Expected Market Capital

Book Value Rate Return Values Weights Components

Bond $5,000,000 9% 5.73% $5,500,000 0.275 1.58%

Preferred

Chapter 12 – Strategy and the Analysis of Capital Investments

12–22

12–34 Determining Cash Flows; Basic Capital Budgeting (10–15 minutes)

1. The after-tax cash flow from disposal of the old machinery = after-tax gain on

sale = ($1,800 – $0) × (1 – t) = $1,800 × 0.60 = $1,080

2. The PV of after-tax operating cash savings = pre-tax operating cash savings × (1

4. C

Notes:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–23

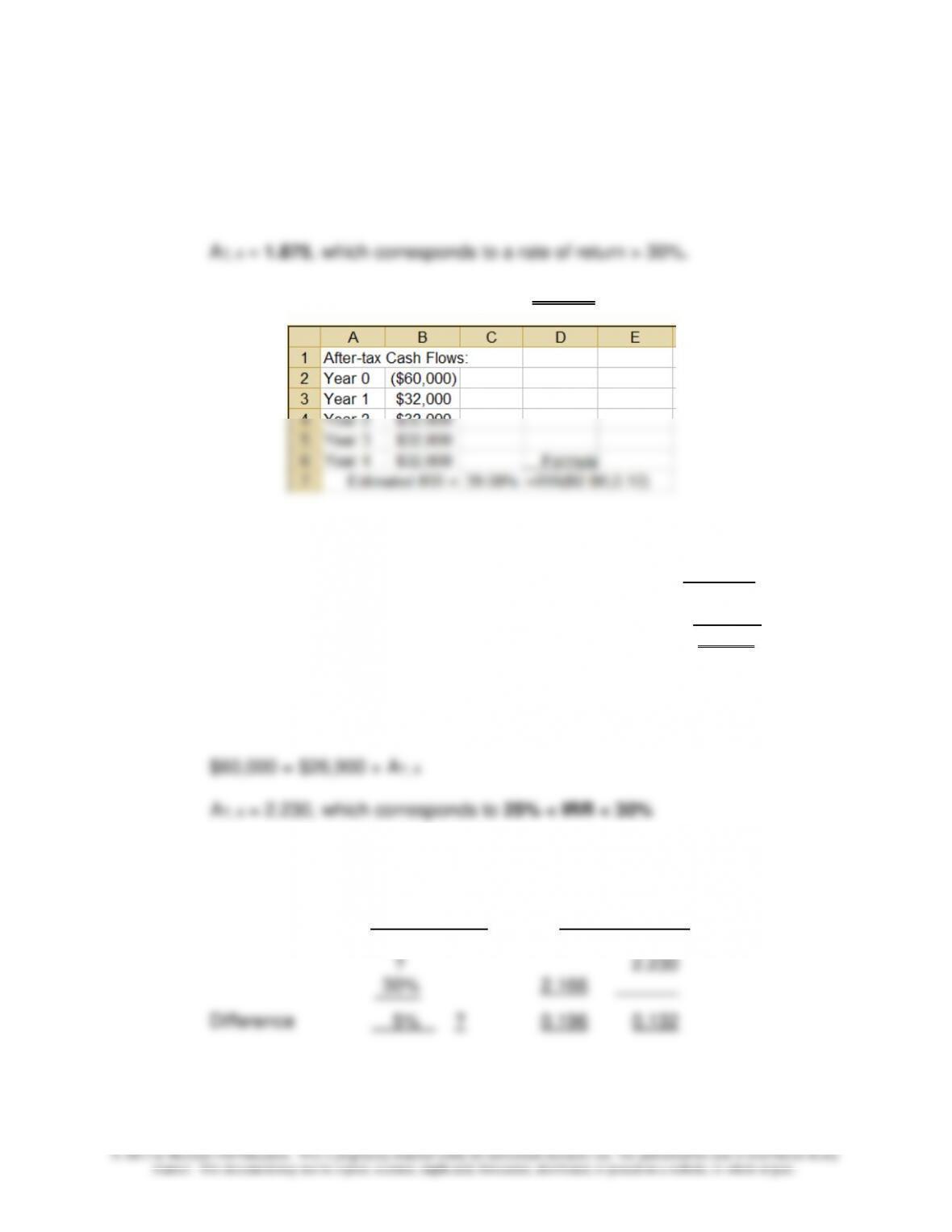

12–35 After-Tax Net Present Value (NPV) and IRR (non-MACRS rules) (40-45 minutes)

1. a. Net cash inflow each year: $62,000 – $30,000 = $32,000

Present value of net cash inflows (@10%) = $32,000 × 3.170 = $101,440

Therefore, NPV = $101,440 – $60,000 = $41,440

b. Net cash inflow before depreciation $32,000

Depreciation expense ($60,000 ÷ 4 years) 15,000

Increase in net income before tax $17,000

c. Double-declining balance depreciation (non-MACRS):

Beginning Depreciation Accumulated Ending

Year Book Value Expense Depreciation Book Value

0 $60,000

1 $60,000 $30,000 $30,000 30,000

2 30,000 15,000 45,000 15,000

Pre-Tax DDB 30% After-tax 10%

Cash Depreciation Taxable Income Net Cash Discount Present

Year Inflows Expense Income Taxes Inflow Factor Values

0 ($60,000) ($60,000) 1.000 ($60,000)

1 $32,000 $30,000 $ 2,000 $ 600 $31,400 0.909 28,543

2 32,000 15,000 17,000 5,100 26,900 0.826 22,219

Chapter 12 – Strategy and the Analysis of Capital Investments

12–24

12–35 (Continued-1)

2. a. Net cash inflow each year: $62,000 – $30,000 = $32,000

$60,000 = $32,000 × A?, 4

Using the IRR function of Excel, IRR = 39.08%, as follows:

b. Net cash inflow before depreciation $32,000

Depreciation expense ($60,000 ÷ 4 years) 15,000

Increase in net income before tax $17,000

Income tax rate × 30%

Income tax $5,100

Net after-tax cash inflow = $32,000 – $5,100 = $26,900 per year

By inspection of the annuity factors in Appendix C, Table 2, we see that:

We can also use the annuity tables in the text (Appendix C), and interpolation, to

estimate the project’s IRR, as follows:

Discount Rate Discount Factor

25% 25% 2.362 2.362

12–35 (Continued-2)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–25

Therefore, estimated Internal Rate of Return (IRR) =

Finally, we could use the built-in IRR function in Excel, which provides an IRR

= 28.27%, as follows:

Chapter 12 – Strategy and the Analysis of Capital Investments

12–26

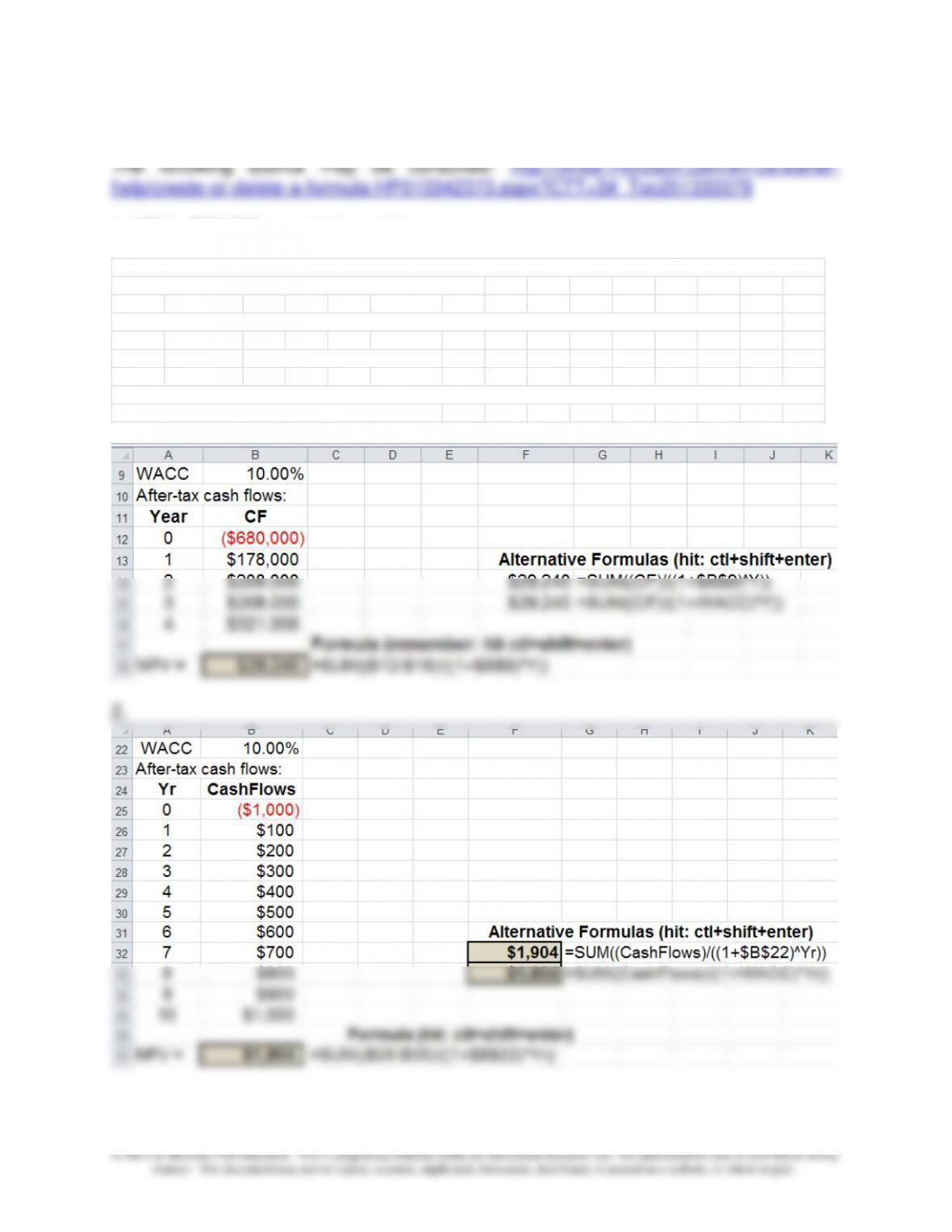

12-36 Using Arrays in Excel; NPV Analysis (45minutes)

1. NPV = $29,240 (rounded), as follows:

First, define variable names (go to “Formulas,” then “Define Names“). For example, define cell B9 as “WACC,” cells A12

through A16 as “Year,” and cells B12 through B16 as “CF.”

Next, enter into an open cell (e.g., B18) the following formula to calculate the estimated NPV of this project:

=SUM(CF/(1+WACC)^Year)

Finally, rather than hitting “enter,” you now hit the following (to enter the array formula): control+shift+enter. Cell B18 should

now display the correct amount, $29,240 (rounded).

12–37 Basic Capital Budgeting Techniques (45-50minutes)

a. Project A:

b. Project B:

After-tax Cumulative

Year Cash Inflows After-tax Cash Inflows

1 $ 500 $ 500

2 1,200 1,700

3 2,000 3,700

4 2,500

c. Project C:

Depreciation expense per year: $5,000 ÷ 5 = $1,000

Taxable income each year: $2,500 – $1,000 = $1,500

Income tax each year: $1,500 × 25% = $375

Annual after-tax net cash inflow: $2,500 – $375 = $2,125

years2.78

$1,800

$5,000

PeriodPayback ==

years3.52

$2,500

$3,700)($5,000

3PeriodPayback =

−

+=

Chapter 12 – Strategy and the Analysis of Capital Investments

12–28

d. Project D:

(1) Depreciation expense per year: ($5,000 – $500) ÷ 5 = $900

Taxable income:

Sales $4,000

Expenses:

Cash expenditures $1,500

Depreciation 900 2,400

Operating income before tax $1,600

Income tax (25%) 400

Operating income after tax $1,200

e. Net Present Values (@8%), rounded:

Project a: ($1,800 x 3.993) – $5,000 =

$7,187 – $5,000 = $2,187

Project b:

After-tax 8% Discount Present

Year Cash Flows Factor Values

0 <$5,000>

1 $ 500 0.926 463

2 1,200 0.857 1,028

3 2,000 0.794 1,588

4 2,500 0.735 1,838

5 2,000 0.681 1,362

Net Present Value (NPV) = $1,279

Chapter 12 – Strategy and the Analysis of Capital Investments

12–29

12–38 Straightforward Capital Budgeting with Income Taxes (Non-MACRS-based

Depreciation) and Sensitivity Analysis (20-25 minutes)

1. Depreciation per year, SL basis: ($30,600 – $600) ÷ 6 years = $5,000

Taxable income $8,000 – $5,000 = 3,000

Tax rate × 40%

Income taxes $1,200

2. Payback period: $30,600 ÷ $5,000* = 6.12 years (if cash flows are assumed to

*Given/assumed.

3. PV of annual after-tax cash savings $5,000 × 4.623* = $23,115

PV of salvage value $ 600 × 0.63** = 378

*From Appendix C, Table 2

**From Appendix C, Table 1

4. The minimum net after-tax annual cost savings needed to justify this investment =

$6,537

Let X = minimum after-tax annual cost savings, and let NPV = 0. The Initial

Investment Outlay ($30,600) is reduced by the PV of the salvage value of the asset

@ an 8% discount rate (i.e., $378). Thus, when NPV = $0, we have (by definition):

PV of After-tax Cash Inflows = PV of Cash Outflows

(or, an increase of approximately 31% over the $5,000 amount given assumed

above in 2 and 3)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–30

12-39 Capital Budgeting with Tax, Non-MACRS Depreciation, and Sensitivity

Analysis (30-35 minutes)

Annual after-tax net cash inflow:

Cash revenue, net of tax $1,200 × (1 – 0.35) = $780

1. Under the assumption that the cash inflows occur evenly throughout the year,

the payback period for the proposed investment is:

2. Estimated Operating Income per year:

Sales $1,200

Depreciation 600

3. The maximum initial investment is such that the project at

this level of investment would yield a NPV = $0 (i.e., a situation where PV of cash

inflows = PV of cash outflows). Alternatively, we’re looking for the maximum level of

4. Required annual (pre-tax) cash revenue:

Given an initial investment outlay of $6,000, the after-tax

annual cash flow needed per year to generate a return

of 15% = $6,000 ÷ 5.019 = $1,195

Less: Annual Tax savings on depreciation expense = 210