Chapter 11 – Decision Making with a Strategic Emphasis

11–61

future service demand? (Would negative media coverage reduce

demand?)

• Does the existing cleaning compound create a hazardous work

environment for employees (the problem is silent on this issue)?

• If the existing cleaning compound is considered hazardous to

employee well-being, is there an effect on employee absenteeism?

• Duncan’s business essentially consists of two service lines/segments:

emission requirements?

Chapter 11 – Decision Making with a Strategic Emphasis

11–62

11–40 Profitability Analysis; Excel (80 min)

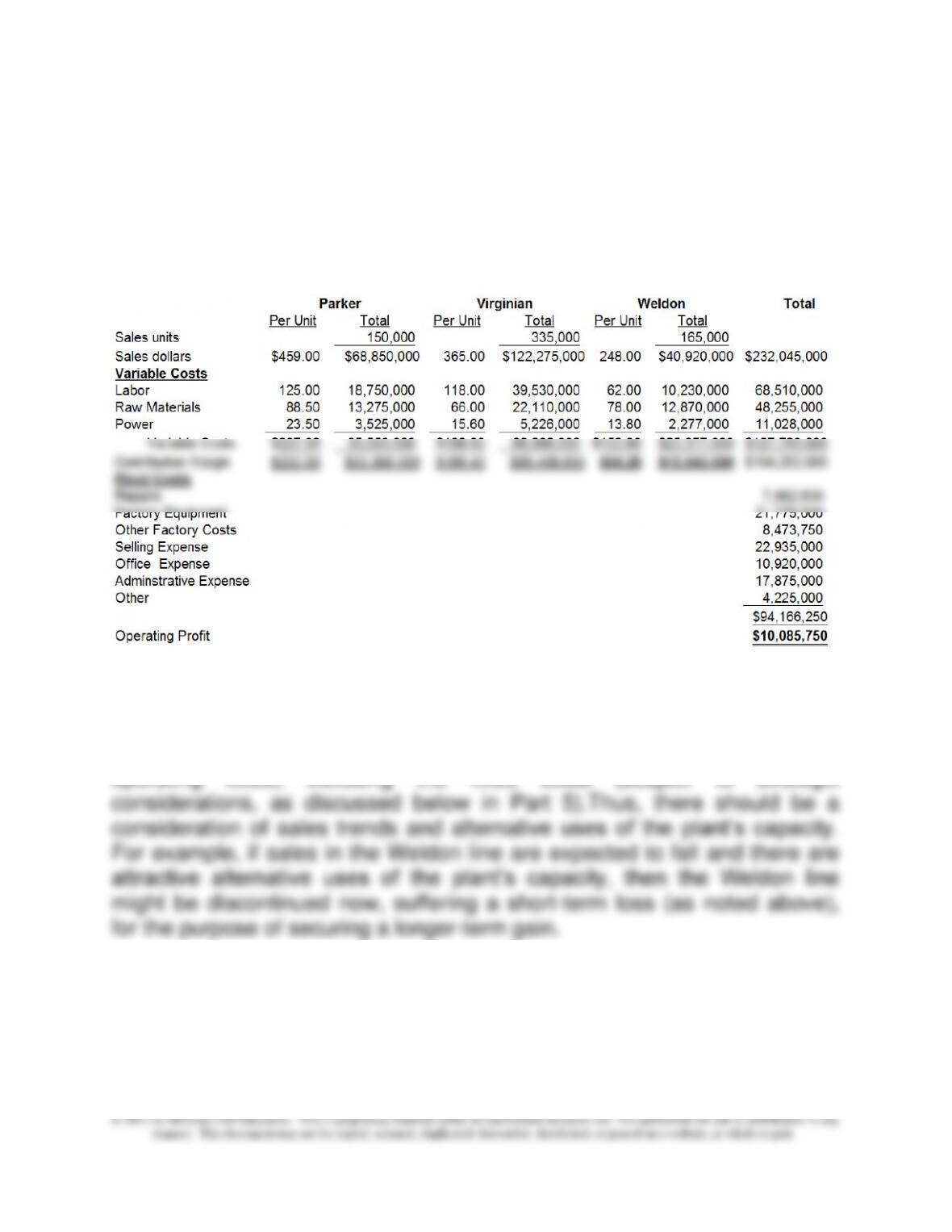

1. The profit report Hal is using is not contribution-based, so the first step

is to produce a contribution income statement for the three product lines, as

shown below. Note that fixed costs are not allocated to the product lines

since they are irrelevant to the short-term profitability analysis.

The analysis shows that all three lines have a positive contribution margin,

including the Weldon line. The short-term financial effect of dropping the

Weldon line would be the loss of $15,543,000 contribution. For a longer-

term perspective, Hal should expect the Weldon product to cover the full

operating costs, including the fixed costs (subject to strategic

Chapter 11 – Decision Making with a Strategic Emphasis

11–63

2. Since the Weldon product has a positive contribution margin of $94.20

per unit, the total contribution margin will be positive irrespective of the

Chapter 11 – Decision Making with a Strategic Emphasis

11–64

11-40 (continued-1)

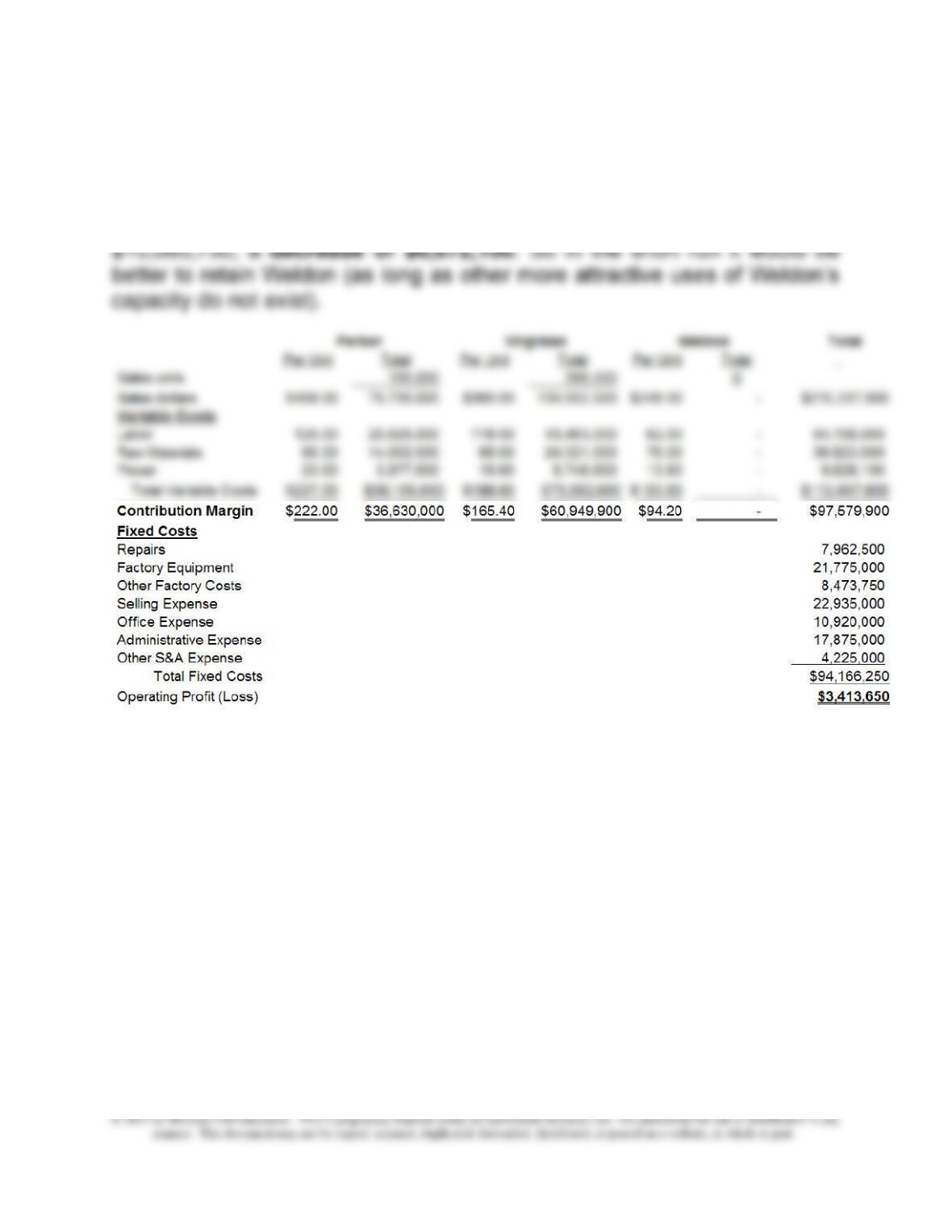

3. The 10% sales increase has total sales of 165,000 units for Parker and

368,500 units for Virginian. The analysis for dropping Weldon is as follows.

The new total profit of $3,413,650 falls short of the profit with Weldon,

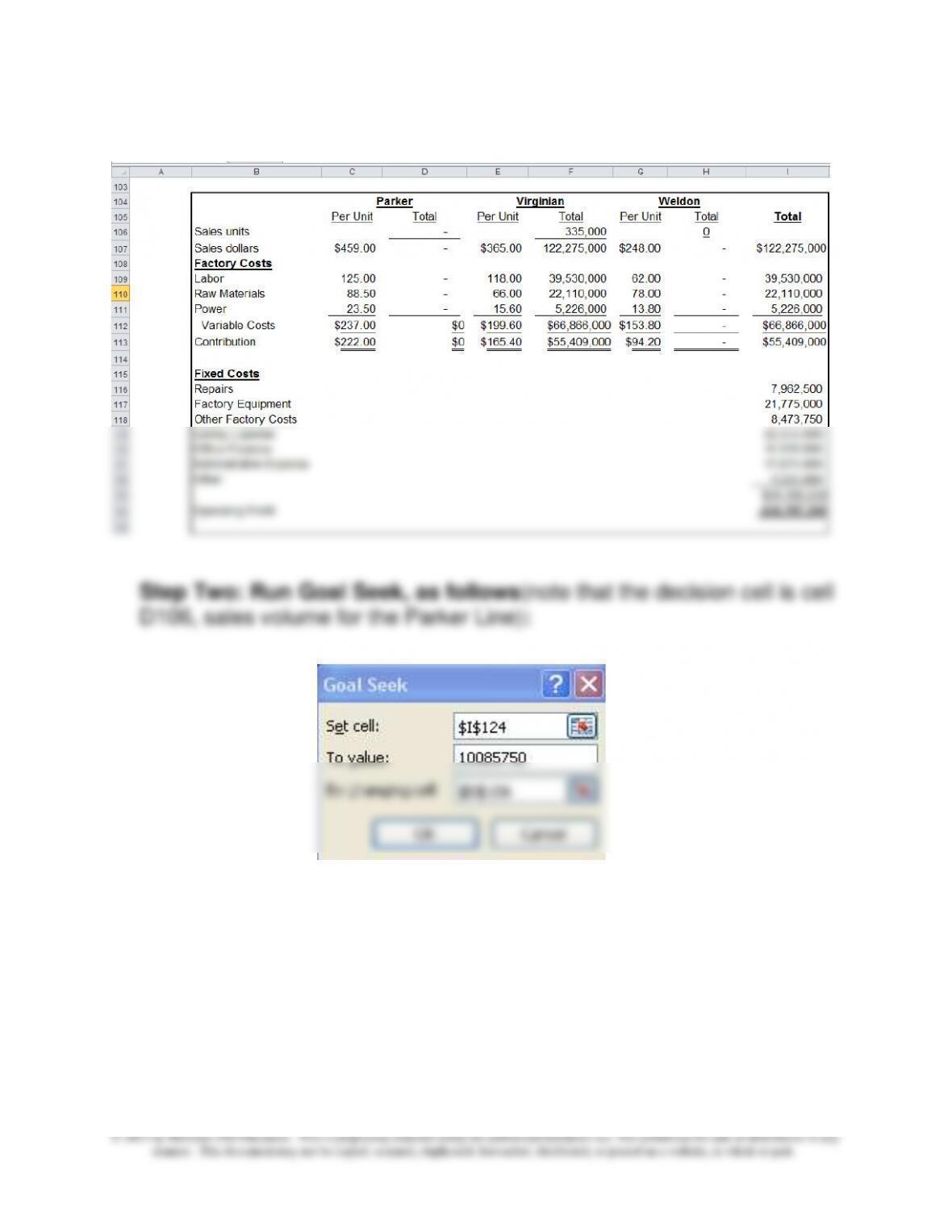

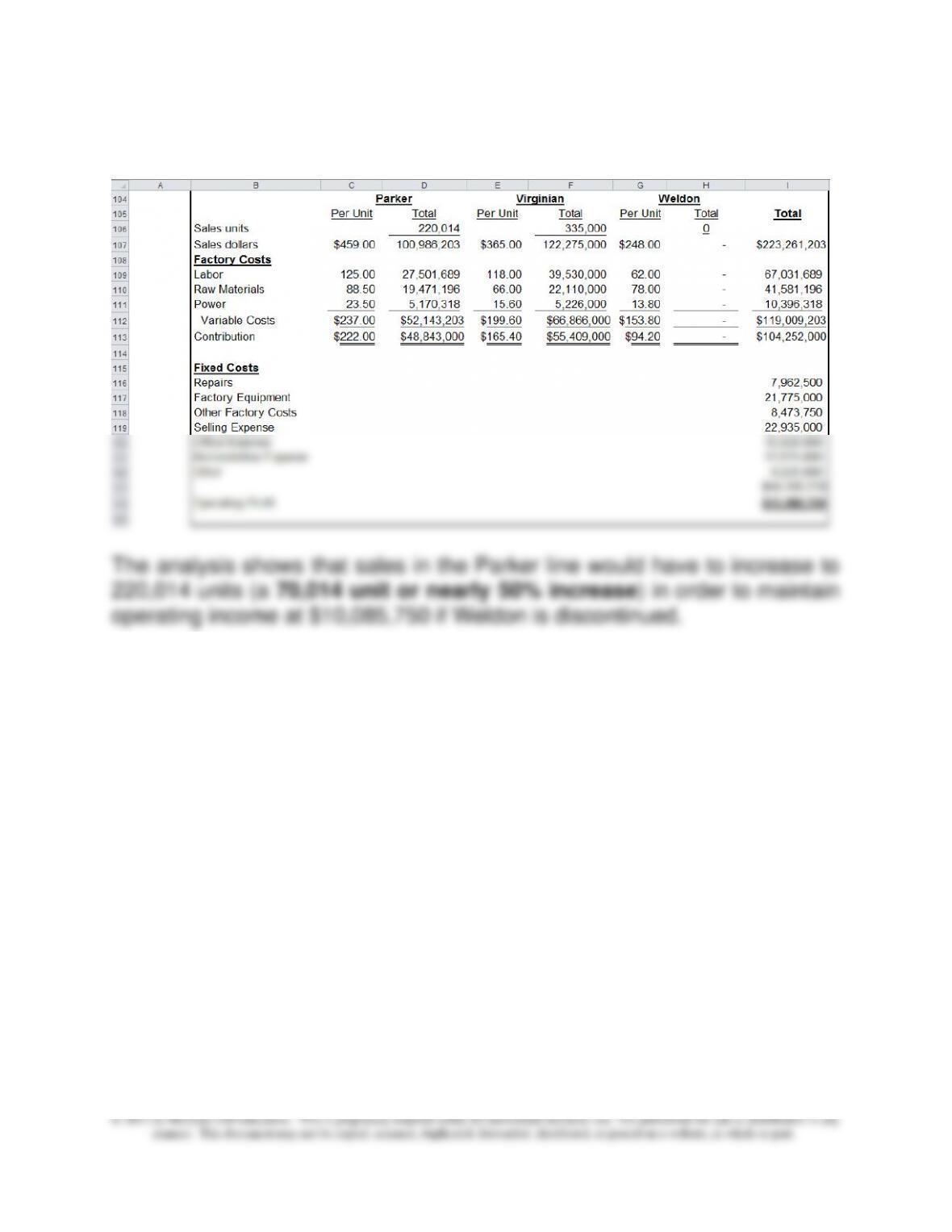

4. Required increase in sales from the Parker line (to compensate

elimination of Weldon line):

Step One: Create the Contribution Income Statement in Part 3 above.

(That spreadsheet occupied B104:I124.) Enter a zero into cell D106 and

335,000 into cell F106. Afterwards, you should see the following:

Chapter 11 – Decision Making with a Strategic Emphasis

11–65

11-40 (continued-2)

Step Three: Results (see below)

Chapter 11 – Decision Making with a Strategic Emphasis

11–66

11–40 (continued-3)

5. HPF competes on the basis of quality and innovation, a differentiation

strategy. The decision about the Weldon line should therefore include how

the line contributes to the firm’s image of quality and innovation. Will the

loss of the line cause HPF’s customers to reduce their perceptions of

HPF’s quality and innovation?

11–67

11–41 Profitability Analysis (45 min)

1. First, calculate the contribution margin per unit for traffic and commercial

paint.

The first step is to determine the unit cost of latex, as follows:

Traffic Paint: (450 lbs. × $32.00/lb.) ÷ 1,000 gallons = $14.40 per gallon

Commercial Paint: (325 lbs. × $32.00/lb.) ÷ 1,000 gallons = $10.40

per gallon

The per-unit contribution margins are then determined as follows:

Traffic Commercial

Selling price/gallon $20.0000 $24.0000

Direct materials costs:

Latex $14.4000 $10.4000

Camelcarb $0.7600 $1.0800

Silica $0.7400 $1.0400

Pigment $0.2400 $0.7600

Other ingredients $0.1200 $0.0600

Direct labor cost $0.9200 $1.7000

Freight $1.5600 $0.8600

Total variable cost $18.7400 $15.9000

Contribution margin $1.2600 $8.1000

Using the above contribution margin per unit figures, the total

contribution margin for each scenario can be determined as follows,

where total traffic paint = 342,000 gallons (i.e., 380,000 gallons × 0.90),

and total commercial paint = 38,000 gallons (i.e., 380,000 gallons –

342,000 gallons). The loss of the Virginia contract would reduce the

traffic paint to 254,000 gallons (i.e., 342,000 gallons – 88,000 gallons).

A doubling of commercial paint (using the promotion) would result in

76,000 gallons (i.e., 38,000 gallons × 2).

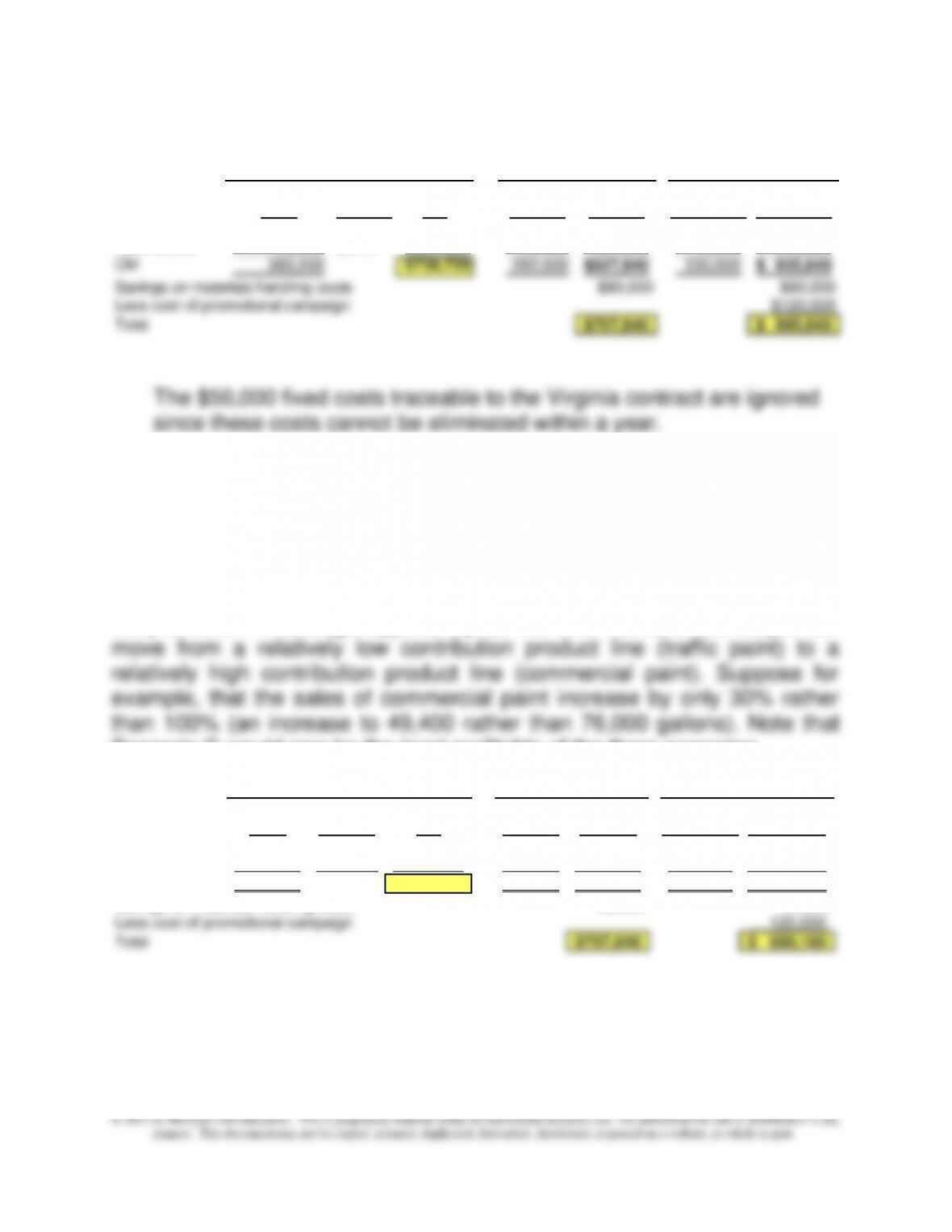

Chapter 11 – Decision Making with a Strategic Emphasis

11–68

Problem 11-41 (continued-1)

Original Original Units w/o CM w/o Units with CM with

units CM/unit CM Virginia Virginia promotion promotion

Traffic 342,000 $1.26 $430,920 254,000 320,040$ 254,000 320,040$

Commercial 38,000 $8.10 $307,800 38,000 307,800 76,000 615,600

CM 380,000 $738,720 292,000 627,840$ 330,000 935,640$

Savings on materials handling costs $80,000 $80,000

Less cost of promotional campaign $120,000

Total 707,840$ 895,640$

Scenario A

Scenario B

Scenario C

2. The proposed promotional campaign without the Virginia contract,

scenario C, has the greatest contribution margin, as shown in the

calculations above. Strategic issues for the decision between scenario B

and scenario C include the reliability of the projected sales-volume increase

in commercial paint and of the assumption that the volume of commercial

paint can be doubled without increasing fixed costs, other than the cost of

the promotion. A strategic opportunity, on the other hand, is that Meyer can

Scenario C would now be the least profitable of the three scenarios.

Original Original Units w/o CM w/o Units with CM with

units CM/unit CM Virginia Virginia

promotion

promotion

Traffic 342,000 1.2600$ 430,920$ 254,000 320,040$ 254,000 320,040$

Commercial 38,000 8.1000 307,800 38,000 307,800 49,400 400,140

CM 380,000 738,720$ 292,000 627,840$ 303,400 720,180$

Savings on materials handling costs 80,000 80,000

Less cost of promotional campaign 120,000

Total 707,840$ 680,180$

Scenario A

Scenario B

Scenario C

11–69

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

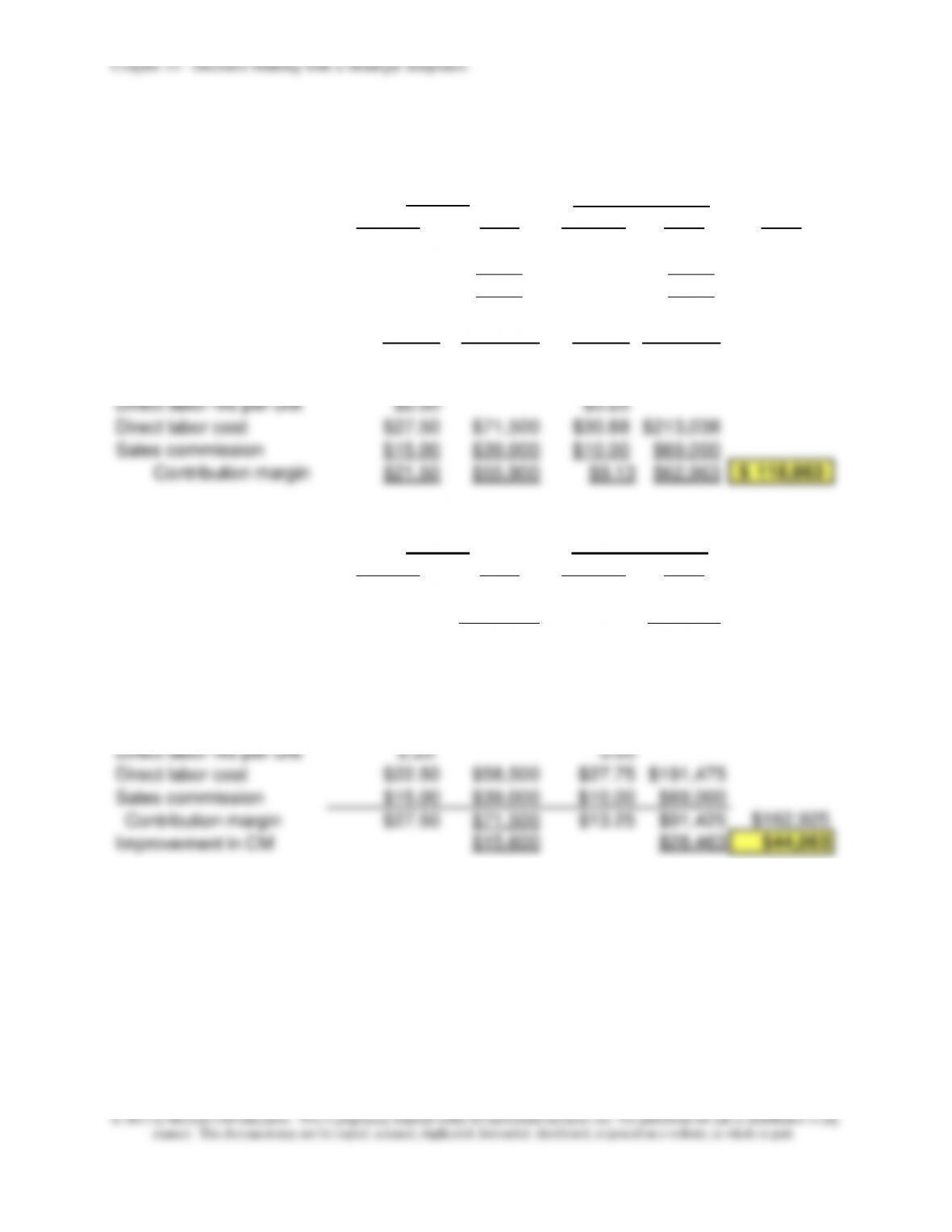

11–42 Project Analysis: Sales Promotions (45-50 min)

1. The relevant cost analysis follows:

Per Unit Total Per Unit Total

Budgeted Sales 4,000 8,000

Actual Sales 2,600 6,900

Sales Shortfall 1,400 1,100

Sales Value of Shortfall $80.00 $112,000 $61.00 $67,100

Direct material $16.00 $22,400 $11.00 $12,100

Direct labor rate per hr $11.00 $9.50

Direct labor hrs per unit $2.50 $3.25

Direct labor cost $27.50 $38,500 $30.88 $33,963

Sales commission $15.00 $21,000 $10.00 $11,000

Contribution margin $21.50 $30,100 $9.13 $10,038

Cost of Prize $16,500 $12,500

Excess of CM over cost 13,600$ (2,463)$

Second contest:

Chair and Stool

First contest: Gliders

The Glider contest has a $13,600 positive contribution margin net of

the estimated cost of the prize. On the other hand, the Chair-and-

Stool Set contest has a negative contribution of $2,463. Note that the

above solution uses actual rather than budgeted price and cost

information.

The analysis below compares the contribution margin for each

product based on actual sales volume at actual cost, actual

selling price, and actual resource usage to the product contribution

Thus, strategically, it is important for Hillside to focus on cost

management as well as improving sales.

11–70

11-42 (continued-1)

Based on Actual Sales Volume, Actual Resource Usage, and Actual Cost Data

Per Unit Total Per Unit Total Total

Budgeted Sales 4,000 8,000

Actual Sales 2,600 6,900

Sales Shortfall 1,400 1,100

Actual Sales $80.00 $208,000 $61.00 $420,900

Direct material $16.00 $41,600 $11.00 $75,900

Direct labor rate per hr $11.00 $9.50

Direct labor hrs per unit $2.50 $3.25

Direct labor cost $27.50 $71,500 $30.88 $213,038

Sales commission $15.00 $39,000 $10.00 $69,000

Contribution margin $21.50 $55,900 $9.13 $62,963 118,863$

Gliders

Chair and Stool

Per Unit Total Per Unit Total

Budgeted Sales 4,000 8,000

Actual Sales 2,600 6,900

Sales Shortfall 1,400 1,100

Actual Sales $80.00 $208,000 $61.00 $420,900

Direct material $15.00 $39,000 $10.00 $69,000

Direct labor rate per hr $10.00 $9.25

Direct labor hrs per unit 2.25 3.00

Direct labor cost $22.50 $58,500 $27.75 $191,475

Sales commission $15.00 $39,000 $10.00 $69,000

Contribution margin $27.50 $71,500 $13.25 $91,425 $162,925

Improvement in CM $15,600 $28,463 $44,063

Based on Actual Sales and Budgeted Usage and Cost Data

Gliders

Chair and Stool

Chapter 11 – Decision Making with a Strategic Emphasis

11–71

11–42 (continued-2)

2. Some strategic factors that should be considered:

• The contest appears to reward an increase of sales in units.

However, the average sales price for each product has already

fallen below budgeted levels. If the contest provides an

expected incentive to reduce price in order to increase sales,

then the result could be lower contribution margins than

expected. Moreover, the price cutting could have adverse long-

term effects. Hillside should carefully consider its short-term

and long-term pricing strategy to make sure it is consistent with

• An unintended effect of the sales contests is that certain retail

customers might buy unusually large orders, at the urging of

sales people, and that some portion of these order might

eventually be returned if not sold by the retailer by the end of

the season.

• While sales of the table are over budget, why does the sales

Chapter 11 – Decision Making with a Strategic Emphasis

11–72

11–43 Profitability Analysis; Pro Forma Income Statement (60 min)

1. The dollar value of DimLok’s present annual fixed costs is calculated

as follows:

Profit target based on 20% of annual fixed costs = $ 800,000

Total fixed costs = $800,000 ÷ 0.20 = $4,000,000

2. DimLok must sell 64,000 units in order to achieve both profit

objectives of 20 percent return on fixed costs and $20 per unit sold.

Supporting Calculations

First: The solution must consider the following constraints:

• 40,000 unit capacity for the current facility.

• $1,000,000 additional fixed charge for production up to 80,000

demonstrated by the following calculations:

Contribution margin per unit below the 40,001 unit level

= $200 selling price per unit − ($80 variable cost per unit + $20

profit per unit)

= $100 contribution margin per unit

Calculation of the number of units to achieve the desired profit

objectives

Chapter 11 – Decision Making with a Strategic Emphasis

11–73

11–43 (continued-1)

Third: Thus, in order to achieve the profit targets, DimLok must

increase plant capacity, thus incurring an additional $1,000,000 in

fixed costs. This, in turn, increases the profit target based on fixed

costs to a total of $1,000,000 (i.e., 0.20 × [$4,000,000 + $1,000,000]),

as follows:

= $180 selling price − ($80 variable cost per unit + $20 profit per unit)

= $80 contribution margin per unit

Recalculation of the number of units to achieve overall profit

objectives:

Fourth: The contribution margin per unit for production in the 60,000

to 80,000 unit range, with the variable cost per unit reduced to $60

per unit, is determined as follows:

Chapter 11 – Decision Making with a Strategic Emphasis

11–74

11–43 (continued-2)

Finally, the calculation of the number of units (X) needed to achieve

overall profit objectives

(Fixed charges + desired profit) = total contribution margin

3. DimLok Division

Pro Forma Income Statement

Revenue

40,000 units × $200/unit = $8,000,000

24,000 units × $180/unit = 4,320,000 $12,320,000

Variable costs

60,000 units × $80/unit = 4,800,000

4,000 units × $60/unit = 240,000 5,040,000

Contribution Margin 7,280,000

4. DimLok has a competitive strategy based on differentiation. The

differentiation is based on the secret process that DimLok has

developed and an advertising program that stresses completely new

5. Critical success factors for DimLok include research and development

(R&D) to maintain the technological advantage of their unique

products, and strong advertising programs to stress the firm’s

differentiation based on innovation. Other strategic success factors to

Chapter 11 – Decision Making with a Strategic Emphasis

11–75

No Frills Standard Super

Model Options Model

Selling price/unit $35 $60 $80

Less: CGS

DM cost/unit $9 $11 $14

DL cost/unit $10 $20 $30

Variable overhead cost/unit $3 $6 $9

maintain product differentiation include quality of production and

customer service.

11–44 Product Profitability Analysis, Scarce Resources (45 min)

1. Fixed manufacturing overhead costs, in total, are by definition

capacity-related costs and as such are not expected to change in the

short run. Thus, in total, short-term fixed costs should be independent

of production volume and production mix. On the other hand, variable

to the short-term product-mix decision.

2. Gross profit per unit and contribution margin per-unit figures:

the presence of resource constraints (or limitations), logic dictates that

we allocate available resources “to their most profitable use.” In this

case, this means on the basis of the contribution margin per unit of the

scarce resource(s). These amounts are provided in Parts 3 and 4

below.

3. In the presence of a single resource constraint, we should focus on

those products that provide the greatest contribution margin per unit of