Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–11

• Competence: The competence standard binds IMA members to “provide decision

support information and recommendations that are accurate.” Will Mary violate the

the credibility standard if she doesn’t object to Michael’s reporting, which she

believes is biased?

III. Learning Objective: Recognition and evaluation of ethical situations.

Students should recognize that ethical dilemmas have no right or wrong answer and that they

must be able to identify the possible courses of action, outcomes, and consequences before

selecting their “best” solution.

Suggested Questions:

1. What are the possible courses of action Mary can follow? What are the potential

consequences of each course of action, and who are the affected parties?

2. What course of action should Mary follow? Defend your answer.

Possible Solutions:

• Mary can go along with her current boss, Michael. All of the current branch

employees who fall under the bonus plan, including Mary and Karl, will receive

longer at the branch. The morale of the branch employees may be affected because

they are expecting higher bonuses than they will receive.

• Mary can talk to Paul Parker, Michael’s supervisor. Even though Parker has a

reputation for strict adherence to the chain of command, Mary can approach Parker

extremely uncomfortable. This has serious potential consequences for her career,

which are exacerbated by the lack of comparable jobs in her current location in

Texas.

• Mary can contact Karl to inform him of the problem and ask his advice. But any

advice he gives must be viewed with the understanding that Karl is motivated by the

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–12

Note: Students may select any of the above or another solution, with the appropriate

defense, as their suggested course of action.

Potential Additions to the Assignment Questions:

1. Does it make a difference that IFS is a multinational public company? Would you

change your selected solution if the company was private?

2. Are the dollar values of the bonuses relevant? Would you make a different

determination if there were no employee bonuses involved?

3. Would you recommend that IFS modify its performance measurement system? Why

and how?

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–13

Teaching Strategies for Readings

18-1 Implementing Sustainability: The Role of Leadership and Organizational Culture

The project upon which the article is based is a research project funded by the Institute of Management

Accountants (IMA). Suggested solutions for each of the discussion questions follow:

1. What is the difference between local and corporate decision making, and what is the significance

of the difference for sustainability?

In the article, Epstein et. al. refer to local versus corporate decision making. Local decision making is

done at the level of business units, geographical units (such as the State of Ohio), or facilities. The

corporate level is at the company headquarters. The difference is important because, as the article

suggests, many sustainability-related decisions are made at the local level where managers in day-to-day

operations make trade-off between environmental issues, speed of operations, cost, and other aspects of

their local operations. The Chief Executive Officer (CEO), Chief Financial Officer (CFO), and perhaps

the Chief Operating Officer (COO) or executive responsible for corporate sustainability goals will set the

tone and the objectives, but ultimately many of the decisions that involve sustainability are made at the

local level.

Corporate decisions would include the decision to replace a fleet of less efficient vehicles with more

efficient vehicles, or to refit a plant for more efficient manufacturing and reduced energy usage.

Corporate decisions have a significant impact in these large scale decisions, while local decisions have an

important cumulative impact of supporting sustainability goals day by day.

2. Study the Corporate Sustainability Model in Figure 1. Based on this study, do you think

sustainability should be managed by means of a cost center, profit center, the balanced scorecard,

or some other method, and why?

Each of these options could be supported in some ways. The cost center would be appropriate for an

organization that is managing its sustainability program as a management function, much like other

management functions such as legal, accounting, or human resources. In this case, the cost center is

likely to be a discretionary cost center in which the processes of the center are well identified and

supported by an appropriate annual budget.

A profit center approach would recognize that, as many companies have discovered, the efforts to

improve sustainability have a positive impact on profitability. In this case, a variation of the cost center,

the processes of the center are carefully defined. The difference is that the sustainability profit center is

expected to provide improvements in operations that reduce cost and/or enhance revenue, ultimately at a

rate greater than the cost of operating the sustainability center.

The balanced scorecard (BSC) approach is probably the most practical, since sustainability goals can

often be readily identified in specific measurable operational improvements. The role of the BSC is to

track progress on these goals, so that managers can promptly and effectively move their operational

processes in the direction of greater sustainability. The BSC approach can also incorporate costs and

profits; these financial measures could simply be part of the scorecard along with the environmental and

other sustainability measures.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–14

3. Identify two of the leading companies in the area of sustainability and explain why you think each

of these companies has chosen to take a leadership role in sustainability.

The article identifies four companies: Nike, Procter & Gamble (P&G), The Home Depot and Nissan. The

articles notes that these companies have a reputation for leadership in sustainability and therefore the

authors chose these companies for the research in this IMA research project. At Nike, the sustainability

issue involved the use of environmentally preferred materials which increased the cost of materials but

reduced waste, a net benefit both for the environment and for the company in savings for reduced waste.

At P&G sustainability is achieved through innovation in both the design of the company’s products and

through more efficient manufacturing techniques.

At The Home Depot and Nissan, sustainability was top-down, driven by strategic planning, coordinated

with the business units, with the goal of both corporate responsibility and cost reduction.

4. Review Exhibit 18.4 in the text. Do you think sustainability is best managed as part of an

informal or a formal type of management control system? Briefly explain your answer.

The article notes that, for the companies studied, individual leadership and corporate culture played a key

role in the success of a sustainability effort. Top management and operational management had to be “on

board” with the goals of the sustainability effort.

5. Explain briefly the role of leadership in sustainability management.

Leadership is critical, as noted in the article. Setting a clear tone and policy at the corporate level can

reduce conflicts and miscommunication at the operational level, to improve the implementation of the

sustainability objectives. Leadership played a key role in sustainability for all four of the companies

studied.

6. Explain briefly the role of organization culture in sustainability management.

The company’s culture, throughout the organization also plays a critical role in achieving the company’s

sustainability objectives. At Home Depot for example, the culture of willingness to take a risk and the

passion for customer service ties in very well to what the company as a whole wants to achieve with

sustainability. In the case of P&G, the motto “We always try to do the right thing,” helps to motivate a

culture in which sustainability is achieved and rewarded.

Additional Source: See also an excellent coverage of sustainability at P&G in the article by Cristiano

Busco, Mark. L. Frigo, Emilia L. Leone, and Angelo Riccaboni, “Cleaning Up,” Strategic Finance, July

2010, pp. 29-37.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–15

18-2 Strategy Maps

This article expands Kaplan’s and Norton’s earlier work on the balanced scorecard and strategy maps (see

Article 18-1 above) to the concepts of customer value propositions and the use of the strategy map to

identify how the balanced scorecard can be used to facilitate achieving the desired value proposition.

Discussion Questions:

1. To achieve desired financial goals the organization focuses on which two levers of success?

2. What are the three strategic approaches through which a company can attempt to create sustainable

value for the shareholder?

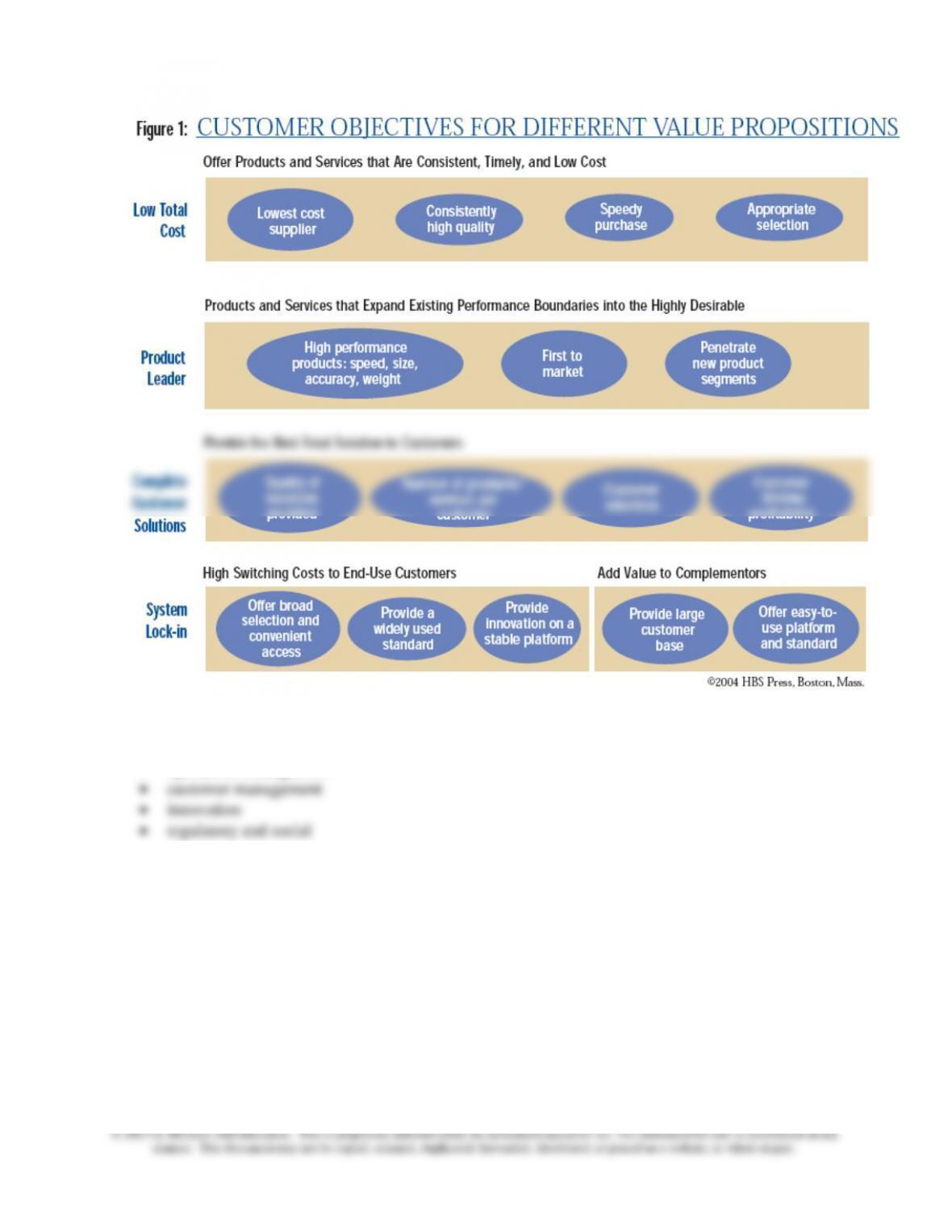

3. What are the four customer value propositions that a company can use to succeed?

• low total cost

lock-in

4. What are the characteristics of firms that compete on the basis of the four customer value propositions

identified above?

These characteristics are identified in Figure 1 (see below):

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–16

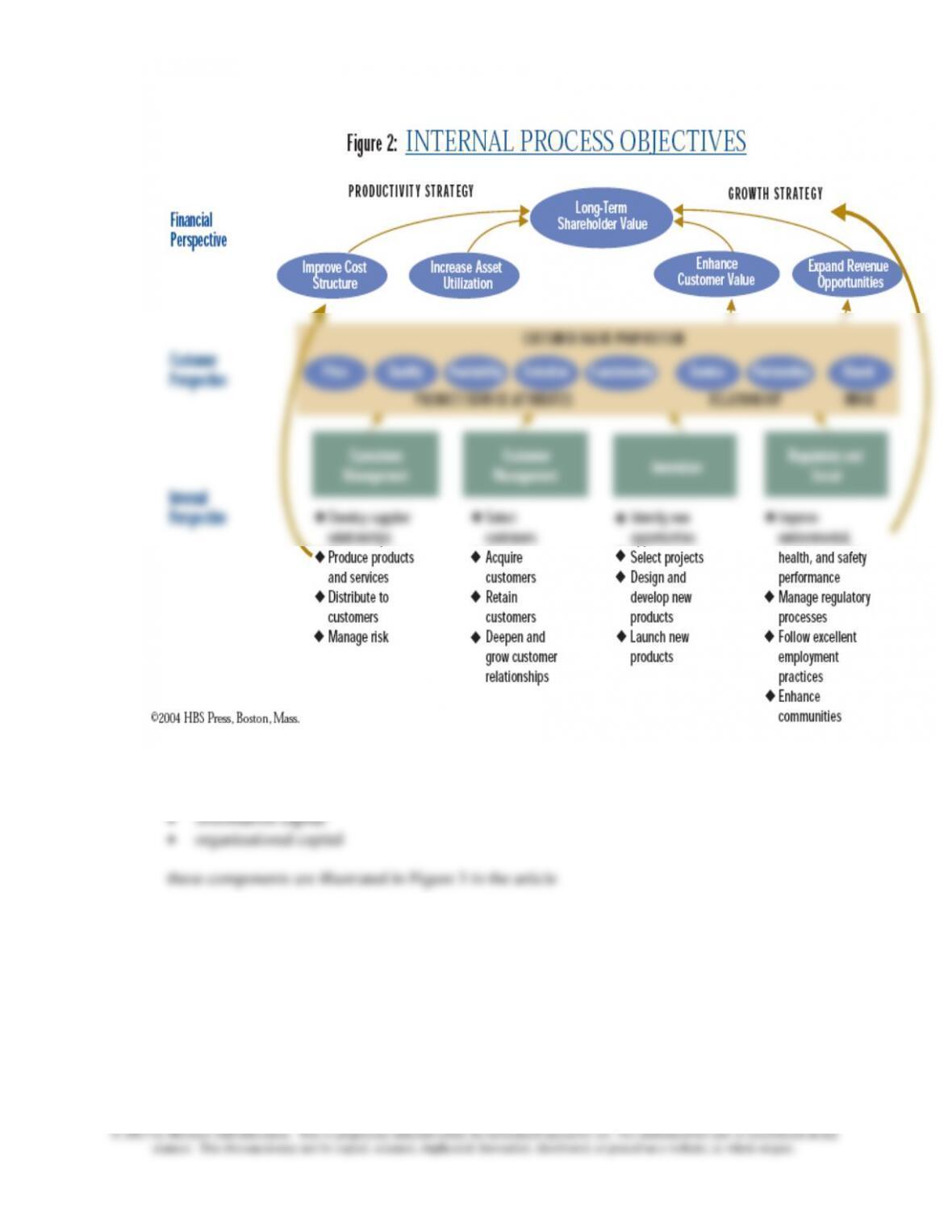

5. What are the four clusters of internal processes through which a company can succeed on the internal

business value proposition:

• operations management

these clusters are illustrated in Figure 2 in the article.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–17

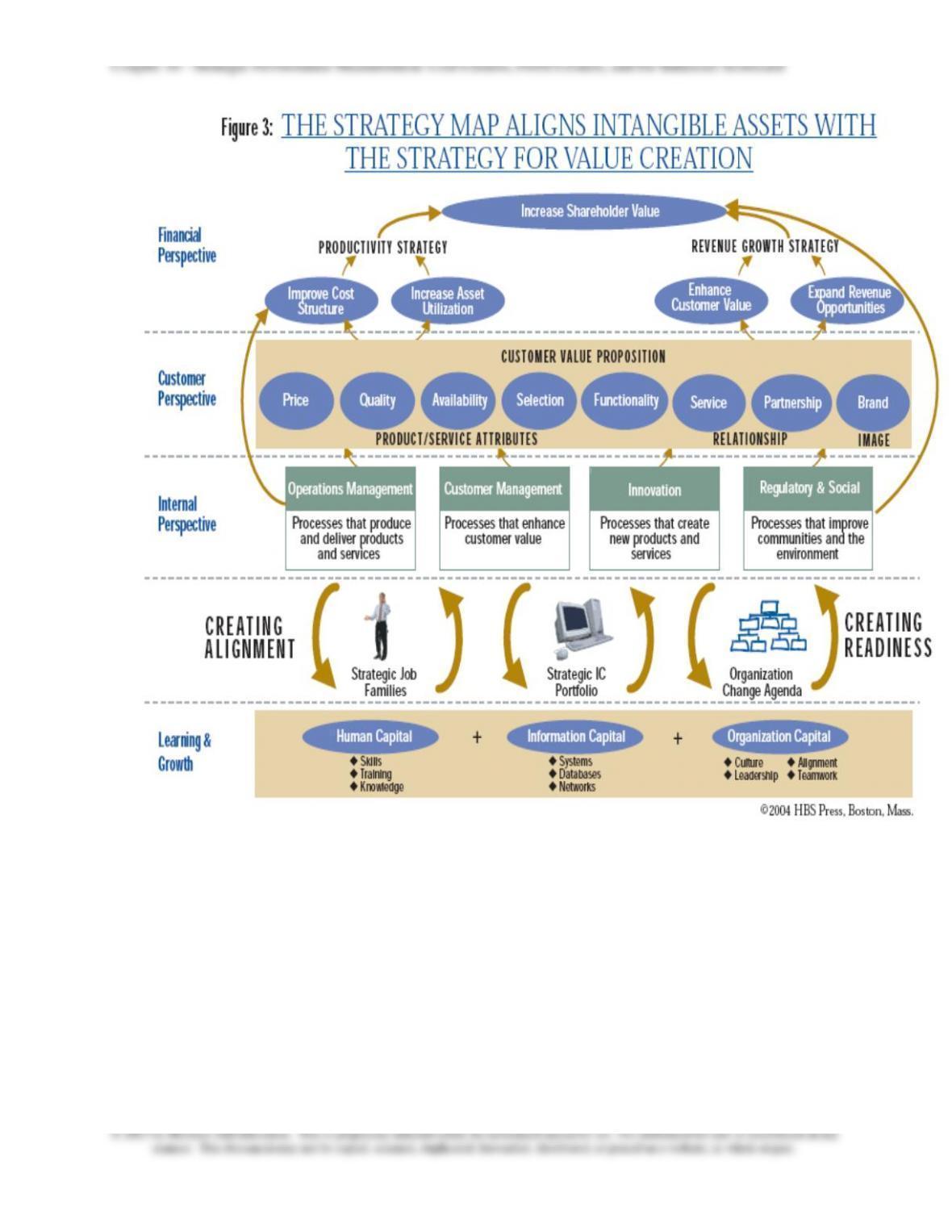

6. What are the three components of the firm’s use of learning and innovation as a value proposition?

• human capital

18–18

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–19

18-3 Evaluating General Managers’ Performances

The article provides a very useful summary of the different measure of performance for general

managers and of the advantages and disadvantages of each measure, relative to a list of key

performance evaluation criteria

Discussion Questions

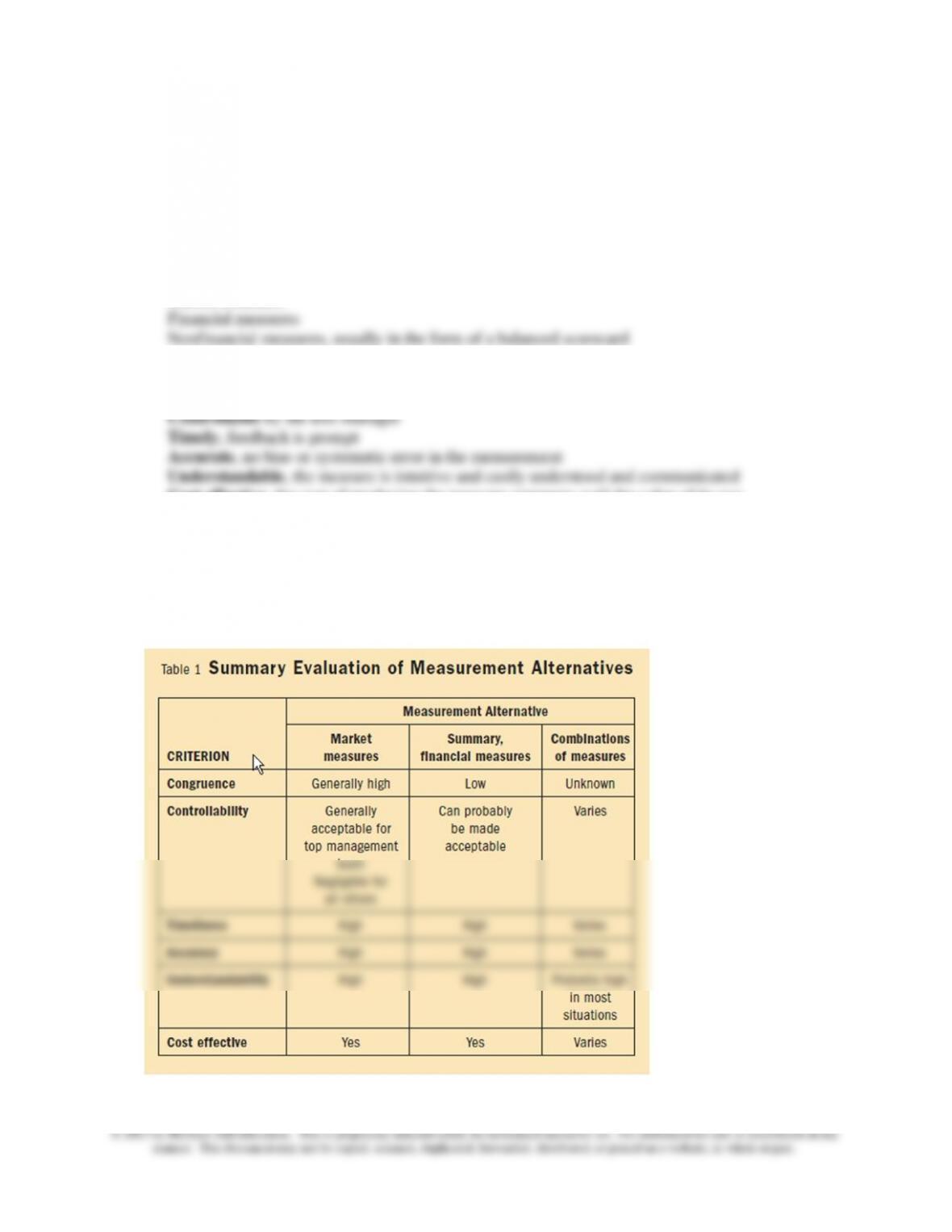

1. What are the key alternative measures of performance for general managers?

Market measures

2. What are the key criteria for evaluating each of the performance measures? Explain each briefly.

Congruence with the organization’s objectives.

Cost effective, the cost of producing the measure compares well the value of its use.

3. How do the alternative measures rank based on the criteria listed in part 2?

See Table 1 below from the article: