Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-31

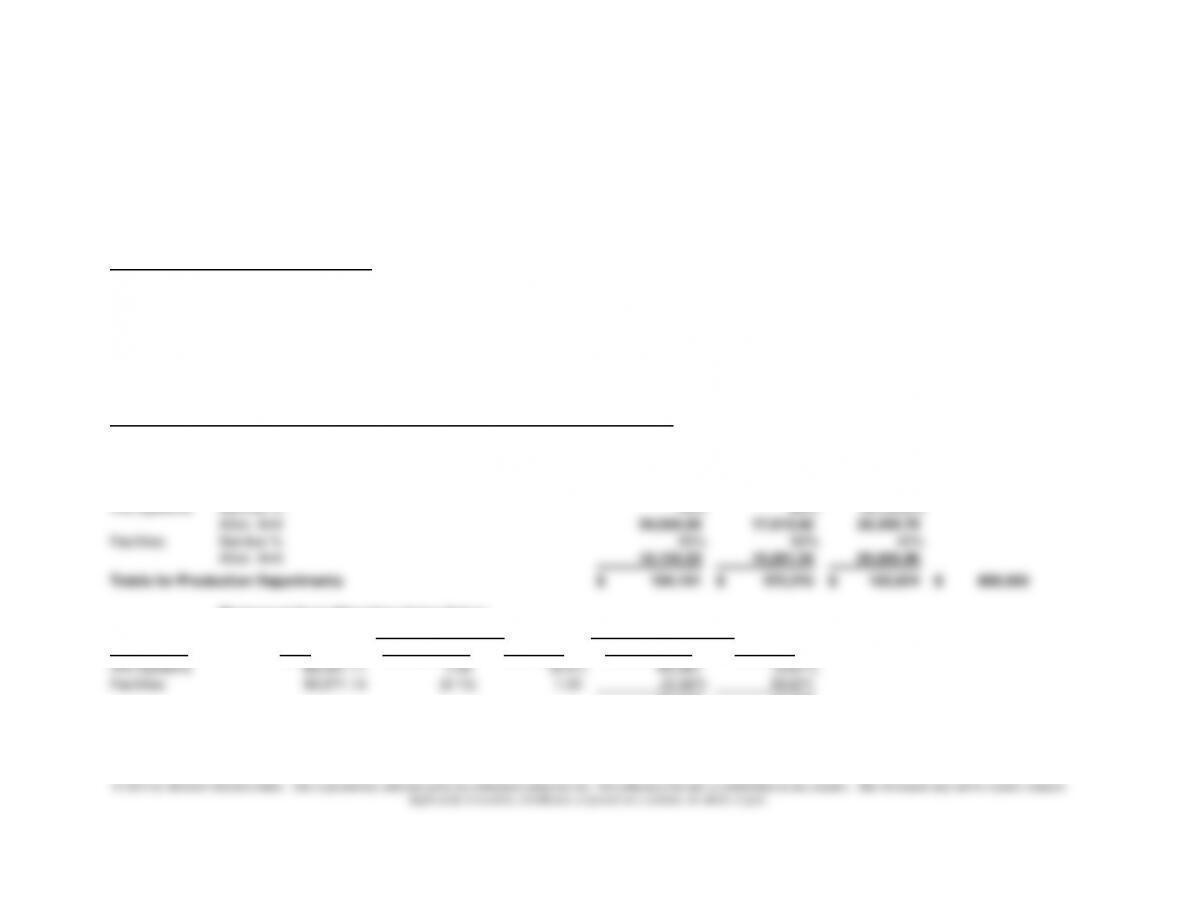

7-35 (continued –3)

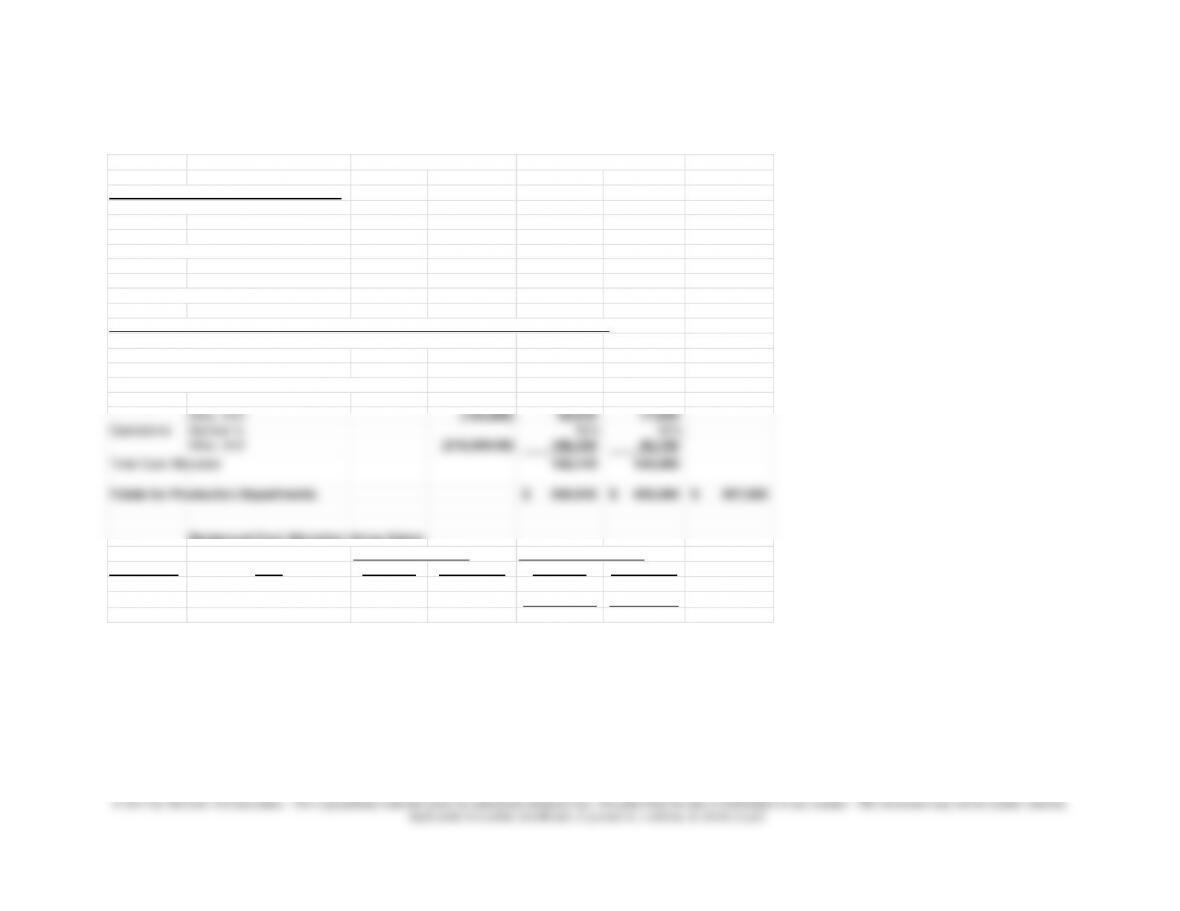

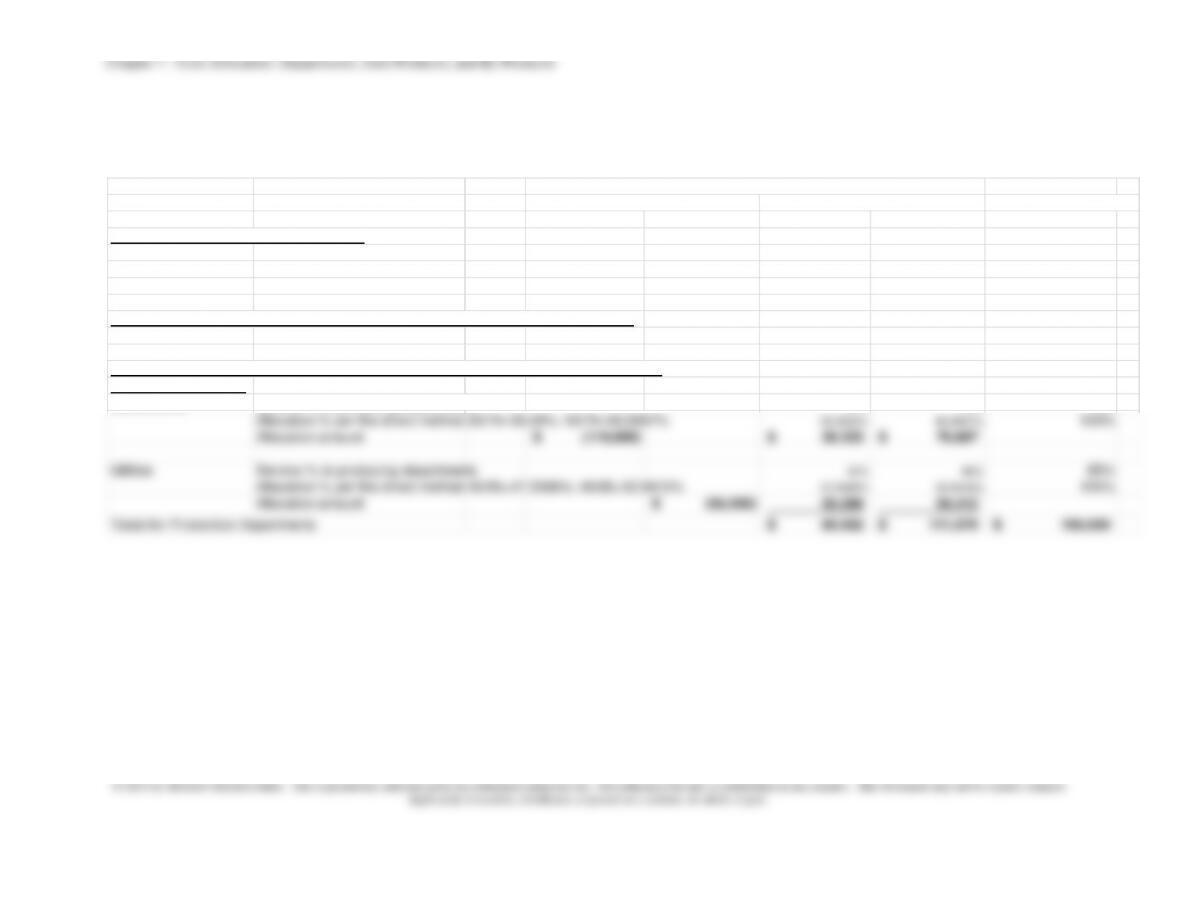

Sourcing Operations Asssembly Finishing Total

DEPARTMENTAL ALLOCATION BASES

Information Systems Hours 25,000 45,000 70,000 140,000

percent 17.8571% 32.1429% 50.00% 100%

Facilities; square feet (000) 10,000 50,000 40,000 100,000

percent 10.00% 50.00% 40.00% 100%

Totals for All Departments 134,000$ 189,000$ 398,500$ 266,000$ 987,500$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

First: Solve the simultaneous equations for Service 1 and Service 2:

Amount Allocated from Info Systems 155,680.00

Amount Allocated from Facilities 216,800.00

Second: Allocate to Producing Departments:

Sourcing Service % 32.1429% 50.0000%

Alloc. Amt (155,680) 50,040 77,840

Operations Service % 50% 40%

Alloc. Amt (216,800.00) 108,400 86,720

Total Cost Allocated 158,440 164,560

Totals for Production Departments 556,940$ 430,560$ 987,500$

Reciprocal Cost Allocation Using Solver

Service Allocated Service Rates To.. Initial Allocation To…

Department Cost Sourcing Operations Sourcing Operations

Sourcing 155,680.00 1.00 (0.1786) 155,680 (27,800)

Operations 216,800.00 (0.10) 1.00 (21,680) 216,800

134,000 189,000

Support Departments

Producing Departments

Note: Equations to Solve (using Solver):

Sourcing = 134,000 + .10 x Operations

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-32

7-36 Departmental Cost Allocation (20 min)

Production

Department

Outside

Price

Percentage

based on

Outside Price

Allocation of Total Maintenance

Cost Using Outside Prices

A

$115,000

25%

$450,000 x .25 = $112,500

B

92,000

20

90,000

C

69,000

15

67,500

D

184,000

40

180,000

Total

$460,000

100

450,000

Departments A and C will be charged more based on the outside

pricing percentage, because the cost of obtaining maintenance

outside the firm is higher for these departments.

2. The overall effect of the new plan will be to motivate the production

departments to continue to use the internal supplier of maintenance

when the outside price is high (as in Departments A and C), and

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-33

7-37 Departmental Cost Allocation (30 min)

The Direct Method:

CFL Group Computer Market Res. Financial Analysis

Total

DEPARTMENTAL ALLOCATION BASES

CFL Group percent 20.00% 60.00% 20.00% 100%

Computer percent 12.00% 48.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 450,000$ 750,000$ 1,000,000$ 1,500,000$ 3,700,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

CFL Group Service % to producing departments 60.00% 20.00%

Allocation % per the direct method 75.0% 25.0%

Allocation amount (450,000)$ 337,500$ 112,500$

Computer Service % to producing departments 48.00% 40.00%

Allocation % per the direct method 54.5455% 45.4545%

Allocation amount (750,000)$ 409,091 340,909

Totals for Production Departments 1,746,591$ 1,953,409$ 3,700,000$

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

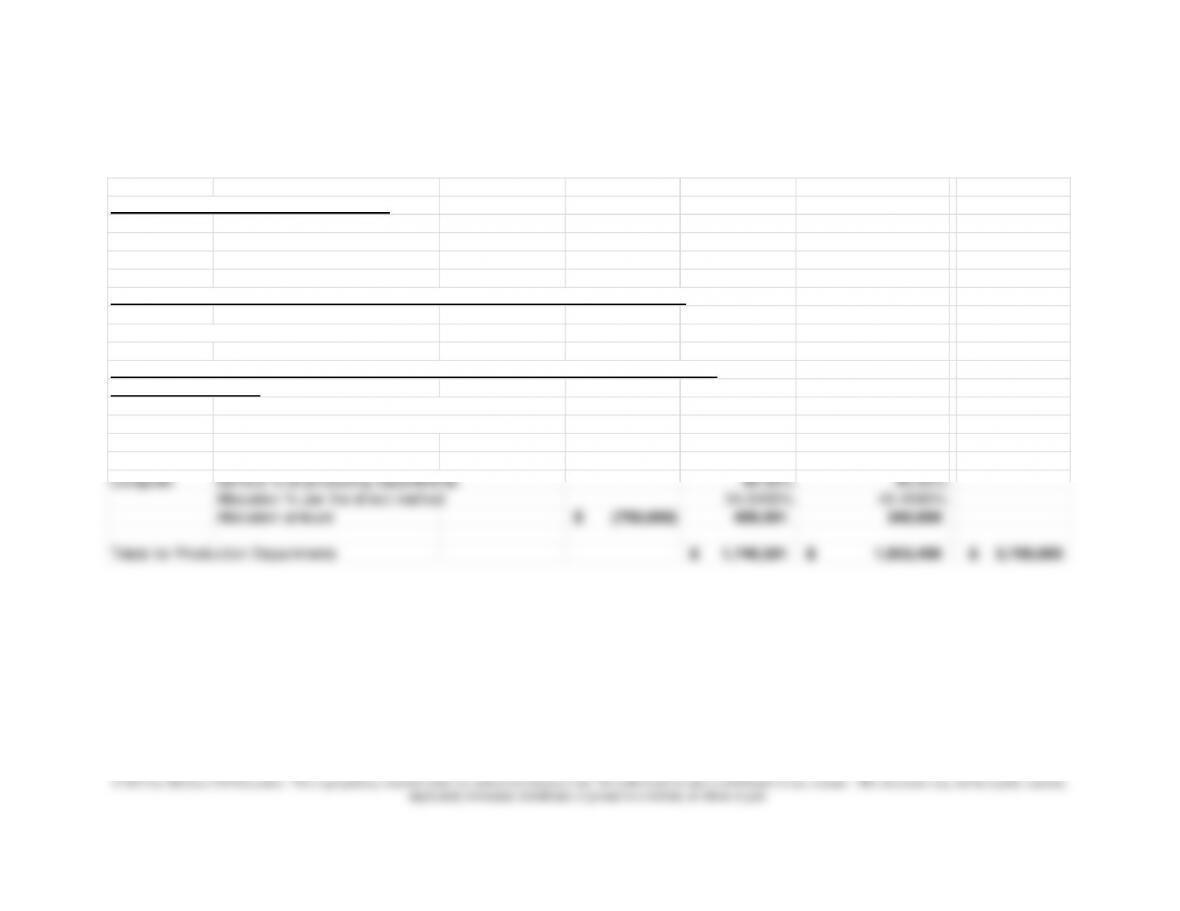

7-37 (continued –1)

The Step Method

The CFL department goes first because it has a higher estimated percentage of dollars work for

the computer group (20%) relative to the computer group’s service to CFL (12%)

CFL Group Computer Market Res. Financial Analysis

Total

DEPARTMENTAL ALLOCATION BASES

CFL Group

percent 20.00% 60.00% 20.00% 100%

Computer

percent 12.00% 48.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 450,000 750,000 1,000,000 1,500,000 3,700,000

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

CFL Group Service % 20.00% 60.00% 20.00%

Amount (450,000) 90,000 270,000 90,000

Second Step

Computer Service % 48.00% 40.00%

Allocation percent per direct method 54.5455% 45.4545%

Amount (840,000.00) 458,182 381,818

Totals for Production Departments 1,728,182$ 1,971,818$ 3,700,000$

Support Departments

Producing Departments

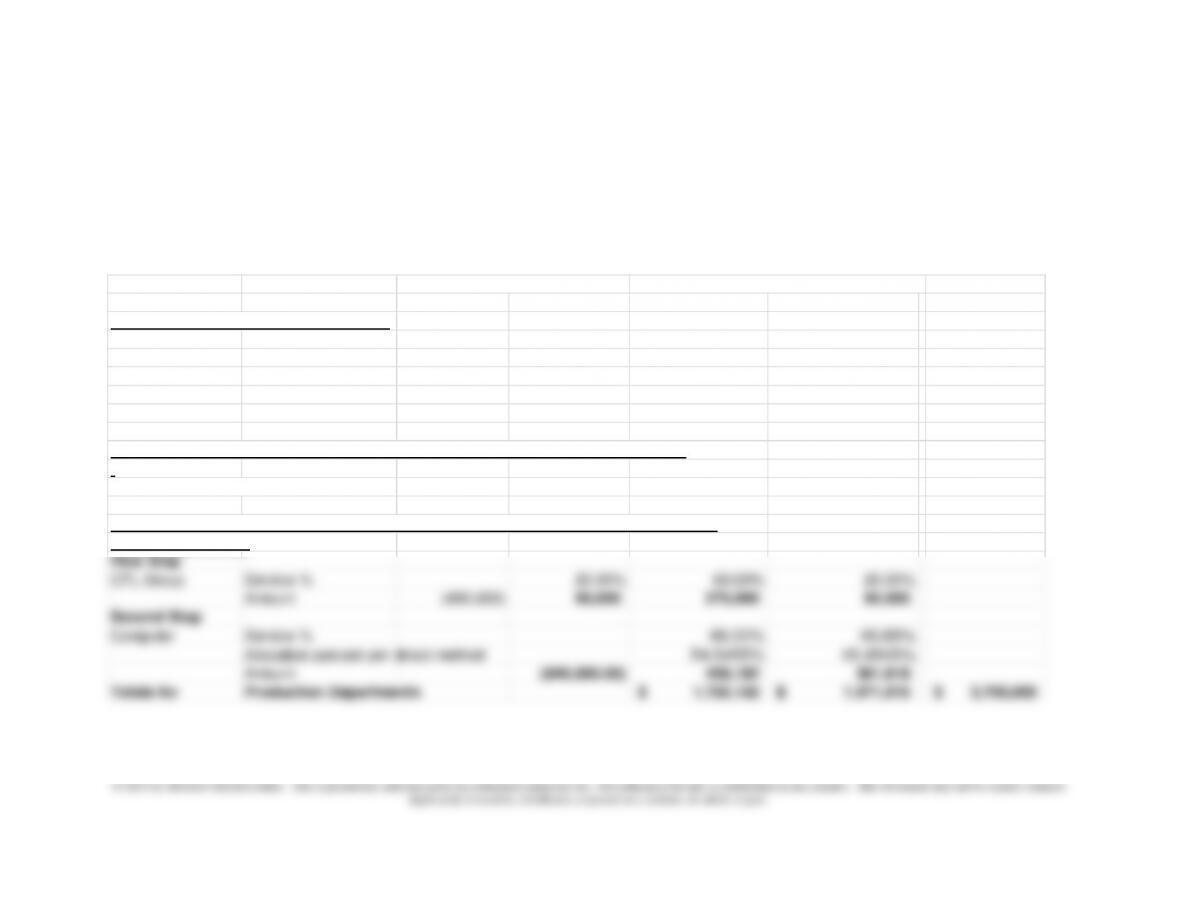

7-37 (continued –2)

Reciprocal Method

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

First: Solve the simultaneous equations

Amount Allocated from CFL 553,278.69

Amount Allocated from Computer 860,655.74

Second: Allocate to Producing Departments:

CFL Group Service % 60% 20%

Alloc. Amt

(553,279) 331,967.21 110,655.74

Computer Service % 48% 40%

Alloc. Amt

(860,655.74) 413,114.75 344,262.30

Totals for Production Departments 1,745,082 1,954,918 3,700,000

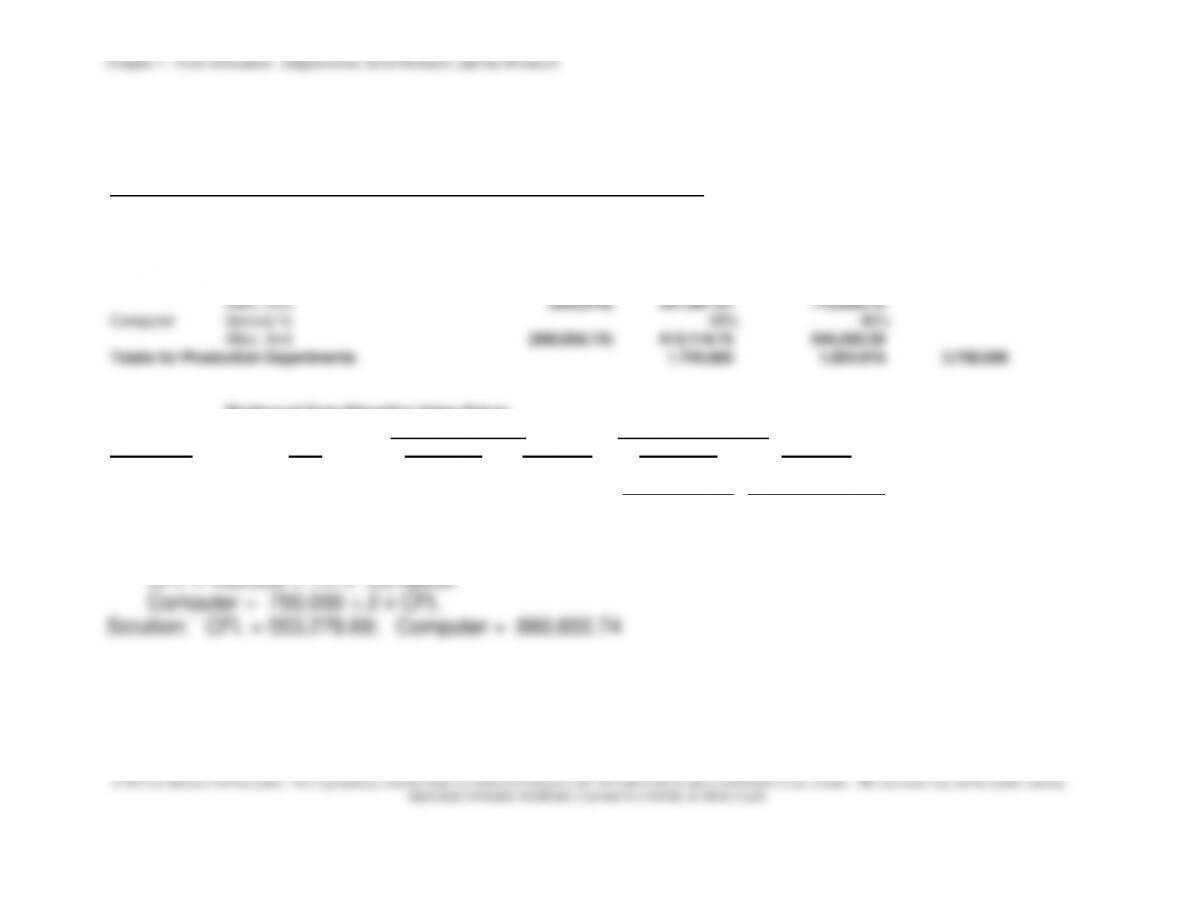

Reciprocal Cost Allocation Using Solver

Service Allocated Service Rates To.. Initial Allocation To…

Department Cost CFL Group Computer CFL Group Computer

CFL Group 553,278.69 1.00 (0.20) 553,279 (110,656)

Computer 860,655.74 (0.12) 1.00 (103,279) 860,656

450,000 750,000

Note: Equations to Solve (using Solver):

CFL = 450,000 + .12 x Computer

7-36

7-38 Departmental Cost Allocation (25 min)

The Direct Method

Base Maintenance Utilities Production A Production B

Total

DEPARTMENTAL ALLOCATION BASES

Maintenance percent 0.0% 25.0% 25.0% 50.0% 100%

Utilities percent 15.0% 0.0% 40.0% 45.0% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Direct Costs 115,000$ 65,000$ –$ –$ 180,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

Maintenance Service % to producing departments 25% 50% 75%

Allocation % per the direct method 25/75=33.33%; 50/75=66.6667% 33.3333% 66.6667% 100%

Allocation amount (115,000)$ 38,333$ 76,667$

Utilities Service % to producing departments 40% 45% 85%

Allocation % per the direct method 40/85=47.0588%; 45/85=52.9412% 47.0588% 52.9412% 100%

Allocation amount (65,000)$ 30,588 34,412

Totals for Production Departments 68,922$ 111,078$ 180,000$

Departments

Service

Production

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-37

7-38 (continued –1)

The Step Method

The maintenance department goes first since it has a greater percentage of service (25%) to utilities

than the utilities department has to maintenance (15%).

Base Maintenance Utilities Production A Production B Total

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Maintenance percent 0% 25% 25% 50% 100%

Utilities percent 15% 0% 40% 45% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Direct Costs 115,000$ 65,000$ –$ –$ 180,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method (Maintenance goes first because it has the highest cost in total or on a precentage basis)

First Step

Maintenance Service % 25.00% 25.00% 50.00% 100%

Amount (115,000)$ 28,750$ 28,750$ 57,500$

Second Step p

Utilities Service % 40.00% 45.00% 85%

Allocation percent per direct method 40/85=47.0588%; 45/85=52.9412% 47.0588% 52.9412% 100%

Amount (93,750) 44,118 49,632

Totals for Production Departments –$ 72,868$ 107,132$ 180,000$

Departments

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-38 (continued –2)

The Reciprocal Method

Base Maintenance Utilities Production A Production B Total

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Maintenance percent 0% 25% 25% 50% 100%

Utilities percent 15% 0% 40% 45% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Direct Costs 115,000$ 65,000$ –$ –$

180,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Reciprocal Method

First: Solve the simultaneous equations (see Solver Solution Section below)

Amount Allocated from Maintenance 129,610.39$

Amount Allocated from Utilities 97,402.60$

Second: Allocate to Producing Departments:

Maintenance Service % 25% 50%

Alloc. Amt

32,403$ 64,805$

Utilities Service % 40% 45%

Alloc. Amt

38,961 43,831

Totals for Production Departments 71,364$ 108,636$ 180,000$

Allocated Service Rates To.. Initial Allocation To…

Cost

Maintenanc

Utilities Production A Production B

Maintenance 129,610 1.00 (0.25) 129,610 (32,403)

Utilities 97,403 (0.15) 1.00 (14,610) 97,403

Departments

Reciprocal Cost Allocation Using Solver

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned,

Equations: Maintenance = 115,000 + (.15 x Utilities)

Utilities = 65,000 + (.25 x Maintenance)

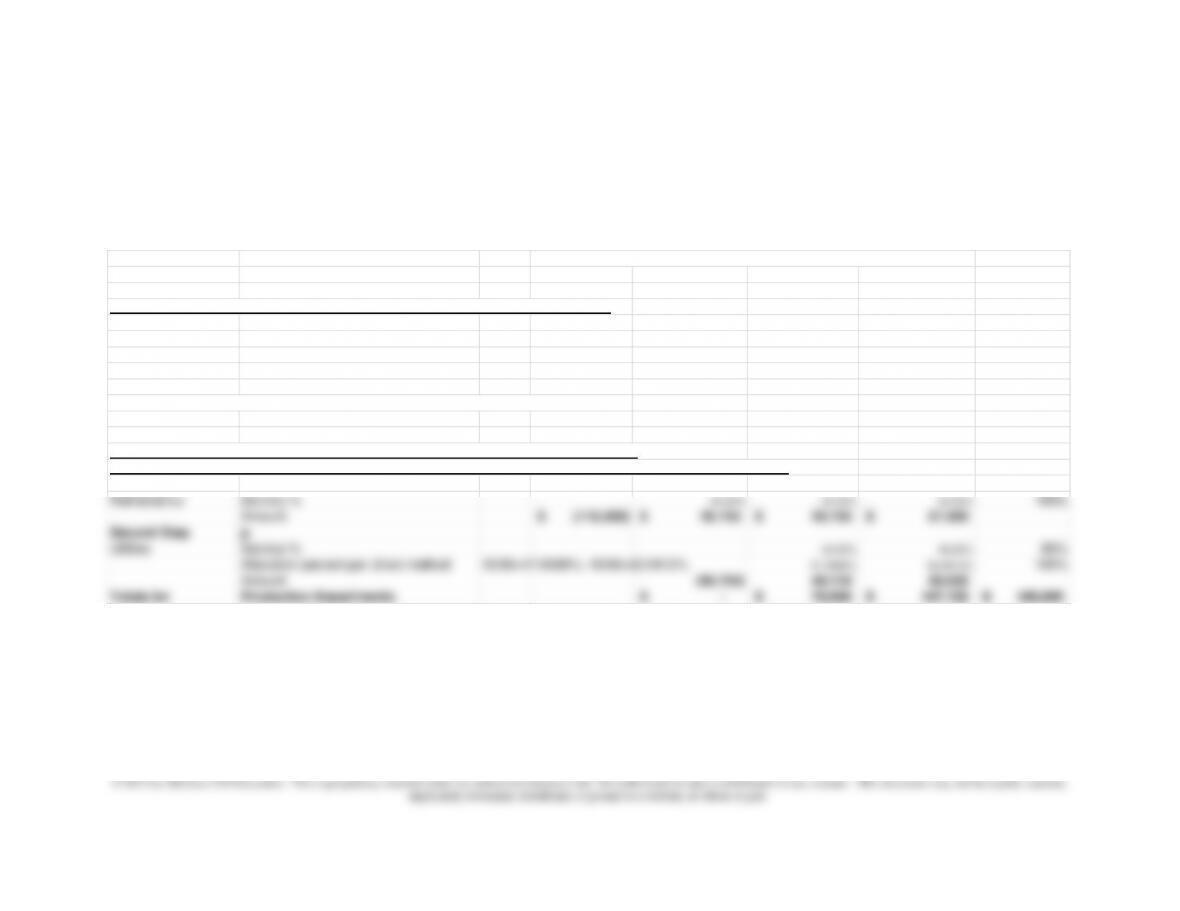

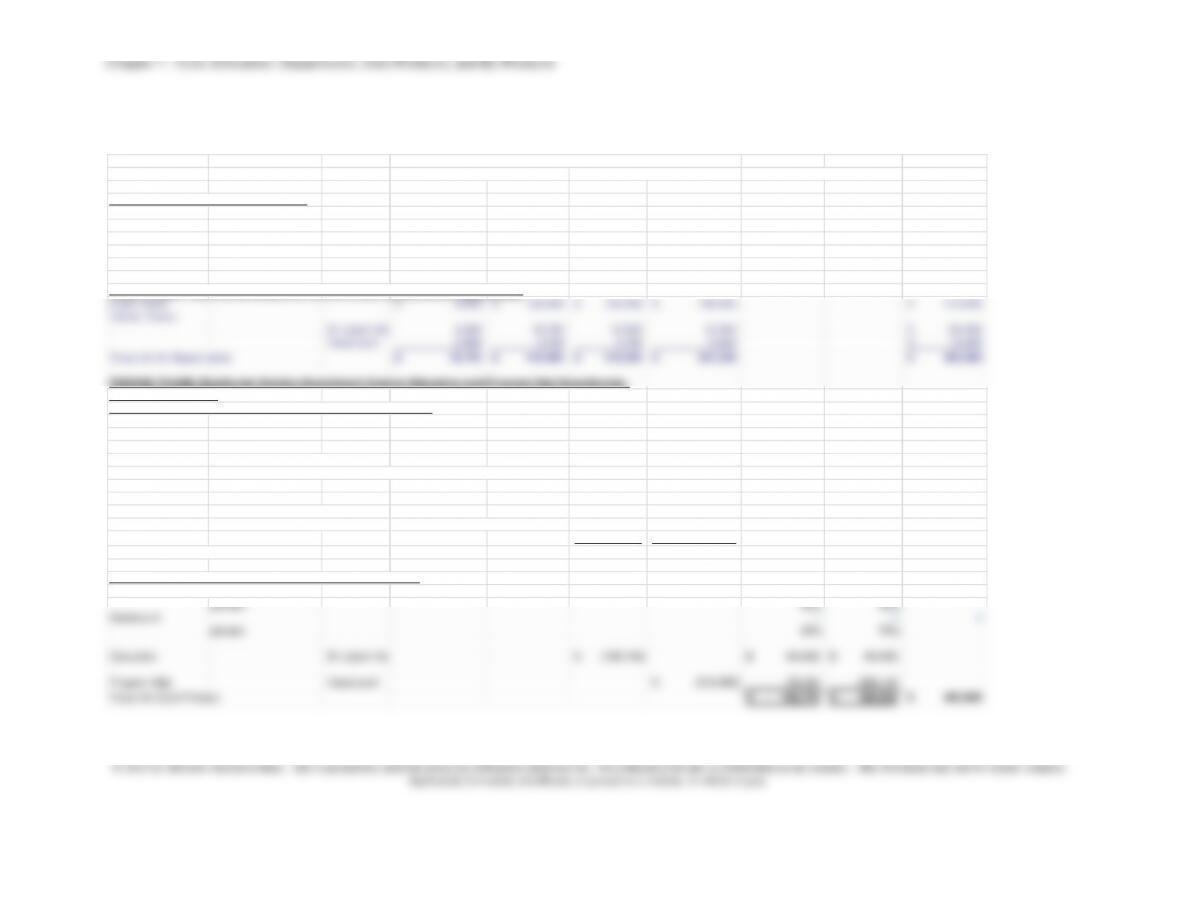

7-39 Departmental Cost Allocation (50 Min)

1.a. The Direct Method

Info Systems Facilities Programming Consulting Training Total

DEPARTMENTAL ALLOCATION BASES

Info Systems

200 1,200 600 1,000 3,000

percent 6.6667% 40.0000% 20.0000% 33.3333% 100%

Facilities

200 400 600 800 2,000

percent 10.00% 20.00% 30.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

80,000$ 45,000$ 150,000$ 190,000$ 135,000$ 600,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Direct Method

Info Systems Service % to producing departments 40.00% 20.00% 33.33% 0.933$

Allocation % per the direct method

40/93.3=42.86%;20/93.3=21.43%;33.3/93.3=35.71%

42.8571% 21.4286% 35.7143%

Allocation amount

(80,000)$ 34,286$ 17,143$ 28,571$

Facilities Service % to producing departments 20.00% 30.00% 40.00% 90%

Allocation % per the direct method 20/90=22.22%;30/90=33.33%;40/90=44.44% 22.2222% 33.3333% 44.4444%

Allocation amount (45,000)$ 10,000 15,000 20,000

Totals for Production Departments 194,286$ 222,143$ 183,571$ 600,000$

Support Departments

Producing Departments

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-40

7-39 (continued -1)

1.b The Step Method (Information Systems Goes First)

Info Systems Facilities Programming Consulting Training Total

DEPARTMENTAL ALLOCATION BASES

Info Systems 200 1,200 600 1,000 3,000

percent 6.6667% 40.0000% 20.0000% 33.3333% 100%

Facilities 200 400 600 800 2,000

percent 10.00% 20.00% 30.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

80,000$ 45,000$ 150,000$ 190,000$ 135,000$ 600,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

Info Systems Service % 6.6667% 40.0000% 20.0000% 33.3333%

Amount (80,000)

5,333 32,000 16,000 26,667

Second Step

Facilities Service % 20.00% 30.00% 40.00% 90%

Allocation percent per direct method 20/90=22.2%;30/90=33.3%;40/90=44.4% 22.2222% 33.3333% 44.4444%

Amount (50,333.33) 11,185 16,778 22,370

Totals for Production Departments 193,185$ 222,778$ 184,037$ 600,000$

Support Departments

Producing Departments

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-41

7-39 (continued -2)

1.b The Step Method (Facilities Goes First)

Info Systems Facilities Programming Consulting Training Total

DEPARTMENTAL ALLOCATION BASES

Info Systems 200 1,200 600 1,000 3,000

percent 6.67% 40.00% 20.00% 33.33% 100%

Facilities 200 400 600 800 2,000

percent 10.00% 20.00% 30.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments

80,000$ 45,000$ 150,000$ 190,000$ 135,000$ 600,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

Facilities Service % 10% 20.00% 30.00% 40.00% 100%

Amount

4,500 (45,000) 9,000 13,500 18,000

Second Step

Info Systems Service % 40.0000% 20.0000% 33.3333% 93.33%

Allocation per direct 40/93.3=42.86%;20/93.3=21.43%;33.3/93.3=35.71% 42.8571% 21.4286% 35.7143% 100%

Amount (84,500)$ 36,214$ 18,107$ 30,179$

Totals for Production Departments 195,214$ 221,607$ 183,179$ 600,000$

Support Departments

Producing Departments

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-39 (continued -3)

1.c. The Reciprocal Method

Reciprocal Method Using Solver

Info Systems Facilities Programming Consulting Training Total

DEPARTMENTAL ALLOCATION BASES

Information Systems Hours 200 1,200 600 1,000 3,000

percent 6.6667% 40.0000% 20.0000% 33.3333% 100%

Facilities; square feet (000) 200 400 600 800 2,000

percent 10.00% 20.00% 30.00% 40.00% 100%

Totals for All Departments

80,000$ 45,000$ 150,000$ 190,000$ 135,000$ 600,000$

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

First: Solve the simultaneous equations for Service 1 and Service 2:

(See Solver Solution below)

Amount Allocated from Info Systems 85,067.11

Amount Allocated from Facilities 50,671.14

Second: Allocate to Producing Departments:

Info Systems Service % 40% 20% 33.3333%

Alloc. Amt

34,026.85 17,013.42 28,355.70

Facilities Service % 20% 30% 40%

Alloc. Amt 10,134.23 15,201.34 20,268.46

Totals for Production Departments 194,161$ 222,215$ 183,624$ 600,000$

Reciprocal Cost Allocation Using Solver

Service Allocated Service Rates To.. Initial Allocation To…

Department Cost Info Systems Facilities Info Systems Facilities

Info Systems 85,067.11 1.00 (0.07) 85,067 (5,671)

Facilities 50,671.14 (0.10) 1.00 (5,067) 50,671

80,000 45,000

Support Departments

Producing Departments

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-43

7-39 (continued -4)

2. Rather than to allocate costs, Computer Intelligence might consider

7-44

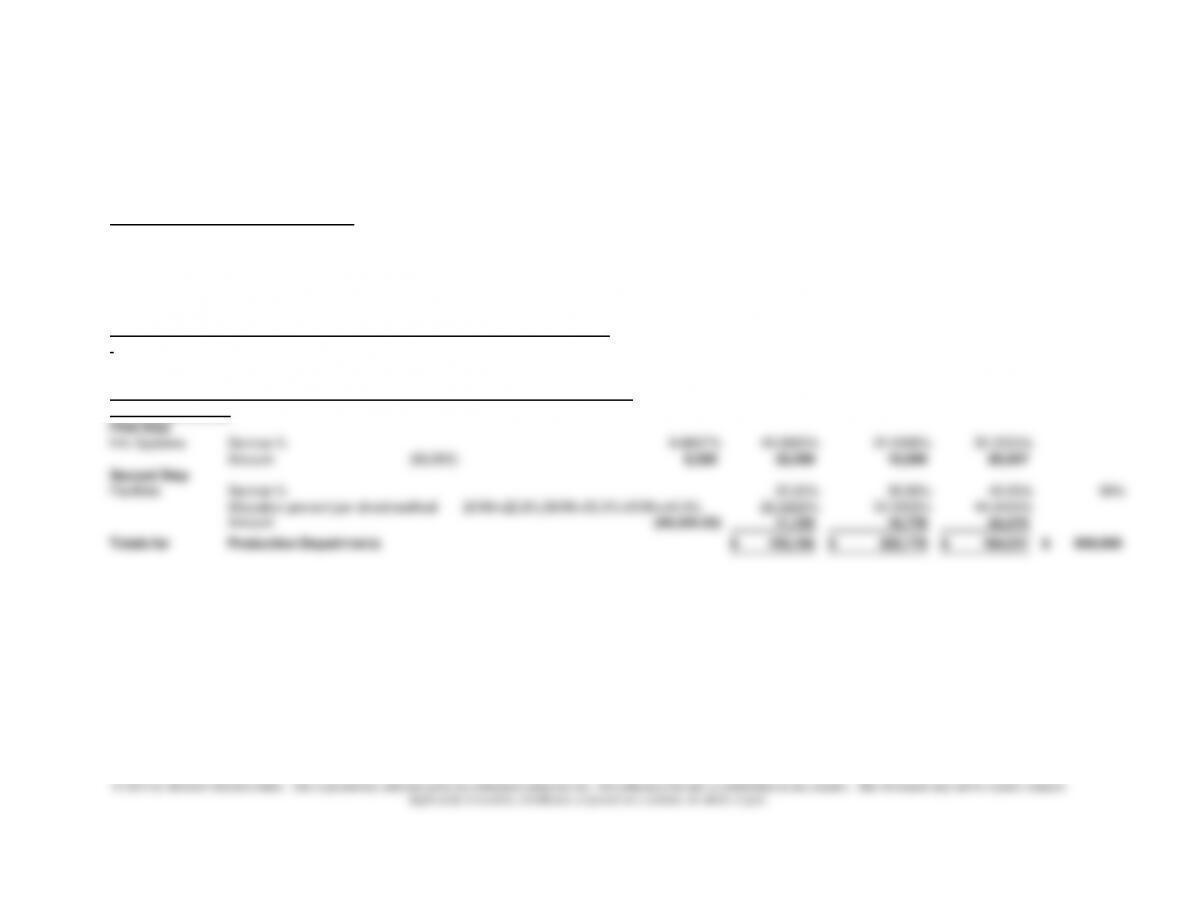

7-40 Departmental Cost Allocation (50 min)

The Direct Method

Base IT Admin Education Program Mgt Mental Health Housing

Total

DEPARTMENTAL ALLOCATION BASES

Direct Labor Hr Direct labor hours 2,000 6,000 4,000 4,000 16,000

percent 12.50% 37.50% 25.00% 25.00% 100%

Headcount Headcount 2 3 3 4 12

percent 16.6667% 25.0000% 25.0000% 33.3333% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Direct Costs 6,000$ 122,000$ 100,000$ 190,000$ 418,000$

Indirect Costs:

Dir Labor Hrs

6,250 18,750 12,500 12,500 50,000$

Headcount 2,500 3,750 3,750 5,000 15,000$

Totals for All Departments 14,750$ 144,500$ 116,250$ 207,500$ 483,000$

SECOND PHASE: Reallocate Service Department Costs to Education and Program Mgt Departments:

The Direct Method

Service Rates for Support Departments and Main Departments

IT 20% 20% 60%

Administration 10% 30% 60%

IT Service % to producing departments 20.00% 60.00% 80%

Allocation % per the direct method (20/80=25%; 60/80=75%) 25.00% 75.00%

Allocation amount (14,750)$ 3,688$ 11,063$

percent 50% 50%

Headcount 1 3 4

percent 25% 75%

Education Dir Labor Hrs (168,104)$ 84,052$ 84,052$

Program Mgt Headcount (314,896)$ 78,724 236,172

Totals for Each Product 162,776$ 320,224$ 483,000$

Departments

Service

Main

Programs

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-45

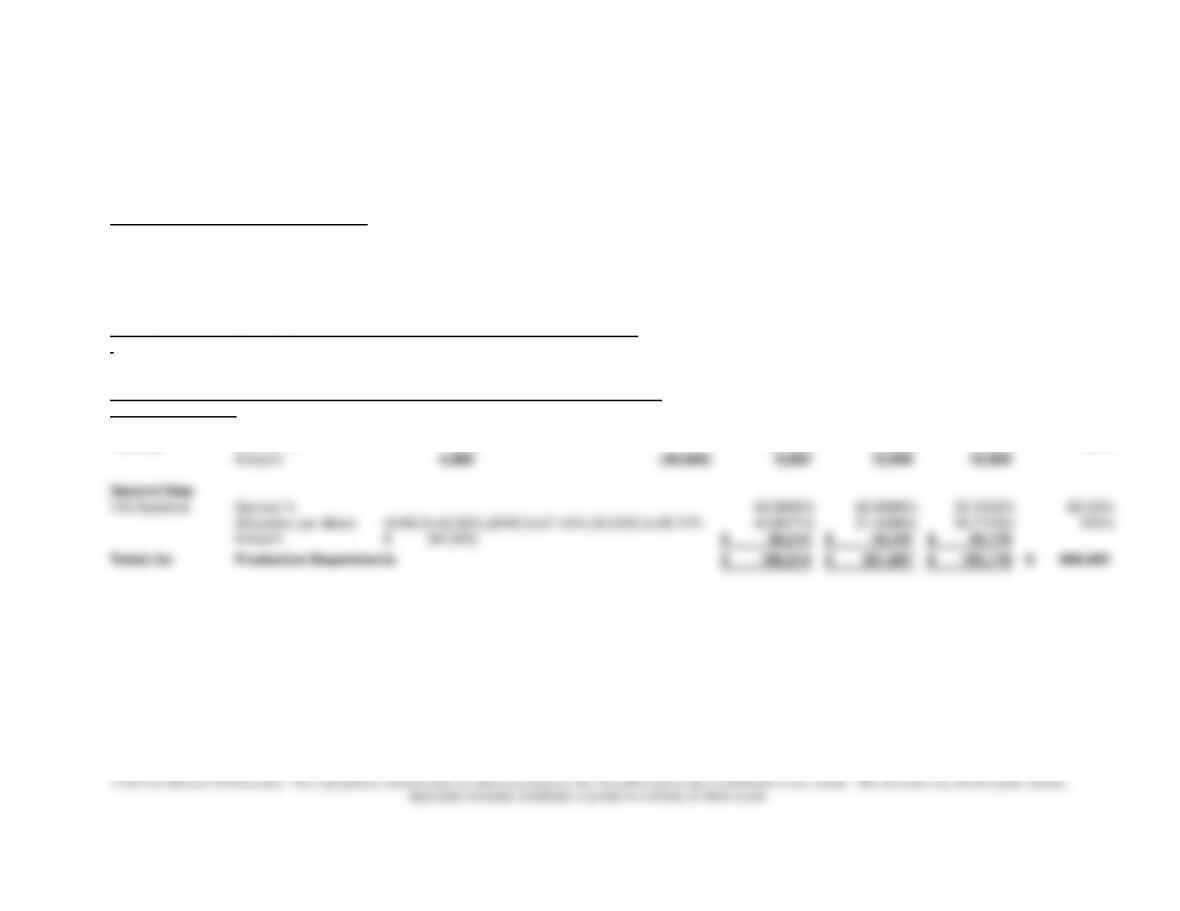

7-40 (continued -1) The Step Method

Base IT Admin Education Program Mgt Mental Health Housing

Total

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Direct Costs 6,000$ 122,000$ 100,000$ 190,000$ 418,000$

Indirect Costs: –$

Dir Lab Hours

6,250 18,750 12,500 12,500 50,000$

Headcount 2,500 3,750 3,750 5,000 15,000$

Totals for All Departments 14,750$ 144,500$ 116,250$ 207,500$ 483,000$

SECOND PHASE: Reallocate Service Department Costs to Education and Program Mgt Departments:

The Step Method

First Step

IT Service % 20% 20% 60% 100%

Amount (14,750)$ 2,950$ 2,950$ 8,850$

Second Ste

p

Admin Service % 30% 60% 90%

Allocation percent per direct method 33.3333% 66.6667% 30/90=33.3%;60/90=66.67%

Amount (147,450) 49,150 98,300

Totals for Production Departments –$ 168,350$ 314,650$ 483,000$

THIRD PHASE: Allocate Main Department Costs to Programs

Base: Direct Labor Hours 2,000 2,000 4,000

percent 50% 50%

Headcount 1 3 4

percent 25% 75%

Departments

Service

Main

Programs