Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–43

20-45 (continued -1)

Liquidity looks OK overall, except for the recent buildup in inventory. The current ratio has fallen

below the bank restriction years ago, but has been safely above it in recent years. On the plus side,

cash flow from operations continues to improve, except for a decline in the prior year. Liquidity looks

good, but it would also be useful to compare these results to an industry average to validate the

findings.

b. Profitability

Ratios

Relevance

2008

2009

2010

2011

2012

2013

Return on

Total Assets

A measure of management’s efficiency

and effectiveness in using available

assets.

6.7%

12.1%

13.5%

2.6%

12.7%

Return on

Equity

A measure of management’s

effectiveness in providing returns to

shareholders

53.9%

71.8%

61.5%

10.5%

50.0%

Gross Margin

%

An important measure of profitability.

Should be compared to prior years and to

relevant industry data. Reflects control

over costs and pricing policies.

35.0%

36.0%

37.9%

38.2%

38.0%

40.5%

Profitability is excellent in 2013, rebounding from a poor year in 2012. Will the improvement

continue? Some concern for variability in sales and profit over the last few years.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-44

20-45 (continued –2)

The spreadsheet for the solution is shown below.

Blue Water Yachts Company

Comparative Balance Sheet

For the Year Ended December 31,

2008 2009 2010 2011 2012 2013

Cash 23,260$ 21,966$ 18,735$ 28,426$ 43,692$ 31,264$

Accounts Receivable 99,465 102,834 112,903 125,663 104,388 142,009

Allowance for Bad Debts (9,304) (8,786) (8,824) (11,266) (7,282) (12,506)

Inventory 35,009 56,784 61,792 67,884 58,994 95,774

Other Current Assets 11,894 12,894 9,024 11,006 18,923 22,903

Total Current Assets 160,324$ 185,692$ 193,630$ 221,713$ 218,715$ 279,444$

Property and Equipment 262,195 282,008 299,380 368,565 405,269 498,626

Accumulated Depreciation (65,984) (93,442) (122,892) (158,099) (187,227) (226,307)

Total Assets 356,535$ 374,258$ 370,118$ 432,179$ 436,757$ 551,763$

Accounts Payable 82,635 78,127 63,346 56,256 40,189 49,544

Taxes Payable 11,630 10,983 11,780 14,083 3,738 15,632

Short Term Loans 59,876 56,980 37,583 41,093 49,594 76,962

Accrued Payroll Payable 5,227 4,598 3,649 4,224 4,774 4,779

Total Current Liabilities 159,368$ 150,688$ 116,358$ 115,656$ 98,295$ 146,917$

Long Term Debt 158,173 172,388 179,490 214,997 229,471 262,258

Partners’ Equity 38,994 51,182 74,270 101,526 108,991 142,588

356,535$ 374,258$ 370,118$ 432,179$ 436,757$ 551,763$

Blue Water Yachts Company

Comparative Statement of Income and Cash Flow

For the Year Ended December 31,

Cost of Sales 473,908 441,298 458,015 545,778 453,669 530,597

Gross Margin 255,293 247,935 279,131 337,702 278,054 361,880

Depreciation Expense 29,075 27,458 29,450 35,207 29,128 39,080

Interest Expense 18,597 19,557 20,998 21,475 24,889 28,993

Salaries and Wages 81,923 73,664 77,846 95,764 92,903 99,447

Total Expense 231,195 223,626 234,073 283,652 266,957 299,003

Net Income 24,098 24,309 45,058 54,050 11,097 62,877

Cash Flow from Operations

Net Income 24,309 45,058 54,050 11,097 62,877

Depreciation 27,458 29,450 35,207 29,128 39,080

Decrease (increase) in Receivables (3,887) (10,031) (10,318) 17,291 (32,397)

Liquidity Ratios

Accounts Receivable Turnover 7.48 7.44 8.09 6.92 7.88

Inventory Turnover 9.62 7.73 8.42 7.15 6.86

Current Ratio 1.01 1.23 1.66 1.92 2.23 1.90

Quick Ratio 0.71 0.77 1.06 1.23 1.43 1.09

Cash Flow Ratio 0.11 0.25 0.61 0.42 0.53

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–45

20–46 Business Valuation (20 min)

Using most recent figures, the net book value for Blue Water Sailboats’

equity is $142,588, taken from the balance sheet.

The earnings multiple method would take a projected value for earnings, as

for example the median value for the three recent years ($54,050) times

additional judgment; a median figure for the multiples valuations would be

approximately $425,000.

Summary of Valuations:

Valuation Method

Valuation

Net Book Value of Equity

$142,588

Earnings Multiple

$432,400 = 8 x $54,050

Operating Cash Flow Multiple

$420,978 = 6 x $70,163

20-47 Business Analysis (50 min)

Calculations for financial ratios:

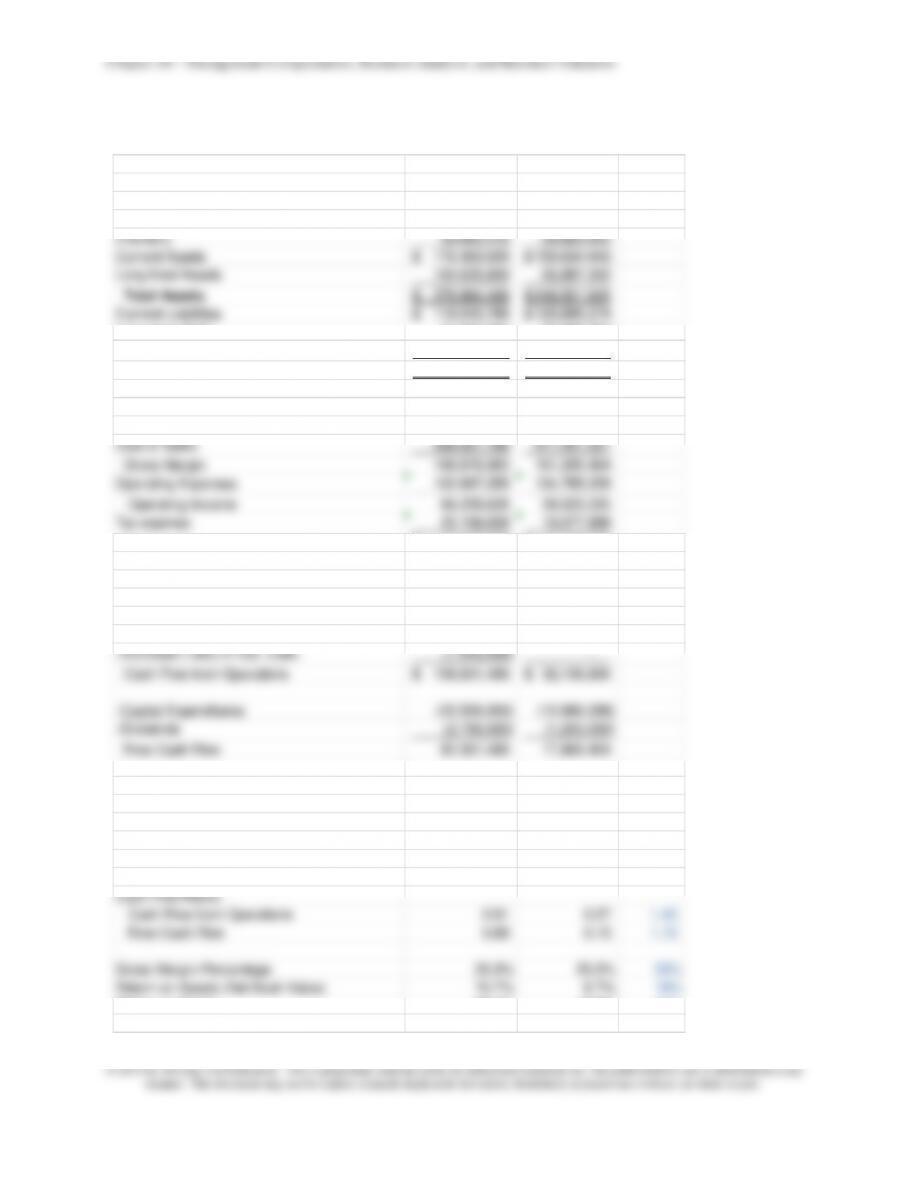

Balance Sheet 2013 2012

Cash 79,919,778$ 3,456,227$

Accounts Receivable 56,778,465 87,294,771

Inventory 39,665,416

59,883,645

Current Assets 176,363,659$ 150,634,643$

Long-lived Assets 100,620,809 95,887,302

Total Assets 276,984,468

$ 246,521,945$

Current Liabilities 119,045,766$ 120,995,274$

Long-term Debt 31,997,364 37,885,302

Shareholder Equity 125,941,338 87,641,369

Total Debt and Equity 276,984,468

$ 246,521,945$

Gross Margin 168,876,983 161,285,464

Operating Expenses 102,667,355 134,765,229

Operating Income 66,209,628 26,520,235

Tax expense 25,159,659 10,077,689

Net Income 41,049,969$ 16,442,546$

Cash Flow From Operations

Cash Flow from Operations 108,601,489$ 32,106,800$

-Capital Expenditures (23,500,000) (12,990,336)

-Dividends (2,750,000) (1,250,000)

Free Cash Flow 82,351,489 17,866,464

Cash Flow from Operations 0.91 0.27 1.40

Free Cash Flow 0.69 0.15 1.10

Gross Margin Percentage 25.3% 25.2% 33%

Return on Assets (Net Book Value) 15.7% 6.7% 19%

Return on Equity 38.4% 18.8% 28%

Earnings per Share 1.694$ 0.679$ 2.33$

20–47

20-47 (continued –1)

A financial ratio analysis of BPP’s liquidity shows a company that is

improving quite well on all measures. The receivables turnover and

inventory turnover ratios are both significantly better than the industry

2012; the result is that the calculation of cash flow from operation for 2012

has no change for these two current asset accounts). Note also that BPP

increased dividends significantly in 2013, with a negative impact on cash

flow and liquidity. Overall, this shows a mixed but improving picture for

BPP relative to liquidity.

As to profitability, BPP’s ratios have improved significantly from 2012

to 2013. However, return on assets is still lower than the industry

average, while return on equity is now substantially higher than the industry

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-48

20-48 Business Valuation (30 min)

1. & 2. Calculation of book value, market value, discounted cash flow, and

multiples-based values:

2013

Book Value of Equity 125,941,338$

Market Value of Equity 919,172,242 =$35.78 x 25,689,554

Discounted Free Cash Flow 1,583,682,488 =$82,351,489/.052

Multiples–Based Valuation

Earnings Multiple 554,174,586 =$41,049,969 x 13.50

Free Cash Flow Multiple 724,693,106 =$82,351,489 x 8.8

Sales Multiple 934,548,679 =$667,534,771x 1.40

3. The six measures provide a wide range of valuations, from a low of

$125,941,338 for the book value of equity to a high of $1,583,682,481 for

the discounted cash flow method. The discounted cash flow measure is

relatively high because of the significant increase in cash flow in 2013 due

4. If the company is valued at approximately $919,172,242, this would

reflect an expected share price close to its current market value of $35.78.

Thus, the $38 offer looks good. On the other hand, if one projects a

20–49

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

20–48 (continued – 1)

5. Sustainabllity issues may arise in the acquisition because both GSI

and BPP operate in environmentally sensitive industries. GSI, a retailer

of gardening supplies, must be vigilant about both the manufacturing

practices of its suppliers (to minimize harmful waste products getting into

the environment) and also about the handling of the materials within

GSI’s stores and in its transportation of these materials. Insecticides,

weed killers, fertilizers, and other products can have toxic and/or harmful

chemicals.

Also, the use of BPP plumbing expertise and materials has a

sustainability dimension. If these products are used to supply home or

commercial lawn and garden watering systems, then for sustainability,

Given that many investors now consider sustainability and important part

of a company’s strategic planning, then valuation will also be affected by

whether or not a company such as GSI or BPP have a sustainability

plan. Sustainability efforts are also often tied to cost reduction, as the

company’s efforts to improve sustainability reduce operating costs and

compliance costs. Companies with an effective plan for sustainability

will likely receive higher valuations, as investors and analysts see the

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-50

20-49 Business Analysis and Business Valuation (45 min)

1. First, determine the amount of cash flow from operations and the

amount of free cash flow, assuming that the 2011 and 2012 balance

sheet values are the same. This means that there is no positive or

negative effect in the calculation of cash flow from operations for the

change in inventory or receivables. Second, calculate the financial

ratios. The results are shown below.

Cash Flow From Operations 2013 2012

Net Income 76,783$ 131,362$

Plus Depreciation Expense 42,746 43,997

+Decrease (-inc) in AccRec and Inv (25,960) –

+Increase (-dec) in Cur. Liabl. (45,564) –

Cash Flow from Operations 48,005$ 175,359$

-Capital Expenditures (50,000) (100,000)

-Dividends – –

Free Cash Flow (1,995)$ 75,359$

Financial Ratios 2013 2012 Industry

Accounts Receivable Turnover 43.14 41.73 8.80

Inventory Turnover 8.85 8.24 7.00

Current Ratio 2.95 2.36 2.00

Quick Ratio 2.24 1.85 1.10

Cash Flow Ratios

Cash Flow from Operations 0.22 0.66 1.40

Free Cash Flow (0.01) 0.28 1.10

Gross Margin Percentage 18.8% 23.8% 30%

Return on Assets (Net Book Value) 7.1% 12.3% 18%

Return on Equity 15.6% 28.9% 24%

Earnings per Share 0.117$ 0.201$ 1.15$

significantly lower than the industry average. In particular, free cash flow is

negative in 2013. A key reason for the decline in the cash flow ratios is the

decline in income and the increase in inventory and receivables from 2012

to 2013. The decline in cash flow is a real concern for JJP and should be

given immediate attention.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20–51

20–49 (continued –1)

1. (continued)

The profitability ratios are also poor. They are declining and below

the industry average. In particular, return on equity has fallen to

approximately half of its 2012 value, from 28.9% to 15.6%. This is a

very unfavorable sign for investors and, together with the decline in

cash flow, is a main reason for the decline in stock price from $5.50

should be investigated thoroughly.

2. Six business valuations are calculated below for 2012 and 2013.

2013 2012 Calc for 2013

Book Value of Equity 531,847$ 455,064$

Market Value of Equity 1,529,316 3,594,547 =$2.34 x 653,554

Discounted Cash Flow (35,000) 1,322,088 =$(1,995)/.057

Multiples-Based Valuation

Earnings Multiple 1,612,433 2,758,599 =$76,783 x 21

Free Cash Flow Multiple (17,556) 663,158 =($1,995) x 8.8

Sales Multiple 3,494,401 3,202,395 =$1,588,364*2.2

Note that every valuation measure except for book value of equity

has declined from 2012 to 2013 due to the decrease in cash flow and

the decrease in income. In fact the 2013 valuations based on free

cash flow are negative and therefore are excluded from further

choose a value of approximately $3 million for 2012 because the

sales multiple, market value of equity and earnings multiple are

centered near that point. For 2013, our judgment would be

conservative, given the recent decline in net income and cash flow.

Chapter 20 – Management Compensation, Business Analysis, and Business Valuation

20-52

20-49 (continued -2)

So, we would exclude the sales multiple as an outlier in 2013 and

choose a value close to that of the market value of equity or the

earning multiple, or approximately $1.5 million. This is a drop of

approximately 50% in market value in one year, a serious concern for

JJP.

20-50 Research Assignment; Business Valuation (50in)

1. The authors make the point that a successful business strategy

expert must be a very competent business valuation expert, and vice

versa, and thus, the roles of the two converge. For example, a

environment, together with the company’s strategy for success, will lead

to higher or lower future valuations.

2. The authors cite their research and include example companies to

show that a great product does not necessarily produce a great,

valuable company. The key is the competitive environment and the

3. The explanation here follows that in part 2 above. That is, the

“differences” have to be those differences that the customers are willing

4. The explanation here follows from the above. A great product does

20–53

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Investors may see for example the same level of cash flows in Company

A as in Company B in the current year, but have different expectations

for the future of those cash flows. If investors are predicting that

Company A’s cash flows will continue and/or grow with greater certainty,

then it is likely that Company A will also have the higher stock price,

even if all of the financial performance measures are identical. The role

of investor expectations is critical. This role is often measured by the

Price-Earnings ratio, or ”earnings multiple” as explained in the chapter.

5. Substantial growth can lead to financial difficulties, as can be seen in

the poor financial performance of many financial and construction firms’