Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-16

9-29 Cost Planning: High-End Copiers (20 min)

1. The breakeven number of copies (C) can be determined as follows:

Ricoh Cost = H-P Cost

2. The breakeven price (P) can be determined as follows:

200,000 copies per year = 600,000 copies for three years

Ricoh Cost = H-P cost

3. Since Tanner and Jones competes on quality and service, it is critical that

the company has a reliable and very high quality color copier. If there is any

question that the H-P copier might not provide the quality of copy that Tanner

and Jones has experienced with the Ricoh, then this concern would trump any

and lower cost. Since the strategic concern is quality, then the H-P copier is

now preferred. From a strategic point of view, Tanner and Jones need to

carefully research the quality of the H-P copies before making a decision. Also,

if Tanner and Jones is expected to grow, then the attractiveness of the H-P

copier also increases, because the lower price per copy now applies to a larger

number of copies.

Source: Christopher Lawton, “H-P Begins Push Into High-End Copiers,” The

Wall Street Journal, April 24, 2007.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-17

9-30 Cost Structure of Retailers; the Internet; Operating Leverage (10 min)

1. A retailer can significantly reduce its operating leverage and reduce

costs during a period of initial growth in e-commerce by outsourcing its e-

commerce activity to service-providers. The term ESP for “e-commerce

2. Globalization presents an opportunity for the retailer to obtain the

outsourcing service in low-cost countries throughout the world. Some of

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-18

9-31 Structuring Sales Commissions (15-20 min)

1. Omega—because it has the higher selling price and therefore the larger

sales commission per unit sold.

2. From the standpoint of the company, profits may be higher if customers

purchase more units of Alpha(relative to Omega). This is because Alpha

has the higher contribution margin per unit.

contribution margin will also maximize operating profit for the company.

Note that if there are production/resource constraints and the two products

consumed, on a per-unit basis, different amounts of the scarce resource(s),

then the sales commission compensation plan should be modified—to

reward salespeople for selling a product mix that maximizes the contribution

margin per unit of the scarce resource(s). Such an incentive plan would

likely lead to more goal-congruent behavior: by maximizing their own

welfare the salespeople would also help maximize operating income for the

company.

Addendum: Bazerman, M., and A. E. Tenbrunsel. 2011. Ethical

breakdowns. Harvard Business Review (April), pp. 58-65.

Ill-Conceived Goals (p. 60)

In the above-reference article, the authors state: “In our teaching, we often

deal with sales executives. By far the most common problem they report is

that their sales forces maximize sales rather than profits. We ask them what

incentives they give their salespeople, and they confess to actually

rewarding sales rather than profits. The lesson is clear: When employees

behave in undesirable ways, it’s a good idea to look at what you’re

encouraging them to do.”

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-19

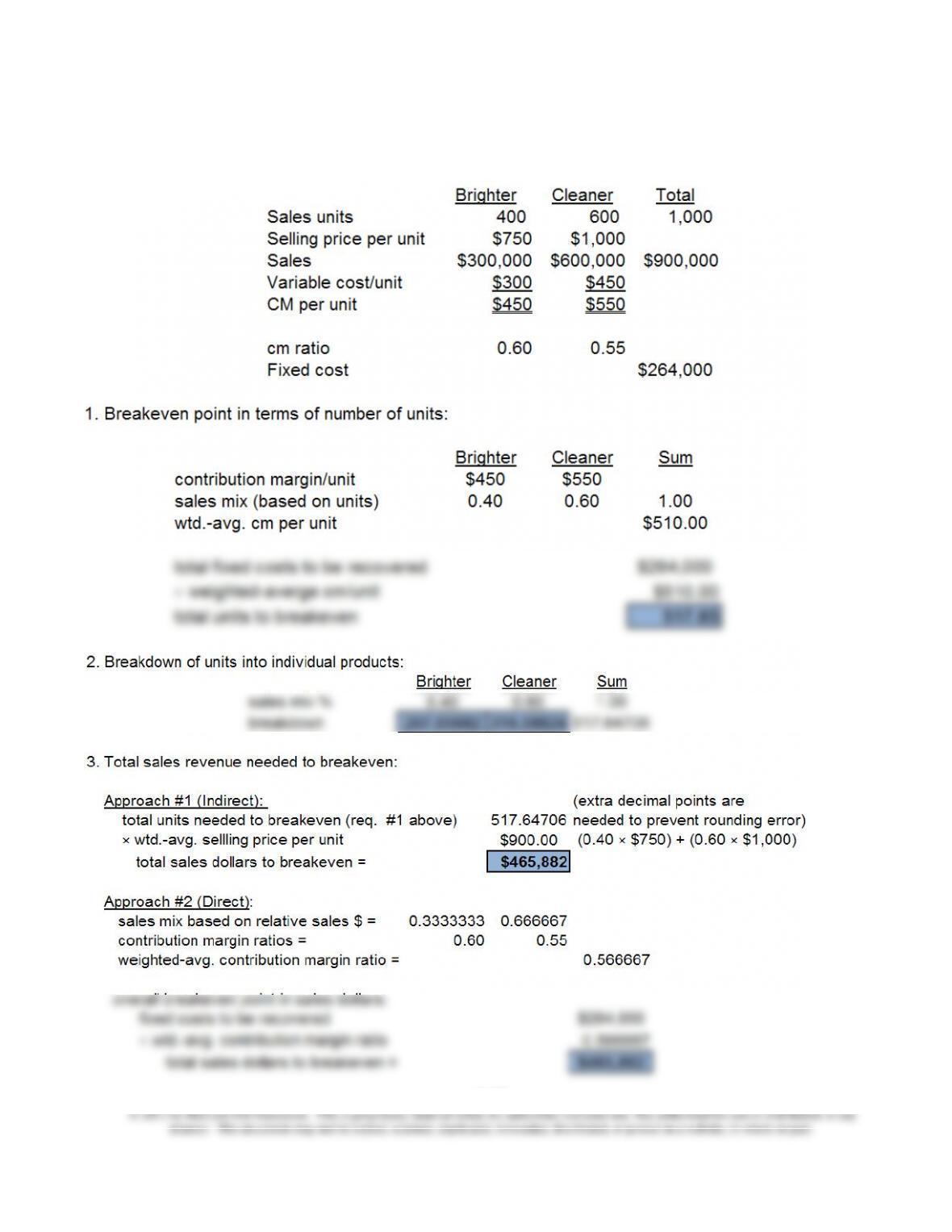

9-32 Multiple Product CVP Analysis (40-45 min)

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-20

Ex. 9-32 (Continued)

4. If machine hours are limited (i.e., if they represent a “scare resource”), then

information regarding the machine-hour consumption of each of the two

products would be important for product-planning purposes. That is, such

the greater the profitability (and therefore desirability) of the product.

An Excel spreadsheet that provides the solution for this exercise is

embedded below:

Ex 9-32.xlsx

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-21

9-33 CVP Analysis (20 min)

1. Contribution margin (CM) ratio = Contribution margin ÷ Sales

Thus, CM ratio = ($46,000,000 − $32,200,000) ÷ $46,000,000

= 0.30

2. Fixed Cost + πB = $7,500,000 + $8,000,000 = $51,666,667

CM ratio 0.30

3. Variable cost ratio = ($32,200,000 × 1.12) ÷ $46,000,000

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-22

9-34 Contribution Income Statements; Sensitivity Analysis; Goal Seek

(Excel) (40-45 min)

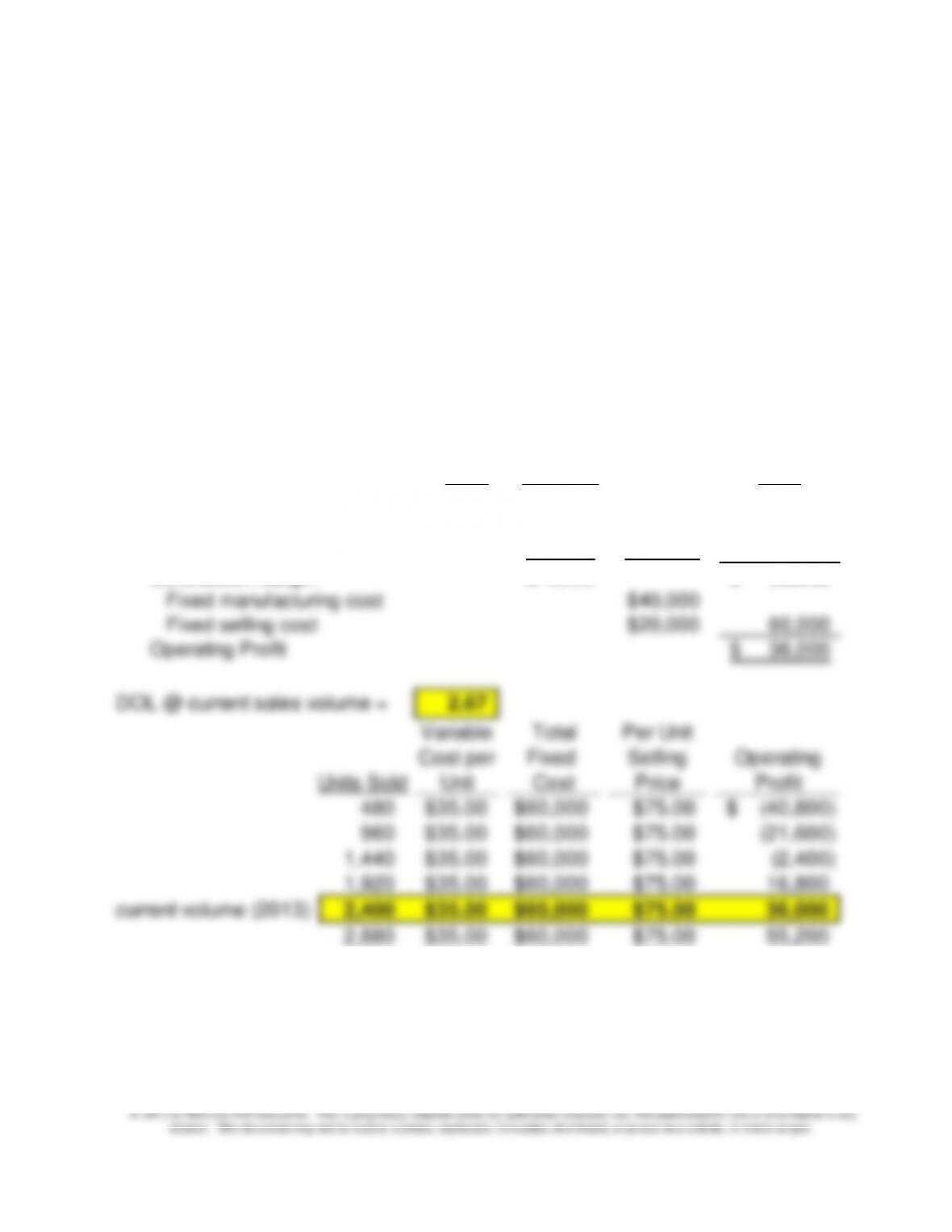

1. A variety of possible spreadsheets could satisfy this requirement. One

example is the spreadsheet embedded below. The sensitivity analysis

shows sales levels from 20% to 200% of 2013 expected sales of 2,400

units, and the related effect on operating profit.

HFI’s degree of operating leverage (DOL) from a sales volume of 2,4000

units is 2 2/3, so that from this volume level profits change much faster

(2.667 times faster) than a given change in the sales level.

Per Unit

Units Amounts Total

Sales 2,400 $75.00 180,000$

Variable manuacturing cost 2,400 $30.00 72,000$

Variable selling 2,400 5.00$ 12,000 84,000

Contribution Margin 40.00$ 96,000$

Fixed manufacturing cost $40,000

Fixed selling cost $20,000 60,000

Operating Profit 36,000$

DOL @ current sales volume = 2.67

Variable Total Per Unit

Cost per Fixed Selling Operating

Units Sold Unit Cost Price Profit

480 $35.00 $60,000 $75.00 (40,800)$

960 $35.00 $60,000 $75.00 (21,600)

1,440 $35.00 $60,000 $75.00 (2,400)

1,920 $35.00 $60,000 $75.00 16,800

current volume (2013) 2,400 $35.00 $60,000 $75.00 36,000

2,880 $35.00 $60,000 $75.00 55,200

3,360 $35.00 $60,000 $75.00 74,400

3,840 $35.00 $60,000 $75.00 93,600

4,320 $35.00 $60,000 $75.00 112,800

4,800 $35.00 $60,000 $75.00 132,000

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-23

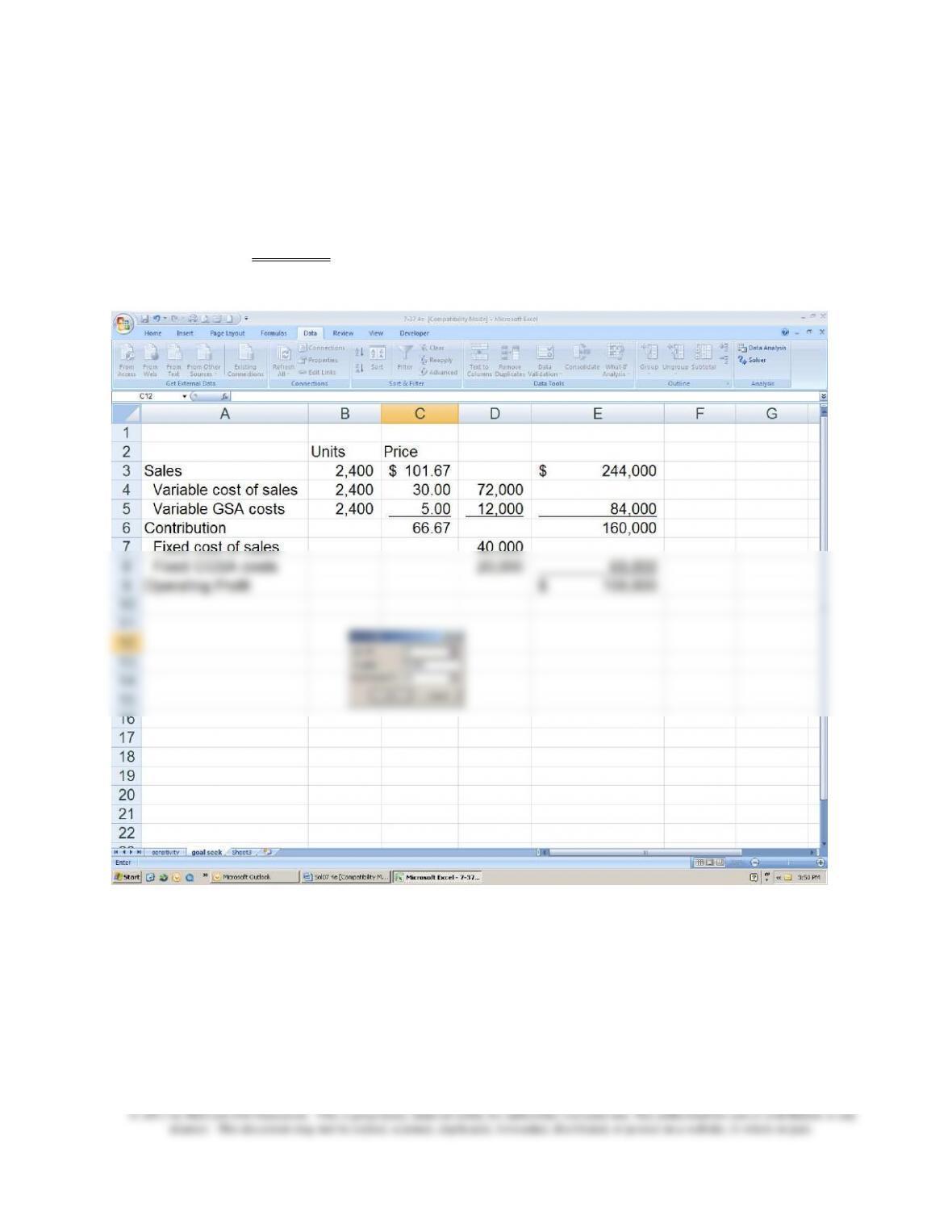

9-34 (continued-1)

2. The Goal Seek tool is available under Data//What-if Analysis/Goal Seek in

Excel. An example of how it is used is show below. The price would have to

increase to $101.67 in order for HFI to make a $100,000 before tax profit.

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-24

9-35 CVP Analysis, DOL, and Margin of Safety (20-30 min)

First, note that the DOL formula, at any sales volume level, Q, is written as:

DOLQ = change (∆) in operating income (OI) ÷ change in sales (S)

= [∆OI/OIQ] ÷ [∆S/SQ]

Second, define the change in OI and the change in S with respect to the break–

even point (B/E), as follows:

Finally, since by definition ([SQ − SB/E]/SQ) = MOS% (at volume level Q), we

have:

DOLQ = 1 ÷ MOS%Q

or, equivalently

MOS%Q = 1 ÷ DOLQ

2. The above specification allows managers to see that operating leverage and

margin of sales are functionally related: the greater the relative amount of

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-25

9-36 Further Analysis—Degree of Operating Leverage (DOL) (30-45 min)

1. Demonstrating that DOL represents the % change in operating income

DOL = CM ÷ Operating Income (OI), for any given sales volume (Q)

New level of OI = DOL × percentage change in sales volume

= (CM ÷ OI) × (new sales volume ÷ current sales volume)

= (∆ in OI) ÷ OI

= percentage change in Operating Income (OI)

2. Relationship between definition of “operating leverage” and the DOL

measure

First, recall the basic profit equation for operating income (OI):

where p = selling price per unit

v = variable cost per unit

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-26

9-36 (Continued)

Second, we can rewrite the above as (where CM = total contribution

margin):

F + OI = (p – v) × Q

= CM

Third,

The advantage of the above specification is that we can more readily see

how sensitivity of operating profit is affected by the amount of FC in the

organization’s cost structure, that is, by the amount of “operating leverage.”

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

PROBLEMS

9-37 CVP Analysis; Strategy (45-50 min)

1. BE units = F ÷ (p − v) = $225,000 ÷ ($45 − $30)/unit = 15,000 units

BE $ = F ÷ CMR = F ÷ [(p − v) ÷ p]

2. πB= Sales − variable costs − fixed costs

= [Q × (unit contribution margin)] − F

= [20,000 units × ($45 − $30)/unit] − $225,000

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-28

9-37(Continued-1)

4. BE units = F ÷ contribution margin per unit

= ($225,000 + $106,500) ÷ ($45 − $25.50)

= $331,500 ÷ $19.50/unit = 17,000 units

πB= Sales − variable costs − fixed costs

*$30.00 − $4.50

5. A key strategic issue is that Hank’s sales staff is a critical success factor

for the business, especially in the growing and competitive environment

of Hank’s business. His knowledgeable and courteous staff help to bring

loyalty to him in prior years, and how the decision will affect their families,

for better or worse?

Finally, there is the issue of operating risk associated with moving to a

cost structure characterized by relatively higher fixed costs (traded-off

against lower variable costs).

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-29

• Possible benefits:

their effect on operating income.

9-37 (Continued-2)

• Possible costs/disadvantages:

o Increased operating (business) risk (e.g., generally speaking,

there will be a higher breakeven point)

o If sales volume recedes, these reductions are magnified in terms

o Increased fixed costs (e.g., those associated with insourcing)

may expose the company to increased risk or exposure to

production slow-downs or stoppages, as experienced in 2011 in

Japan as a consequence of the earthquake/tsunami that hit the

country).

Chapter 9 – Short-Term Profit Planning: Cost-Volume-Profit (CVP) Analysis

9-30

There are two additional points worth making to students:

1. Ultimately, the decision to increase operating leverage is affected by

some of the following considerations: year-to-year fluctuations in sales—

that is, uncertainty (the greater the uncertainty, the greater the

maker’s/owner’s attitude toward risk.

2. Without knowing the future, it is impossible to specify which of the two