Chapter 17 – The Management and Control of Quality

17–46

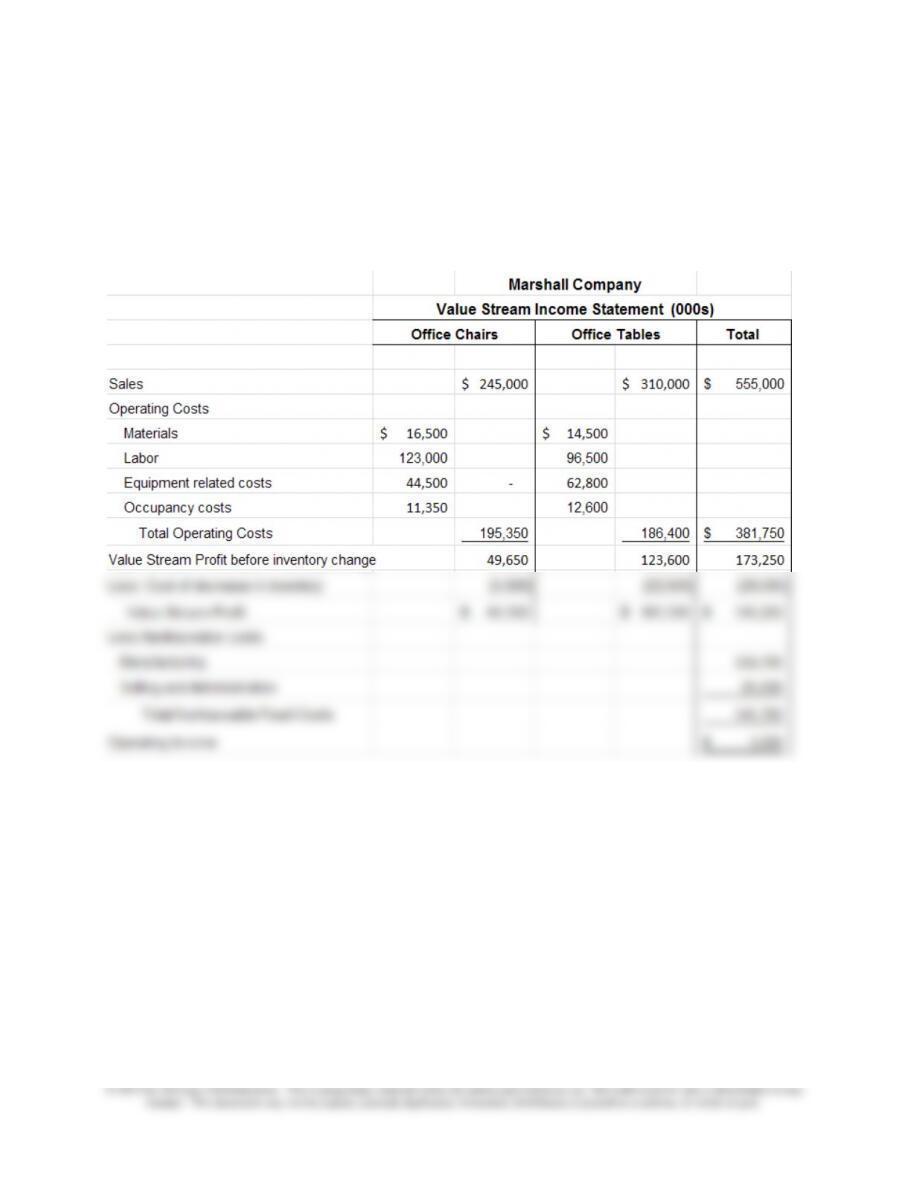

17–46 Value-Stream Income Statement (20-30 Minutes)

The value stream income statement is shown below. Note that the temporary $28

million effect on income due to the decrease in inventory is separated so that the

company can adjust operating income and interpret the long-term operating income by

eliminating the temporary effect of the inventory decrease.

Chapter 17 – The Management and Control of Quality

17–47

PROBLEMS

17–47 Ethics (45-60 Minutes)

1. An examination of the IMA’s Statement of Ethical Professional Practice

(www.imanet.org; note—requires log-in name and password) suggests that Maria

Sanchez likely violated the following standards of ethical conduct when she asked

Mary Stein to suppress pertinent information.

Competence—Maria Sanchez, controller, has a responsibility to:

▪ Provide decision support information and recommendations that are accurate,

clear, concise, and timely.

standards and has a favorable impact on earnings, as requested by Jim March,

vice-president of manufacturing. Thus, the reported financial information with the

omission lacks relevance and reliability for decision-making. Management does not

have a clear solution to overcome the component failure.

Integrity—Sanchez has a responsibility to:

▪ Mitigate actual conflicts of interest. Regularly communicate with business

associates to avoid apparent conflicts of interest. Advise all parties of any

potential conflicts.

▪ Disclose deficiencies in information, in accordance with organization policy and/or

applicable law.

Chapter 17 – The Management and Control of Quality

17–48

17–47 (Continued)

The request by Sanchez is unethical because it would suppress information that

could influence an understanding of the results of operations by the company.

Also, by withholding information about the contingent liability, Sanchez is not

communicating information objectively.

2. Resolution of Ethical Conflict—the IMA Standards specify that when an individual

is faced with ethical issues, the individual should follow the policies established by

the organization to deal with (resolve) such conflicts. If these policies do not resolve

the ethical conflict, then the following courses of action are recommended:

▪ The individual should discuss the issue with his/her immediate supervisor (except

when it appears that the supervisor is involved). In this regard, Stein might want

to write a report that provides details regarding the issue, including the probable

possible courses of action.

▪ If, after exhausting all other options, the ethical conflict still exists, then Stein may

have no choice but to resign and to write an informative memorandum to the

appropriate organizational representative.

▪ Finally, Stein may want to contact a qualified attorney to more fully determine her

legal obligations and rights concerning this ethical conflict.

Chapter 17 – The Management and Control of Quality

17–50

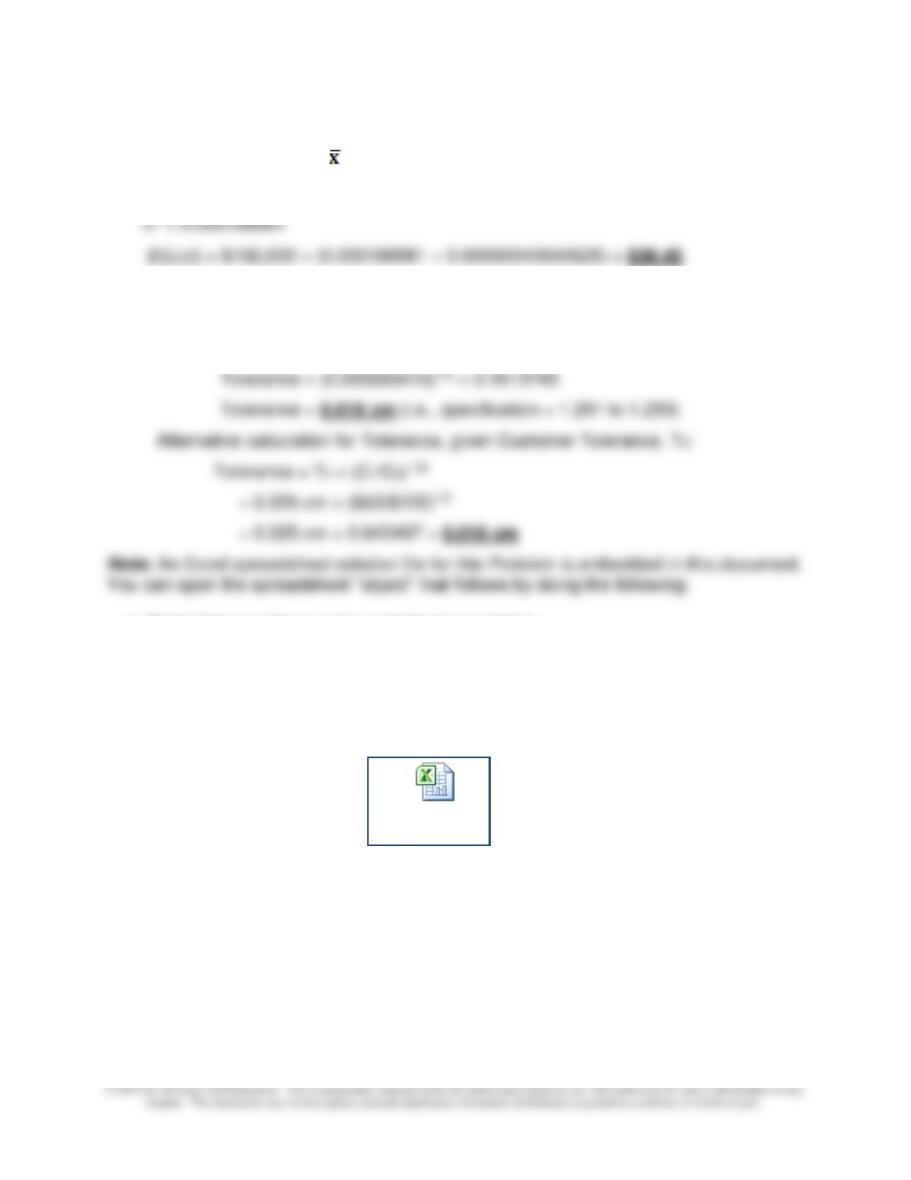

17–48 (Continued)

Mean actual diameter, = 1.2756500

D2= (1.2756375 − 1.275000)2 = 0.00000040640625

2. Allowed tolerance:

Repair Cost = k × (Tolerance) 2

$50 = $192,000 × (Tolerance)2

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to the

Word document.

Pr. 17-48.xlsx

Chapter 17 – The Management and Control of Quality

17–51

17–49 Research Assignment, Strategy (60 Minutes)

1. As noted in the forward to the article (HBR, July-August, 2005, p. 107):

When the Gallup Organization applied Six Sigma principles to sales and

service groups at several companies, it learned how much performance

variation exists between seemingly similar work groups. Managing that

variability can raise overall performance by orders of magnitude and can

create organic growth.

In Chapter 17, we discuss the notion of improving quality through a reduction in

variation from standard. However, this discussion was made solely within the context

of a manufacturing setting. Thus, in that context, students come to realize that quality

can be measured by the extent to which there is variation in product specifications.

The overall purpose of the cited HBR article is to extend student thinking by applying

the manufacturing-based notion of process variation to the management of human

capital. As such, the discussion pertains (as illustrated by the above quote) to sales

and customer-service groups within organizations.

2. Six Sigma, as developed and applied in a manufacturing setting, focuses on

underlying engineering (or economic) relationships and in this sense is considered

data-driven, rational, and analytical. In short, typical Six-Sigma implementations

require the use of rigorous analytical standards; the goal is to refine and continuously

coined by the authors to describe the quality-improvement approach they developed.

Notably, rather than focusing on the management of physical processes, Human

Sigma represents a way to manage the employee-customer encounter.

3. The authors propose that a single overall metric, called the “Human Sigma score,”

which combines two performance indicators—employee and customer engagement.

(The particulars regarding this metric are provided on page 114 of the article.) At its

Chapter 17 – The Management and Control of Quality

17–52

17–49 (Continued)

The authors hypothesize that emotional attachment, both from customers and from

employees, is an important leading indicator (or predictor) of financial performance.

They state (p. 110) that “Performance metrics that acknowledge the importance of

emotional engagement—on the part of both employees and customers—provide

much stronger links to desired financial and operational outcomes.”

To support this claim, they provide data from a large retail bank in the U.S. Data from

both employee and customer engagement metrics (i.e., the components of the

Human Sigma score) are, on average, 3.4 times more effective financially than units

ranked in the bottom half on both metrics. Those business units ranked relatively high

on one but not both of these dimensions on average were only about half as effective

as those units scoring high on both dimensions.

4. The authors offer (pp. 113-114) three suggestions for how to manage and reduce

customer and employee engagement at the local level (i.e., at the level where

performance variation occurs):

a) Centralize Responsibility for Human Sigma—based on the preceding arguments,

customer and employee engagement need to be managed “holistically,” not

the management of employee and customer engagement.

c) Overhaul HR Practices—in some cases, the authors argue that more substantive

(transformational) interventions regarding the overall management process may be

needed. This would be the case if the organization as a whole is experiencing

relatively low Human Sigma scores or if parts of the organization are consistently

generating low HS scores.

17–53

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

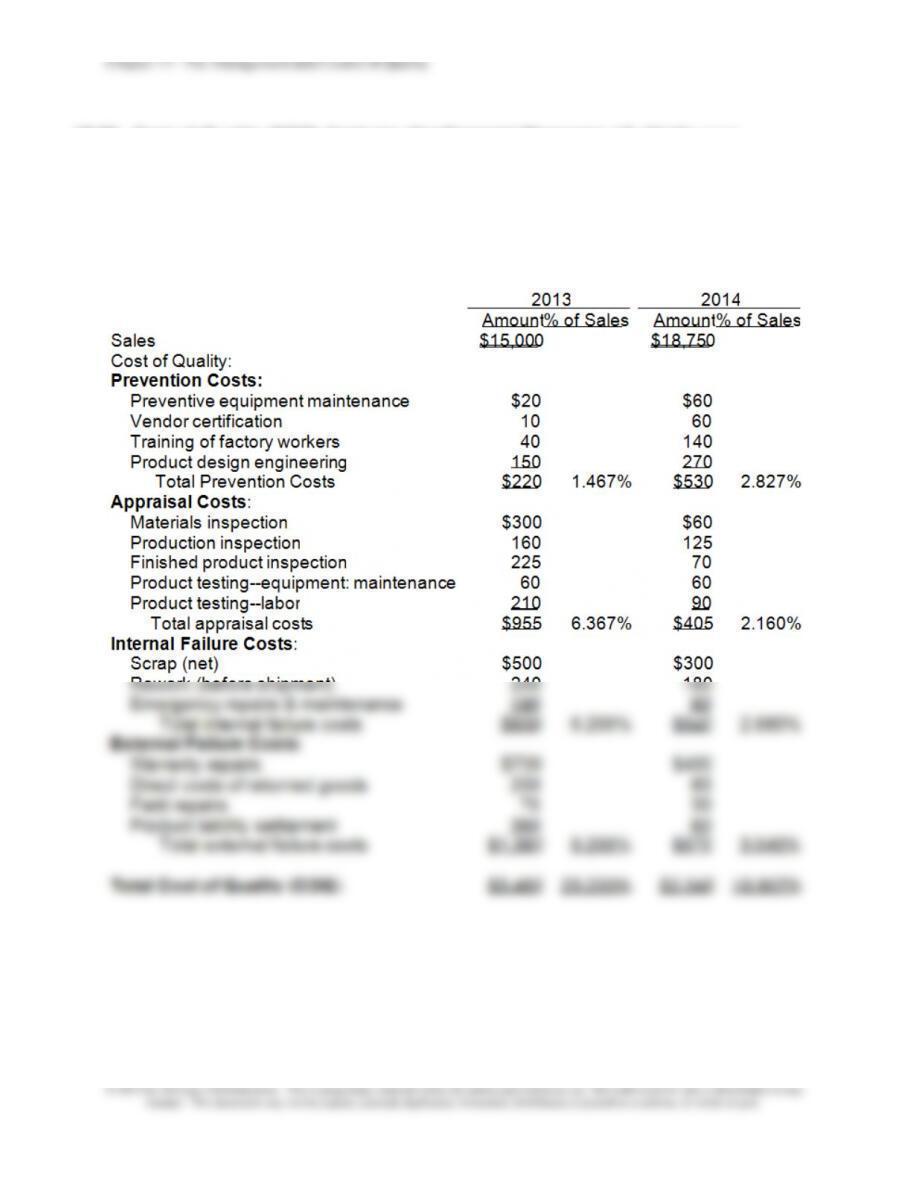

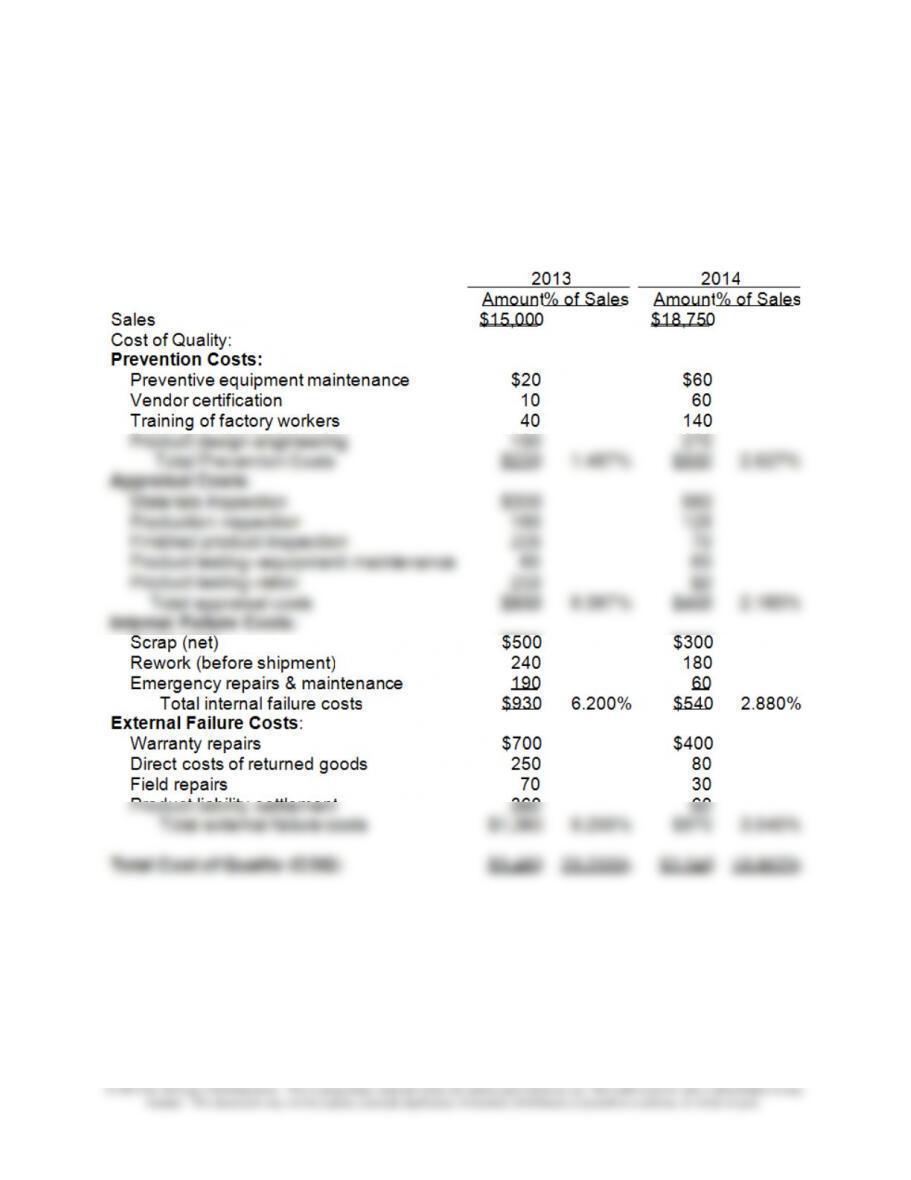

17–50 Cost-of-Quality (COQ) Analysis; Nonfinancial Measures (45–60 Minutes)

1. and 2. Cost-of-Quality (COQ) Report

Duncan Materials Company

Cost of Quality (COQ) Report

2013 and 2014

17–54

17–50 (Continued)

3. From 2013 to 2014, Duncan’s total cost of quality (COQ) has decreased from

23% of sales to 11% of sales. Part of the decrease in COQ as a percentage of

sales is the higher sales in 2014 compared to 2013. However, even without the

4. To complement the COQ data, the company may want to collect both internal

and external nonfinancial measures of quality, such as the following:

Internal Measures of Quality

▪ The number of defects per period

▪ Process yield (ratio of good output to total output)

▪ Percentage first-pass yield

date to the total units shipped)

▪ Surveys of customer satisfaction

Chapter 17 – The Management and Control of Quality

17–55

5. As should be obvious from an examination of Exhibit 17.3, there is a role for

both financial and nonfinancial quality data (metrics) in a comprehensive

framework for managing and controlling quality. COQ (i.e., financial) data are

reported only periodically. As such, they are likely of greater interest/value to

managers. After all, these are the individuals who ultimately have responsibility

over financial performance and who make spending and investment decisions

regarding quality costs.

Operating personnel, on the other hand, are likely to find nonfinancial quality

data to be more useful. For one thing, such data are expressed in terms that

are understandable/comprehensible to operating personnel. For another thing,

Chapter 17 – The Management and Control of Quality

17–56

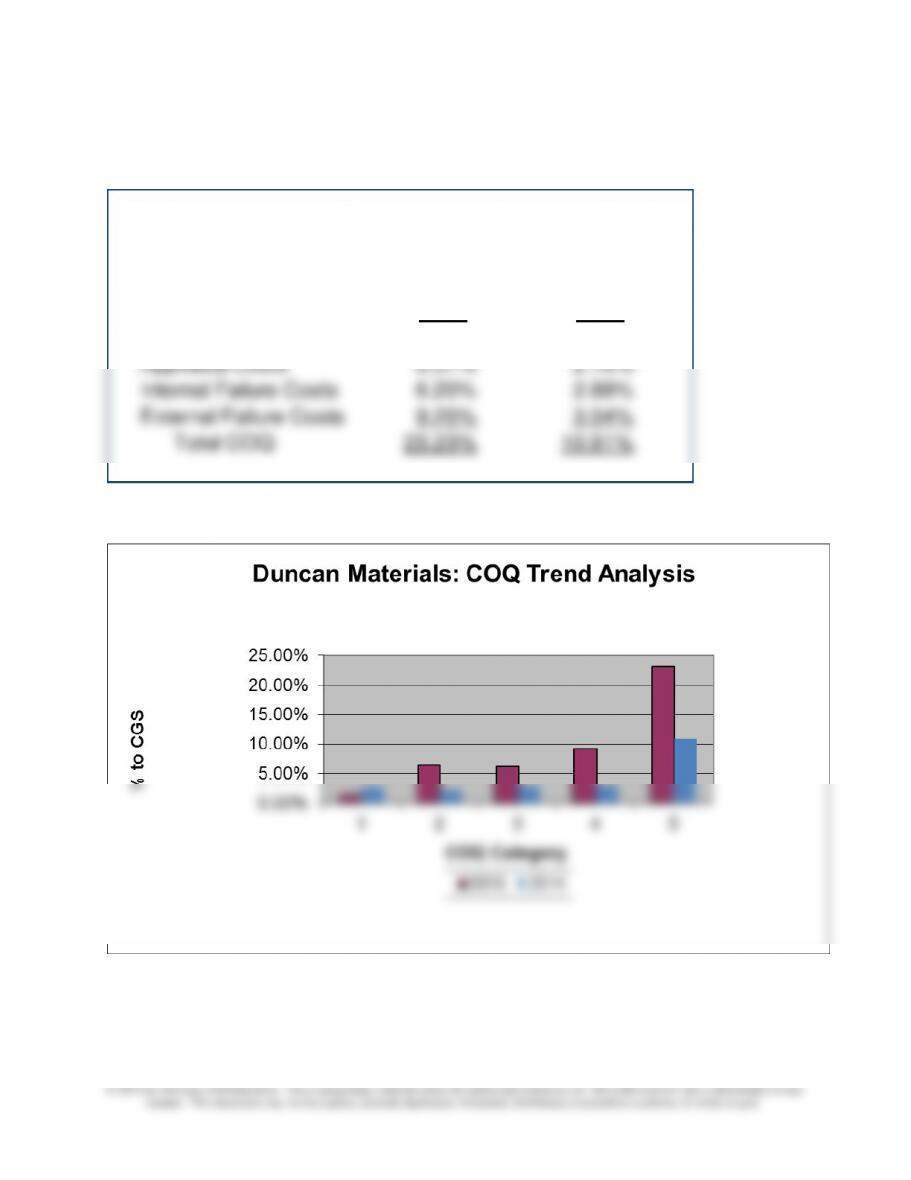

17–51 Cost-of-Quality (COQ) Analysis—Spreadsheet Application (60 Minutes)

1-4: Cost of Quality (COQ)—Excel-Generated Report

Duncan Materials Company

Cost of Quality (COQ) Report

2013 and 2014

Chapter 17 – The Management and Control of Quality

17–51 (Continued-1)

5. Data for Trend Analysis (2013 and 2014 Category Results)

Duncan Materials Company

Cost of Quality (COQ)—Trend Analysis

2013 and 2014

2013 2014

Prevention Costs 1.47% 2.83%

Appraisal Costs 6.37% 2.16%

Internal Failure Costs 6.20% 2.88%

External Failure Costs 9.20% 3.04%

Total COQ 23.23% 10.91%

6. Bar Chart: COQ Report, 2013 and 2014

COQ Categories:

1 = Prevention Costs 4 = External Failure Costs

2 = Appraisal Costs 5 = Total COQ

3 = Internal Failure Costs

17–58

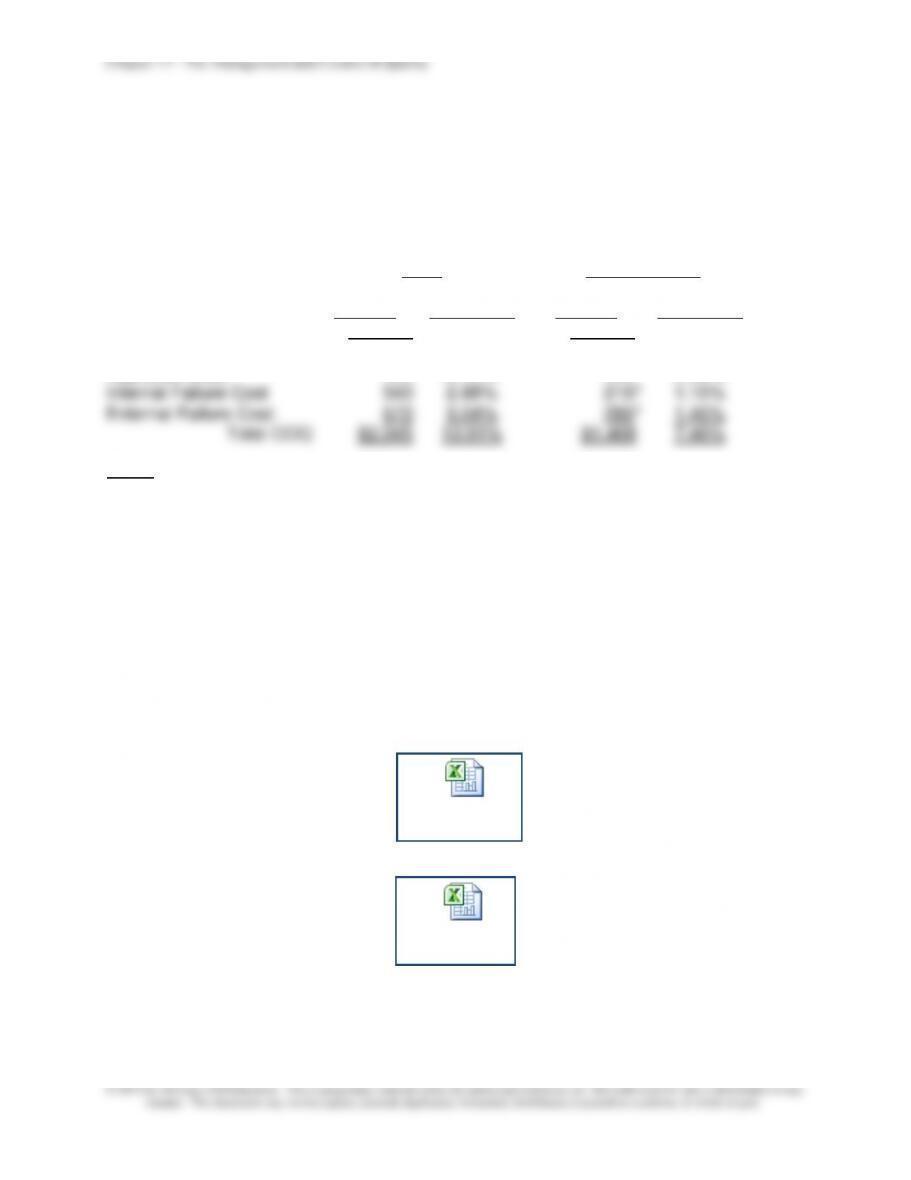

17–51 (Continued-2)

7. Sensitivity Analysis

Duncan Materials Company

Cost-of-Quality (COQ) Report

Sensitivity Analysis

2014

2014–Revised

Amount

Cost as a

% of Sales

Amount

Cost as a

% of Sales

Sales

$18,750

$19,6881

Prevention costs

$530

2.83%

$5622

2.85%

Appraisal costs

405

2.16%

405

2.06%

Internal Failure Cost

540

2.88%

2163

1.10%

External Failure Cost

570

3.04%

2854

1.45%

Total COQ

$2,045

10.91%

$1,468

7.46%

Notes:

11.05 × $18,750 30.40 × $540

21.06 × $530 40.50 × $570

Note: An Excel spreadsheet solution file for this Problem is embedded in this

document. You can open the spreadsheet “object” that follows by doing the

following:

1. Right click anywhere in the worksheets below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

the Word document.

Pr. 17-50.xlsx

Pr. 17-51.xlsx

Chapter 17 – The Management and Control of Quality

17–59

17–52 Ethics (45–50 Minutes)

1. COQ provides a general, comprehensive framework for reporting quality-related

costs using a four-category approach: prevention costs, detection/appraisal costs,

internal failure costs, and external failure costs. Thus, the COQ framework can

theoretically be applied to the management and control of environmental-related

quality costs. That is, it is theoretically possible for an organization to prepare a

Cost of Environmental Quality Report. Such a report would likely be of use to

managers for many of the same reasons that managers see value in a COQ

report:

▪ A Cost of Environmental Quality Report brings together environmental quality

spending trade-offs across categories (e.g., do investments in the prevention

area result in decreased environmental failure costs?).

2. Several Standards from the IMA’s Statement of Ethical Professional Practice

(www.imaorg.net; note—login name and password are needed) relate to the

ethical situation faced by Williams. The crux of the matter, however, is that

Williams has an ethical responsibility to take some action in the matter of

GroChem, Inc. and the dumping of toxic wastes. Specific Standards that relate to

the present context are as follows:

Competence—management accountants have a responsibility to perform their

professional duties in accordance with relevant laws and regulations.

Confidentiality—in general, management accountants are required to keep

internal controls, in conformance with organization policy and/or applicable laws.

17–60

17–52 (Continued)

3. In accordance with the IMA Standards, the first alternative (seeking the advice of

her boss) is appropriate. To resolve an ethical conflict, the IMA Standards specify

stage. Basically, the IMA Standards specify that Williams should report the

conflict to successively higher levels within the organization and turn only to the

Board of Directors if the problem is not resolved at lower levels.

4. Jan Williams should follow the established policy of the organization bearing on

the resolution of such conflict. If these policies do not resolve the ethical conflict,

Williams should report the problem to successively higher levels of management,

up to the Board of Directors, until it is satisfactorily resolved. There is no