Chapter 6 – Process Costing

6-40

Problem 6-50 (continued –2)

Ted is apparently correct about the under-costing of ending working

process. The activity-based method, which separates the batch-related

costs from the other conversion costs, shows $104,329 ending work in

Chapter 6 – Process Costing

6-41

6-51 FIFO Method with Rising Prices (30 min)

1.,2.

Physical Percent

Units Completion Materials Conversion Materials Conversion

Beginning WIP 14,000 100%

Materials 100% 14,000

Conversion 25% 3,500

Units started or Trans-in 33,000 100%

Total to account for 47,000

Units Finished or Trans-out 34,000 100% 34,000 34,000 34,000 34,000

Normal spoilage 1,000 100% 1,000 1,000 1,000 1,000

Abnormal spoilage – 100% – –

Ending WIP 12,000 100%

Materials – 100% 12,000 12,000

Conversion –

40% 4,800 4,800

Total accounted for 47,000 – – – –

Total Equivalent Units 47,000 39,800 33,000 36,300

COST ADDED

Materials Conversion Total

Beginning WIP 3,500$ 3,400$ 6,900$

Current Costs 66,000 104,000 170,000

TOTAL 69,500$ 107,400$ 176,900$

WTAVG Cost per EU 1.4787$ 2.6985$ 4.1772$

FIFO Cost per EU 2.0000$ 2.8650$ 4.8650$

Cost Accounted For: Weighted Average Completed Ending Work

& Trans-out in Process Total

Finished Goods 34,000 units 142,025$ 142,025$

plus Normal Spoilage 1,000 units 4,177 4,177

Total 146,203

Ending Work-in-process 12,000 units

Materials 12,000 units 17,745 17,745

Conversion 4,800 units – 12,953 12,953

Total Costs Accounted For 146,203$ 30,697$ 176,900$

Cost Accounted For: FIFO

Finished Goods 34,000 units

Normal Spoilage 1,000 units 4,865$

Prior period costs in Beginning WIP 6,900

Current cost to complete Beginning WIP

Materials –

Equiv units

–

Conversion 10,500

Equiv units

30,083

Units started & finished 20,000

Equiv units

97,300

TOTAL 139,148$

Ending WIP 12,000 units

Materials 24,000 24,000

Conversion – 13,752 13,752

Total Costs Accounted For 139,148$ 37,752$ 176,900$

—–This Dept—–

Weighted Average

Equivalent Units

FIFO

Equivalent Units

Chapter 6 – Process Costing

6-42

6-51 (continued –1)

3. The CFO is on the right track to consider FIFO costing. With prices

rising rapidly, FIFO provides a way to separate the current and prior

period costs, so that the price increases can be examined and

charged properly to each period’s production. Note that in this case

there is a sizeable amount of beginning and ending work-in-process

inventory, which makes the issue of separating prior period and

For a company like HSC that competes on quality and brand loyalty,

it is likely that the company will be able to pass along at least a good

portion of these increased costs. The FIFO method provides HSC a

good tool to watch the cost changes as they affect the company’s

inventory and cost of goods sold from month to month, and in this

way provide a solid basis for determining the price increases that will

ultimately be necessary.

Chapter 6 – Process Costing

6-43

6-52 Weighted Average Method; Two Departments

1. Production Cost report for the mixing department

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 28,000

Materials 100%

Conversion 60%

Units started 74,000

Total to account for 102,000

Units Finished 76,000 76,000 76,000

Ending WIP 26,000

Materials 100% 26,000

Conversion –

60% 15,600

Total accounted for 102,000 – –

Total Equivalent Units 102,000 91,600

Cost Added Materials Conversion Total

Beginning WIP 56,480$ 282,400$ 338,880$

Current Costs 288,500 989,400 1,277,900

TOTAL 344,980$ 1,271,800$ 1,616,780$

WTAVG Cost per EU 3.3822$ 13.8843$ 17.2664$

Units Completed

Units in Ending

Cost Assigned – Weighted Average

and Transferred

WIP

Out Inventory Total

Finished Goods

76,000 gallons 1,312,249$ $1,312,249

Ending WIP

26,000 gallons

Materials 87,936 $87,936

Weighted Average

Equivalent Units

Chapter 6 – Process Costing

6-52 (continued –1)

2. Process cost report for reacting department

Physical Percent Transferred

Units

Completion

in Costs Materials Conversion

Beginning WIP 16,500 100%

Materials 0%

Conversion 30%

Units started or Trans-in 76,000 100%

Total to account for 92,500

Units Finished or Trans-out 72,000 100% 72,000 72,000

Normal spoilage 2,250 2,250 2,250

Ending WIP 18,250 100% 18,250

Materials – 0% –

Conversion –

40% 7,300

Total accounted for 92,500 – – –

Total Equivalent Units 92,500 81,550

Cost Added

Trans-in Materials Conversion Total

Beginning WIP 242,150$ –$ 412,510$ 654,660$

Current Costs 1,312,249 – 1,245,320 2,557,569

TOTAL 1,554,399$ –$ 1,657,830$ 3,212,229$

WTAVG Cost per EU 16.8043 0.0000 20.3290 37.1333

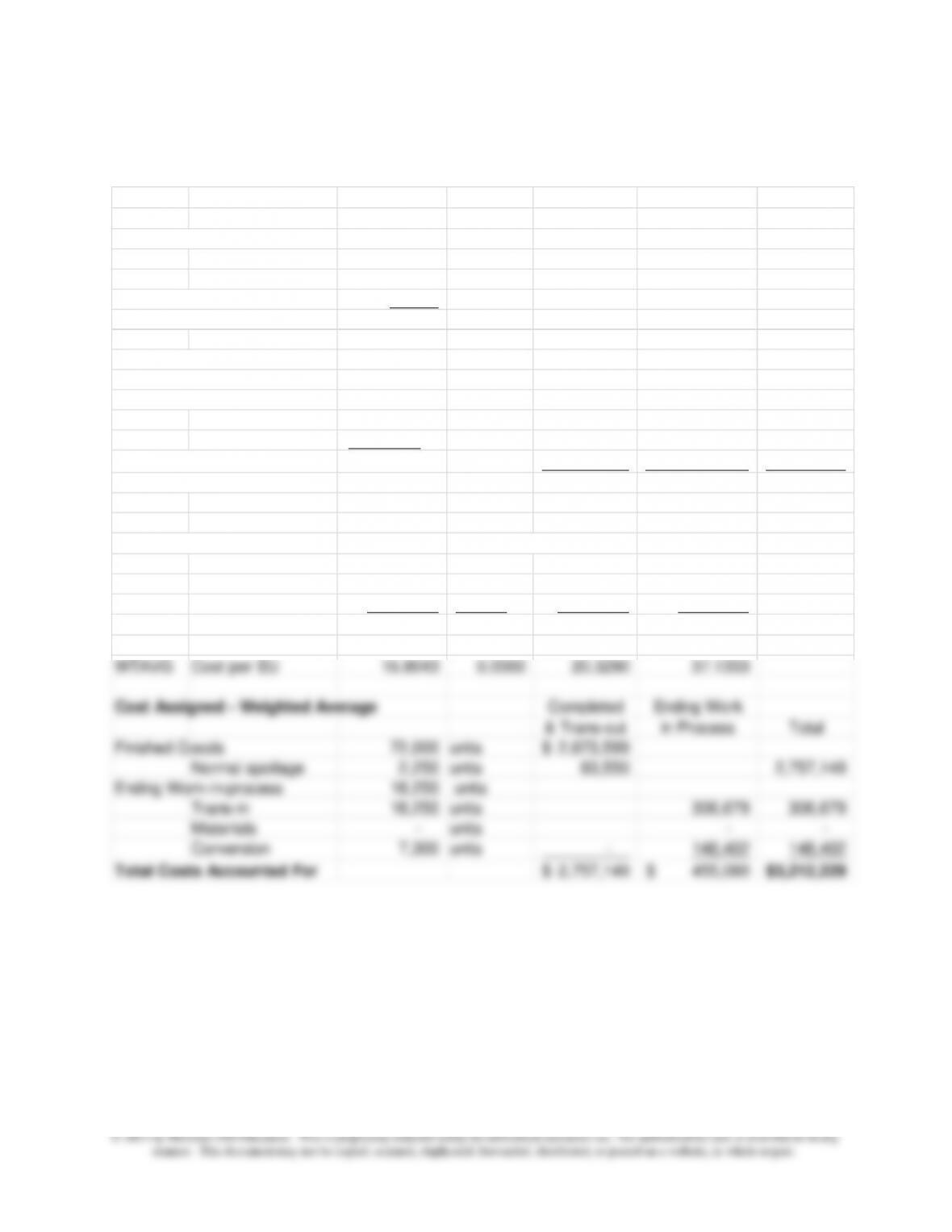

Cost Assigned – Weighted Average Completed Ending Work

& Trans-out in Process Total

Finished Goods

72,000 units 2,673,599$

Normal spoilage 2,250 units 83,550 2,757,149

Ending Work-in–process

18,250 units

Trans-in 18,250 units 306,679 306,679

Materials – units – –

Conversion 7,300 units – 148,402 148,402

Total Costs Accounted For 2,757,149$ 455,080$ 3,212,229$

——–This Dept––—

6-45

6-52 (continued –2)

3. Some observations about the two cost reports:

• The amount of normal spoilage is relatively small at less than

3%. Why, however, does the firm not consider accounting for

abnormal spoilage to take into account the cost of spoilage

arising from for example: operating error, impure materials,

delays or interruptions in processing, etc. The additional

in materials cost over time

4. The company’s strategy is best described as a differentiation strategy

based upon its focus on research, product development and

customer service. Note in particular that the company has focused

on a small number of customer that purchase in large quantities. So

a part of the company’s strategy is to achieve strong profits through

lower downstream costs, as noted in the previous chapter in the

the customer.

The company uses a combination of job and process costing. Job

costing is a good fit for the company’s strategy of focusing on large

purchases; the job costs are efficiently and conveniently allocated to

these large purchase orders. Also, the use of process costing

Chapter 6 – Process Costing

6-46

6-53 Backflush Costing

(1) Materials purchased.

Materials Inventory 690,000

Accounts Payable, Cash 690,000

(2) Conversion cost incurred.

Conversion Cost Incurred 1,300,000

(4a) Close the two conversion cost accounts to Cost of Goods Sold:

Conversion Cost Applied 1,317,500

Cost of Goods Sold 17,500

Conversion Cost Incurred 1,300,000

(4b) Close the actual usage of inventory to Cost of Goods Sold

1. Note to Instructor: the above treatment of the differences between

actual and applied materials and conversion is simplified for this brief

section on backflush costing, and assumes that the topic is covered

prior to standard costing. If covered after standard costing, the

treatment of the materials and conversion variances can be

enhanced.

Chapter 6 – Process Costing

6-47

2. Backflush costing is used when the level of work-in-process inventory

is very small. This can be the case for firms that use just–in-time