Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–76

18-59 (continued –1)

3. The scorecard perspectives appear to be correctly aligned with the

mission statement which has goals for improvement in terms of patient

care, physician satisfaction, and overall staff satisfaction. The

perspectives of process and quality improvement should support the

satisfaction of patients, while the focus on the organizational health

4. The strategy map is likely to follow the sequence of perspectives

provided in the article.

Organization Health, as the foundation of the

strategy map, supports…

Process Improvement, which in turn supports…

Quality Improvement, which in turn supports…

Volume and Market Share Growth, which finally

supports…

Financial Results

5. It is unlikely that a profit center approach alone would be able to

capture the breadth of goals that BHHS has. In this case, because of

Source: “Journey to Destination 2005,” by Andra Gumbus, Bridget Lyons,

and Dorothy E. Bellhouse, Strategic Finance, August 2002, pp. 46-50.

18–77

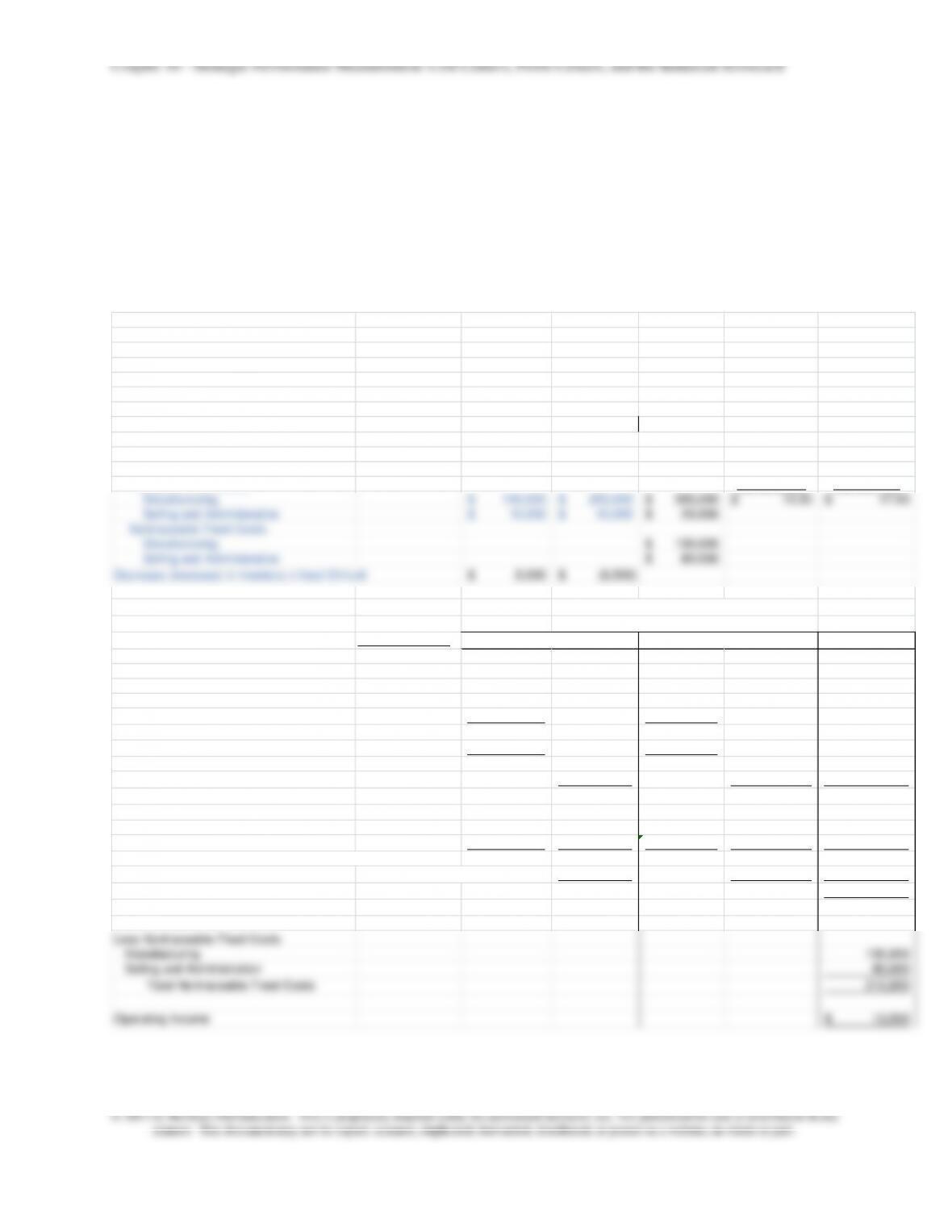

18–60 Value Streams and Profit Centers (30 min)

1. The value stream income statements for the two value streams of

Anderson Company is shown below. The value stream income

statement is based on a contribution type income statement (variable

costing-based) to which is added the effect of a change in inventory

level on income, thereby converting the variable costing income

statement to a full cost statement.

Units DVD Group TV Group

Beginning Inventory 200 900

Price 55$ 45$

Sold 13,500 15,500

Actual Production 14,000 15,000

Budgeted Production 14,000 15,000

Ending Inventory 700 400

DVD Group TV Group Total

Unit Variable Costs

Manufacturing 30$ 16$ Traceable Traceable

Selling and Administrative 5$ 5$ Fixed Mfg Cost Fixed MFG Cost

Traceable Fixed Costs Per unit DVD Per unit TV

Manufacturing 140,000$ 255,000$ 395,000$ 10.00$ 17.00$

Selling and Administrative 10,000$ 10,000$ 20,000$

Nontraceable Fixed Costs

Manufacturing 130,000$

Selling and Administrative 80,000$

Decrease (increase) in inventory x fixed OH/unit 5,000$ (8,500)$

Anderson Company

Income Statement

DVD Calculations Total

Sales =13,500 x $55 742,500$ 697,500$ 1,440,000$

Cost of Goods Sold (variable costs only)

Contribution Margin 270,000$ 372,000$ 642,000

Less Traceable Fixed Costs

Manufacturing 140,000 255,000

Selling and Administration 10,000 150,000 10,000 265,000 415,000

Value Stream Income before inventory change 120,000 107,000 227,000

Increase (decrease) in inventory =(700-200) x ($140,000/14,000) 5,000 (8,500) (3,500)

Value Stream Profit 125,000$ 98,500$ 223,500

Less Nontraceable Fixed Costs

Manufacturing 130,000

Selling and Administration 80,000

Total Nontraceable Fixed Costs 210,000

Operating Income 13,500$

DVDs

TVs

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–78

18–60 (continued –1)

Note that the effect on value stream income of a change in inventory

is displayed separately in the income statement; there is a $5,000

increase in income for the DVD group (because of an increase in

inventory of DVDs; ending inventory increases from 200 to 700,

where 700=200+14,000-13,500) and a decrease in value stream

company operating income of $13,500.

2. The value stream income statements show that both value streams

are profitable though the DVD value stream has a higher value

stream return on sales ($125,000/$742,500 = 16.8%) relative to the

TV value stream ($98,500/$697,500 = 14.1%). One reason for the

lower returns for TVs is that the TV group has reduced inventory

3. The value stream income statement is a combination of the variable

costing and full costing income statement that shows as a separate

line item in the statement the effect of inventory change on income.

For a useful reference on lean accounting and value streams, see:

Frances A. Kennedy and Peter C. Brewer, “Lean Accounting: What’s it All

About,” Strategic Finance, November 2005, pp. 27-34.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–79

18–61 Cost Centers; The Finance Function; Spreadsheet Application

(25 min)

The data are for selected countries from the A.T. Kearney 2007 survey.

1. There are a large number of strategies for ranking the countries, so there

are a number of possible rankings. Here are a few ways to develop the

ranking:

1. Sum the three criteria and then rank the countries on this number;

this would be useful if the criteria are equally weighted, though the

financial attractiveness measure would have a slightly larger

weight since it is scored on the range 0-4 while the other two are

scored on a smaller range, 0-3.

2. Weight the three criteria; for example, if the firm is interested

above would be used to rank the remaining firms.

A variety of different ranking methods are possible. The following ranking is

developed using the approach that is similar to the third approach above.

A country is deleted if business environment is less than 1.5 or skills

availability is less than 1.0. The remaining countries are ranked on the

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–80

Financial Skills Business Weighted

Attractiveness Availability Environment Score*

China 2.93 2.25 1.38 2.416

Thailand 3.19 1.21 1.62 2.282

Bulgaria 3.16 1.04 1.56 2.204

Malaysia 2.84 1.26 2.02 2.202

Mexico 2.63 1.49 1.61 2.084

Chile 2.65 1.18 1.93 2.065

Slovakia 2.79 1.04 1.79 2.065

Poland 2.59 1.17 1.79 2.004

Czech Republic 2.43 1.10 2.05 1.955

Estonia 2.44 0.96 2.20 1.948

Singapore 1.65 1.51 2.53 1.784

* weight is .5,.3,.2

18–61 (continued –1)

The results show that China is the most highly ranked and Thailand,

Bulgaria and Malaysia are a close second. China’s relatively low scores on

financial attractiveness and business environment are more than made up

for by the highest score on skills availability. A firm should carefully

consider whether the level of skills availability should be the deciding factor

given the high weighting on financial attractiveness and the fact that

Thailand and Bulgaria are the highest on financial attractiveness. Also,

democratically-elected. Also, in 2011 Thailand is suffering from disastrous

flooding. The 2011 measure of business environment might be somewhat

lower than for 2007.

2.

Strategic issues to consider in the potential outsourcing of the finance

function include:

• Before choosing to outsource, the firm must first determine if the

finance function is strategically critical in day-to-day decision making.

This would be true for example if the firm operated in a dynamic,

differentiated market, in which financial analysis was a key part of

18–81

18–61 (continued –2)

function is to pay the bills and record customer payments and the

like, then outsourcing to a reliable, low cost provider makes sense.

• If the decision is made to outsource, then additional measures of the

country’s suitability should be considered. These could include

political stability, availability of high-speed internet support, language,

Reference: Kate O’Sullivan, “Where in the World is Your Offshore Finance

Team?” CFO.com, January 31, 2008. Source cited: A. T. Kearney Global

Services Location Index.

18–82

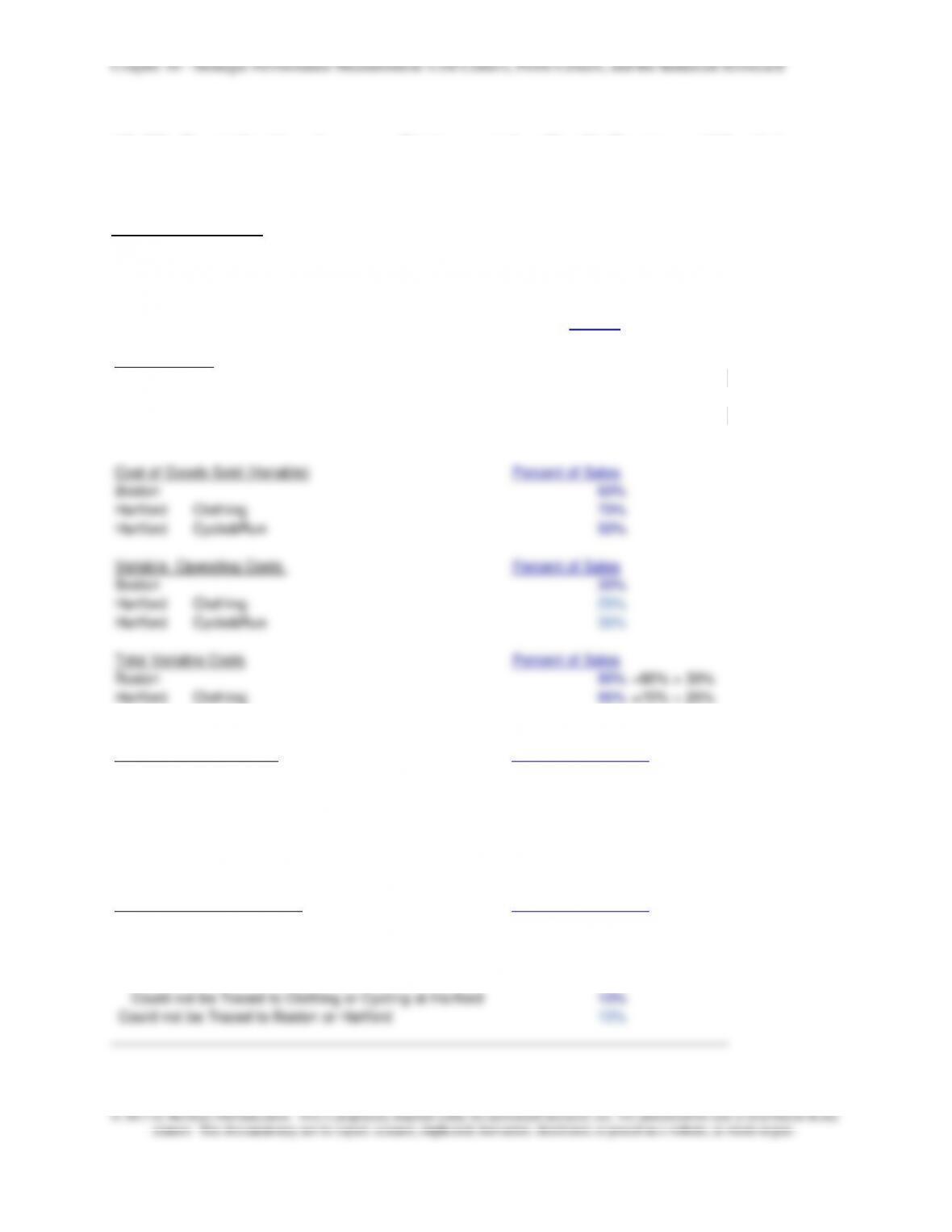

18–62 Contribution Income Statement for Profit Centers (40 min)

1.

Data Summary:

Total Net Sales ($6,875,000 Hartford; $5,625,000 Boston) 12,500,000$

Fixed Costs

Partly Traceable and Controllable 400,000

Partly Traceable but Noncontrollable

350,000

Nontraceable Costs 325,000

1,075,000

Total Net Sales

Boston 5,625,000$

Hartford Total Sales 6,875,000$

Hartford Clothing 60%

Hartford Cycle&Run 40%

Cost of Goods Sold (Variable) Percent of Sales

Boston 60%

Hartford Clothing 70%

Hartford Cycle&Run 50%

Variable Operating Costs Percent of Sales

Boston 30%

Hartford Clothing 25%

Hartford Cycle&Run 35%

Fixed Noncontrollable Costs Percent of Total Cost

Boston 40%

Hartford Total 50%

Clothing 55%

Cycle&Run 35%

Could not be Traced to Clothing or Cycling at Hartford 10%

Could not be Traced to Boston or Hartford 10%

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–83

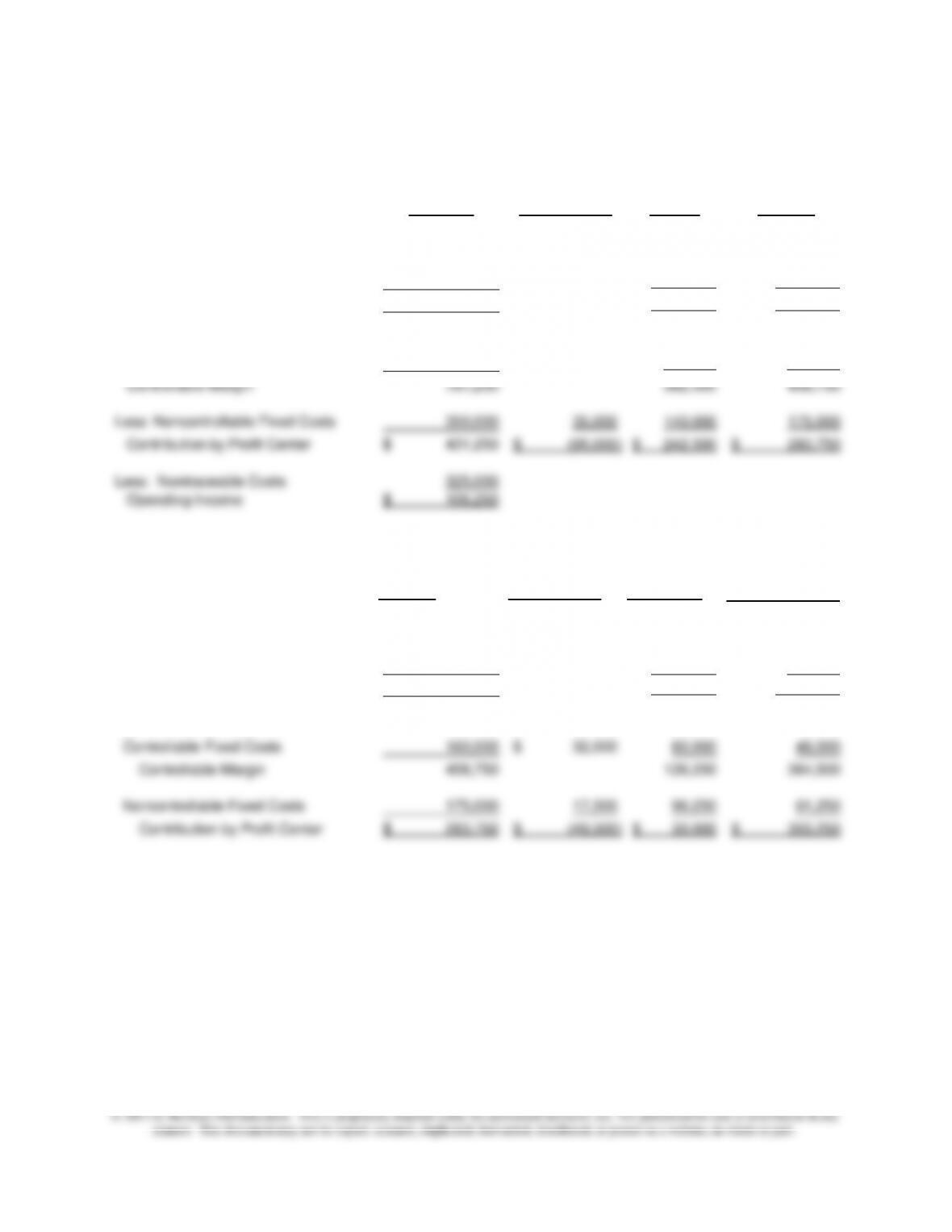

18–62 (continued –1)

Income Statement by Business Unit

Combined

Company Not Allocated Boston Hartford

Net Sales 12,500,000$ 5,625,000$ 6,875,000$

Variable Costs:

COGS 7,637,500 3,375,000 4,262,500

Operating Costs 3,681,250 1,687,500 1,993,750

Total Variable Costs 11,318,750 5,062,500 6,256,250

Contribution Margin 1,181,250 562,500 618,750

Less:Controllable Fixed Costs 400,000 60,000$ 180,000 160,000

Controllable Margin 781,250 382,500 458,750

Less: Noncontrollable Fixed Costs 350,000 35,000 140,000 175,000

Contribution by Profit Center 431,250$ (95,000)

$ 242,500

$ 283,750

$

Less: Nontraceable Costs 325,000

Operating Income 106,250

$

Breakdown of contribution: Hartford

Hartford Not Allocated Clothing Cycle & Run

Net Sales 6,875,000$ 4,125,000$ 2,750,000$

Variable Costs:

COGS 4,262,500 2,887,500 1,375,000

Variable Operating Costs 1,993,750 1,031,250 962,500

Total Variable Costs 6,256,250 3,918,750 2,337,500

Contribution Margin 618,750 206,250 412,500

Controllable Fixed Costs 160,000 32,000$ 80,000 48,000

Controllable Margin 458,750 126,250 364,500

Noncontrollable Fixed Costs 175,000 17,500 96,250 61,250

Contribution by Profit Center 283,750

$ (49,500)

$ 30,000

$ 303,250

$