Chapter 17 – The Management and Control of Quality

17–31

17–37(Continued-1)

The instructor might want to use some of the following example disclosures from First

Energy Corporation (https://www.firstenergycorp.com/environmental.html) for illustrative

purposes:

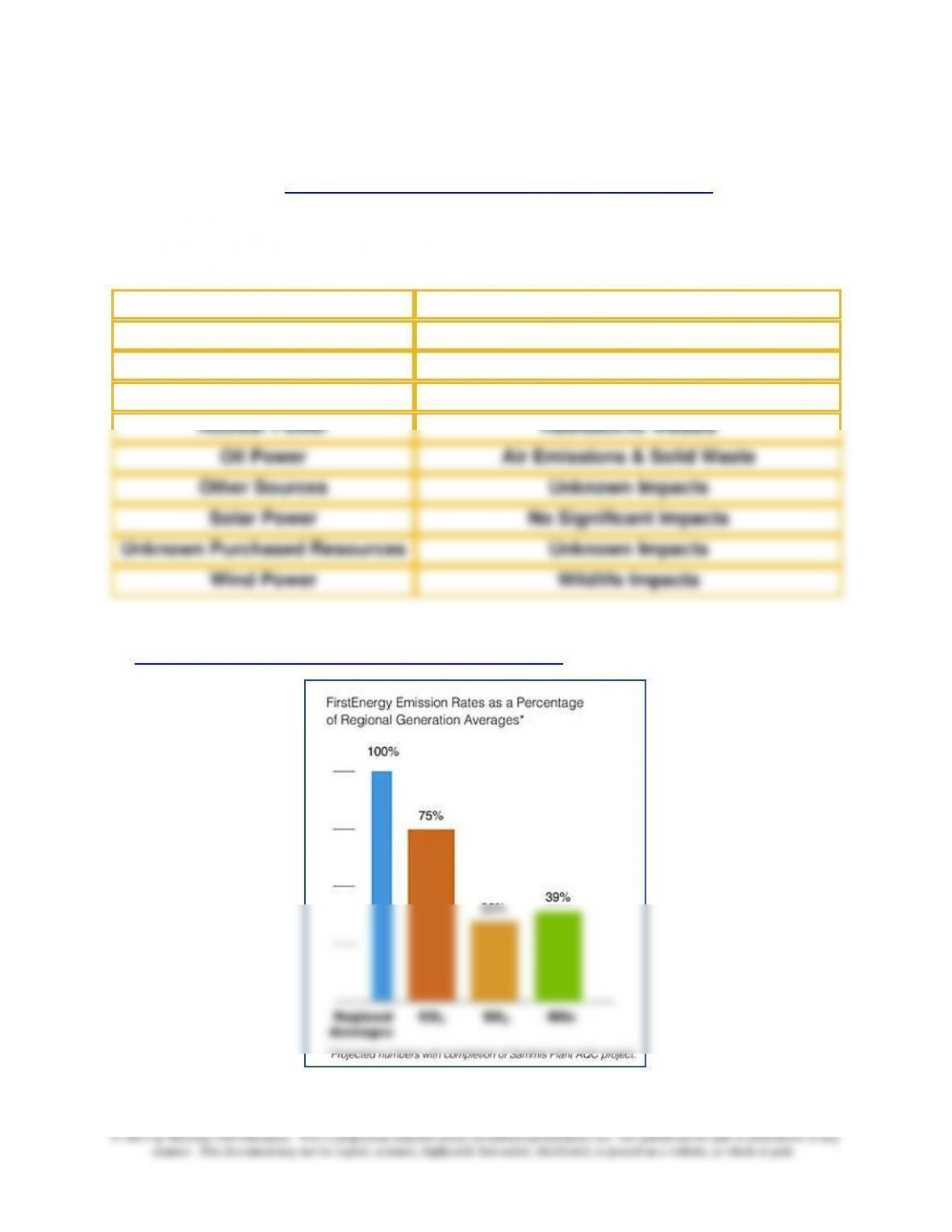

Environmental Characteristics Associated with Various

Sources of Power Generation

Biomass Power

Air Emissions & Solid Waste

Coal Power

Air Emissions & Solid Waste

Hydro Power

Wildlife Impacts

Natural Gas Power

Air Emissions & Solid Waste

Nuclear Power

Radioactive Wastes

Oil Power

Air Emissions & Solid Waste

Other Sources

Unknown Impacts

Solar Power

No Significant Impacts

Unknown Purchased Resources

Unknown Impacts

Wind Power

Wildlife Impacts

Air Emission Disclosure: First Energy Corporation, 2011

(https://www.firstenergycorp.com/environmental.html, accessed 25 November 2011)

website updated: 08 September 2011

Chapter 17 – The Management and Control of Quality

17–32

17–37(Continued-2)

Note: The following chart is no longer available on the FirstEnergy website, but is

viewed as instructive nonetheless.

Radioactive Waste Produced:

Projected (2007) vs. Actual (First Three Quarters 2007)

and Projected Data for 2008

2007

2008

Projected

Quantity

Actual

Quantity

Projected

Quantity

Measure

High-Level

Radioactive

Waste

0.0032

0.0032

0.0032

Lbs./1,000 kWh

Low-Level

Radioactive

Waste

0.0001

<0.0001

0.0003

Ft3/1,000 kWh

Chapter 17 – The Management and Control of Quality

17–33

17–38 Assessing the Use and Role of Nonfinancial Performance Indicators (45-60

Minutes)

1. Nonfinancial performance indicators pertain to areas such as customer loyalty and

employee satisfaction. The authors of this cited article argue that monitoring and

reporting such measures as part of a comprehensive management accounting and

control system is important because:

• as represented by the framework known as The Balanced Scorecard (BSC),

performance in these areas represents a precursor to financial performance

drivers of competitive advantage in the so–called “knowledge economy”

• such performance measures can aid top management in terms of the

resource-allocation decisions it must make (across divisions, product lines,

managers, etc.)

• these indicators can, if appropriately developed, be used to assess

managerial performance

2. The authors hypothesize that many organizations are not able to reap the benefits of

including nonfinancial performance indicators in their management accounting and

control systems because:

• haphazard selection of the set of nonfinancial performance indicators—many

organizations simply fail to choose and act on the right measures; in short,

proliferation of performance measures, many of which are not useful

predictors of financial performance)

Chapter 17 – The Management and Control of Quality

17–34

17–38 (Continued)

• there is a natural tendency (i.e., bias) for managers to choose performance

measures that make these managers “look good;” this is especially a concern

increase progressively over time. Among other things, this approach is

consistent with a long-term (strategic) use of nonfinancial performance

indicators.

• measurement errors—that is, companies choose performance indicators that

are not psychometrically sound (i.e., evidence regarding the validity of the

measures is not established)

3. The Institute of Management Accountants (IMA) has recently (December 11, 2008) a

revised its definition of “management accounting” (http://www.imanet.org [requires

log-in name and password]). This statement indicates that management accounting:

… is a profession that involves partnering in management decision–

making, devising planning and performance-management systems, and

an organization’s strategy. This implies a substantive role in the design of an effective

control system that includes both financial and nonfinancial performance measures.

Source: Christopher D. Ittner and David F. Larker, “Coming Up Short on Nonfinancial

Performance Measurement,” Harvard Business Review (November 2003), pp. 88-95.

Chapter 17 – The Management and Control of Quality

17–35

17–39 Pareto Diagram (15 minutes)

(1) (2) (3) (4) (5) (6)

(1) Personal emergency (32) (4) Unexpected visitor (11)

(2) A child’s illness (26) (5) Overslept (9)

(3) Personal illness (12) (6) Car broke down (8)

Pareto Charts (Diagrams) can be used for diagnostic control purposes, that is,

to identify the primary causes of an identified quality problem (such as

“absenteeism”) and, as such, to identify possible solutions to the problem. These

charts are named after the Italian economist Vilfredo Pareto; they provide a

prioritization of causes of an indicated quality problem, based on frequency of

occurrence. Thus, they focus attention on causes that could offer the greatest

potential for improving quality. A loose interpretation of the information contained

in Pareto charts is that a relatively small number (e.g., 20%) of causes represent

a majority (e.g., 80%) of reasons for the quality failure (here, absenteeism).

17–36

17–40 Relevant Cost Analysis—Quality Improvements (20-30 Minutes)

Estimated cost savings resulting from the recently enacted quality program come from

two sources:

1. Manufacturing cost savings associated with the reduction in rework costs:

= (reduction in reject rate) × (annual volume of output) × (total rework cost per

unit)

= (0.05 − 0.035) × 15,000 units × [($480 − 70 − 200) + ($362 – 80) + ($80 −

3. Total estimated savings due to quality improvement program

= rework cost savings + inventory financing cost savings

Chapter 17 – The Management and Control of Quality

17–37

17–41 Control Chart; Spreadsheet Application (45 Minutes)

1. Control Chart—Manufacturing Cycle Times (Weekly Data)

Control Chart: Destin Company

10

12

14

16

18

20

22

24

26

Week #

1

2

3

4

5

6

7

8

9

10

11

12

Week #

Manufacturing Cycle Time

(Weekly Average)

Average

2. The target cycle time is 14.0 minutes; the lower control limit is 12.0 minutes and

the upper control limit is 16.0 minutes. As indicated in the accompanying Excel file,

the mean of the 12 weekly observations is 15.2, while the sample standard

deviation is 3.6 minutes (which seems high).

Note: An Excel spreadsheet solution file for this exercise is embedded in this

document. You can open the spreadsheet “object” that follows by doing the

following:

1. Right click anywhere in the worksheet area below.

2. Select “worksheet object” and then select “Open.”

3. To return to the Word document, select “File” and then “Close and return to…”

while you are in the spreadsheet mode. The screen should then return you to

the Word document.

Ex. 17-41.xlsx

Chapter 17 – The Management and Control of Quality

17–38

17–41 (Continued)

3. As indicated in part (2), the mean of the sample observations (15.2) is not that far

from the target value (14.0). However, inspection of the control chart suggests

wide variability in the process, which is confirmed by the sample standard deviation

of the 12 observations around the mean value of the dataset. As well, we note that

warranted.

4. Management can determine the upper and lower control limits on their control

charts through experience (e.g., trial and error) or through the use of statistical

procedures. When these control limits are determined statistically (based on

Chapter 17 – The Management and Control of Quality

17–39

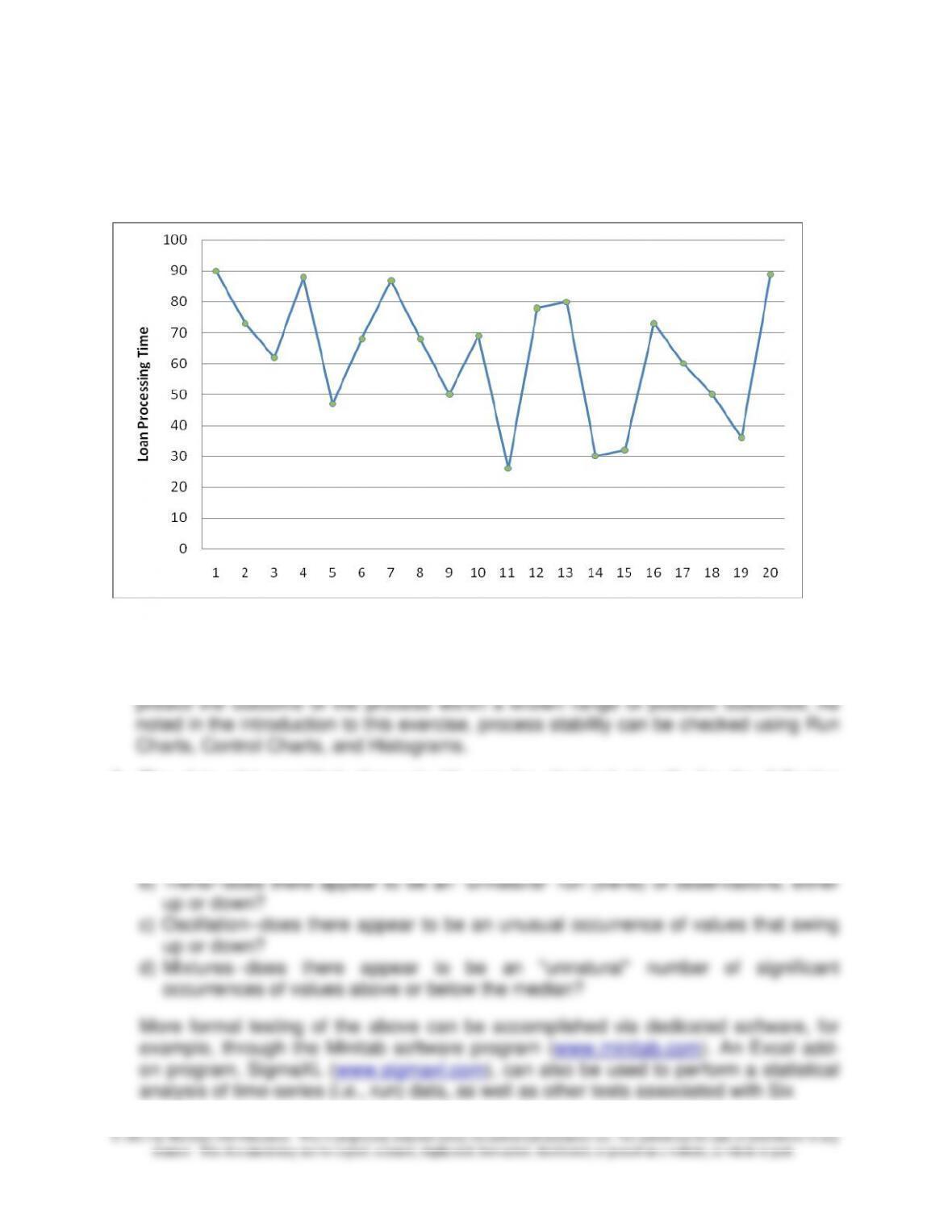

17-42 Using Run Charts to Examine Process Stability; Spreadsheet Application (30-

45 Minutes)

1. Time-series data plot:

Median Processing Time = 68.00; Mean (average) Processing Time = 62.80

2. The term “process stability” generally refers to how a process (in this case, loan

processing activity) performs over time. Having a stable process implies that you can

3. The data plot provided above in (1) can be checked visually for the following

indicators of process stability (or instability):

a) Clustering—is there what appears to be an “unnatural” grouping of values around

a certain observation?

Chapter 17 – The Management and Control of Quality

17–40

Sigma processes.

17–43 Benefits and Challenges of Lean (60minutes)

To: Management of MyOrg

From: I M Student

Re: Lean Accounting

You have asked me to provide information regarding: (1) the definition of “lean,” (2) the

strategic value of adopting lean principles, (3) anticipated costs of moving to lean, (4)

implications for cost-system design, and (5) sources for additional information. Below is

my response to your request.

1. The notion of “lean” can perhaps best be described as a philosophy or strategy of

meeting customer expectations in an increasingly competitive environment. As such,

the term is broad in that it encompasses changes in the way business processes are

executed as well as embracing the notion of continuous improvement coupled with

the elimination of waste and inefficiency. It was probably within this context that the

notion of the “lean enterprise” was coined. In such an organization, we usually find

changes in organizational structure: reduction of managerial layers accompanied by

an increased span of control. In turn, this change is supposed to result in faster and

more flexible decision-making. Finally, we note that some organizations, in

delivering its value proposition on time, error-free, and according to customer

expectations.

Note the distinction with “lean accounting,” which is a term normally used to describe

changes in the internal accounting system (i.e., the comprehensive management

accounting and control system) made to support the implementation of a “lean”

philosophy.

2. Strategically, the adoption of a lean philosophy can enable an organization to more

effectively deliver its stated value proposition to its targeted customer group. The

term “value proposition” is generally construed to mean meeting customer needs in

a unique, sustainable way—one that differentiates you from competitors. Thus, the

adoption of a lean philosophy should be of strategic importance to both cost–

3. Cost associated with the move to “lean” are similar to those associated with any

major philosophical shift for an organization:

Chapter 17 – The Management and Control of Quality

17–41

17–43 (Continued-1)

• Education—employees as well as managers need to be educated regarding the

the goals that accompany the switch to “lean.”

• Incentive System—to align employee actions with expectations and demands of

the “lean enterprise,” employee compensation and incentive plans might have to

be reconfigured.

While not specifically asked for, the instructor at this point might mention the

following anticipated benefits of moving to “lean:”

• Strategic benefits—see (1) and (2) above

• Short-term Cost Savings—associated with efficiency improvements/elimination of

wastes and the performance of non-value-added activities

• Reduction in Inventory-Holding Costs (both out-of-pocket and opportunity costs,

4. Management accounting systems should be constructed to support managerial

initiatives and prerogatives, such as transformation of an organization to a “lean

enterprise.” Broadly speaking, this change affects accounting-system design in at

least the following ways:

• Rather than periodic departmental-based cost reports, cost reporting is done on

a value-stream basis (see example in this chapter as well as Chapter 18 for

Chapter 17 – The Management and Control of Quality

17–42

overhead absorption and the calculation of direct-labor cost variances).

17–43 (Continued-2)

• Internal reporting is vastly decentralized (consistent with the “flattened”

organizational structure that may accompany a switch to “lean”), with information

prepared on a real-time basis; in this environment, the focus of the accounting

reports is on the efficacy of business processes that constitute each specified

value stream.

• As stated on p. 14 of the Statement of Management Accounting (IMA, 2006),

Value-Stream accounting includes relevant non-financial metrics, such as:

▪ productivity of the value stream as a whole (e.g., sales per person)

▪ performance to customer demand

▪ involvement activities of team members

▪ safety

5. Sources of additional information regarding “lean” and “accounting for lean:”

a. B. Maskell and B. Baggaley, Practical Lean Accounting: A Proven System for

Measuring and Managing the Lean Enterprise. New York: Productivity Press,

2004.

b. N. J. Sayer and B. Williams, Lean for Dummies. Hoboken, NJ: Wiley Publishing,

Inc., 2007.

c. Breakthrough Management Group, The Complete Idiot’s Guide to Lean Six

Sigma. New York: Penguin Group (USA), Inc., 2007.

d. R. J. Schonberger, Best Practices in Lean Six Sigma Process Improvement: A

Deeper Look, Hoboken, NJ: John Wiley & Sons, Inc., 2008.

e. A. van der Merwe and J. Thompson, “The Lowdown on Lean Accounting: Should

Management Accountants Get on the Bandwagon—or not?” Strategic Finance

(February 2007), pp. 26-33.

f. J. P. Brosnahan, “Unleash the Power of Lean Accounting,” Journal of

Accountancy (July 2008), pp. 60-66.

g. R. J. Schonberger, “Lean Performance Management (Metrics Don’t Add Up), Cost

Management (January/February, 2008). (Copyright Thompson/RIA, 2008.)

h. B. H. Maskell and F. A. Kennedy, “Why Do We Need Lean Accounting and How

Chapter 17 – The Management and Control of Quality

17–43

Does It Work?” The Journal of Corporate Accounting & Finance (March/April,

2007). (Copyright Wiley Periodicals, Inc., 2007.)

17–43 (Continued-3)

i. R. Cooper and B. Maskell, “How to Manage Through Worse-Before-Better,” MIT

Sloan Management Review (Summer 2008), pp. 58-65.

j. Websites:

http://www.leanaccountingnews.com

http://www.leanaccountingsummit.com

http://www.maskell.com/lean_accounting.html

http://www.imanet.org/resources_and_publications.aspx

Chapter 17 – The Management and Control of Quality

17–44

17–44 Implementation of Lean Accounting (20–30 Minutes)

This question is intended for class discussion. Here are some examples of points that

could be included in the discussion. The overview is that while many of the

implementation steps have been taken, the process of implementing a new system,

lean accounting, is likely to be a continuing challenge, as problems arise, new

employees are added, and changes in the competitive environment require the VSM to

be adapted.

1. As described in the problem, Watlow has implemented the first four of the

principles of lean: Customer value, Value Streams, Pull and Flow (inventory

reduction), and Empowerment (coordination and communication for employees).

2. Though not included in the description of Watlow’s implementation of lean, it is

likely that significant training was needed to prepare Watlow’s employees for the

new system, lean accounting. The challenge facing Watlow is to continue this

3. It will likely be a challenge for Watlow to sustain the energy and goodwill that was

generated in the employees as they felt included and valued in the

4. Will the implementation, by producing operating efficiencies, require the

reduction in facilities or the lay-off of certain personnel, or can this excess

capacity be utilized in new ways? What would be the impact on morale if

employees are laid off?

Source: Jan P. Bosnahan, “Unleash the Power of Lean Accounting,” Journal of

Accountancy, July 2008, pp. 60-66.

Chapter 17 – The Management and Control of Quality

17–45

17–45 Toyota—Keeping It Lean (15 Minutes)

Toyota, as a lean manufacturer, has employee empowerment as a key success factor.

Employee empowerment, the communication and coordination of employees, is a

principle of both lean manufacturing and of the Toyota Production System. It is

particularly important for Toyota, because of the strength of the culture of continuous

improvement at the company which has been one of hallmarks of its success.

Toyota’s continued success depends on its effectiveness in integrating new employees

quickly into the culture of continuous improvement, so that productivity and quality

continue to improve. Both quality and productivity are a concern for Toyota in recent

years. Quality defects are at a higher rate than in prior years and Toyota’s productivity,

while still the standard for the auto industry, has lagged the improvements made by its

competitors, as indicated by the following excerpt from the article:

One measure of productivity, the number of hours per vehicle assembly, in

2004 was 27.9 hours for Toyota, 37 for Ford, and 35.9 for Chrysler LLC; and

while Ford, GM, and Chrysler improved productivity prior to 2004, Toyota’s

productivity increased at a faster rate. In contrast, the productivity gap has

decreased since 2004, as recent productivity reports show that in 2007

Toyota required 29.9 hours per vehicle (a small increase over 2004) while

the respective productivity numbers at Ford and Chrysler are 35 and 32.3

hours per vehicle, an improvement over 2004.

Source: David Welchand and Ian Rowley, “Toyota’s All-Out Drive to Stay Toyota,”

Business Week (December 2007), pp. 54-56.