Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–46

14–44 Materials Purchase-Price Variance and Foreign Exchange Rates (20-30

minutes)

1. Actual Results

Actual Purchase Standard Price

Quantity Price Total Cost Price Variance

1st Quarter 4,000 $68 $ 272,000 $60 $ 32,000U

2nd Quarter 4,000 69 276,000 60 36,000U

3rd Quarter 4,000 73 292,000 60 52,000U

Further analysis of the 4th Quarter’s materials purchase-price variance:

Price variance due to increase in the negotiated price:

24,000 kg. × ($76 − $60)/kg. = $384,000U

Price variance due to changes in exchange rate:

2. The favorable materials purchase-price variance for the 4th quarter and for

the year is due to fluctuations in foreign currency exchange rates. The firm

gained $864,000 from the favorable changes in currency exchange rates.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–47

14-45 Direct Materials: Joint Price-Quantity Variance (30-45 minutes)

1. Direct materials price variance = AQ × (AP − SP)

= 25,000 tons × ($12 − $10)/ton = $50,000U

2. Standard direct materials allowed for the units manufactured, SQ:

5,000 units × 4.5 tons per unit = 22,500 tons

Direct materials usage variance = SP × (AQ − SQ)

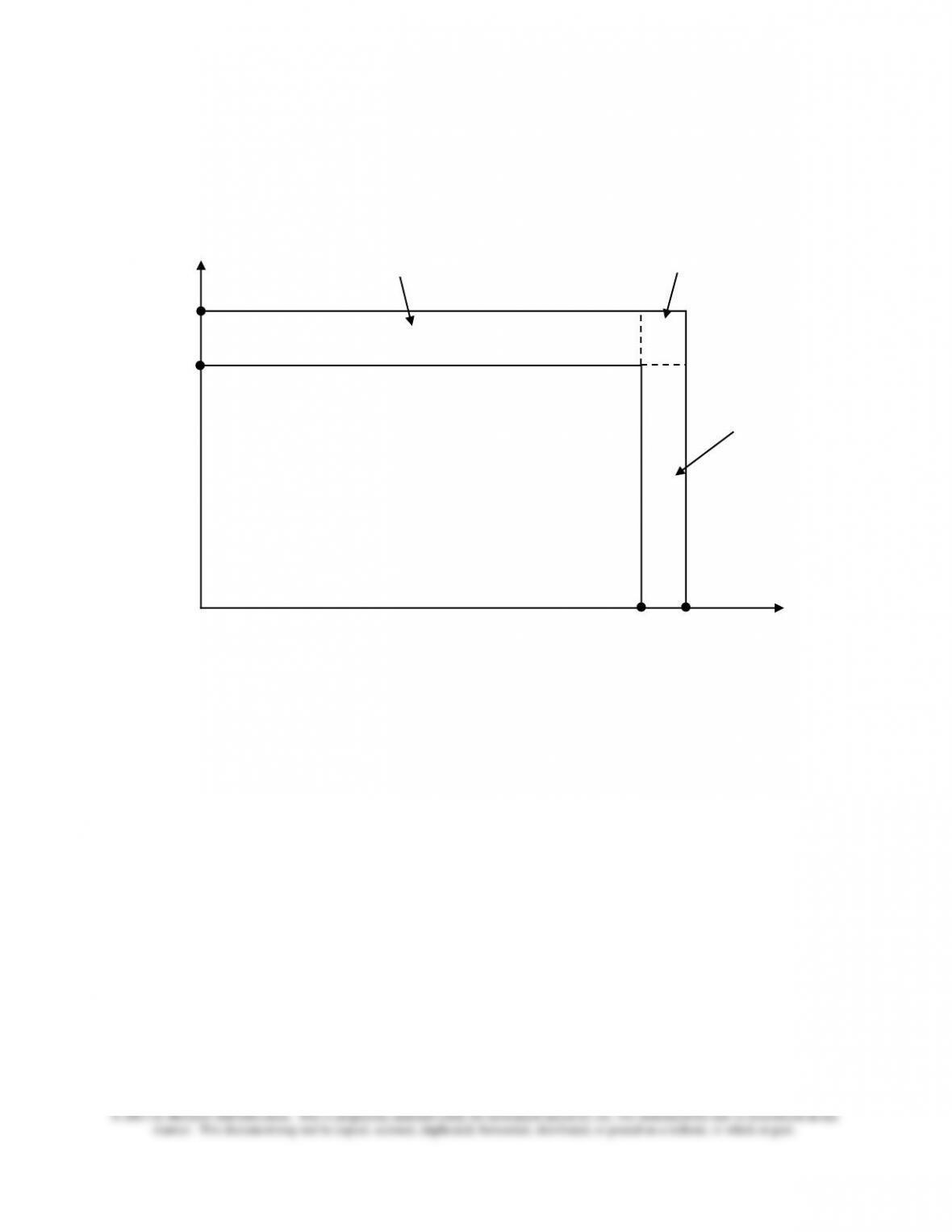

The preceding calculations are illustrated graphically below:

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–48

14–45 (continued)

Legend:

AP = actual price per ton of raw material

SP = standard price per ton of raw material

AQ = actual tons of raw material used in production

SQ = standard # of tons allowed for the output achieved

SQ × (AP − SP) = “pure” price variance

SP × (AQ − SP) = “pure” quantity variance

(AP − SP) × (AQ − SQ) = “joint” price-quantity variance

Note that in practice the joint price-quantity variance is usually included as part of the

price variance under the assumption that price paid is less controllable than quantity

consumed in the production process. That is, there is a desire to keep the efficiency

variance as “pure” as possible.

Q

P

SP

AP

SQ

AQ

[( [(AP − SP) × (AQ − SQ)]

SQ x (AP – SP)

SP × (AQ − SQ)

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–49

14–46 Standard Cost Sheet and Use of Variance Data (45-50 minutes)

1. Standard cost for each ten-gallon batch of raspberry sherbet:

(a) (b)

Standard Standard

Quantity Rate

Direct materials:

Raspberries (7.5 qts.* × $4.00) = $30.00

Other ingredients (10 gal. × $2.25) = 22.50 $52.50

Direct labor:

Sorting (3 min. × 6 qts.)/60 × $15.00 = 4.50

**4 quarts per gallon × 10 gallons = 40 quarts.

2. a. In general, the purchasing manager is held responsible for unfavorable

materials purchase price variances. Causes of these variances include

the following:

▪ Failure to correctly forecast price increases.

▪ Purchasing nonstandard materials or in uneconomical lots.

In some situations, however, someone other than the purchasing manager

may be responsible for the price variance. For example, an expedited

shipment of materials, with associated higher shipping cost, could be the

result of a rush order accepted by the sales department and as such not

assigned to the purchasing manager.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–50

14–46 (Continued)

As a small producer, ColdKing’s competitive strategy is likely to be

differentiation through brand recognition, just as the firm has apparently

been doing. The success of the competitive strategy requires that the firm

maintains high quality and good cost control. Unfavorable price variances

decrease the profit of the firm and, unless corrected in the short run, may

compromise the firm’s competitive position and the survival of the firm in the

long-run.

b. In general, the production manager or foreman is held responsible for

unfavorable labor efficiency variances. Causes of these variances include

the following:

▪ Poorly trained labor

▪ Substandard, inefficient, or improperly set equipment

Note: One issue to raise with students at this point is the danger of too

much focus on the labor-efficiency variance. For example, in many cases

today, labor is a short-term fixed cost. Thus, a principal cause of an

unfavorable labor efficiency variance is lack of sales orders/production

demand, not worker efficiency! The only way a manager in this situation can

avoid an unfavorable labor efficiency variance is to produce excess

inventory, which would be counter to the JIT philosophy that many

organizations are pursuing today. The moral here is that when the

workforce is basically fixed in the short run, labor efficiency variances have

to be interpreted with caution. For this reason, some writers have advocated

doing away with the reporting of labor efficiency variances for control

purposes when the labor force is essentially fixed in the short run.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–51

14–47 Standard Cost Systems—Behavioral Considerations (45-

50minutes)

1. a. The major advantages of using a standard cost system include:

▪ Budgeting. Standard costs can be the building blocks for budget

preparation and allow the development of flexible-budgets.

costs and facilities inventory control (i.e., items need be

maintained in physical quantities only).

b. The disadvantages/challenges that can result from using a standard

cost system include the following:

▪ Cost standards that are too tight can cause the employees to

ignore the standards, or worse, have negative behavioral

implications leading to undesirable actions.

▪ Focus on cost-drivers. As a corollary to the above comment, many

strategic cost management systems today are focusing on the

identification of the factors that drive production costs (e.g., batch–

level and customer-level costs).

2. A standard cost system must be supported by top management to be

successful. However, the parties that should participate in the standard-

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–52

3. The general features and characteristics associated with the introduction

and operation of a standard cost system that make it an effective tool for

cost control include the following.

▪ Standard-setting can be a participative process with those individuals

most familiar with the variables associated with standard-setting

available to provide the most accurate information. This sense of

and performance reports, similar to those discussed in Chapters 14,

15, and 16.

4. The consequences of having the standards set by an outside consulting

firm are the following:

▪ There could be negative employee reaction as the employees did not

this could result in poor management decisions based on faulty

information.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–53

14–48 Standard Cost in Process Costing; Variances, and Journal Entries (45–60

minutes)

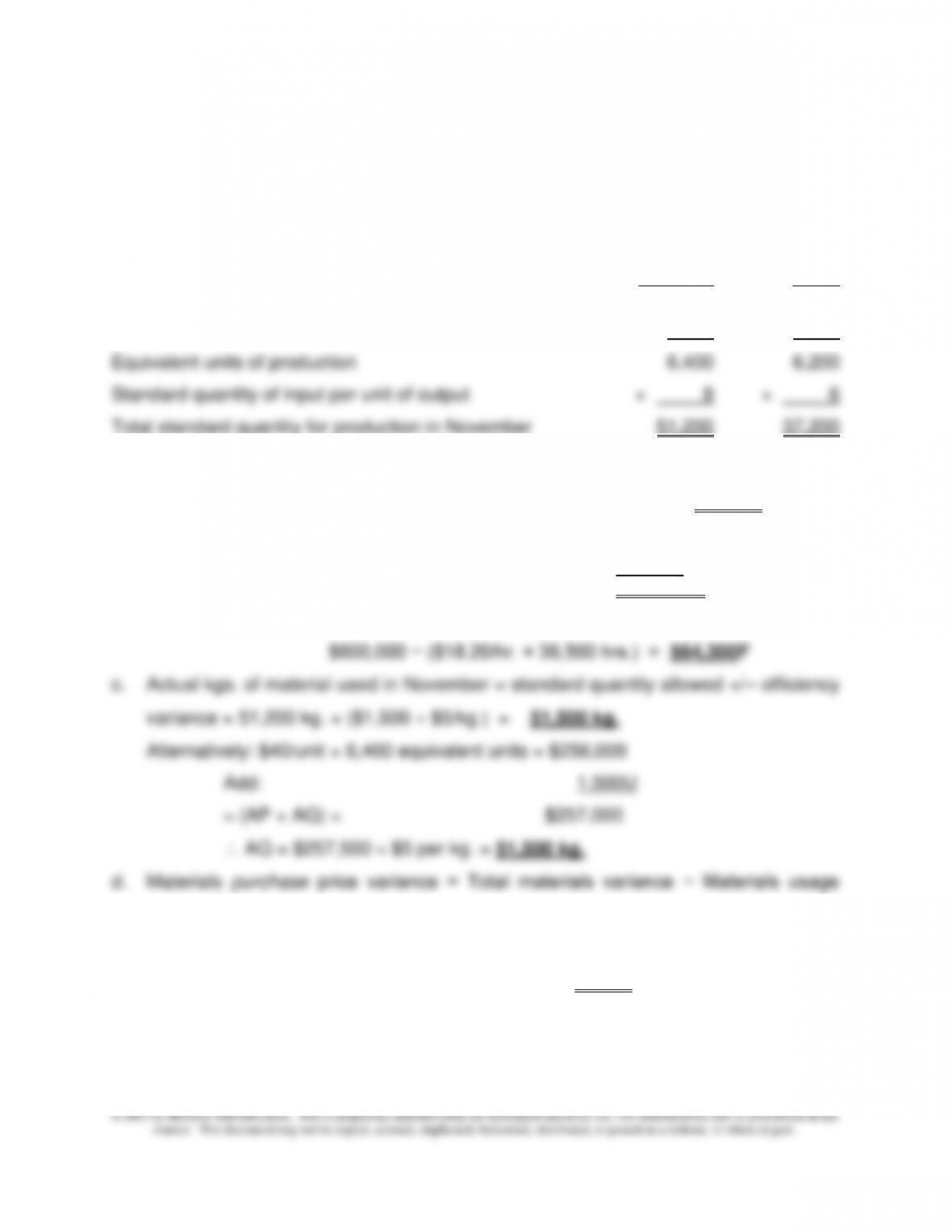

1. Equivalent units of production in November:

Direct Direct

Materials Labor

Units completed 5,600 5,600

Equivalent units in ending WIP inventory + 800 + 600

a. Direct labor efficiency variance = SP × (AQ − SQ)

= $18.20/hr. × (36,500 − 37,200) hrs. = $12,740F

Alternatively: $109.20/unit × 6,200 Equivalent Units = $677,040

Less: $18.20/hour × 36,500 hours = 664,300

$ 12,740F

b. Direct labor rate variance = (AP × AQ) − (SP × AQ)

variance = $750U − $1,500U = $750F

Actual price per kilogram (AP) = Standard price per kg. (SP) – Per-unit favorable

price variance = $5.00/kg. − ($750 50,000 kgs.) = $4.985 (note: this answer

assumes that the price variance for DM is calculated at point of purchase)

e. Total amount of prime costs transferred to the finished goods account in November

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–54

= Standard manufacturing cost/unit × #units manufactured in November = ($40.00 +

$109.20) × 5,600 units = $835,520

14–48 (Continued)

f. Materials Labor Total

Equivalent units in ending WIP inventory 800 600

2. Materials Inventory ($5 × 50,000 kg.) $250,000

Materials Purchase-Price Variance (see (d) above) $750

Accounts Payable (plug) $249,250

Purchase of 50,000 kilograms of materials for $249,250 ($4.985/kg.)

Work-in-Process Inventory (6,400 eq. units × $40) $256,000

Accrued Payroll (given) $600,000

Direct labor wages incurred to manufacture 6,200 equivalent units; actual

wage rate = $16.438/hr.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–55

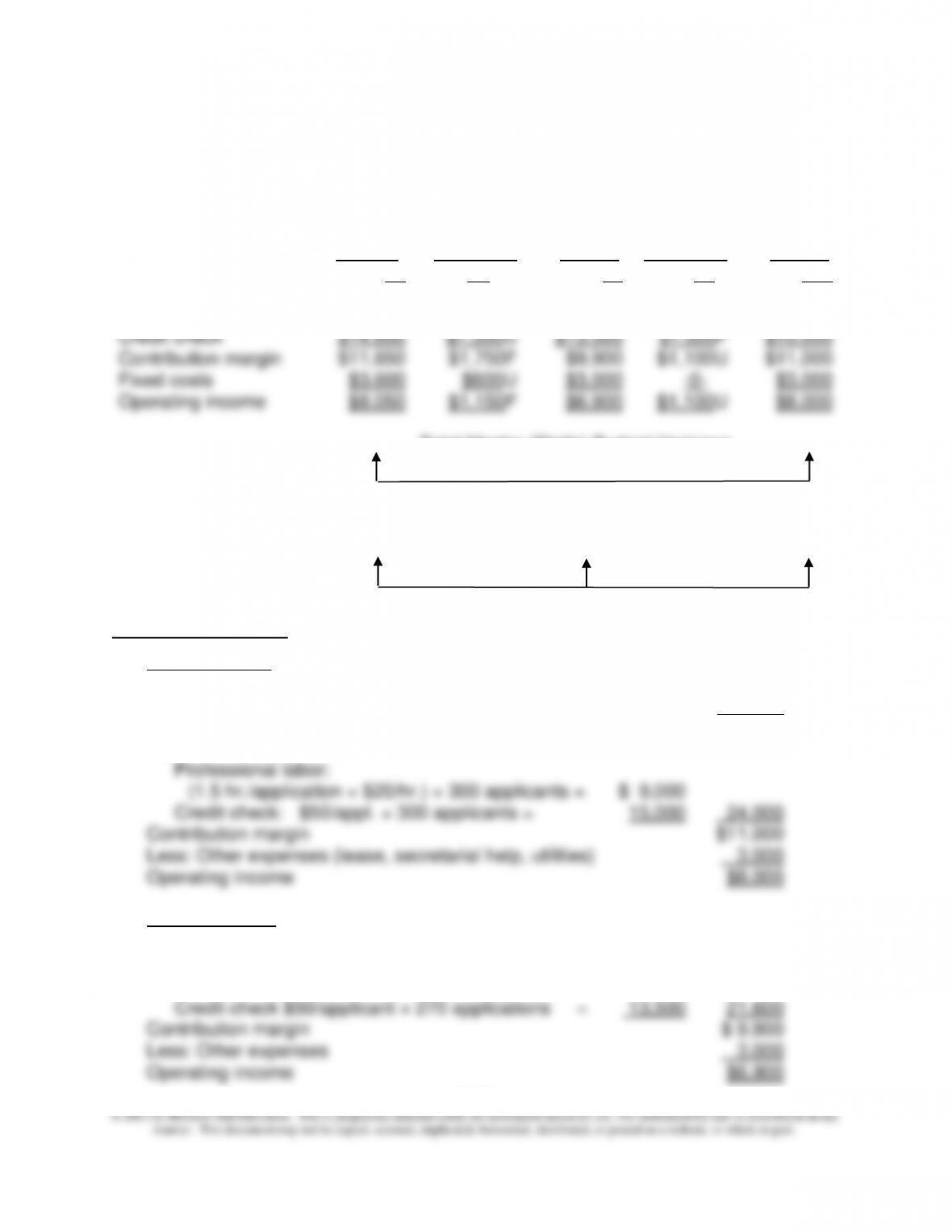

14-49 Flexible Budget and Operating-Profit Variances (60 minutes)

1. Flexible- Sales Master

Actual Budget Flexible Volume (Static)

Results Variances Budget Variances Budget

Units sold 90 -0- 90 10U 100

Revenues $36,000 $4,500F $31,500 $3,500U $35,000

Professional labor $9,500 $1,400U $8,100 $900F $9,000

Total Master (Static) Budget Variance

$50F

Flexible-Budget Sales Volume

Variance Variance

$1,150F $1,100U

Detailed Calculations:

Master budget:

Number of apartments rented 100

Revenue per apartment rented $700 2 = $ 350

Total revenue $35,000

Less: Variable costs:

Flexible Budget

Total revenue 90 rentals × $350/rental = $31,500

Less: Variable costs:

Professional labor (1.5 × $20) × 270 applications = $ 8,100

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–56

14–49 (continued)

Operating Income:

Total revenue 90 rentals × $800/rental × 0.5 = $36,000

Less: Variable costs:

Professional labor $ 9,500

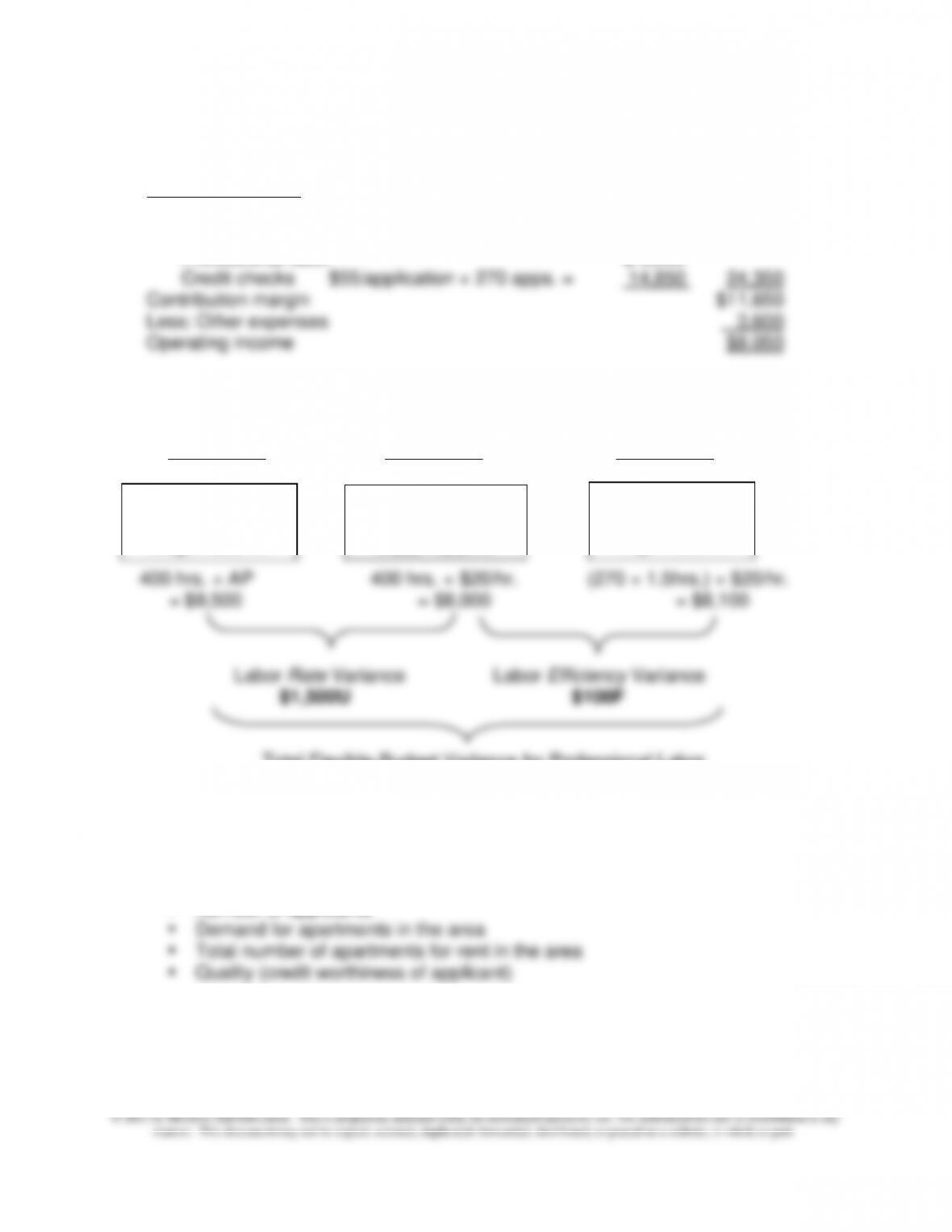

2.

Actual Quantity Flexible Budget (FB)

Actual Labor Cost at Standard Price Based on Outputs

(AQ) × (AP) (AQ) × (SP) (SQ) × (SP)

Total Flexible-Budget Variance for Professional Labor

$1,400U

3. Among factors to be considered in evaluating the effectiveness of professional labor

are:

▪ Number of units successfully rented

▪ Number of applicants

Actual Hrs.

Worked × Actual

Wage Rate/Hr.

Actual Hrs.

Worked × Std.

Wage Rate/Hr.

Std. Hrs.

Allowed × Std.

Wage Rate/Hr.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–57

14–50 Standard Costing, Variance Analysis, and Strategic Considerations (60

Minutes)

1. The term “engineered labor standards” refers to the use of engineering (i.e., input–

output) analysis regarding labor-hour consumption associated with the production of a

good or a service. This method of establishing the quantity component of labor-hour

standard costs can be contrasted to the use of historical observations as the basis for

Typically, these times were “engineered” in the sense that they reflected highly

efficient effort on the part of employees.

2. An organization, for any given operating period, can determine for each class of labor

the difference between the actual labor cost incurred (given the output of the period)

and the standard labor cost for that period (based on the actual output). This latter

amount should be viewed as “the labor cost that should have been incurred, given

actual output for the period just ended.” This difference, in dollar terms, is referred to

for activities performed by their employees (such as check-out clerks). In short, the

article focuses on the application of “work–measurement” techniques in a retailer

environment. Of particular interest is the fact that these techniques were developed,

many years ago, in a manufacturing environment.

3. As noted above in (2), the process of using time-and-motion studies to establish

standards for labor-hour consumption was developed and refined (many years ago!)

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–58

14–50 (Continued-1)

The key question, therefore, is whether in a retail environment worker activities are

sufficiently repetitive to allow for the development of labor-consumption standards

(expressed in minutes or portions thereof). As noted in the article, one possible

solution is to develop more refined standards—which would be able to capture the

unique (i.e., non-repetitive) nature of certain events and activities performed by retail

clerks.

4. As with any new employee monitoring/performance-evaluation system, behavioral

considerations are important for the implementation success of the new system. In

the present case, one might anticipate the following employee and customer-service

problems associated with the newly implemented system:

• employees manipulate the system (see the quote near the end of the article)

• customers are “processed efficiently,” but at the expense of poor or

inconsiderate service

As indicated in the article, there are several steps that a retailer can take to improve the

success of the new system (by minimizing problems associated with the system):

• education—employees, through various types of education programs, need to

understand why the new system is needed (i.e., what business problem is

the standards that will be used to evaluate their performance

• balanced scorecard type system: the new labor-efficiency system might be

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–59

14–50 (Continued-2)

implemented in conjunction with the use of other key performance measures,

such as customer satisfaction, increases in market share, etc.

5. It would seem as if retailers competing on the basis of cost (low-cost strategy) rather

than a differentiation strategy would benefit most by the type of system discussed in

the article. The information from the new monitoring system can be used to improve

Below is a reproduction of the original article.

______________________________________________________________________

WSJ, November 13, 2008 (pp. A1, A15) By VANESSA O’CONNELL

SHELBY TOWNSHIP, Mich.—Daniel A. Gunther has good reason to keep his checkout

line moving at the Meijer Inc. store north of Detroit. A clock starts ticking the instant he

scans a customer’s first item, and it doesn’t shut off until his register spits out a receipt.

To assess his efficiency, the store’s computer takes into account everything from the

kinds of merchandise he’s bagging to how his customers are paying. Each week, he

gets scored. If he falls below 95% of the baseline score too many times, the 185-store

megastore chain, based in Walker, Mich., is likely to bounce him to a lower-paying job,

or fire him.

American retailers have come under tremendous financial pressure as beleaguered

consumers curtail their spending. At least 14 major chains have sought bankruptcy

protection over the past 12 months, and many others are struggling. With nearly all of

them under the gun to cut costs and improve profit margins, “labor–waste elimination”

systems like the one used by Meijer are sweeping the industry.

Daniel Gunther, who works at a Meijer megastore north of Detroit, says he has been

told ‘get people in and out’ of the checkout line to improve efficiency.

14–60

14-50 (Continued-3)

The brains behind Meijer’s system is a consulting and software company known for

decades as H.B. Maynard & Co., which last year became the Operations Workforce

Optimization unit of Accenture Ltd. Borrowing from time-motion concepts first developed

for U.S. steel mills and factory floors, it breaks down tasks such as working a cash

register into quantifiable units and devises standard times to complete them, called

“engineered labor standards.” Then it writes software to help clients keep watch over

their work forces.

The client list of OWO, as it is now known, has included more than five dozen retail

chains, including Gap Inc., TJX Cos., Limited Brands Inc., Office Depot Inc., Nike Inc.,

and Toys “R” Us Inc. A host of other “work force management” companies also offer to

help retailers improve worker productivity.

Interviews with cashiers at 16 Meijer stores suggest that its system has spurred many to

get out right away,” says Barb Bush, who shops at Meijer stores in DeWitt and Owosso

and says she likes the current system. “A lot of [the cashiers] like to stop and chat, and I

don’t really have the time for it.”

Linda Long, 58, who shops at the Okemos store weekly, says of the cashiers:

“Everybody is under stress. They are not as friendly. I know elderly people have a hard

time making change because you lose your ability to feel. They’re so rushed at checkout

that they don’t want to come here.”