Chapter 12 – Strategy and the Analysis of Capital Investments

12–46

12-46 (Continued)

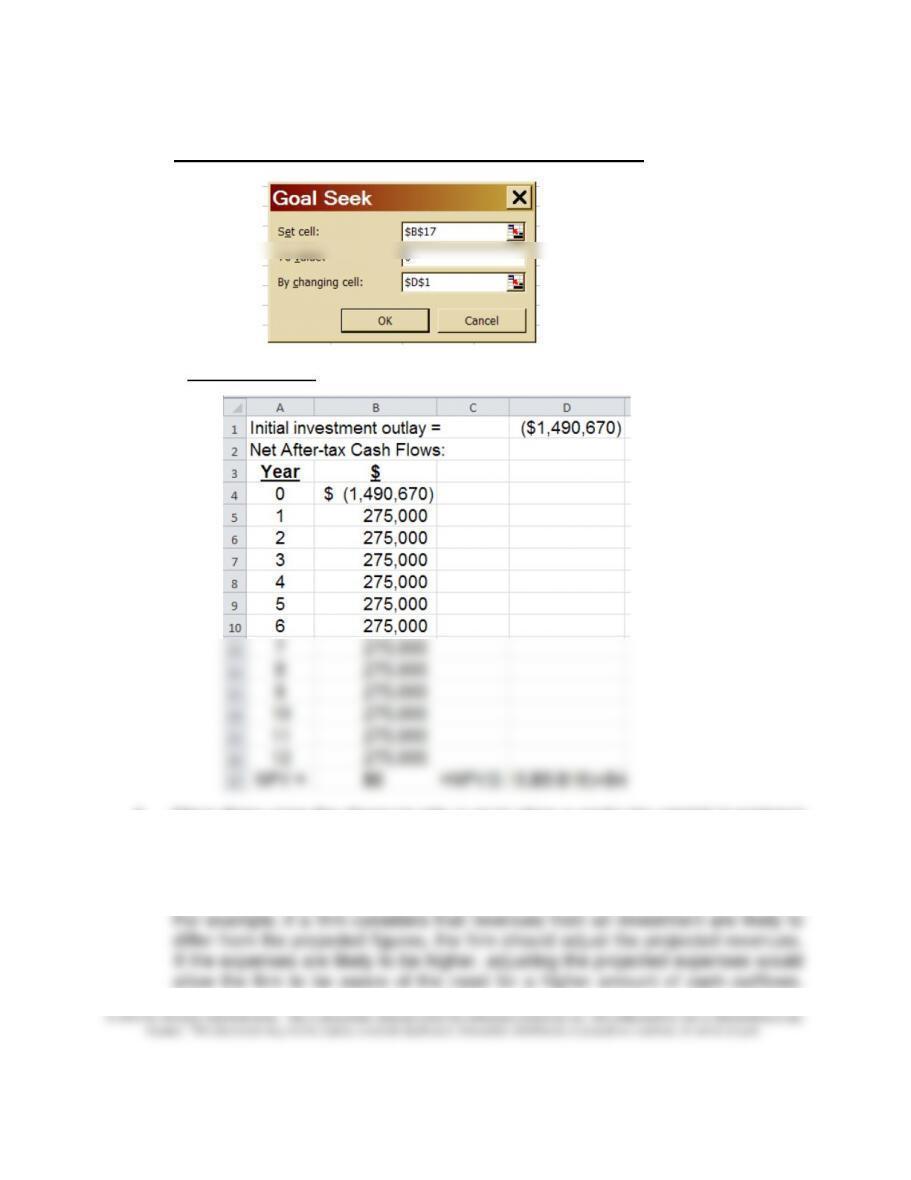

Step 2: Complete the following “Goal Seek” dialog box:

Step 3: Results

4. Many firms raise the discount rate in evaluating a particular capital investment

in view of uncertainties underlying the investment. This approach allows

managers to factor in risks and uncertainties. The higher the risk or uncertainty

a project has, the higher the discount rate.

An alternative is to use a direct approach in dealing with risk or uncertainty.

Chapter 12 – Strategy and the Analysis of Capital Investments

12–47

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

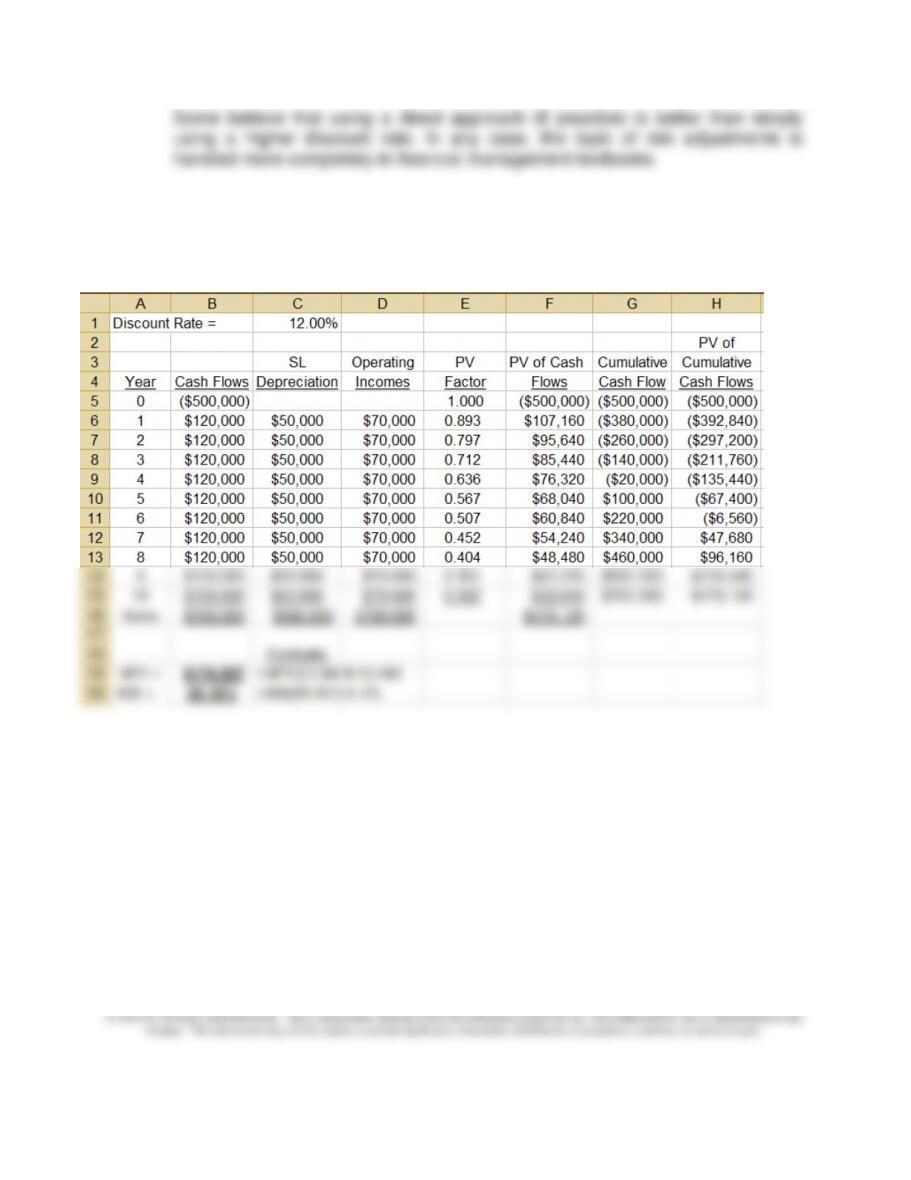

Some believe that using a direct approach (if possible) is better than simply

using a higher discount rate. In any case, the topic of risk adjustments is

handled more completely in financial management textbooks.

PROBLEMS

12–47 Basic Capital-Budgeting Techniques; No Taxes; Uniform Net Cash Inflows;

Spreadsheets (45-60 minutes)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–48

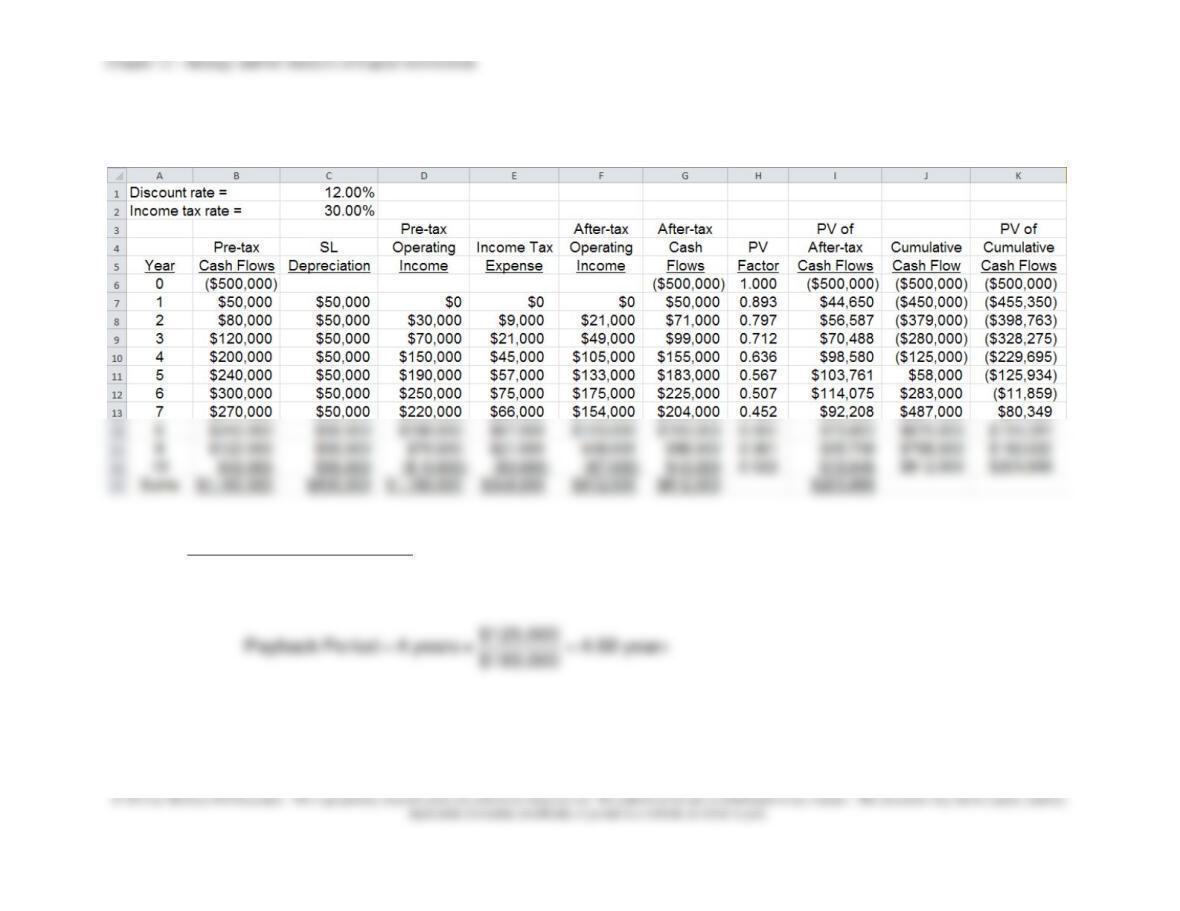

1. Unadjusted Payback Period: As shown above, the payback period occurs

2. Book (accounting) rate of return (ARR):

As indicated above, the average increase in net income over the ten-year period

= $700,000 ÷ 10 years = $70,000 ÷ year. Thus, the ARR

(a) On initial investment: $70,000 ÷ $500,000 = 14.00%

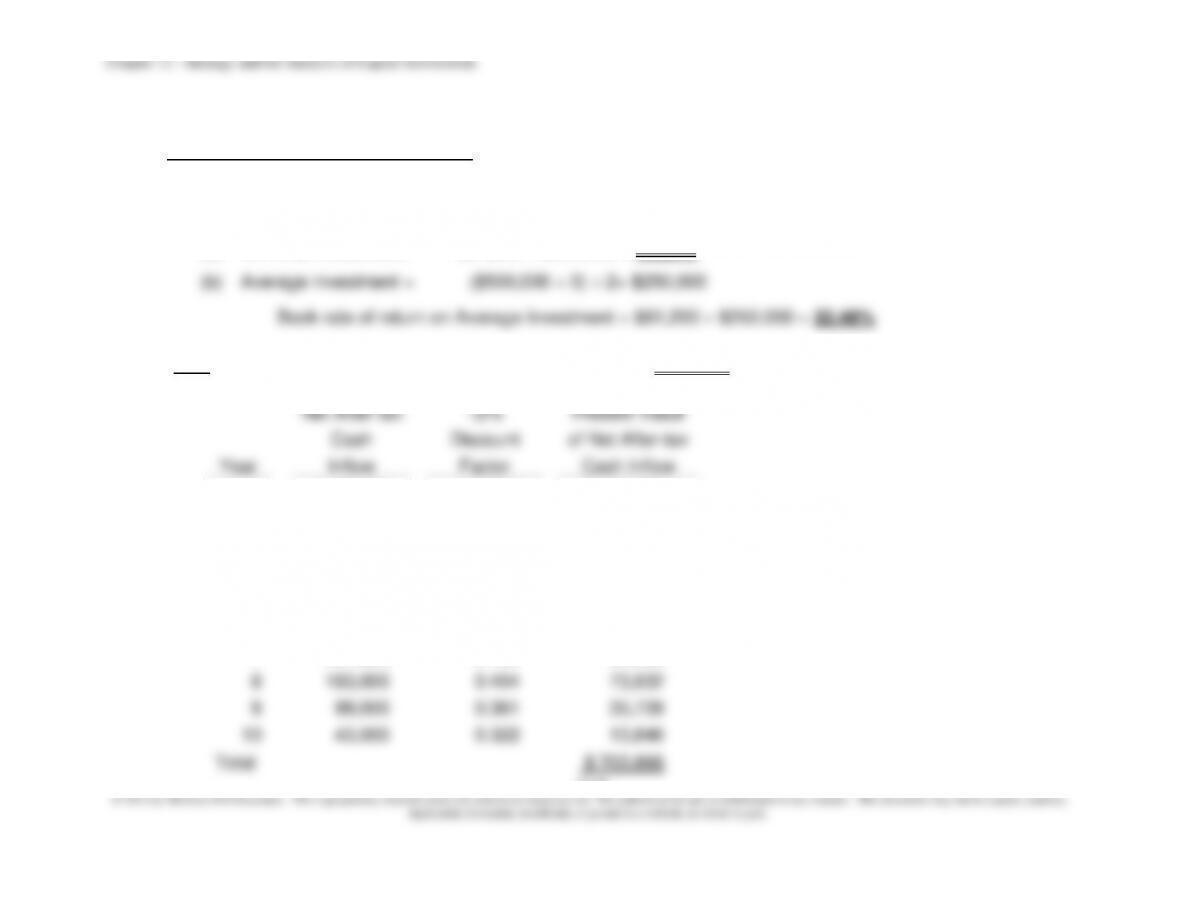

(b) On average investment:

3. NPV: using the PV factors from Appendix C, Table 2, NPV =$178,120

Based on the NPV function of Excel, the NPV = $178,027(the difference in NPV

estimates is due to rounding that takes place when using the PV factors

provided in the Table 2 rather than the built-in NPV function)

4. Present value payback period: as indicated in the above schedule, the present

value payback period is “6–plus” years; this is the time it takes for the present

value of future cash inflows to cover the original investment outlay of $500,000.

If we assume that the cash inflows occur evenly throughout the year, then the

payback period for the proposed investment is:

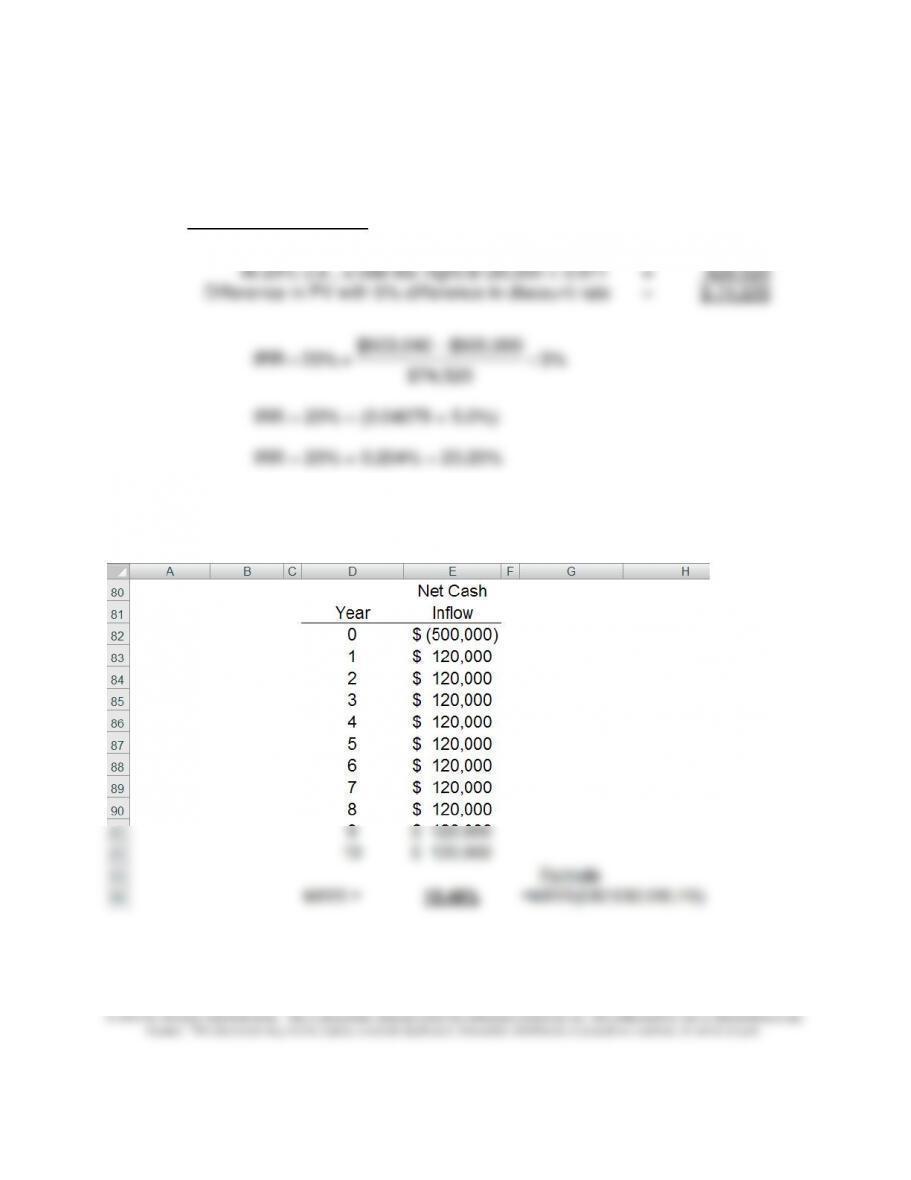

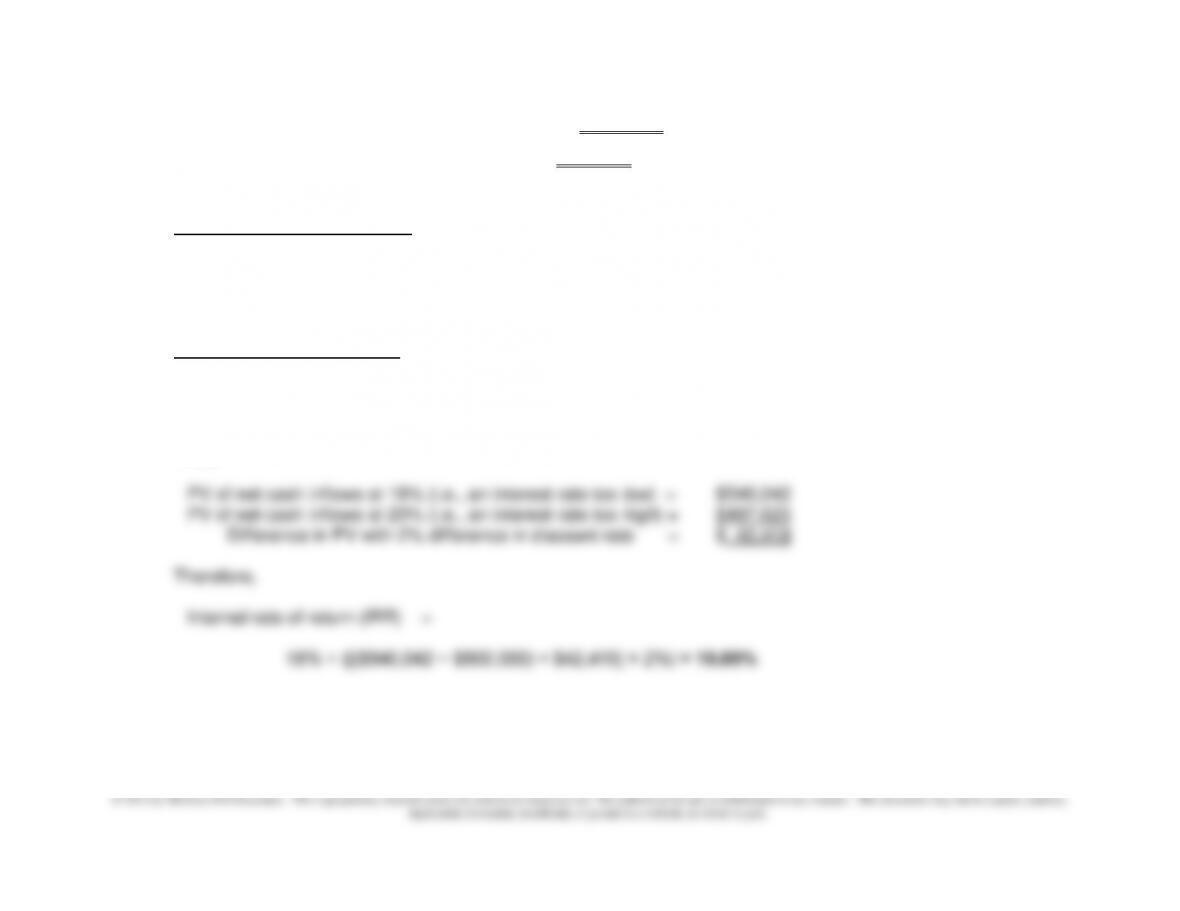

5. Internal rate of return: as indicated in the above schedule, we can use the built–

in function in Excel to estimate the IRR for this proposed investment; IRR =

Chapter 12 – Strategy and the Analysis of Capital Investments

Alternatively, we can estimate the IRR as follows. We are looking for an

interest/discount rate that provides for a NPV = $0 (i.e., a rate that provides a

present value of future cash inflows equal in amount to the original investment

outlay, $500,000). Thus,

PV of net cash inflows:

At 20% (i.e., a rate too low): $120,000 × 4.192 = $503,040

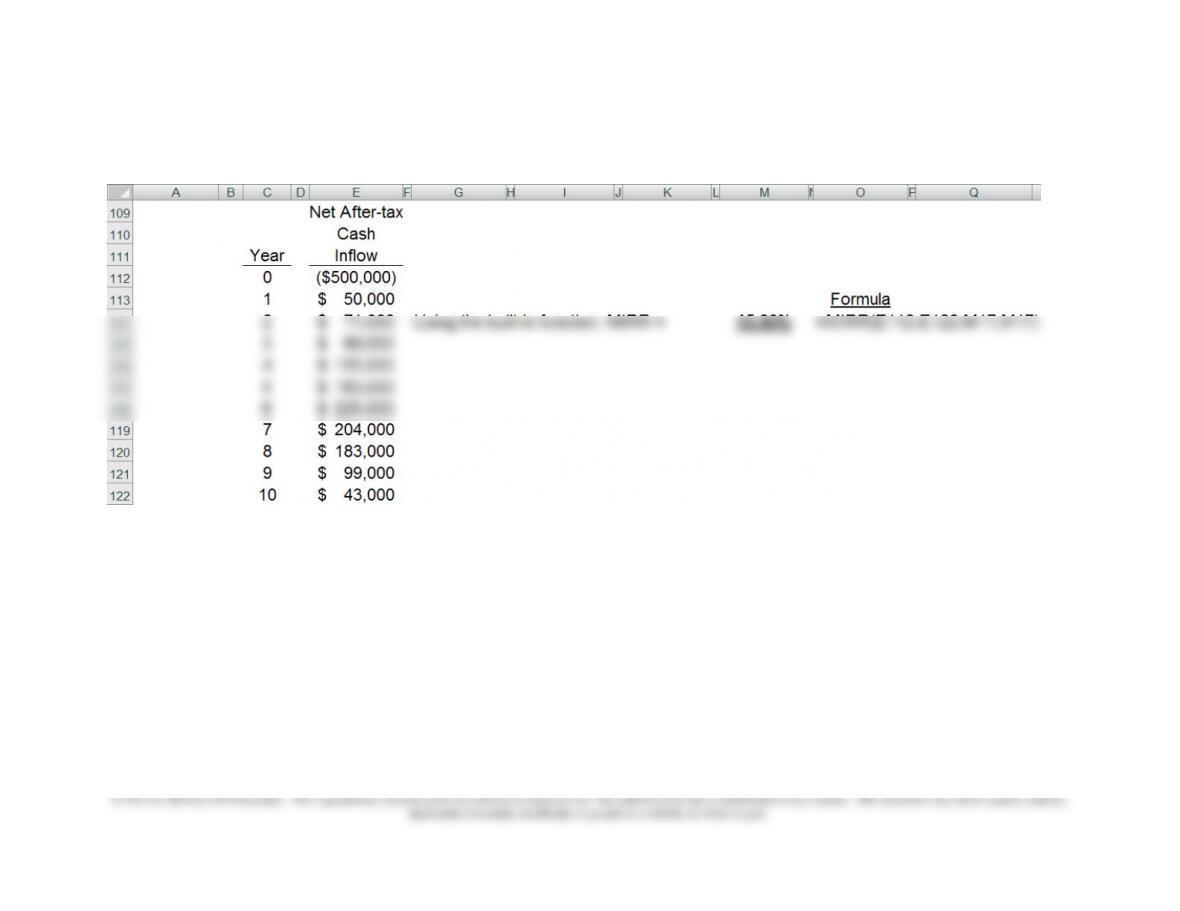

6. Modified internal rate of return (MIRR)—see next page:

12–48 Basic Capital-Budgeting Techniques; Uneven Net Cash Inflows with Taxes and MACRS; Spreadsheet

Application (60-75 minutes)

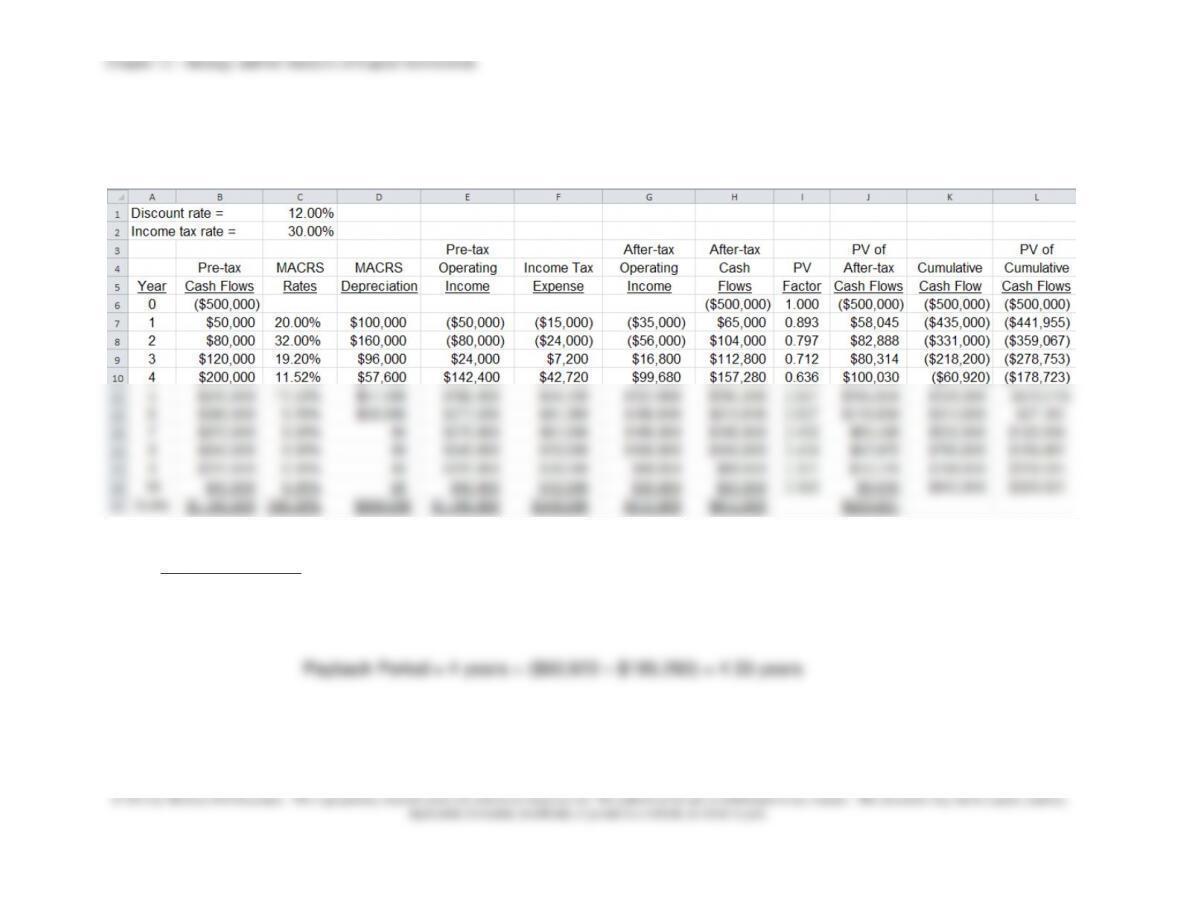

1. Unadjusted Payback Period: as shown by the above schedule, the payback period is between 4 and 5 years.

Under the assumption that the cash inflows occur evenly throughout the year, and using a linear interpolation,

we estimate the payback period as:

12–51

12–48 (Continued-1)

2. Book (accounting) rate of return (ARR):

As indicated above, the average increase in after-tax operating income over the ten-year period = $812,000 ÷ 10

years = $81,200/year. Thus, the ARR

(a) On initial investment: $81,200 ÷ $500,000 = 16.24%

3. NPV: using the PV factors from Appendix C, Table 2, NPV = $203,866

Net After-tax

12%

Present Value

Cash

Discount

of Net After-tax

Year

Inflow

Factor

Cash Inflow

1

$ 50,000

0.893

$ 44,650

2

71,000

0.797

56,587

3

99,000

0.712

70,488

4

155,000

0.636

98,580

5

183,000

0.567

103,761

6

225,000

0.507

114,075

7

204,000

0.452

92,208

8

183,000

0.404

73,932

9

99,000

0.361

35,739

10

43,000

0.322

13,846

Total

$ 703,866

Chapter 12 – Strategy and the Analysis of Capital Investments

12–52

12–48 (Continued-2)

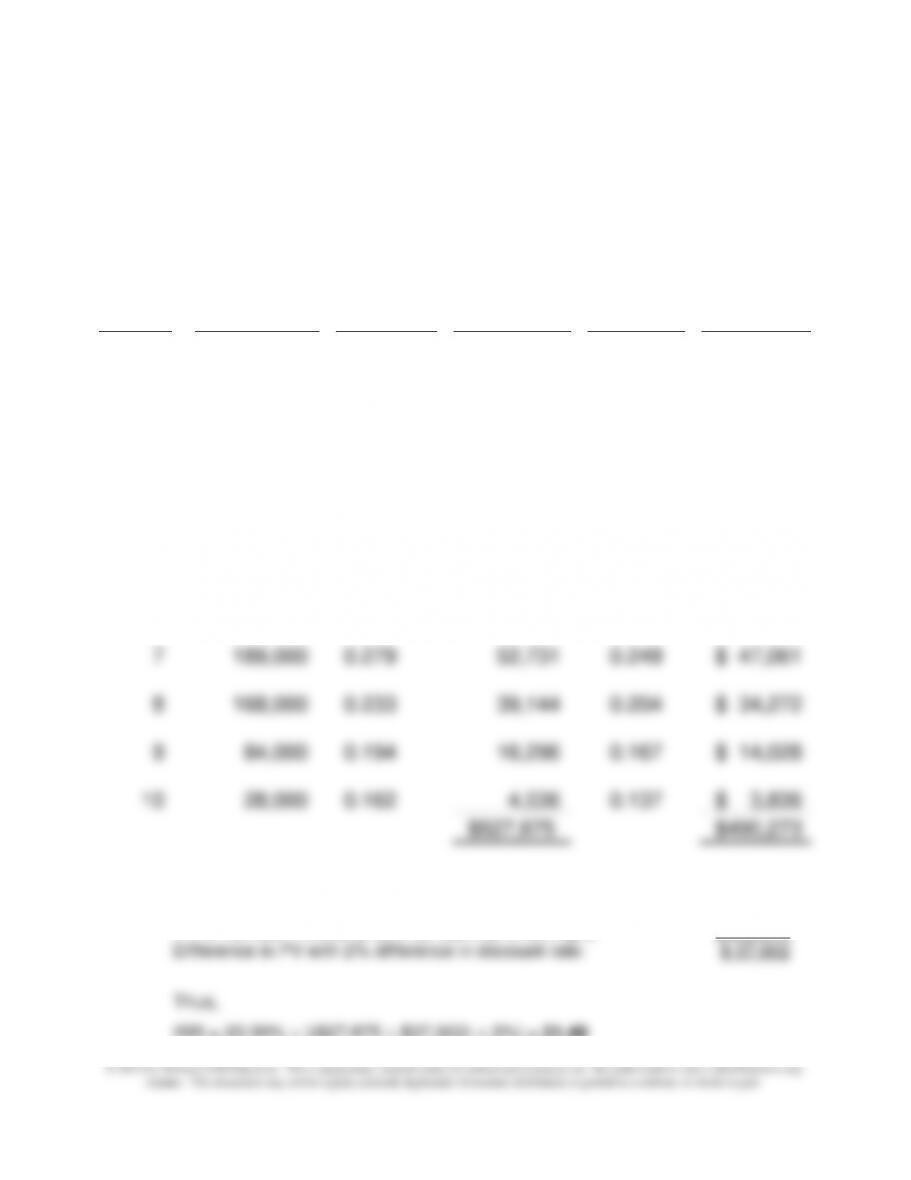

Based on the NPV function of Excel, the NPV = $203,781(the difference in NPV estimates is due to rounding that

takes place when using the PV factors provided in the Table 2 rather than the built-in NPV function).

4. Present value payback period: as indicated in the above schedule, the present value payback period is “6–plus”

(6.1286) years; this is the time it takes for the present value of future cash inflows to cover the original investment

outlay of $500,000. If a finer estimate is needed, and under the assumption that cash inflows occur evenly

throughout the year, a linear interpolation procedure can be used.

5. Internal rate of return (IRR): as indicated in the above schedule, we can use the built-in function in Excel to

estimate the IRR for this proposed investment; thus, IRR = 19.88%

Alternatively, we can estimate the IRR as follows. We are looking for an interest/discount rate that produces a

NPV = $0 (i.e., a present value of cash inflows equal in amount to the original investment outlay, $500,000).

Thus,

NPV =

$ 203,866

Chapter 12 – Strategy and the Analysis of Capital Investments

12–53

12–48 (Continued-3)

6. Modified internal rate of return (MIRR):

12–54

12–49 Basic Capital-Budgeting Techniques, Uneven Net Cash Inflows, with Taxes and MACRS; Spreadsheet

Application (45-60 minutes)

1. Payback period: as shown by the above schedule, the payback period is between 4 and 5 years. Under the

assumption that the cash inflows occur evenly throughout the year, and using a linear interpolation, we estimate

the payback period as

Chapter 12 – Strategy and the Analysis of Capital Investments

12–55

12–49 (Continued-1)

2. Book rate of return (ARR):

Average after-tax operating income/year: $812,000 ÷ 10 = $81,200

Book (accounting) rate of return (ARR):

a. On initial investment: $81,200 ÷ $500,000 = 16.24%

b. On average investment:

Computation of Simple Average Annual Investment:

Average investment: $1,149,200/10 = $114,920

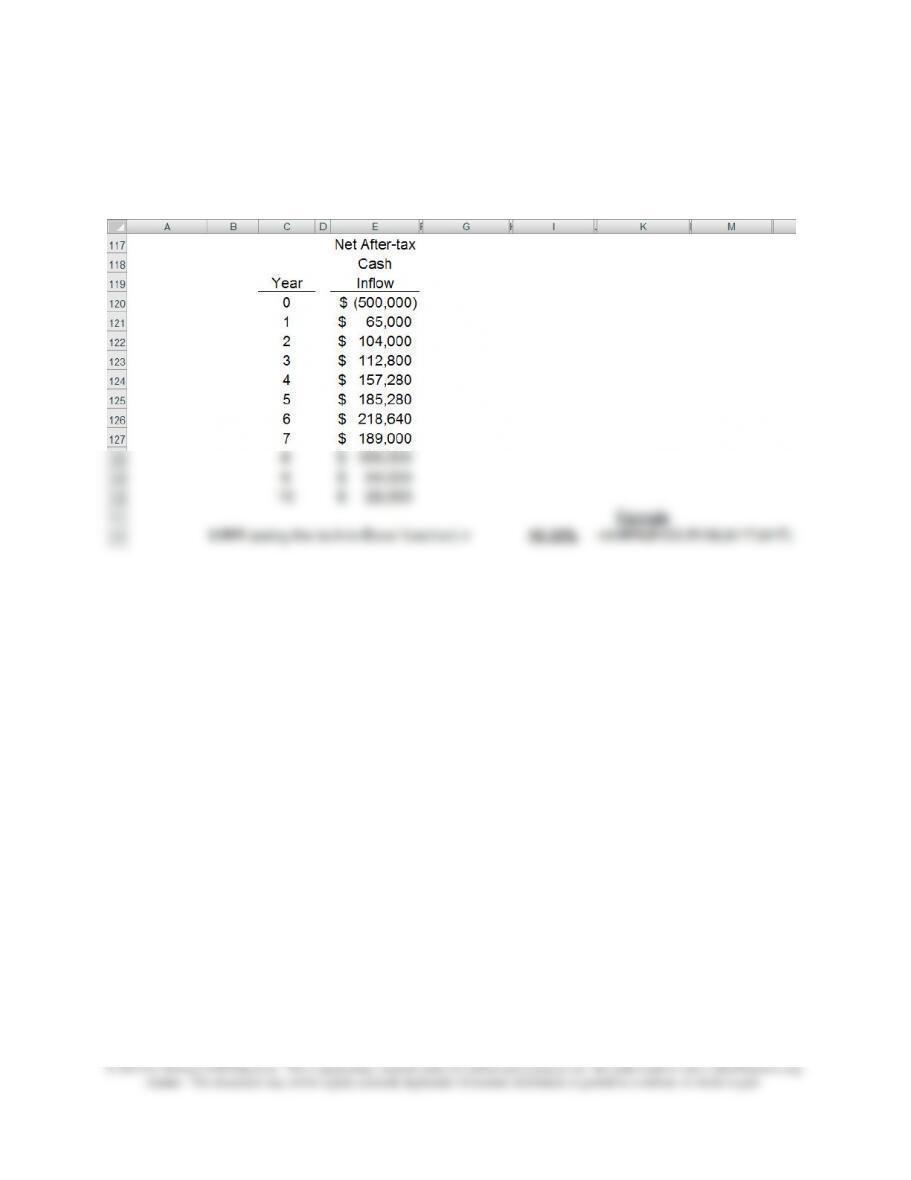

3. Net Present Value (NPV): the NPV of the proposed investment is $229,821 (based

on PV factors from Appendix C, Table 1), as follows:

Year

Book Value,

Beginning-of–

Year

Depreciation

Expense for

the Year

Book Value,

End-of-Year

Average BV

During the

Year

1

$500,000

$100,000

$400,000

$450,000

2

400,000

160,000

240,000

320,000

3

240,000

96,000

144,000

192,000

4

144,000

57,600

86,400

115,200

5

86,400

57,600

28,800

57,600

6

28,800

28,800

0

14,400

7

0

0

0

8

0

0

0

9

0

0

0

10

0

0

0

Totals

$500,000

$1,149,200

Chapter 12 – Strategy and the Analysis of Capital Investments

12–56

12–49 (Continued-2)

Net After-

tax

12%

Present

Value

Cash

Discount

of Net

Year

Inflow

Factor

Cash Inflow

1

$ 65,000

0.893

$ 58,045

2

104,000

0.797

82,888

3

112,800

0.712

80,314

4

157,280

0.636

100,030

5

185,280

0.567

105,054

6

218,640

0.507

110,850

7

189,000

0.452

85,428

8

168,000

0.404

67,872

9

84,000

0.361

30,324

10

28,000

0.322

9,016

Total

$729,821

NPV =

$229,821

4. Internal Rate of Return (IRR): as indicated in the above schedule, we can use the

built-in function in Excel to estimate the IRR for this proposed investment; IRR =

21.46%.

Chapter 12 – Strategy and the Analysis of Capital Investments

12–57

12–49 (Continued-3)

Thus,

PV

PV

Net After-

20%

of Net

22%

of Net

Year

tax Cash

Inflow

Discount

Factor

Cash

Inflow

Discount

Factor

Cash

Inflow

1

$ 65,000

0.833

$ 54,145

0.820

$ 53,300

2

104,000

0.694

72,176

0.672

$ 69,888

3

112,800

0.579

65,311

0.551

$ 62,153

4

157,280

0.482

75,809

0.451

$ 70,933

5

185,280

0.402

74,483

0.370

$ 68,554

6

218,640

0.335

73,244

0.303

$ 66,248

7

189,000

0.279

52,731

0.249

$ 47,061

8

168,000

0.233

39,144

0.204

$ 34,272

9

84,000

0.194

16,296

0.167

$ 14,028

10

28,000

0.162

4,536

0.137

$ 3,836

$527,875

$490,273

PV of net cash inflows at 20% (a rate that is too low): $527,875

PV of net cash inflows at 22% (a rate that is too high): $490,273

IRR = 20.00% + [($27,875 ÷ $37,602) × 2%] = 21.48

Chapter 12 – Strategy and the Analysis of Capital Investments

12–58

12–49 (Continued-4)

5. Modified internal rate of return (MIRR):

Chapter 12 – Strategy and the Analysis of Capital Investments

12–59

12–50 Real Options (50-60 Minutes)

1. “Real Options” are options embedded in capital investment projects. These options

provide an opportunity for management to dynamically adjust to new information and as

such are analogous to financial options. There are two primary differences between

financial options and real options: (1) the latter involve investments in real assets

(tangible and/or intangible property) while the former relate to financial assets; and (2)

the former are traded on an organized exchange, while the latter are not.

There are, in general, two types of real options: those that provide managerial

flexibility, and those that provide growth options. As noted in the excerpt regarding the

CMA exam, these two general types of options can be further subdivided into the

market demand; these options are also referred to as “wait and see” options)

D. Scale-Back Options (i.e., the ability, through production methods or varying

output, to reduce, but not eliminate, investment in a project)

2. The following two terms are associated with financial options:

A. “Put Option” provides the holder with the ability, but not the requirement, to sell a

given security (e.g., share of stock) at a specified price (called the “exercise price”

or “strike price”) on or before a given date, called the “exercise date”

conceptually similar to “put options” on financial assets.

Chapter 12 – Strategy and the Analysis of Capital Investments

12–60

12–50 (Continued-1)

3. Part a:

Required Investment Outlay, t = 0, $100

Outcome (Demand)

p

Year 1

Year 2

Year 3

NPV of

Outcome

Weighted

NPV

High

0.25

$70

$70

$70

$59.83

$14.96

Medium

0.50

$50

$50

$50

$14.16

$7.08

Low

0.25

$5

$5

$5

($88.58)

($22.15)

1.00

$43.75

$43.75

$43.75

($0.11)

Sample calculations:

1. $59.83 = ([$70 ÷ (1+0.15)1] + [$70 ÷ (1+0.15)2] + [$70 ÷ (1+0.15)3] ) – $100

2. $14.96 = $59.83 × 0.25

3. $43.75 = ($70 × 0.25) + ($50 ×0.50) + ($5 × 0.25)

Part b:

Expected NPV of Project =($108,901) (i.e., ($0.11)*1,000,000, rounded);

Expected NPV of Project =($108,901) (based on PV of stream of $43.75 minus $100)

4. As seen from Part 3 above, the NPV of the project if demand is “low” for each of the

three years would be negative. In Exhibit 12.11, Panel B, this negative amount would be

discounted back from t = 1 to t = 0. As such, at t = 1 (when the level of consumer

project, at t = 1, would be positive.

5. In Panel B of Exhibit 12.11, show for each of the three scenarios the calculation for

present value (at t = 0) of cash inflows (cells H20:H22), present value of cash outflows