Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–46

18-45 Balanced Scorecard (15 min)

Solution for problem 2-43, The Tartan Corporation.

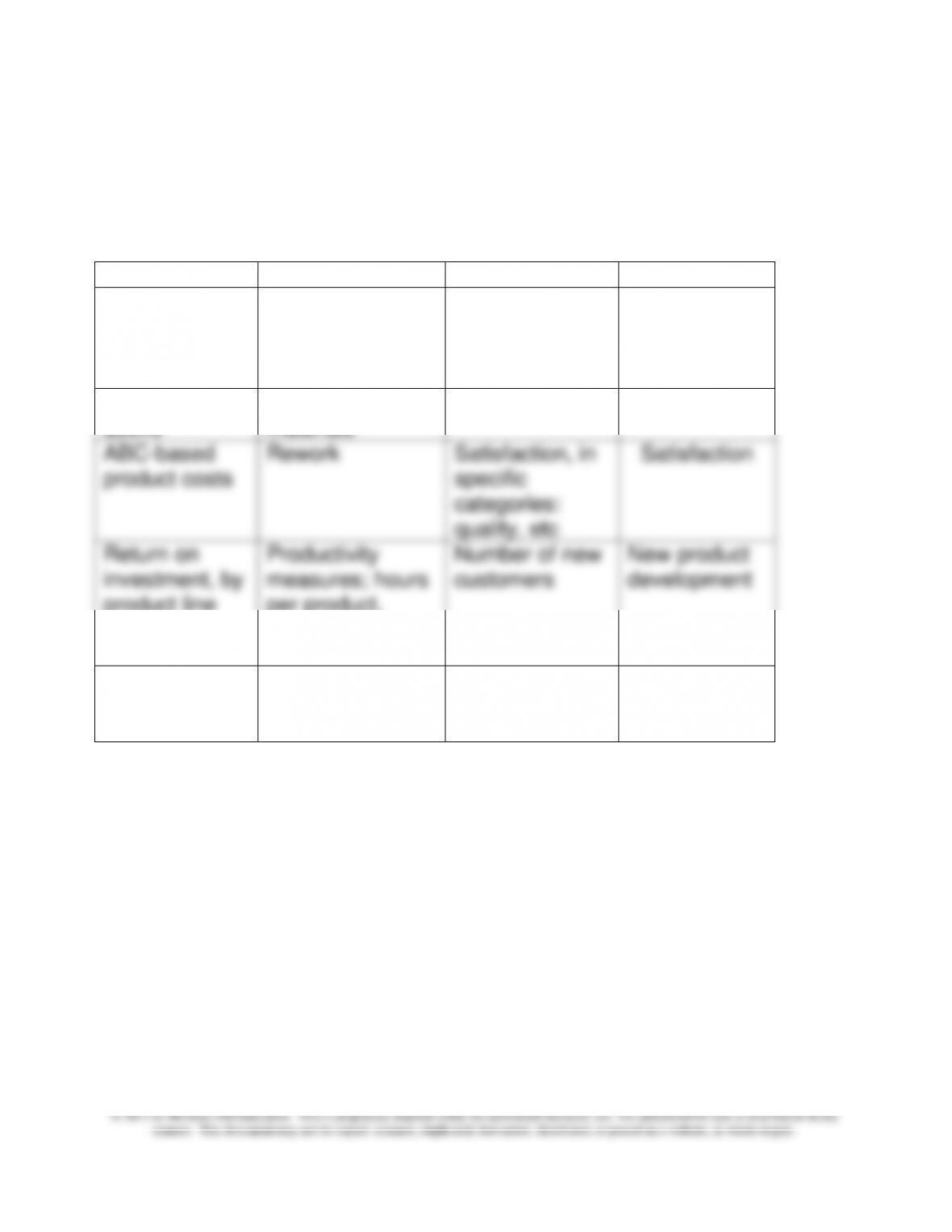

An example of a balanced scorecard for Tartan Corp follows:

Financial

Internal

Customer

Employee

Sales, sales

growth, by

product and

region

Cycle time

Lead time

Training hours

Earnings, as

above

Waste of

materials

Retention

Retention

ABC-based

product costs

Rework

Satisfaction, in

specific

categories:

quality, etc

Satisfaction

Return on

investment, by

product line

Productivity

measures; hours

per product,

materials per

product

Number of new

customers

New product

development

New

investment, by

product line

Inventory levels

Employee

suggestions

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–47

PROBLEMS

18-46 Profit Center Limitations (25 min)

This question is intended primarily for class discussion. The objective

of the question is to have the class understand and discuss some of the

key limitations of the profit center approach for strategic performance

measurement, and to understand some of the methods for addressing

these limitations. The question will work best if the class has some prior

experience in either intermediate accounting, financial statement

analysis, or both. The Merchant and Sandino article is one of many that

have addressed the limitations of profit centers over the years, and it is

one of my favorites. Instructors may have their own favorite in this

regard, and could add their own favorite reading assignment on the topic

as part of the class assignment for this question,

1. Merchant and Sandino (especially in the full article) present a solid

case for moving away from the pure profit center evaluation, and

incorporating one or more of their four suggested approaches for

addressing the problem. Students who have had a solid financial

accounting background including for example, the financial

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–48

18-46 (continued –1)

Other GAAP issues include differences between profit centers in:

a) Judgments of the allowance for bad debts

b) Inventory valuation (FIFO vs LIFO or other method)

g) The effect of judgment in choosing the method for cost allocation

when profit centers share a common resource or service

h) Accounting for leases

The use of a contribution type of income statement as explained in

the chapter can provide an improvement over full cost-based profit

since it incorporates the concepts of traceability and controllability.

If the instructor wishes, this problem provides a good opportunity to

discuss the relationship between GAAP and IFRS and the potential

impact of the convergence of GAAP to IFRS on performance

measurement, particularly of profit centers. As noted in the chapter,

these difference include differences in inventory valuation (no LIFO

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–49

18-46 (continued -2)

2. The proposals fit solidly within the range of proposals made by many

authors in performance management (management control systems),

financial statement analysis, and cost management. In particular the

and urgency to the proposal for a market oriented approach for

performance measurement is the on-going consideration at the SEC

of the convergence of U.S. GAAP and International Financial

Reporting Standards. International reporting standards have a much

stronger focus on market value, allowing under certain conditions for

long-lived assets to be measured at market value, and for research

and development costs to be capitalized, in contrast to the more

conservative cost-based approach for long-lived assets and expense-

based approach to R&D in U.S. GAAP.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–50

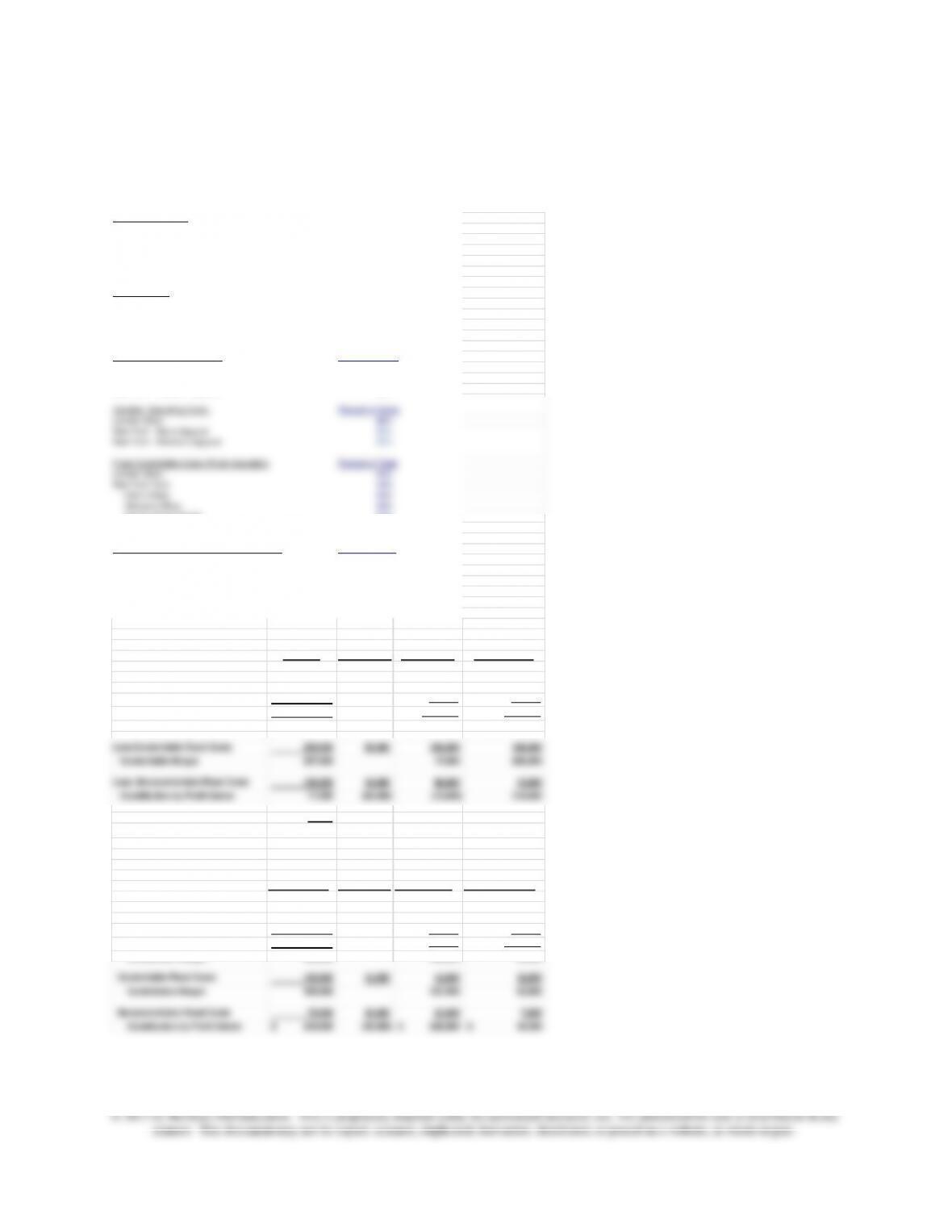

18–47 Contribution Income Statement; Excel Application(25 min)

Data (in thousands)

Total Net Sales 3,250,000$

Fixed Costs

Partly Traceable and Controllable 250,000

Partly Traceable but Noncontrollable 180,000

Nontraceable Costs 65,000

Total Net Sales

London Store 40%

New York Store 60%

New York – Men’s Apparel 40%

New York – Women’s Apparel 60%

Cost of Goods Sold (Variable) Percent of Sales

London Store 55%

New York – Men’s Apparel 40%

New York – Women’s Apparel 60%

Variable Operating Costs Percent of Sales

London Store 36%

New York – Men’s Apparel 22%

New York – Women’s Apparel 32%

Fixed Controllable Costs (Partly traceable) Percent of Total

London Store 40%

New York Total 40%

– Men’s Wear 45%

-Women’s Wear 40%

-Could not be Traced 15%

Could not be Traced to London or New York 20%

Fixed Noncontrollable Costs (Partly traceable) Percent of Total

London Store 50%

New York Total 40%

-Could not be Traced to Men or Women’s Wear 60%

-Men’s Wear 30%

-Women’s Wear 10%

Total Variable Costs 2,743,000 1,183,000 1,560,000

Contribution Margin 507,000 117,000 390,000

Less:Controllable Fixed Costs 250,000 50,000 100,000 100,000

Controllable Margin 257,000 17,000 290,000

Less: Noncontrollable Fixed Costs 180,000 18,000 90,000 72,000

Contribution by Profit Center 77,000 (68,000) (73,000) 218,000

Less: Nontraceable Costs 65,000

Operating Income 12,000$

Breakdown for the New York Store

New York Store Not Allocated – Men’s Wear -Women’s Wear

Net Sales 1,950,000$ 780,000$ 1,170,000$

Variable Costs:

COGS 1,014,000 312,000 702,000

Variable Operating Costs 546,000 171,600 374,400

Noncontrollable Fixed Costs 72,000 43,200 21,600 7,200

Contribution by Profit Center 218,000$ (58,200) 229,800$ 46,400$

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–51

18-47 (continued –1)

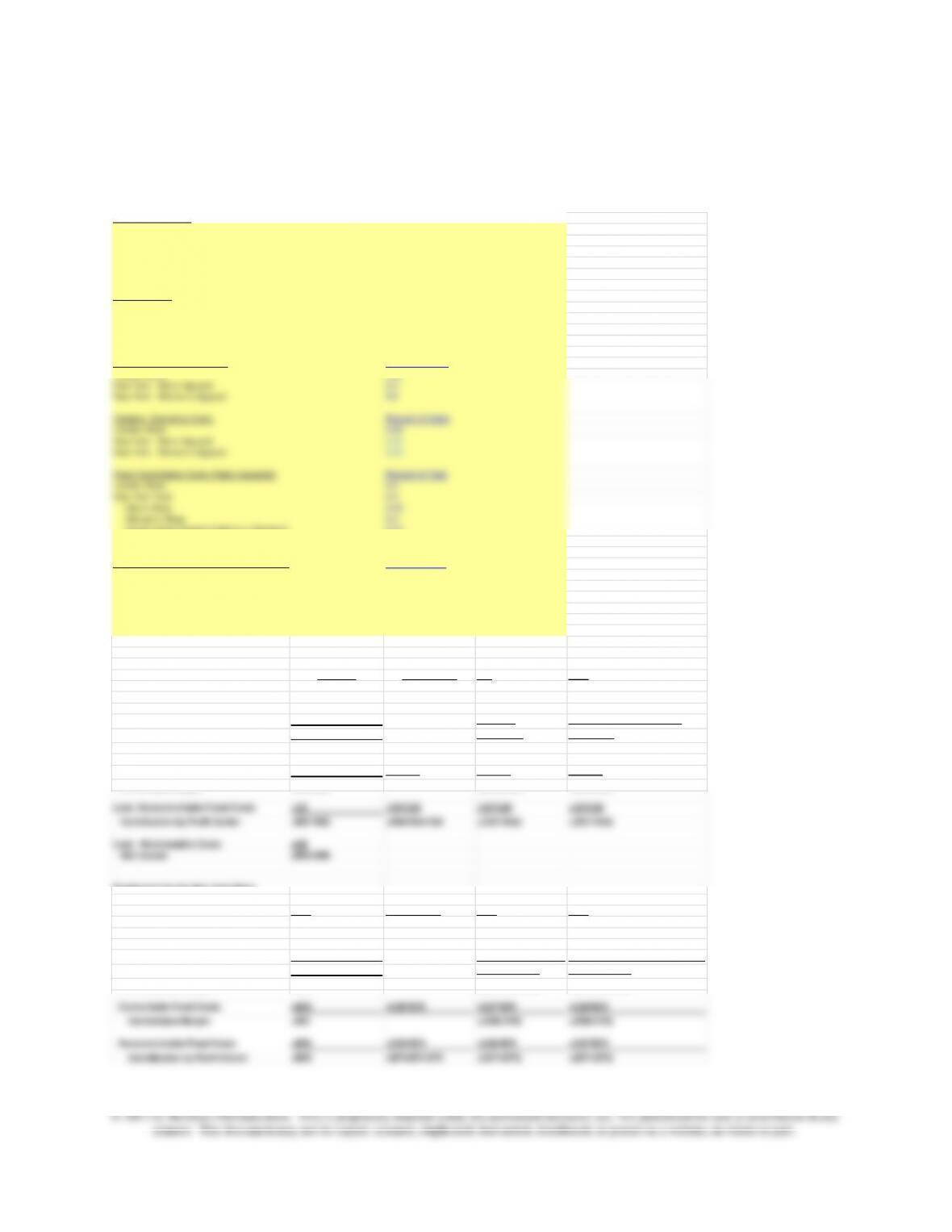

The formulas for the above spreadsheet are as follows:

Data (in thousands)

Total Net Sales 3250000

Fixed Costs

Partly Traceable and Controllable 250000

Partly Traceable but Noncontrollable 180000

Nontraceable Costs 65000

Total Net Sales

London Store 0.4

New York Store 0.6

New York – Men’s Apparel 0.4

New York – Women’s Apparel 0.6

Cost of Goods Sold (Variable) Percent of Sales

London Store 0.55

New York – Men’s Apparel 0.4

New York – Women’s Apparel 0.6

Variable Operating Costs Percent of Sales

London Store 0.36

New York – Men’s Apparel 0.22

New York – Women’s Apparel 0.32

Fixed Controllable Costs (Partly traceable) Percent of Total

London Store 0.4

New York Total 0.4

– Men’s Wear 0.45

-Women’s Wear 0.4

-Could not be Traced to Men’s or Women’s 0.15

Could not be traced to New York or London 0.2

Variable Costs:

COGS =D45+E45 =D43*C15 =((C11*C16)+(C12*C17))*E43

Operating Costs =D46+E46 =C20*D43 =((C11*C21)+(C12*C22))*E43

Total Variable Costs =D47+E47 =(D45+D46) =(E45+E46)

Contribution Margin =D48+E48 =(D43-D45-D46) =(E43-E45-E46)

Less:Controllable Fixed Costs =C4 =C4*C30 =C4*C25 =C4*C26

Controllable Margin =B48-B50 =(D48-D50) =(E48-E50)

Less: Noncontrollable Fixed Costs =C5 =C5*C38 =C5*C33 =C5*C34

Contribution by Profit Center =B51-B53 =B54-D54-E54 =(D51-D53) =(E51-E53)

Less: Nontraceable Costs =C6

Net Income =B54-B56

Breakdown for the New York Store

=A10 Not Allocated =A27 =A28

Net Sales =E43 =E43*C11 =E43*C12

Variable Costs:

COGS =E45 =C16*D63 =C17*E63

Variable Operating Costs =E46 =C21*D63 =C22*E63

Noncontrollable Fixed Costs =E53 =C35*B73 =C36*B73 =C37*B73

Contribution by Profit Center =E54 =B74-D74-E74 =(D71-D73) =(E71-E73)

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–52

18-47 (continued -2)

2. The global issues for High Fashion include foreign currency

translation, as the U.S. dollar fluctuates relative the U.K. pound. For

example, the U.S. dollar increased in value approximately 25%

relative to the pound during 2008 but the two currencies have been

relatively stable since then (as of April 2012). The higher value of the

net effect of the currency change is hard to determine, but it is

important for the company to anticipate an effect on income as a

result of any currency fluctuation.

Other global issues include the state of the economies of the

different countries where High Fashion is doing business. In 2011

and early 2012, the U.K. was in recession and the U.S. economy

was very weak. Economists in mid-2011 had not stated clearly

in the types of clothing carried at the various locations, the hours the

stores are open, and new product offerings, among other measures.

In keeping with the principles of strategic performance measurement

and decentralization, the local store managers should have discretion

in how they respond to the declining economy. The profit center is a

useful tool overall for evaluating performance, but given the economic

changes, the firm should broaden its approach to evaluation to

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–53

18–48 Allocating the Costs of the Legal Department(20 min)

The discussion here is based in part on the article cited below.

The question about allocation of legal department costs raises a number of

key issues which will likely arise in the discussion of the case:

• can legal costs be traced to SBUs that caused or used the legal

assistance?

• are legal costs controllable?

• what is the effect on SBU managers’ behavior and motivation if the

firm allocates legal costs based on revenues, total assets, or some

other measure of size?

• what is the effect on SBU’s managers’ behavior and motivation if the

firm allocates legal costs on the basis of usage?

• what is the effect on SBU’s managers’ behavior and motivation if the

firm treats the legal department as a profit SBU, and allows the other

units to obtain legal services within the firm or to purchase them from

outside legal counsel?

• why not outsource the legal function?

In addressing these questions, some students will argue that the use of

revenues or assets (or any other measure of size) to allocate the legal

costs is arbitrary, and will have hopefully no effect on motivation or

employees to seek legal advice (particularly in regard to compliance with

Sarbanes-Oxley Act’s requirements for a code of ethics and related

requirements), and that it would not provide the experience and continuous

oversight that can be provided by an in-house staff.

18–54

18–48 (continued -1)

Allocating legal costs on the basis of usage raises the question of whether

the legal issues involved are controllable by the units. If so, then this

ethical climate within the firm.

Resource: Bruce R. Gerhardt, “Who Should Pay for In–house Lawyers,”

Cost Management, August 2005, pp. 21-24.

18–55

18–49 Validating the Balanced Scorecard; Spreadsheet Application

(35 min)

1. The balanced scorecard is a more comprehensive approach to

strategic performance measurement. In addition to profit, it includes

measures of performance also for customer service, operational

performance, and improvements in and contributions from operating

personnel.

2. The correlation matrix for the data are shown below. Some

observations are as follows:

• There is a high correlation (r= .88) on the customer survey data with

the sales increase variable, indicating that the survey is a valuable

• Note that there is a high negative correlation between wait time and

customer survey results, as expected from the above observations.

Wait time is a key factor for customers, and appears to figure

significantly in their survey responses.

• There is an indication that some of the older stores are the poorest

performers. Is this due to location or lack up updating in product and

facilities. What is behind this finding?

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–56

18–49 (continued -1)

The change in sales at each of the stores is driven by a number of factors

in addition to those in the analysis shown here. For example, the

economic environment at each store could be changing for better or worse.

Also, a given store might be impacted by the opening or closing of a

competitive store in its area. A full validation study would attempt to

capture as many of these additional variable as possible.

The correlations results for the data:

Sales Survey Review Wait Time Training

Sales 1

Survey 0.882604 1

Review 0.092917 0.030199 1.000000

Wait Time -0.9102 -0.841705 –0.066946 1

Training 0.016167 0.012398 0.056979 -0.109419 1

Note: correlations greater than .5 are significant at p < .05

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–57

18-50 Contribution Income Statement for Profit Centers; Strategy;

International (60 min)

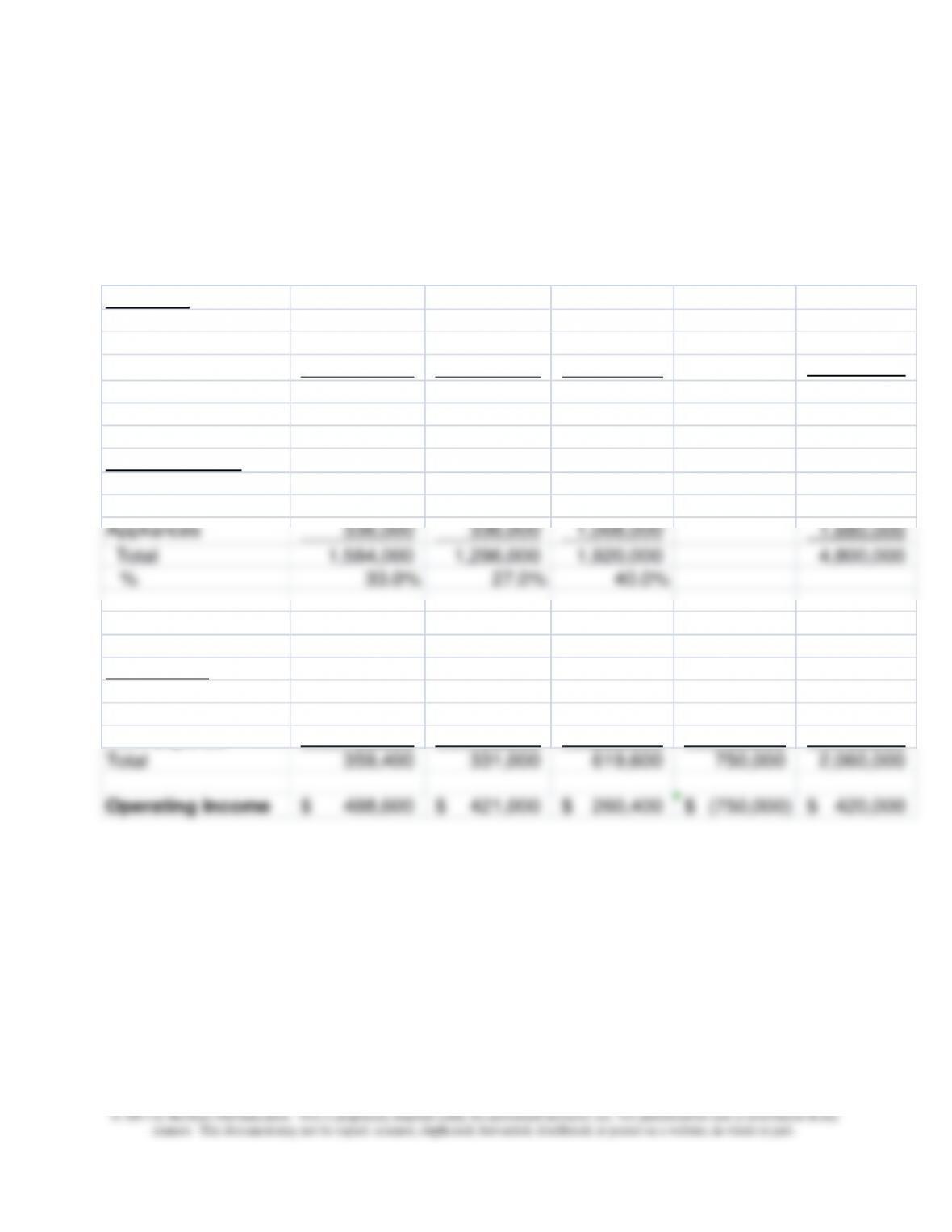

1. Stratford Corporation

Statement of Income by Geographic Area

For the Fiscal Year Ended April 30, 2013

Revenue U.S. Canada Europe

Unallocated

Total

Pharmaceutical 512,000$ 128,000$ 640,000$ 1,280,000$

Sports 1,440,000 1,440,000 720,000 3,600,000

Appliances 480,000 480,000 1,440,000 2,400,000

Total 2,432,000 2,048,000 2,800,000 7,280,000

Variable Costs

Pharmaceutical 384,000 96,000 480,000 960,000

Sports 864,000 864,000 432,000 2,160,000

Appliances 336,000 336,000 1,008,000 1,680,000

Total 1,584,000 1,296,000 1,920,000 4,800,000

% 33.0% 27.0% 40.0%

Contribution Margin

848,000 752,000 880,000 2,480,000

Fixed Costs

Factory Overhead 165,000 135,000 200,000 500,000

Depreciation 134,400 96,000 169,600 400,000

GSA Expense 60,000

100,000

250,000

750,000

1,160,000

Total 359,400 331,000 619,600 750,000 2,060,000

Operating Income 488,600$ 421,000$ 260,400$ (750,000)$ 420,000$

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–58

18-50 (continued -1)

Supporting Calculations

Sales in Units

United StatesTotal Units X % of Sales = Units Sold

Pharmaceutical 160,000 .40 64,000

Sports 180,000 .40 72,000

Appliances 160,000 .20 32,000

Canada

Pharmaceutical 160,000 .10 16,000

Sports 180,000 .40 72,000

Appliances 160,000 .20 32,000

Europe

Revenue

Units Sold x Unit Price = Revenue

United States

Pharmaceutical 64,000 $8.00 $512,000

Sports 72,000 20.00 1,440,000

Appliances 32,000 15.00 480,000

Canada

Pharmaceutical 16,000 8.00 128,000

Sports 72,000 20.00 1,440,000

18–59

18–50 (continued -2)

Variable Costs

Variable Variable Total

Units Mfg Selling Variable

Sold Cost/unit Cost/Unit Cost

(1) (2) (3) (1)x[(2)+(3)]

United States

Pharmaceutical 64,000 $4.00 $2.00 $384,000

Sports 72,000 9.50 2.50 864,000

Appliances 32,000 8.25 2.25 336,000

Canada

Pharmaceutical 16,000 4.00 2.00 96,000

Sports 72,000 9.50 2.50 864,000

Total Area Proportion Allocated

Factory Variable of Factory

Overhead Costs Total Cost

United States $500,000 $1,584,000 33% $ 165,000

Canada 500,000 1,296,000 27% 135,000

Europe 500,000 1,920,000 40% 200,000

$4,800,000 $ 500,000

Depreciation expense

Area Proportion

Total Units of Allocated

Depreciation Sold Total Depreciation

United States $400,000 168,000 33.6% $ 134,400

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–60

18–50 (continued -3)

2. Areas where Stratford Corporation should focus its attention in

order to improve corporate profitability include the following:

The income statement by product line shows that the

pharmaceutical product line may not be profitable. The

pharmaceutical product line does have a positive contribution.

However, because the fixed costs assigned to the product line result

in a loss, Stratford should investigate:

—the possibility of increasing the selling price of these products.

—cutting variable costs associated with this product line.

—discontinuing the manufacture of pharmaceuticals and

concentrating on the other product lines that are more profitable.

The income statement by geographic area shows that the

European market is the least profitable sales area. In order to

3. As a large multinational company, Stratford should develop a

strategic performance measurement system that includes the critical

success factors for such a company. These are likely to include the

effects of foreign exchange fluctuations, differences in taxes between

Europe, Canada, and the United States, as well as currency and