Chapter 11 – Decision Making with a Strategic Emphasis

11–16

Some students may consider the implementation of a shared-services arrangement without the investment

in a systems upgrade. The cost incurred would be only the $45,000 in consultant fees.

However, it is unlikely that the company could achieve the efficiency necessary to implement the

arrangement without a common information system for the three divisions.

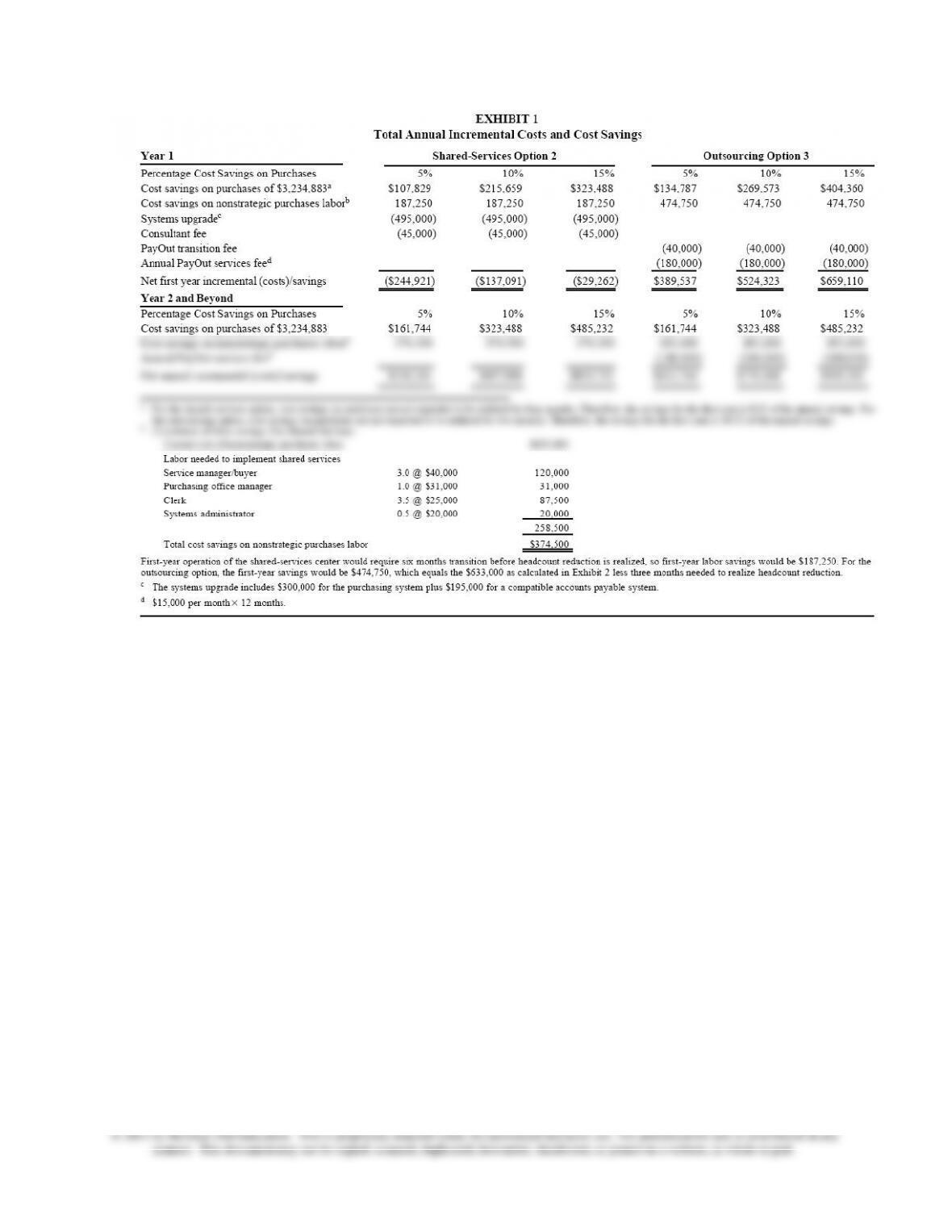

OPTION #3: OUTSOURCE THE PURCHASES-THROUGH-PAYABLES PROCESS

Based on the financial analysis in Exhibit 1, this option provides the greatest potential financial impact for

the company. Among the many nonfinancial issues students may identify are the following (other relevant

courses and topics are included in parentheses).

Chapter 11 – Decision Making with a Strategic Emphasis

11–17

Nonfinancial Issues

Advantages

• Technological risk is passed to PayOut.

• PayOut is more likely to achieve the maximum savings on purchases due to its volume with

multiple clients.

• PayOut is more likely to achieve savings on all nonstrategic purchases for which GPF does not

Disadvantages

• GPF may end up paying for excess capacity if invoices are collapsed across GPF subsidiaries and

result in total volume of less than 30,000.

• Unforeseen difficulties may be experienced in integrating PayOut and GPF information systems.

• Longer lead times may be experienced when local vendors are not used (integrate performance

measurement, contracting, and community involvement).

Other Potential Concerns

• What recourse does GPF have for late or missed payments by PayOut? (integrate service level

agreements, performance measurement, and contracting requirements)

• Who is responsible for processing errors and exceptions? (integrate accounting information

systems processing and contracting requirements)

• Does PayOut have a SAS No. 70 Service Organizations review report available from a reputable

auditor? (integrate audit special reports and SAS No. 70)

• What internal controls are in place to segregate GPF.s data from data of other clients? (integrate

auditing and design of effective internal control systems)

Chapter 11 – Decision Making with a Strategic Emphasis

11–18

CONCLUSION

In teaching the case, one of the issues that might be raised is why GPF should focus on improving the

bottom line through cost efficiencies instead of focusing on the customer and increasing revenues. Such a

question may be even more meaningful if the concept of the balanced scorecard has been discussed. First,

the internal process of purchasing nonstrategic items is not one at which the company must excel to

Finally, if time allows or other directions are desired, the instructor may choose to point out the various

areas of accounting and business knowledge that are needed for such a decision. For example, the

decision to outsource should lead GPF to require a service level agreement with PayOut. Such an

agreement would specify acceptable levels of performance, so the discussion could move to performance

metrics and measurement. With these items being specified in the outsourcing contract, there is the

opportunity to address legal issues involved in such contracting arrangements, including penalties for

nonperformance. Approaching the discussion in this manner will enforce the reality that functional areas

of accounting are integrated not only with other areas of accounting, but also across other business

disciplines.

Chapter 11 – Decision Making with a Strategic Emphasis

11–19

Case 11-6: Pop’s, Inc.

Targeted Courses/Prerequisites

The case is targeted for use in a upper-level Managerial/Cost Accounting Course, but could also be used

in an Introductory MBA-level course in Managerial Accounting. Because the case is designed for

beginning managerial accounting students, there are no formal pre-requisites for completing the case.

However, a background in cost allocation, mark-ups, and spreadsheets would be useful in finishing the

case.

Case Summary and Objectives

The attached case is based on cost analysis techniques used by finance managers working in the consumer

products industry. While the sensitivity of strategic positioning and cost structures prevented us from

utilizing actual product information, the attached case is based upon a real world situation in the beverage

industry. The case is designed to challenge students to think beyond the numbers and encourage them to

integrate cost accounting into some basic strategic business concepts normally covered in Marketing and

Policy & Strategy Courses.

The case requires students to engage in the process of finding the total cost associated with producing and

selling a new product. While students are required to utilize cost accounting skills in solving the case, the

main focus is on the strategic analysis of the situation. A critique of the cost summary requires students to

engage in the discussion of several strategic decisions embedded in the case. The case discussion should

lead students to begin generating many important questions that should be asked in this type of business

situation. Questions such as: (1) What assumptions are we making?; (2) How reliable are the data?; (3)

Are we thinking myopically?; (4) What are we missing [what data do we still need]?; (5) Are the numbers

actionable?

Specific case requirements include performing the basic cost procedures of accounting for direct costs,

allocating manufacturing overhead and period costs, and determining margins to develop a “cost +

margin” pricing analysis. Upon completion, students should be able to think through the production

process, identify key cost drivers, and understand the role cost accounting plays in the introduction of new

product initiatives.

Time Frame for Teaching the Case

This case has been classroom tested on four separate occasions in the lead author’s 300-level

managerial/cost accounting course. The lead author has found that introducing the case early in a

managerial/cost accounting class provides students with a basic understanding of key cost accounting and

manufacturing fundamentals that can later be leveraged when introducing more advanced topics. In fact,

the benefits of utilizing the case endure throughout the course by not only increasing student interest, but

also redefining student perceptions of the accountant’s expanding role in an organization.

A fifteen-minute introduction to the case is normally provided during the 3rd week of a semester course.

Historically students have spent between 3-5 hours in preparing the case, and the completed case and

discussion is normally required during the 5th week of the semester. After the students have finished the

case 30-35 minutes of class time is invested in discussing the case and the strategic implications.

Chapter 11 – Decision Making with a Strategic Emphasis

11–20

Learning Outcomes

This case has been used in the classroom on several occasions, which has provided the opportunity to

improve several aspects of the case and obtain feedback on learning outcomes. While the breadth of

topics and the variance in student backgrounds make it difficult to pinpoint every learning objective, the

major competencies addressed include (1) Problem Solving and Decision making, (2) Strategic / Critical

Thinking, (3) Fundamental Cost Accounting Skills, and (4) Spreadsheet Development / Presentation.

Instructor’s Solution/Discussion Items

Before beginning a discussion of the cost analyses, it is extremely important to remind the students of the

“big picture.” After completing the cost calculations, students tend to be very narrowly focused. It is quite

helpful to remind them of the following case facts: (1) Pop’s currently has a 4.7% share of the non-cola

market, (2) top management wants to accelerate growth, (3) the company is considering entering the cola

market and competing directly with Coke and Pepsi, (4) Pop’s Cola tested well in a national blind taste

test and in a Denver test market, (5) Pop’s has no manufacturing capacity, and (6) Pop’s has limited

distribution capabilities.

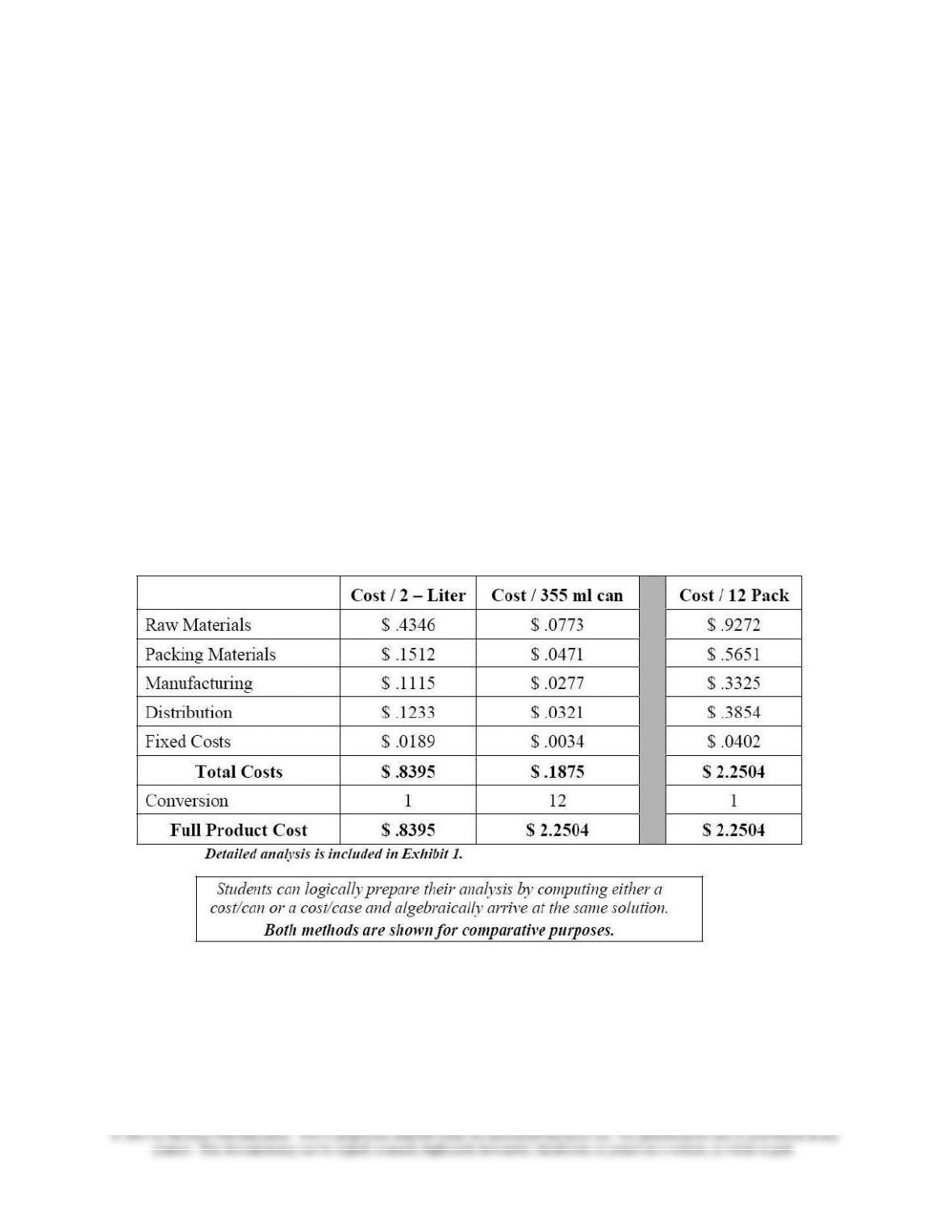

Question 1: Calculate the Full Product Unit Cost of both the 12 pack and 2-Liter products. Make

certain to round to four decimal places and include a detailed analysis by component (Raw

Materials, Packing Materials, etc.)

It is important that students understand that unlike this and other ‘textbook’ problems there is seldom one

single answer in any cost analysis project. Several iterations often need to be run using different volume

and mix scenarios to enable management to understand the sensitivity of these factors. These iterations

need to reveal how significantly fixed costs / unit changes with fluctuations in volume. Volume changes

may also influence other factors such as pricing tiers or volume penalties on Raw Materials, Packing

Materials, and even Contract Manufacturing activities.

Chapter 11 – Decision Making with a Strategic Emphasis

11–21

While Pop’s Cola’s volume forecast comes from an actual test market (often an accurate volume

indicator), it is important to realize that the volume and mix forecasts provided are still only estimates and

there is a high probability that there will be fluctuations. Because Pop’s, Inc. did not test a specific price

point but merely matched the pricing of Coke and Pepsi, its volume forecasts are less reliable and

therefore require even greater analysis.

Additionally, the company needs to adjust its volume forecast to include a competitive response from

Coke and Pepsi. Otherwise, its volume assumption will likely be overstated.

When the cost model is set-up correctly (see Exhibit 1) it is easy to plug in different volume estimates and

observe that given the relatively low amount of incremental fixed costs, there is very little change in fixed

costs per unit even with large fluctuations in volume. For instance if volume doubles there is less than a

5-Cent decrease in cost / unit, and conversely a 50% decrease in volume results in less than a 10-Cent

increase in cost / unit. This unusually low cost sensitivity is due to Pop’s, Inc. decision to outsource its

manufacturing process, which provides a more variable costing scenario and reduces the risk associated

with building a new manufacturing facility.

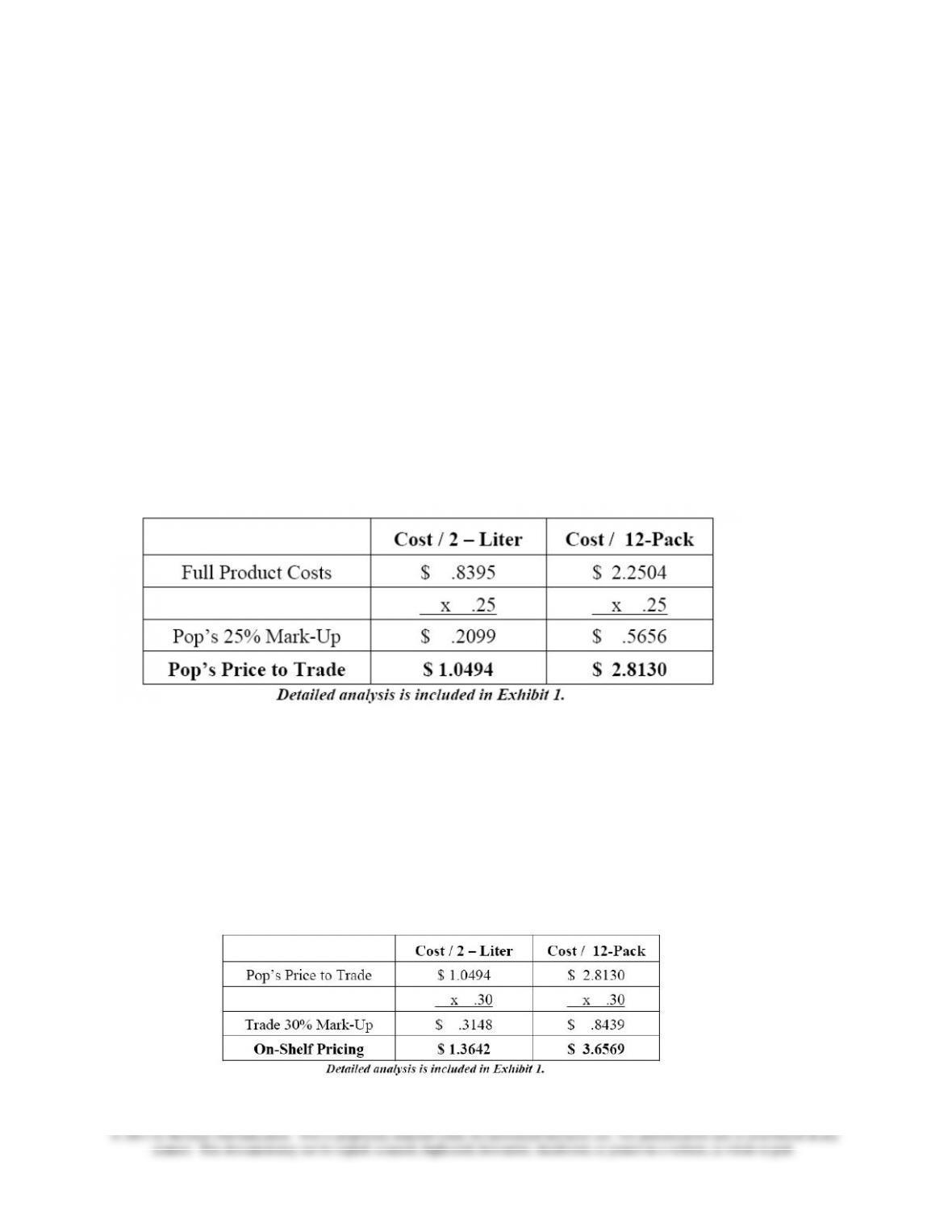

2. At what price would Pop’s, Inc. need to sell the 2–Liter and 12 pack to “the trade” in order to

provide a 25% profit mark-up for Pop’s, Inc. shareholders (Pre-Tax & Pre-Interest Expense)?

Pop’s, Inc. has determined that it needs a 25% mark-up on its costs to provide a return for its shareholders

and cover any incremental general and administrative costs, interest expense, income taxes. While beyond

the scope of this case, an analyst would normally build a NPV model requiring the estimation of cash

flows by determining revenue growth rates, estimating inflation of inputs and processing, and discounting

those cash flows at cost of capital that reflects the risk associated with the project. This model would treat

the capital investments as outflows in year zero and utilize depreciation to provide a tax shield.

3. At what Price would the trade sell the 2 Liter and 12-pack on-shelf to the final consumer

assuming on average “the trade” requires a 30% mark–up?

Chapter 11 – Decision Making with a Strategic Emphasis

11–22

Trade Margin Discussion

It is important to emphasize that because of the risk involved in selling a new brand most retailers will

require a higher mark-up (return) for selling Pop’s Cola than other more established brands. This trade

disadvantage is compounded in the Cola Industry, where Coke and Pepsi have established such a large

consumer pull that retailers are willing to sell Coke and Pepsi at a loss in order to attract consumers

(“Loss Leader” pricing). Depending on Pop’s influence on retailers they may also be required to pay

slotting allowances in order to obtain shelf-space. These fees can be substantial and could quickly

consume a $6 million promotional/advertising budget.

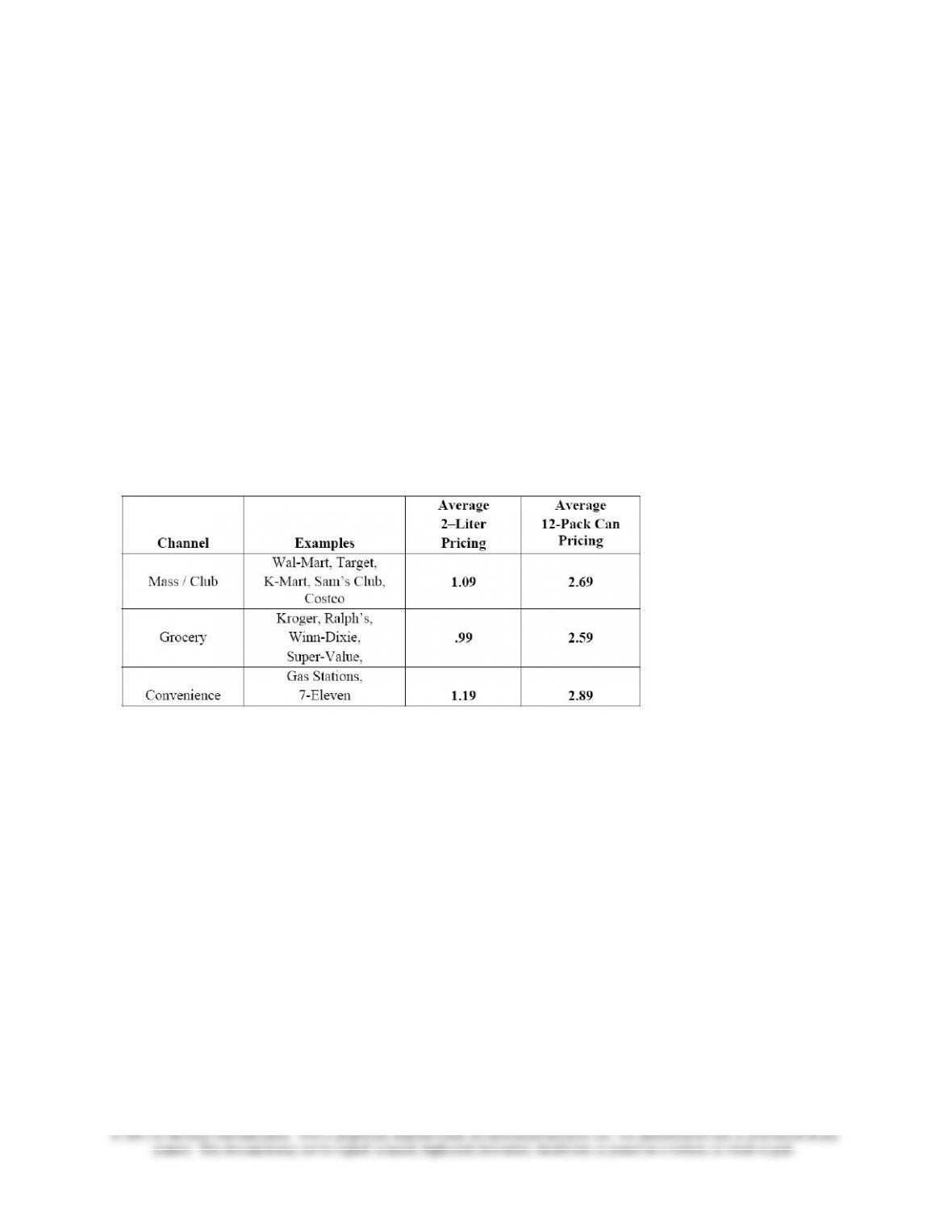

4. (Optional) Visit at least three different channels (i.e. Grocery, Mass/Club Stores, and

Convenience Stores) that distribute Coke and Pepsi products. For each location visited list the Store

Name, Location, Date, and the promotional pricing currently offered for both the 2-Liter and 12-

Pack products.

Note: If this question is not selected, students will need to be provided with the following on-shelf pricing

in order to properly answer questions 5 & 6. The following should be used with caution as actual pricing

will fluctuate depending on the product’s location, promotions, and type of channel researched.

For the vast majority of consumer products the Mass/Club channel will require the lowest trade margins

followed by Grocery stores, and Convenience/Specialty stores. However, in the cola industry on-shelf

pricing is usually the lowest in the grocery channel, because Supermarkets and Convenience stores tend to

utilize cola products as “loss leaders”, while Mass and Club stores generally draw customers based on

overall low pricing and attempt to maintain some small margin on all products.

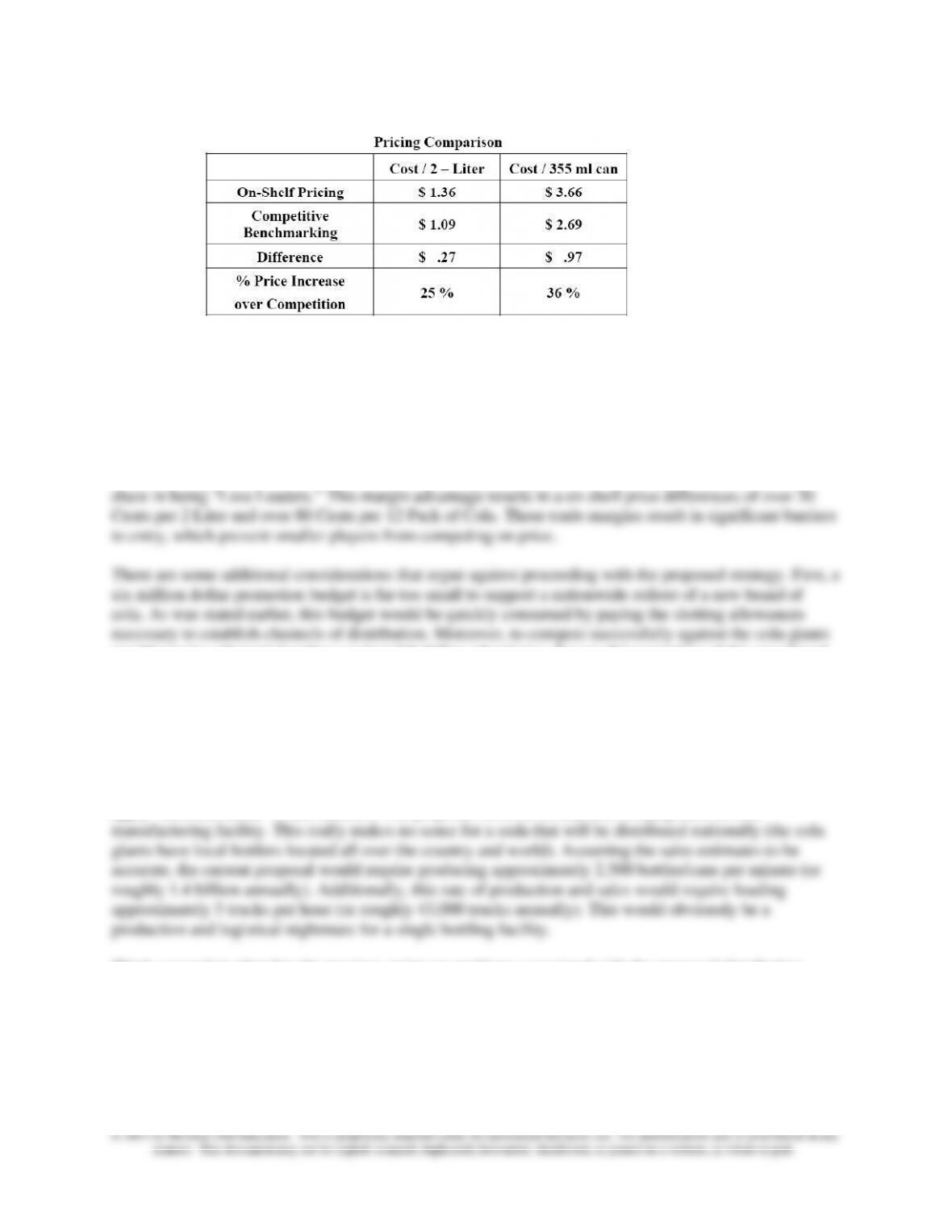

5. Based on a comparison between your cost analysis and competitive benchmarking would you

recommend that Pop’s, Inc. enter the “Cola Market” and compete directly with Coke and Pepsi?

Provide a strong justification for your conclusion and discuss what factors influence the difference

in on-shelf pricing between Coke & Pepsi and Pop’s Cola.

Competing head to head with Coke and Pepsi directly on a cost basis will obviously not be a wise strategy

for Pop’s Cola. In fact, the following table reveals that Pop’s pricing is approximately 25% higher than its

competition on the 2 Liter and 36% higher on the 12-Pack product.

Chapter 11 – Decision Making with a Strategic Emphasis

11–23

Several reasons exist for the pricing/cost advantages that Coke and Pepsi share. Probably the most

obvious advantage deals with mere scale in relation to manufacturing and advertising expenditures. For

example, the combined U.S advertising spending for Coke and Pepsi is approximately $300 Million. It is

nearly impossible for a company like Pop’s, Inc. to compete on cost against these giants, because the

competition can spread these costs over such large sales volumes.

The other major reason that makes it difficult to compete on price is the advantage that Coke and Pepsi

would require substantial outlays on brand-building advertising. Successful promotion of this new brand

would also require various forms of sales promotion such as: (a) free samples, (b) price

promotions/coupons, (c) aisle/point of purchase displays, (d) ongoing trade allowances, and perhaps (e)

sponsored events. The proposed budget could not begin to cover these various expenses.

Second, while the contract manufacturing arrangement with Shull Enterprises may appear on the surface

to be a good solution to Pop’s limited production capabilities, a deeper analysis will demonstrate the

infeasibility of this approach. Indeed, this represents a situation where somebody failed to sit down and

apply “business sense” to the numbers. The proposal involves investment in equipment for one

Third, somewhat related to the previous point are problems associated with the proposed distribution

strategy. The current plan involves delivering full truckloads to customers’ distribution warehouses. This

may work for larger retail chains, but would likely be infeasible for smaller chains and independent

stores. For example, the latter would be incapable of receiving and storing 46,000 cans of Pop’s Cola.

Even if these retailers were part of some type of retail cooperative, the costs of marketing to and through

them would quite likely be different than with larger chains, and these differences would need to be

incorporated in the cost analyses.

Chapter 11 – Decision Making with a Strategic Emphasis

11–24

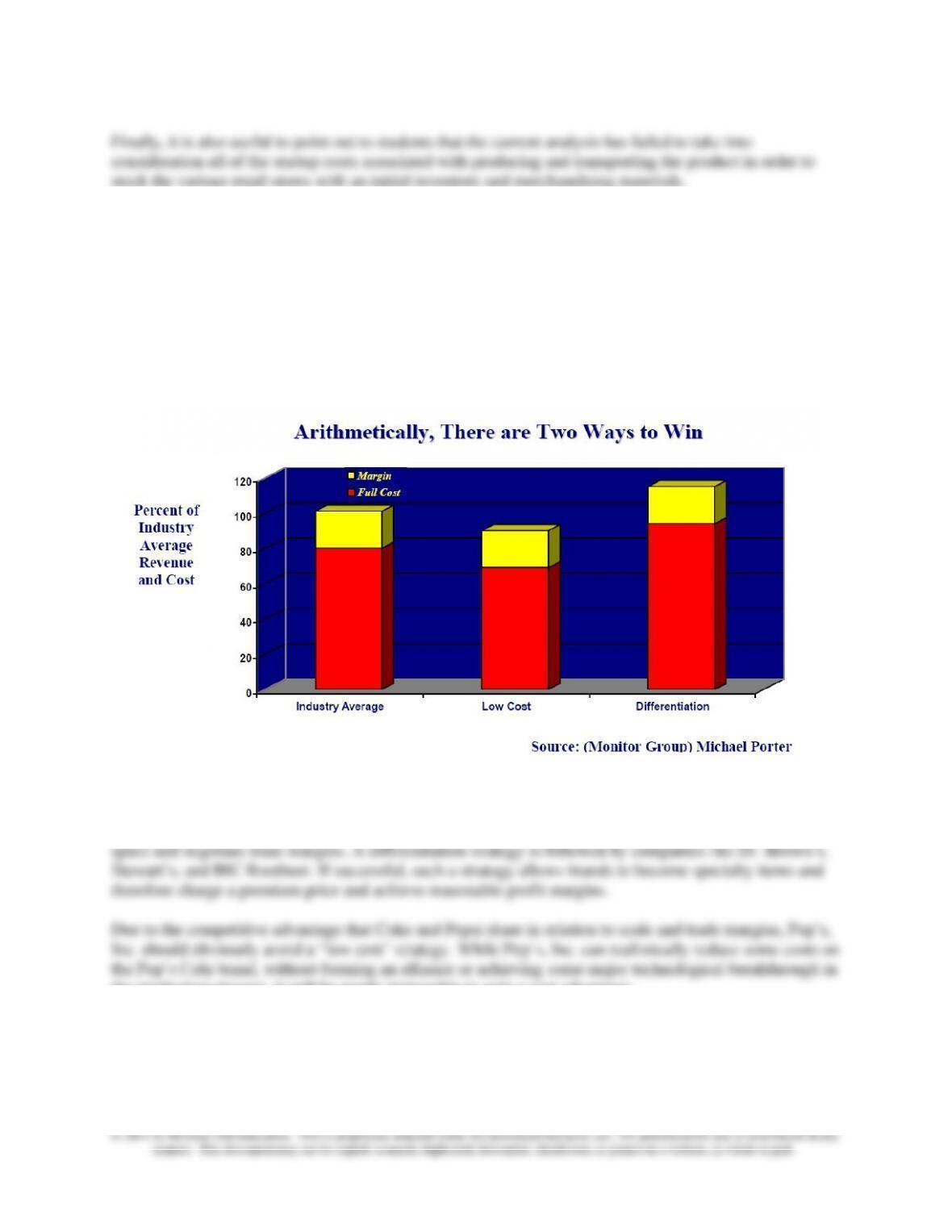

6. Prepare an alternative strategy for gaining market share in the beverage industry. Determine

whether Pop’s, Inc. should compete using a “Low Cost” or a “Differentiation” strategy, and

provide specific examples of how you would implement your strategy.

In most industries there are two distinct ways to compete through following either a “Low Cost” or a

“Differentiation” Strategy. Assuming an industry has an average 20% profit margin and maintains 80%

full product costs, the graph below is useful in illustrating that both strategies can be successful. In order

to successfully maintain a 20% margin, producers must either have a competitive cost advantage, or have

a differentiable product that adds enough value to allow them to price above the industry average.

Several examples of these two strategies exist in the beverage industry. Store brands such as Sam’s

Choice or Big K follow a “Low Cost” strategy. Since these store brands are obviously marketed directly

through the retailer they have the unique relationship with the trade channels that allow them to gain shelf

the production process, it will be nearly impossible to gain a cost advantage.

Moreover, ask the students whether it would be wise to market the proposed cola on the basis of price. At

this point students should be reminded of the national blind taste test results. The Pop’s management team

became excited about the new cola when consumers responded favorably to it when compared to Coke

and Pepsi in the blind taste tests. Students should be asked to consider whether it would be sound business

Chapter 11 – Decision Making with a Strategic Emphasis

11–25

strategy to market a new cola with a superior taste on the basis of a low price. It might also be useful to

have them discuss whether they believe consumers would view it as superior when the “Pop’s” brand is

attached to it. Consumers often cannot distinguish well between brands in blind tests, but have clear

preferences when a product is branded.

In the authors’ opinion it is quite clear that Pop’s, Inc. would need to follow a differentiation strategy.

This decision would require Pop’s, Inc. to research ways to redefine its target markets and differentiate its

• Sizing – In order to take the emphasis off Coke and Pepsi price points, Pop’s, Inc. may want to create a

totally new size line-up. For instance Pop’s, Inc. may be able to sell a .75L Bottle or a 200 ml can of its

premium beverage that would alleviate consumers’ desire to constantly compare pricing to Coke and

Pepsi.

• New–to–the-world flavors/ingredients – Research could be conducted to identify ways of creating a new

soda category. In other words, many good arguments could be built against competing directly with the

flagship brands of the cola giants. There have been few successful national cola brands and those that

have survived are relatively minor players in the global cola war (e.g., R.C. Cola, Shasta, and Jolt). As is

described in the case, Pop’s, Incorporated achieved its current level of success in the non-cola market.

strategies. For example, many school systems have recently removed soda machines due to concerns

about health. Pop’s may be able to re-open this distribution channel by developing one or more healthful

carbonated soft drinks that would be acceptable to schools and parents. Additionally, this type of

differentiation strategy would require re-thinking the entire distribution strategy. Some retailers (e.g.,

convenience stores and club/mass retailers) may be less appropriate channel members and other types

(e.g., specialty, gourmet, and health food stores, as well as certain types of restaurants and delis) may

become important channel members.