1) the mathematical technique that underlies the reciprocal cost allocation method is:

a.regression analysis

b.simultaneous equations

c.analysis of variances

d.complex algebraic functions

e.multiple correlation

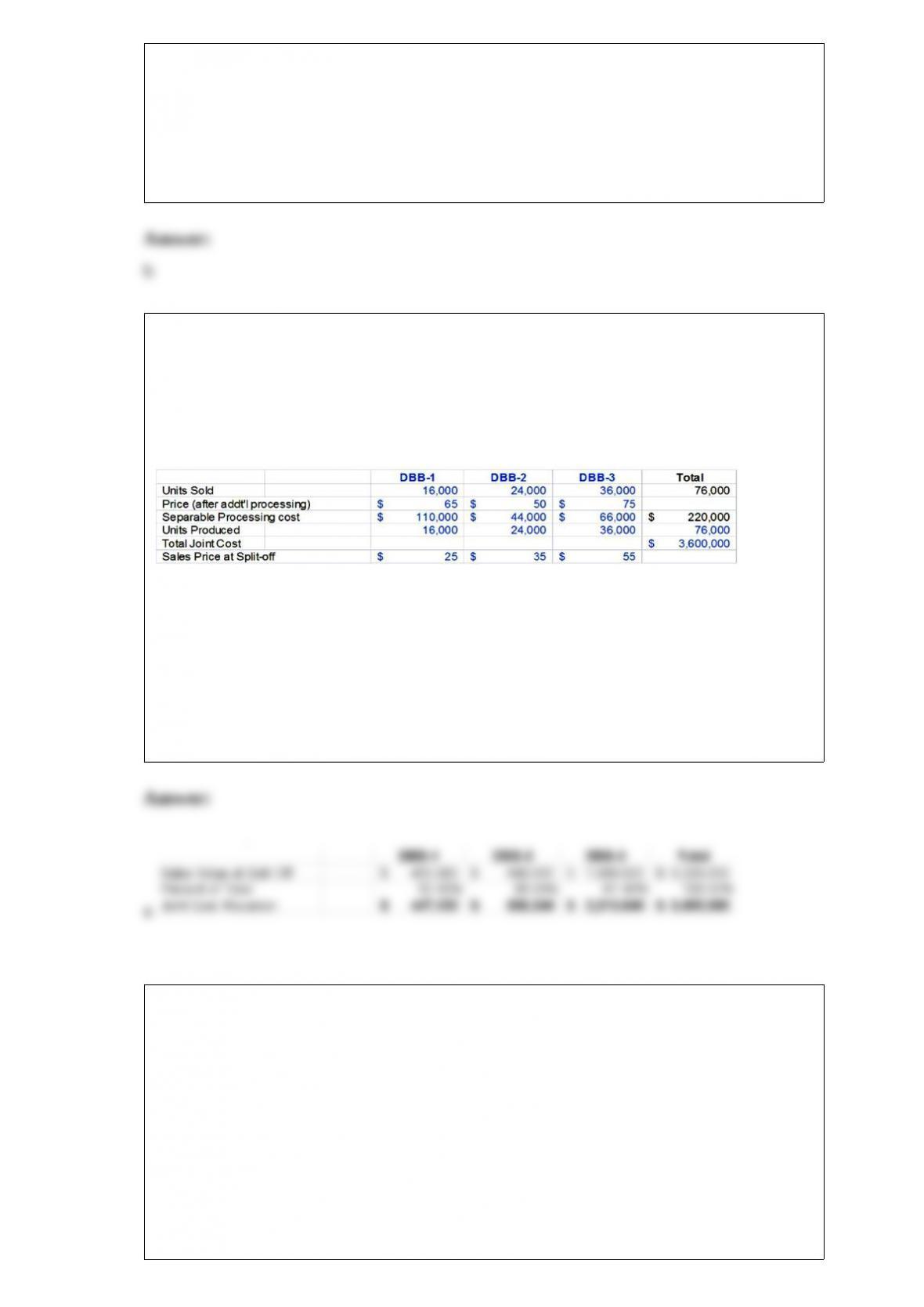

2) marin products produces three products dbb-1, dbb-2, and dbb-3 from a joint

process. each product may be sold at the split-off point or processed further. additional

processing requires no special facilities, and production costs of further processing are

entirely variable and traceable to the products involved. key information about marin’s

production, sales, and costs follows.

the amount of joint costs allocated to product dbb-2 using the sales value at split-off

method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%,

and round all dollar amounts to the nearest whole dollar):

a.$939,240

b.$216,870

c.$447,120

d.$757,800

e.$2,213,640

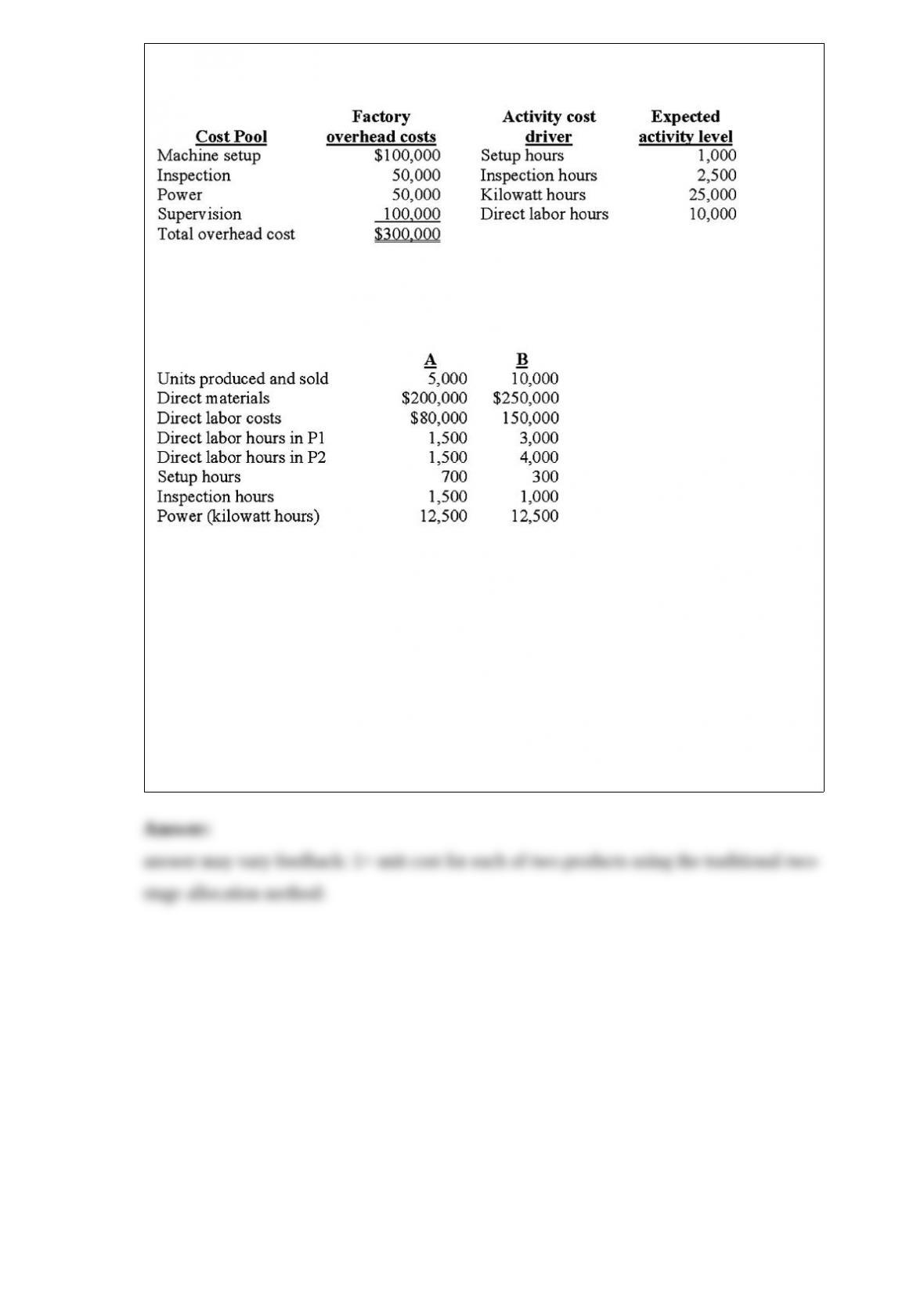

3) demski company has used a two-stage cost allocation system for many years. in the

first stage, plant overhead costs are allocated to two production departments, p1 and p2,

based on machine hours. in the second stage, demski uses direct labor hours to assign

overhead costs from the production departments to individual products a and b.

budgeted factory overhead costs for the year are $300,000. both the budgeted and actual

machine hours in p1 and p2 are 12,000 and 28,000 hours, respectively.

after attending a seminar to learn the potential benefits of adopting an activity-based

costing system (abc), ted demski, the president of demski company, is considering

implementing an abc system. upon his request, the controller at demski company has

compiled the following information for analysis:

demski manufactures two types of product, a and b, for which the following

information is available:

required:

1> determine the unit cost for each of the two products using the traditional two-stage

allocation method. round calculations to 2 decimal places.

2> determine the unit cost for each of the two products using the proposed abc system.

3> compare the unit manufacturing costs for product a and product b computed in

requirements 1 and 2 .

(a) why do two the cost systems differ in their total cost for each product?

(b) why might these differences be important to the demski company?

4) the weighted-average method is most appropriate when:

a.work in process is relatively small

b.conversion costs are stable

c.direct materials prices are stable

d.all of the above

5) all of the following are examples of total quality management practices except:

a.redesign of a product to reduce its parts by 50 percent

b.reduction in the movement required in a manufacturing job

c.separating the sales and services functions

d.raising raw material quality standards

e.cross-training assembly line workers to cover sick leave absences

6) the journal entry to record requisitioned and usage of direct materials would include

a credit to:

a.work-in-process inventory

b.accrued payroll

c.factory overhead

d.materials inventory

e.finished goods inventory

7) the sum of the beginning inventory units and the number of units started during the

period determines the:

a.units completed during the period

b.units to account for

c.units transferred in during the period

d.units accounted for

e.units started during the period

8) assume the following information pertaining to moonbeam company:

costs incurred during the period are as follows:

materials purchases are calculated to be:

a.$143,000

b.$156,000

c.$91,000

d.$169,000

e.$140,000

9) calcuco hired effner & associates to design a new computer-aided manufacturing

facility. the new facility was designed to produce 300 computers per month. the variable

costs for each computer are $660 and the fixed costs total $74,700 per month. the

average cost per unit, if the facility normally expects to operate at eighty-five percent of

capacity, is calculated to be (round to nearest cent):

a.$952.94

b.$909.00

c.$936.67

d.$971.25

e.$942.47

10) a plan showing the units of goods expected to be sold and the expected revenue

from sales is called the:

a.cash budget

b.sales receipts budget

c.selling expense budget

d.cash receipts budget

e.sales budget

11) strategic analysis uses which of the following to help a firm improve its competitive

position through an analysis of product and production complexity?

a.differential cost drivers

b.discretionary cost drivers

c.structural cost drivers

d.marginal cost drivers

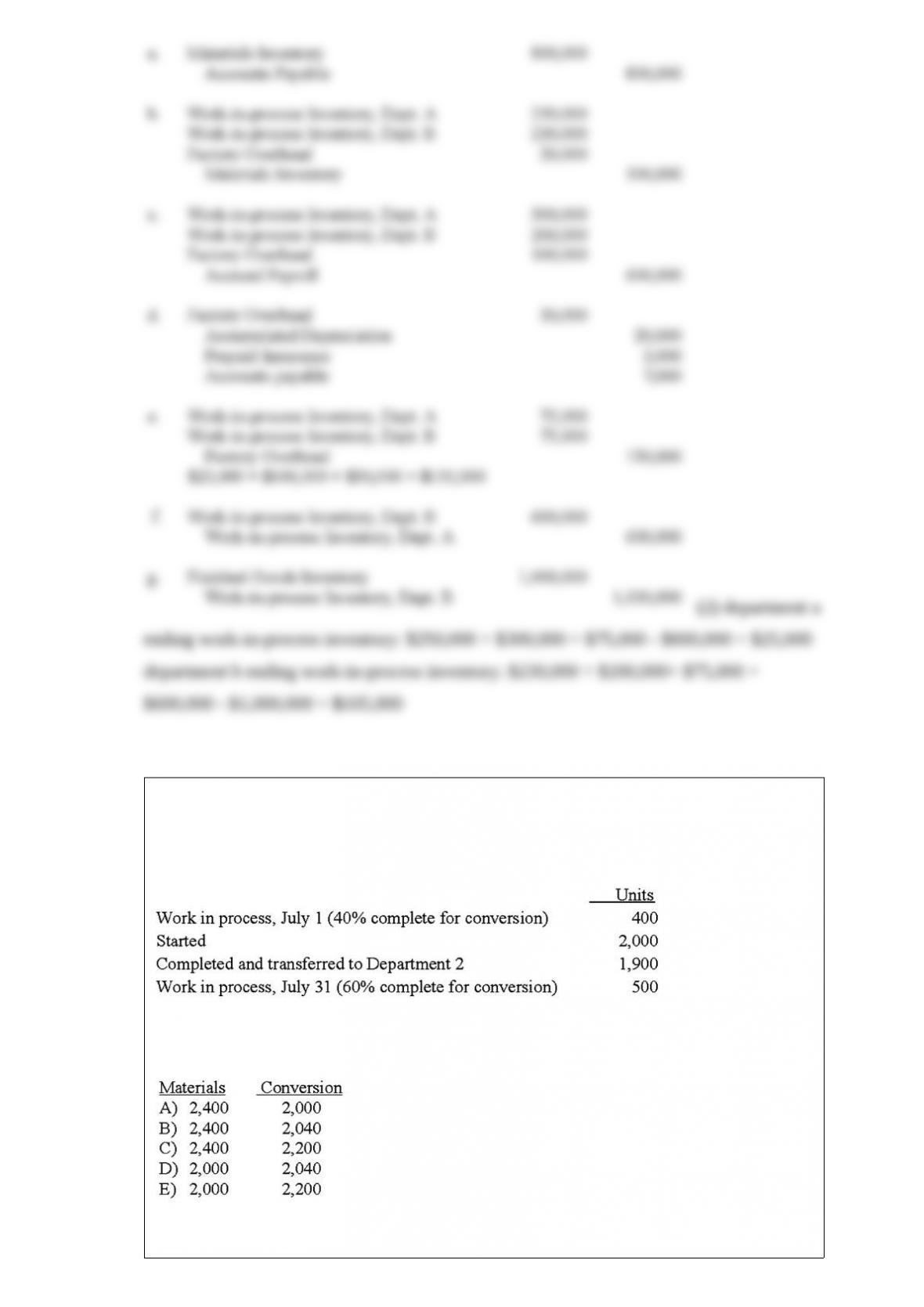

12) irvine company uses process costing. the following data are available for the month

of june.

(a) materials purchased, $800,000.

(b) materials used: direct materials: department a $250,000, department b $230,000.

indirect materials: $20,000.

(c) factory payroll incurred, $600,000: direct labor: department a $300,000, department

b $200,000. indirect labor: $100,000.

(d) other factory overhead incurred, $30,000: power and light $2,000, depreciation

$20,000, property tax $5,000, insurance $3,000.

(e) factory overhead cost was allocated equally to department a and department b.

(f) department a completed and transferred to department b $600,000.

(g) department b completed and transferred to finished goods inventory account

$1,000,000.

required:

(1) prepare journal entries for june activities in irvine company.

(2) compute ending working-in-process inventories in department a and department b.

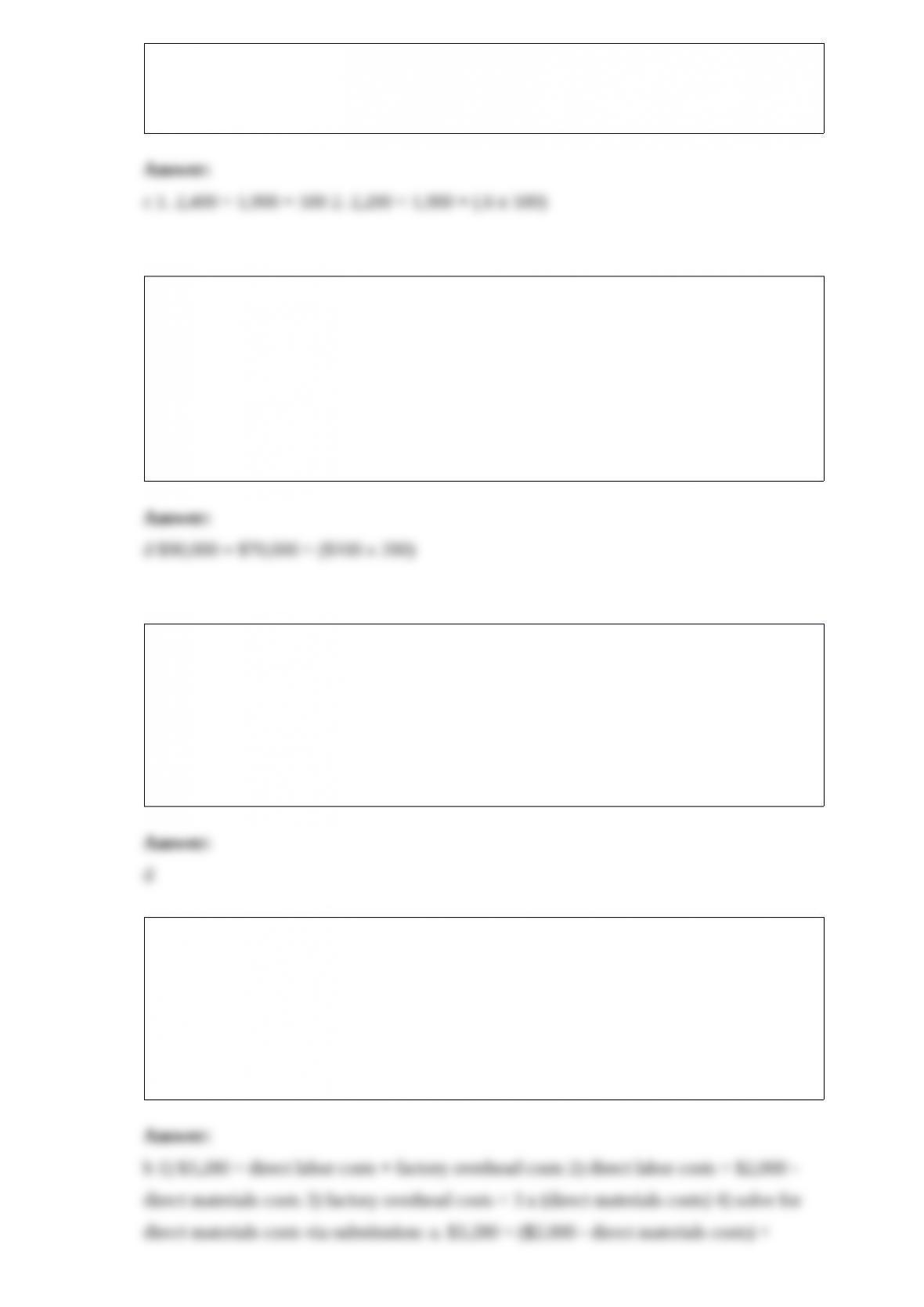

13) defond company has a process costing system. all materials are introduced at the

beginning of the process in department one. the following information is available for

the month of january:

what are the equivalent units for the month of july if the company uses the

weighted-average method?

a.option a

b.option b

c.option c

d.option d

e.option e

14) direct materials and direct labor costs total $70,000 and factory overhead costs total

$100 per machine hour. if 200 machine hours were used for job #333, what is the total

manufacturing cost for job #333?

a.$20,000

b.$70,200

c.$70,000

d.$90,000

e.$100,000

15) “budgetary slack” occurs when:

a.employees refuse to adhere to budgeted plans and operations

b.the budget is so difficult to meet that employees slack-off from work

c.an authoritative, or imposed, budgeting process is used

d.in order to “meet” budget objectives, employees ask for resources in excess of what

they need

e.employees ask for fewer resources than they need, in order to continuously improve

16) factory overhead costs for a given period were 3 times as much as the direct

material costs. prime costs totaled $2,000. conversion costs totaled $3,280. what are the

direct labor costs for the period?

a.$1,220

b.$1,360

c.$1,410

d.$1,540

17) the emphasis on effective _________ has ________ significantly in recent years in

response to sec requirements imposed by the sarbanes-oxley act of 2002 .

a.cost allocation; decreased

b.internal accounting controls; increased

c.profitability; increased

d.cost drivers; decreased

18) which of the following is not a step in the preparation of a production cost report?

a.analyze the physical flow of production units

b.determine total costs for each manufacturing cost element

c.compute cost per equivalent unit for each manufacturing cost element

d.calculate incomplete units for each manufacturing cost element

19) cost management information typically is the responsibility of the:

a.chief financial officer

b.controller

c.treasurer

d.chief information officer

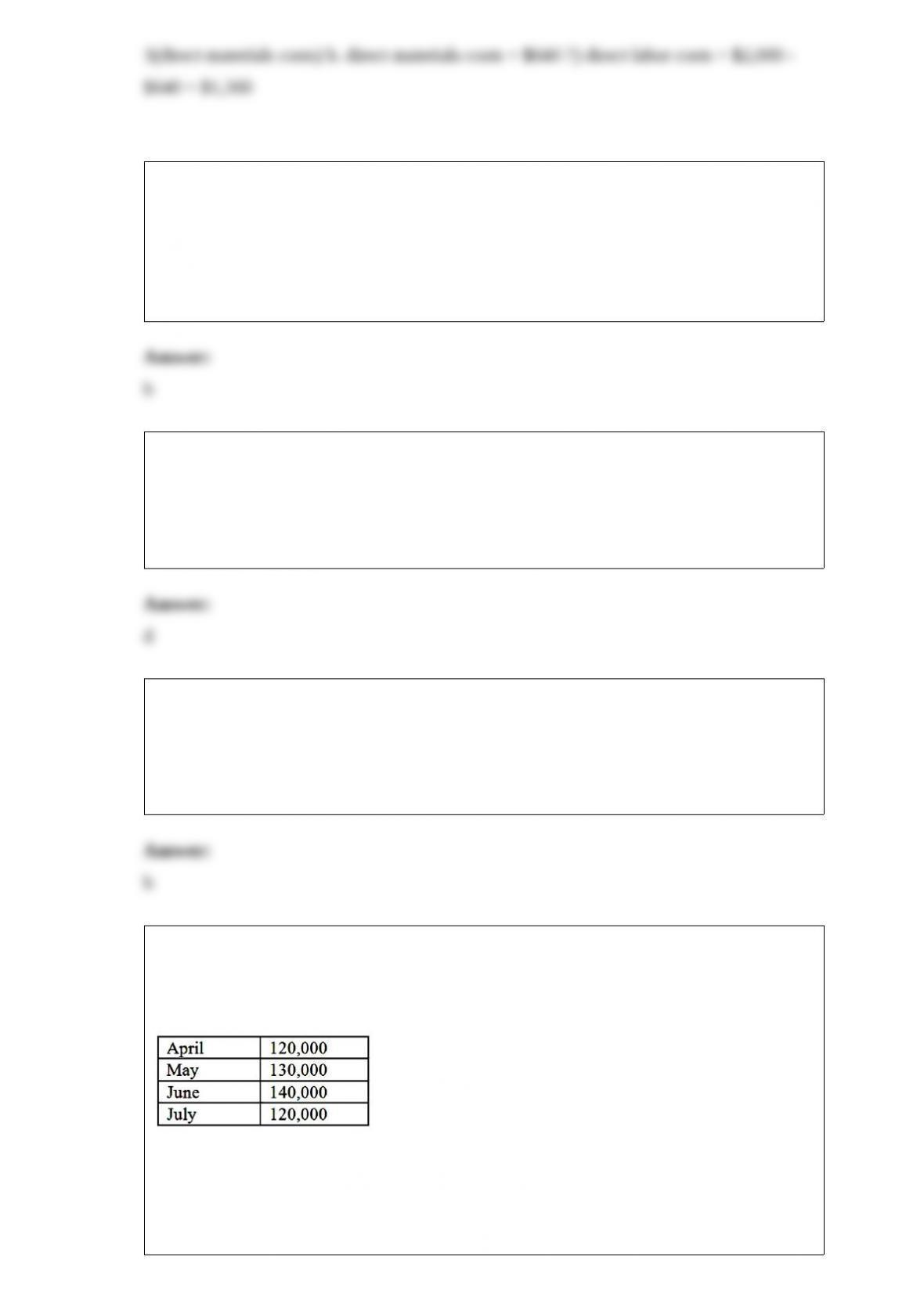

20) doanne food processing expects to have 36,000 pounds of raw materials inventory

on hand on march 31, the end of the current year. the company budgets the following

production (in units) for the first four months of the coming year:

at the end of each month the firm desires its ending raw material inventory to be 10% of

the next month’s production needs. a finished unit requires three pounds of raw

materials.

doanne’s budgeted purchases for raw materials (in pounds) during april should be:

a.224,000

b.360,000

c.363,000

d.399,000

e.435,000