Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-1

CHAPTER 13:

Cost Planning for the Product Life Cycle: Target Costing, Theory of

Constraints, and Strategic Pricing

QUESTIONS

13-1 Target costing is a method by which the firm determines the desired cost for the

13-2 A firm has two options for reducing costs to a target cost level:

a. Reduce costs to a target cost level by integrating new manufacturing

technology, using advanced cost management techniques such as activity-based

method is the more common of the two, because it recognizes that design

decisions account for much of total product life cycle costs (see Exhibits13.3 and

13.12). By careful attention to design, significant reductions in total cost are

possible. This approach to target costing is associated primarily with Japanese

manufacturers, especially Toyota, which is credited with developing the method

in the mid-1960s. This method of cost reduction is common in consumer

electronics.

13-3 The sales life cycle refers to the phase of the product’s sales in the market - from

introduction of the product to decline and withdrawal from the market. In

contrast, the cost life cycle refers to the activities and costs incurred in

developing a product, designing it, manufacturing it, selling it and servicing it. The

phases of the sales life cycle are:

Phase Three: Maturity. Sales continue to increase but at a decreasing rate.

There is a reduction in the number of competitors and product variety. Prices

soften further, and differentiation is no longer important. Competition is based on

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-2

13-4 The strategic pricing approach changes over the sales life cycle of the product. In

the first phase, pricing is set relatively high to recover development costs and to

take advantage of product differentiation and the new demand for the product. In

the second phase, pricing is likely to stay relatively high as the firm attempts to

and life-cycle costing methods are used, as the firm becomes more of a price

taker rather than a price setter.

13-5 At the introduction and into the growth phases, the primary need is for value

chain analysis, to guide the design of products in a cost-efficient manner. Master

budgets (Chapter 10) are also used in these early phases to manage cash flows;

13-6 Value engineering is used in target costing to reduce product cost by analyzing

the tradeoffs between different types and levels of product functionality and total

product cost. There are two common forms of value engineering.

1) Design analysis is a process where the design team prepares several possible

designs of the product, each having similar features but different levels of

product’s life cycle. Value engineering is important in target costing because it

identifies the options for product design that can then be evaluated in terms of

desirability to the customer and manufacturing cost, as a means for coming up

with the best design that satisfies customer needs at the desired target cost.

13-7 Target costing is most appropriate for firms that are in a very competitive

industry, so that the firms in the industry compete simultaneously on price, quality

and product functionality. In very competitive markets such as this, target costing

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-3

13-8 Life-cycle costing considers the entire cost life cycle of the product, and thus

provides a more complete perspective of product costs and product profitability.

13-9 There are five steps in TOC analysis:

Step One: Identify the Constraint

The purpose is to identify the resource that limits production to less than market

demand. Use of a flow diagram may aid in this step.

Step Two: Determine the Most Efficient Utilization of Each Constraint

-focus on throughput rather than efficiency

Step Four: Increase Capacity on the Constrained Resource

This becomes an investment decision: Invest in additional capacity if it will

increase throughput greater than the cost of the investment. Do not move to

throughput.

One could argue that any step could be the most important; for example step one

can be considered to be the most important because the analysis undertaken is

intended to improve the speed of product flow through the constraint.

13-10 TOC emphasizes the improvement of throughput by removing or reducing the

constraints, which are bottlenecks in the production process that slow the rate of

output. These are often identified as processes wherein relatively large amounts

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-4

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

constraint, and chooses the mix of product so as to maximize the profitability of

the product flow through the constraint.

13-11 The purpose of the flow diagram is to assist the management accountant in the

first step of TOC, that is, to identify the constraints.

13-12 Activity-based costing (ABC) is used to assess the profitability of products, just

as is TOC. The difference is that TOC takes a short-term approach to profitability

analysis, while ABC develops a longer-term analysis. The TOC analysis has a

short-term focus because of its emphasis on materials related costs only, while

provides a useful method for improving the short-term profitability of the

manufacturing plant through short-term product mix adjustments and through

attention to production bottlenecks.

13-13 TOC is appropriate for many types of manufacturing, service and not-for-profit

firms. It is most useful where the product or service is prepared or provided in a

sequence of inter-related activities as can be described in a flow diagram such as

13-14 Product design is important in life cycle costing because the design of the

product locks in most of the downstream costs – manufacturing, distribution and

service. A well-designed product will be easy and inexpensive to manufacture,

13-15 Life-cycle costing is most appropriate for firms that have high upstream costs (i.e.

design and development) and/or high downstream costs (i.e. distribution and

service costs). Firms with high upstream and downstream costs need to manage

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-5

13-16 Strategic pricing is used to help a firm develop and implement its strategy for

success as its products and services mature in the market place. The focus for

testing to manufacturing and finally distribution and customer service.

13-17 Takt time is the ratio of available manufacturing time for a period to the units of

customer demand for that period. Each unit must be produced within the Takt

13-18 Pricing based on the cost life cycle is a common form of pricing. It involves a

markup on full product cost or product life cycle cost. In contrast, pricing based

product is currently in.

13-19 Prices are likely to be highest in the introduction phase because costs are

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-6

BRIEF EXERCISES

13-20 Current profit per unit = $50 - $ 38 - $8 = $4 per unit

Target total cost = $45 - $4 = $41

13-24 20 days: May 1 to May 20

13-25 2 days in production (May 19 to May 20) ÷ 20 day cycle time (May 1 to May 20)

= 2 ÷ 20 = .1

such as fuel costs for travel, the economy, weather, etc.

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-7

EXERCISES

13-28 Target Costing (15 min)

1. The unit cost is currently $548.60 = $13,715,000÷ 25,000

The current profit per item is $610 - $548.60 = $61.40

Thus, the target cost to meet the competitive price is:

$550 - $61.40 = $488.60, a reduction of $60 from the current cost.

2. The target cost can probably be achieved by efforts in two areas:

opportunity for cost savings.

c. The remaining manufacturing costs can be considered non-

value adding costs, since they do not add to the functionality or

quality of the product. Efforts can be made to reduce the total cost of

these manufacturing costs, which now total a significant $4,090,000

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-8

13-29. Target Costing; Spreadsheet Application (30 min)

1., 2.

Cost and Activity Usage for Each Product

A-10 A-25 A-10 A25

Direct Materials 143.76$ 66.44$ 78.65$ 42.45$

Number of parts 121 92 110 81

Machine hours 6 4 5 2

Inspecting hours 1 0.6 1 0.5

Packing hours 0.7 0.4 0.7 0.2

Number of setups 2 1 1 1

Activity-based Costs

Rate

Direct Materials 143.76$ 66.44$ 78.65$ 42.45$

Materials Handling 2.25$ 272.25 207.00 247.50 182.25

Mfg Supervision 23.50 141.00 94.00 117.50 47.00

Assembly 2.55 308.55 234.60 280.50 206.55

Number of Setups 44.60 89.20 44.60 44.60 44.60

Inspection and Test 35.00 35.00 21.00 35.00 17.50

Packaging 15.00 10.50 6.00 10.50 3.00

Total 1,000.26$ 673.64$ 814.25$ 543.35$

Price 1,050.00$ 725.00$ 825.00$ 595.00$

Margin 49.74$ 51.36$ 10.75$ 51.65$

Current

Revised

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-29 (continued -1)

3. The solution uses Goal Seek or trials in the Excel sheet. The number of

parts must be reduced to 101 or fewer to get at least $50 margin.

Alternatively, the current activities using parts as a driver are materials

handling and assembly. These costs now total $528.00 ($247.50 +

4. Target costing should be useful to BSI to assist the firm in meeting the

Cost and Activity Usage for Each Product

A-10 A-25 A-10 A-25

Direct Materials 143.76$ 66.44$ 78.65$ 42.45$

Number of parts 121 92 101 81

Machine hours 6 4 5 2

Inspecting time 1 0.6 1 0.5

Packing time 0.7 0.4 0.7 0.2

Set-ups 2 1 1 1

Activity-based Costs

Direct Materials 143.76$ 66.44$ 78.65$ 42.45$

Materials Handling 272.25$ 207.00$ 227.25$ 182.25$

Mfg Supervision 141.00$ 94.00$ 117.50$ 47.00$

Assembly 308.55$ 234.60$ 257.55$ 206.55$

Set-ups 89.20$ 44.60$ 44.60$ 44.60$

Inspection and Test 35.00$ 21.00$ 35.00$ 17.50$

Packaging 10.50$ 6.00$ 10.50$ 3.00$

Total 1,000.26$ 673.64$ 771.05$ 543.35$

Price 1,050.00$ 725.00$ 825.00$ 595.00$

Margin 49.74$ 51.36$ 53.95$ 51.65$

Current

Revised

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-10

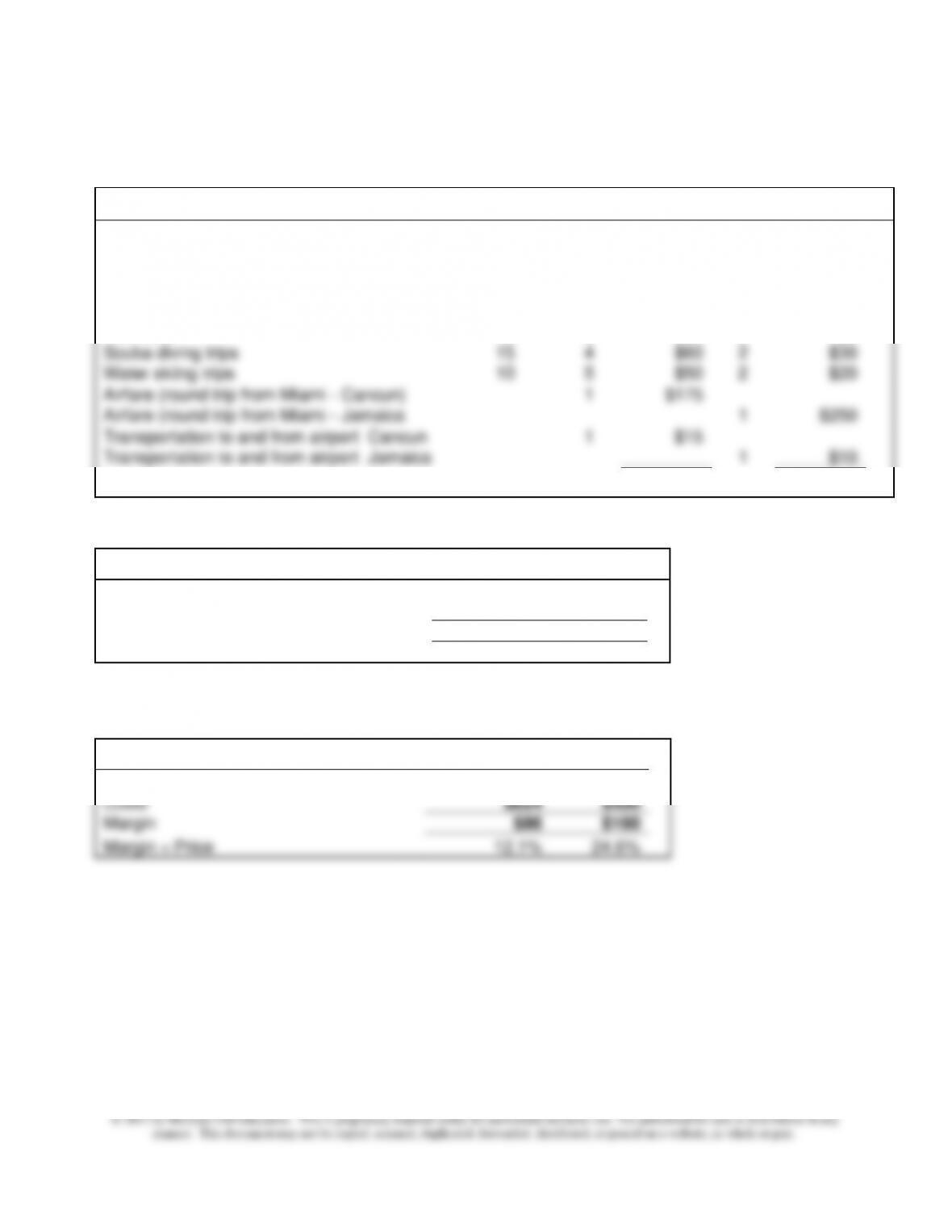

13-30 Target Costing in a Service Firm (20 min)

1.

Package Specifications COST

Unit Cost

Qty

Cancun

Qty

Jamaica

Oceanfront room; number of nights

30

6

$180

4

$120

Meals:

Breakfasts

5

7

$35

5

$25

Lunches

7

7

$49

5

$35

Dinners

10

6

$60

0

$0

Scuba diving trips

15

4

$60

2

$30

Water skiing trips

10

5

$50

2

$20

Airfare (round trip from Miami - Cancun)

1

$175

Airfare (round trip from Miami - Jamaica

1

$250

Transportation to and from airport Cancun

1

$15

Transportation to and from airport Jamaica

1

$10

$624

$490

Package Specification Margins

Cancun

Jamaica

Old Price

$750

$690

Costs

$624

$490

Margin

$126

$200

Margin ÷ Price

16.8%

29.0%

2.

Package Specification Margins

Cancun

Jamaica

New price

$710

$650

Costs

$624

$490

Margin

$86

$160

Margin ÷ Price

12.1%

24.6%

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-11

3. The airfare costs are the largest component of cost and this category

could have room for improvement. By further negotiating group discount

rates or searching for lower cost discount carriers, Take-a-Break could try

lowering its cost in this category, possibly by having the package not

include any per bag fees charged by the airline, letting the purchaser bear

the cost.

Room costs also comprise a major portion of total package costs. While

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-12

13-31 Target Costing Using QFD (20 min)

1. The calculations are shown below:

First: Customer Criteria and Ranking

Importance

Relative

Importance

Taste

45

15.0%

Comfort

95

31.7%

Enjoyment

160

53.3%

Total

300

100.0%

Second: Components and Cost

Components

Cost

% of Total

Menu and food preparation

$8.00

30.8%

Wait staff

$12.00

46.2%

Food ingredients

$6.00

23.1%

$26.00

100.0%

Third: Determine How Components Contribute to Customer Satisfaction

Customer

Criteria

Components

Taste

Comfort

Enjoyment

Menu and food prep

30%

20%

45%

Wait staff

30%

60%

35%

Food ingredients

40%

20%

20%

100%

100%

100%

Fourth& Fifth: Determine Importance Index for Each Component and Compare to Relative Cost

Customer Criteria

Taste

Comfort

Enjoyment

Importance

Relative

Relative importance of criteria

Index

Cost

Ratio

Action

The % contribution of each

15.0%

31.7%

53.3%

component to each customer criterion:

Menu and food prep

30%

20%

45%

34.825%

30.77%

1.13

Spend

more

Wait staff

30%

60%

35%

42.175%

46.15%

0.91

Spend

less

Food ingredients

40%

20%

20%

23.00%

23.08%

1.00

No

action

Total

100%

100%

100%

100%

100%

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-13

2. The cost index for menu and food preparation is low relative to the

importance index, which indicates that Rick should consider spending more

time and cost on this activity. In contrast, the cost index for wait staff is

13-32 Manufacturing Cycle Efficiency (10 min)

MCE = total processing time/total cycle time

Note that new product development time and order taking time are

not considered part of the manufacturing cycle and are excluded from

cycle time.

The level of MCE is best interpreted by reference to the prior MCE

values for the firm or to an industry average. A number closer to one

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-14

13-33 Takt Time (10 min)

1. The Takt time for this product is the number of available hours÷ total

demand.

Total manufacturing time ÷ 8,400

2. The processing line is not properly balanced. Operation 5 exceeds Takt

time by 4 sec. and Operation 2’s time is much less than Takt time. To

balance the line, so that products can be expected to come off the line

every 30 seconds as needed, the capacity of operation 5 should be

3. The strategic role of Takt time is to help operations managers to balance

the operations and to improve the speed of throughput and reduce cycle

Chapter 13 - Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13-15

13-34 Life Cycle Costing; Service Department (20 min)

Life cycle costing can be used in the cost management of the IT

department (or other service departments) over the life cycle of the

department’s assets. This is also called the management of the “total cost

As the strategic goals of the organization change, the focus on different

phases of the IT life cycle can change. For example, when the

organization experiences significant growth, the acquisition of new assets

in phases one and two is accelerated. At other times, the need for

increased focus on user support is important, as the firm faces challenges

in introducing new organizational plans or management structures. The

overall goal of taking a life cycle view of IT is to realize that the total cost of

the service department is made up of significantly different components,

of data or processing capability, and how can these unexpected events be

prevented to reduce the overall cost of IT?