Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–74

15–52 (Continued-2)

efficiency of the customer order-handling process. (Note: this cost might increase a

bit to cover the cost of the TQM initiative.)

Note, however, that the cost of unused capacity increases, from $112,000 (80%

capacity utilization) to $240,000 (57.14% capacity utilization).

Practical Capacity:

Prior to TQM Implementation = 10,000

After TQM Implementation = 14,000

Resource Cost (Handling Customer Orders) = $560,000

Budgeted # of Customer Orders = 8,000

Capacity Utilization:

Prior to TQM Implementation = 80.00%

After TQM Implementation = 57.14%

Conclusion: Efficiency initiatives (e.g., TQM) will lead to reduce resource spending

5. Faced with unused capacity, for example, the company can:

(1) Reduce spending on resources for the support activity in question, or

(2) Find ways to utilize existing, but currently unused, capacity (e.g., new-product

introduction)

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–75

6. Logically, we would assign to a given customer or market segment the cost of

unused capacity IF the associated capacity were acquired specifically to serve that

customer or market segment. IF the unused capacity is associated with a given

product line, then the cost of unused capacity should logically be assigned to that

where the decision to acquire the associated capacity was made.

15–53 Two-Variance Analysis: Service Company Example (30 minutes)

1. Budgeted number of letters of credit approved: $1,000,000 $2,000 = 500

Overhead application rates:

2. Actual overhead costs incurred:

Variable: $2,000 × 600 × 0.75 × 110% = $990,000

Insurance premium 270,000 $1,260,000

Fixed: $560,000 × 95% = 532,000

Total $1,792,000

Flexible-budget: $1,760,000

Overhead applied $3,120 × 600 × 0.75 = $1,404,000

$2,700 ÷ (1 − 0.10) = 300,000 1,704,000

15–76

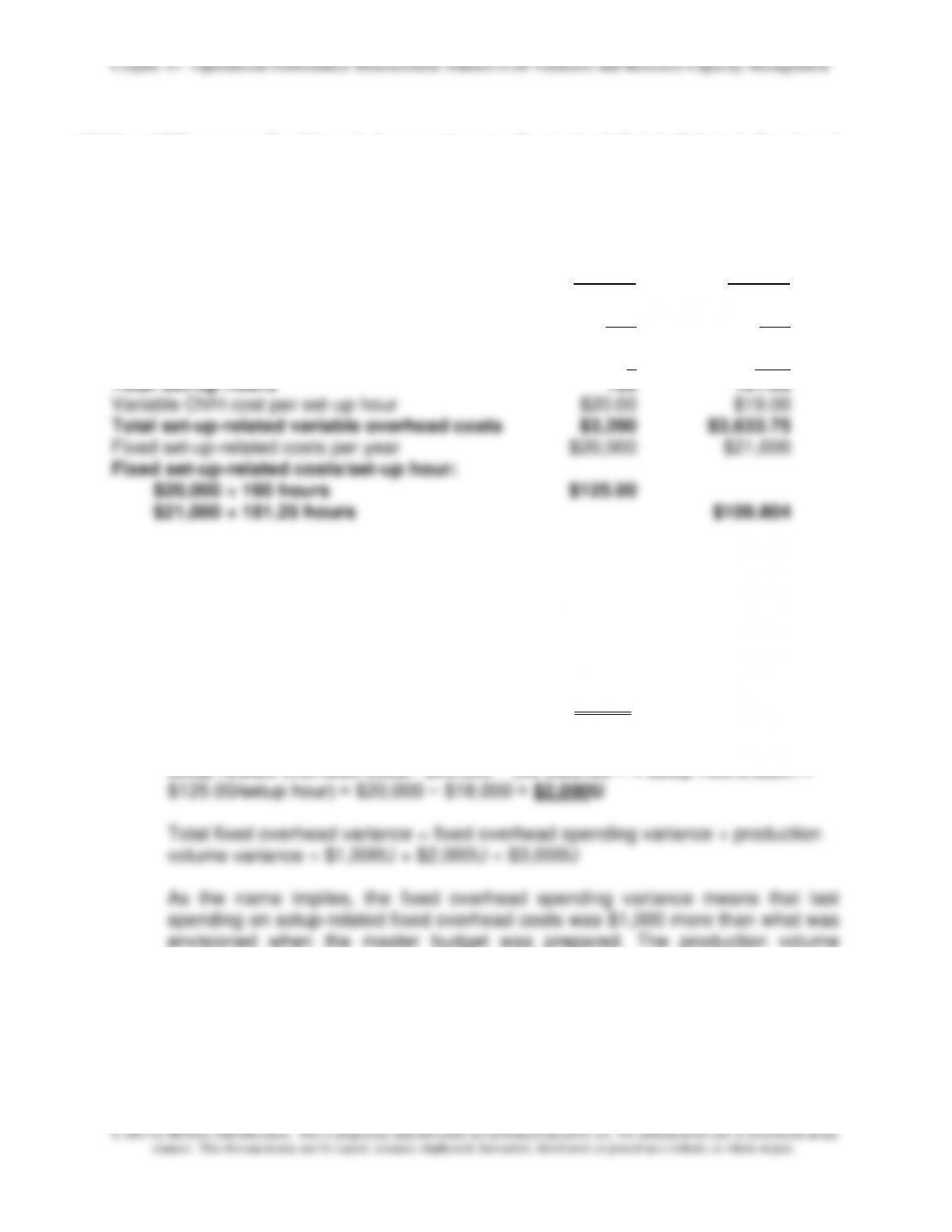

15–54 ABC versus Traditional Approaches to Control of Batch-Related Overhead

Costs (50-60 minutes)

Additional information needed to solve this problem (highlighted in bold):

Budgeted Actual

Results Results

Units produced and sold 10,000 9,000

Batch size (units) 250 200

No. of batches 40 45

Set-up hours per batch 4 4.25

Note that the control (flexible) budget for set–up-related variable overhead costs should

be based in this case on set-up hours (the controllable factor). Thus, given an output

last year of 9,000 units, the company should have used 36 batches (9,000 units ÷ 250

units per batch). At a standard of 4.0 set-up hours per batch, the 9,000 units produced

equates to 144 set-up hours.

(1) (a) Fixed overhead spending variance = Actual fixed setup-related costs – budgeted

fixed setup-related costs = $21,000 − $20,000 = $1,000U

(b) Production volume variance = budgeted fixed setup-related costs – applied fixed

setup-related overhead costs= $20,000 − (36 batches × 4 setup-hours/batch ×

variance in this context means that capacity, measured in terms of budgeted

setup hours, was not fully utilized during the period. Specifically, the standard

allowed setup hours (for this year’s production), 144, was 16 less than capacity

available (160 hours). Thus, $2,000 = 16 hours × $125/hour.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–77

15–54 (Continued-1)

(2) (a) Variable setup-related overhead spending variance = actual variable setup–

related overhead costs − budgeted variable setup-related overhead costs based

on inputs (i.e., based on actual setup hours worked during the year)

= (actual batches × actual setup hours/batch × actual variable setup-related

overhead costs/setup hour) − (actual batches × actual setup hours/batch ×

(b) Variable setup-related overhead efficiency variance = FB for variable setup–

related overhead costs based on Inputs − FB for variable setup-related

overhead costs based on Outputs

= $3,825 − (36 batches × 4 setup-hours/batch × $20.00/setup hour)

variance for variable setup-related overhead costs is due to a combination of the

following two factors: (1) the actual output of the period (9,000 units) took 9 more

batches than standard (actual # of batches = 45; standard allowed batches = 36,

as shown above); and (2) each setup took slightly more time than standard (4.25

hours/setup vs. 4.00 hours/setup). The net unfavorable variable setup-related

overhead variance indicates that the favorable spending variance was not

enough to offset the unfavorable efficiency variance.

(3) Fixed setup-related overhead costs are controlled primarily prior to the point of

operations. That is, they are controlled primarily through the planning process (for

example, the capital budgeting process or the use of zero-based budgeting). These

costs basically relate to the capacity/ability to produce.

On the other hand, variable setup-related costs, by definition, vary in response to

one or more underlying causal factors (cost drivers). Therefore, these costs are

controlled by attempting to identify and eliminate non-value-added activities and to

perform value-added activities more efficiently. ABC systems, because of their

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–78

15–54 (Continued-2)

of these overhead costs are capacity-related and therefore controlled differently,

and (b) fails to identify meaningful strategies for cost control. When machine hours

are used as the basis for cost allocation and some costs (as in this case) are not

related to machine hours, then the variable overhead spending variance based on

machine hours will include the effect of spending on these other activities—in other

(4) Most companies find that a comprehensive control system consists of both financial

and nonfinancial performance indicators. Thus, one would expect that operating

units in the Bangor Manufacturing Company would have timely access to

nonfinancial performance indicators such as process yields (e.g., ratio of good

outputs to inputs), manufacturing processing time, reject rates, percent first-pass

yield, defect rates (e.g., parts-per-million, ppm), etc. Such information has the

advantage of being expressed in a manner that is readily interpretable by operating

personnel. As well, these data direct worker attention to actionable steps when a

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–79

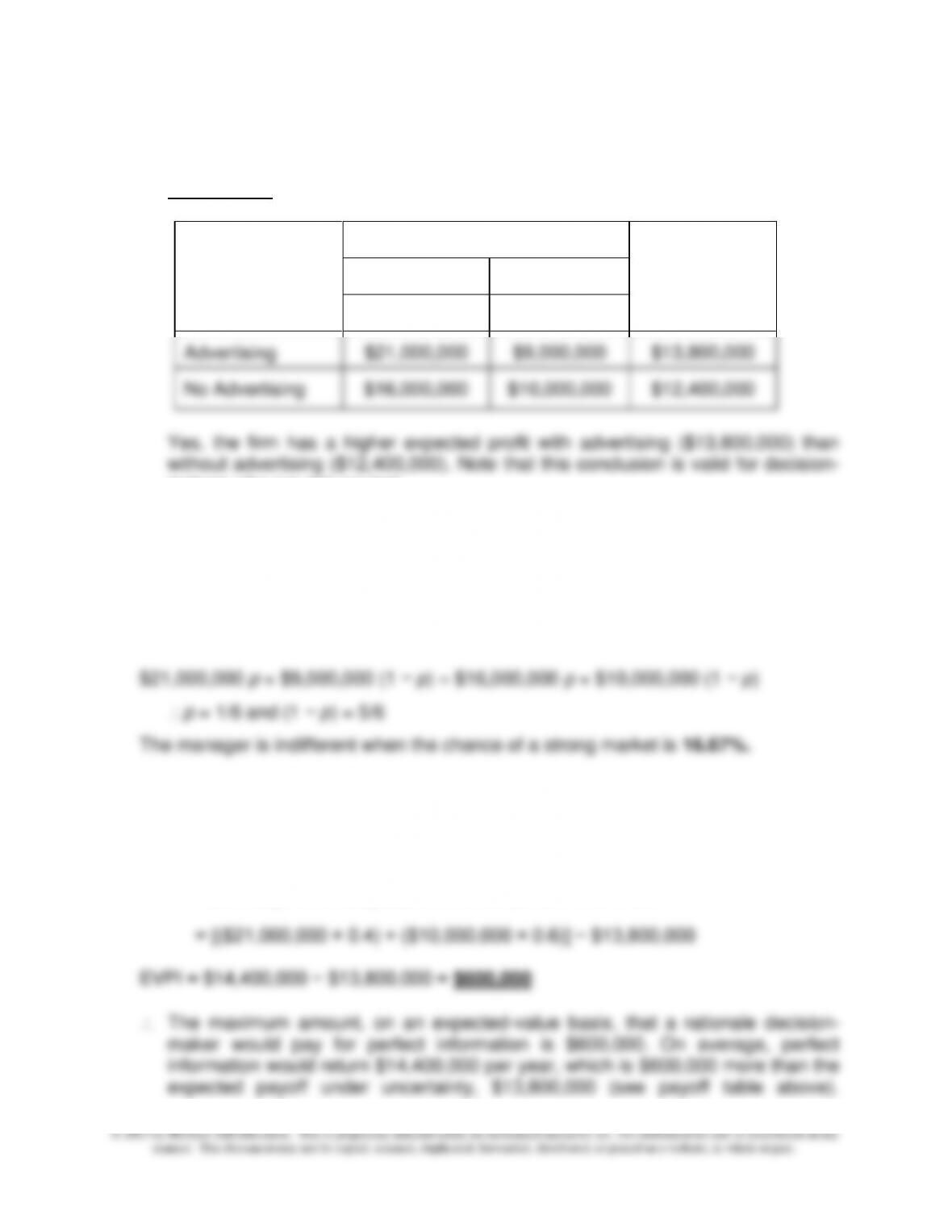

15–55 Decision-Making under Uncertainty (Appendix) (30-40 minutes)

1. Payoff Table

Possible

Courses of

Action

State of the Market

Expected

Value of Each

Action

Strong

Weak

Prob. = 0.4

Prob. = 0.6

Advertising

$21,000,000

$9,000,000

$13,800,000

No Advertising

$16,000,000

$10,000,000

$12,400,000

Yes, the firm has a higher expected profit with advertising ($13,800,000) than

without advertising ($12,400,000). Note that this conclusion is valid for decision–

makers who are risk-neutral.

2. Let p be the probability that the market is strong; thus, the probability that the market

is weak is 1 − p.

At the indifference point:

E(Advertising) = E(No Advertising)

3. The Expected Value of Perfect Information (EVPI) = maximum value the manager

would pay to have knowledge (i.e., certainty) of the revealed state of nature.

EVPI = Expected (i.e., long-run average) profit with perfect information − expected

(i.e., long-run average) profit without perfect information

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–80

15–56 Variance Investigation under Uncertainty (Appendix) (30-40 minutes)

1. Payoff Table

Courses of Action

States of Nature

In-Control

Out-of-Control

(1 − p) = 0.75

p = 0.25

Investigate

$20,000

$20,000 + $60,000

Don’t Investigate

$0

$240,000

2. Expected cost of conducting:

manager should conduct an investigation: the expected cost of not making an

investigation > expected cost of conducting an investigation.

3. The Expected Value of Perfect Information (EVPI) = maximum value the manager

would pay to have knowledge (i.e., certainty) of whether the process is in control or

out of control. In this decision context, the EVPI can be thought of as the difference

between the expected cost with perfect information and the expected cost without

perfect information. (To calculate the former, we need to choose for each possible

state of nature the best course of action [decision] and then multiply the associated

“cost” by the probability of that state of nature occurring. We then sum these resulting

expected costs to get the expected cost with perfect information.)

EVPI = expected (average) cost with perfect information − expected cost without

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–81

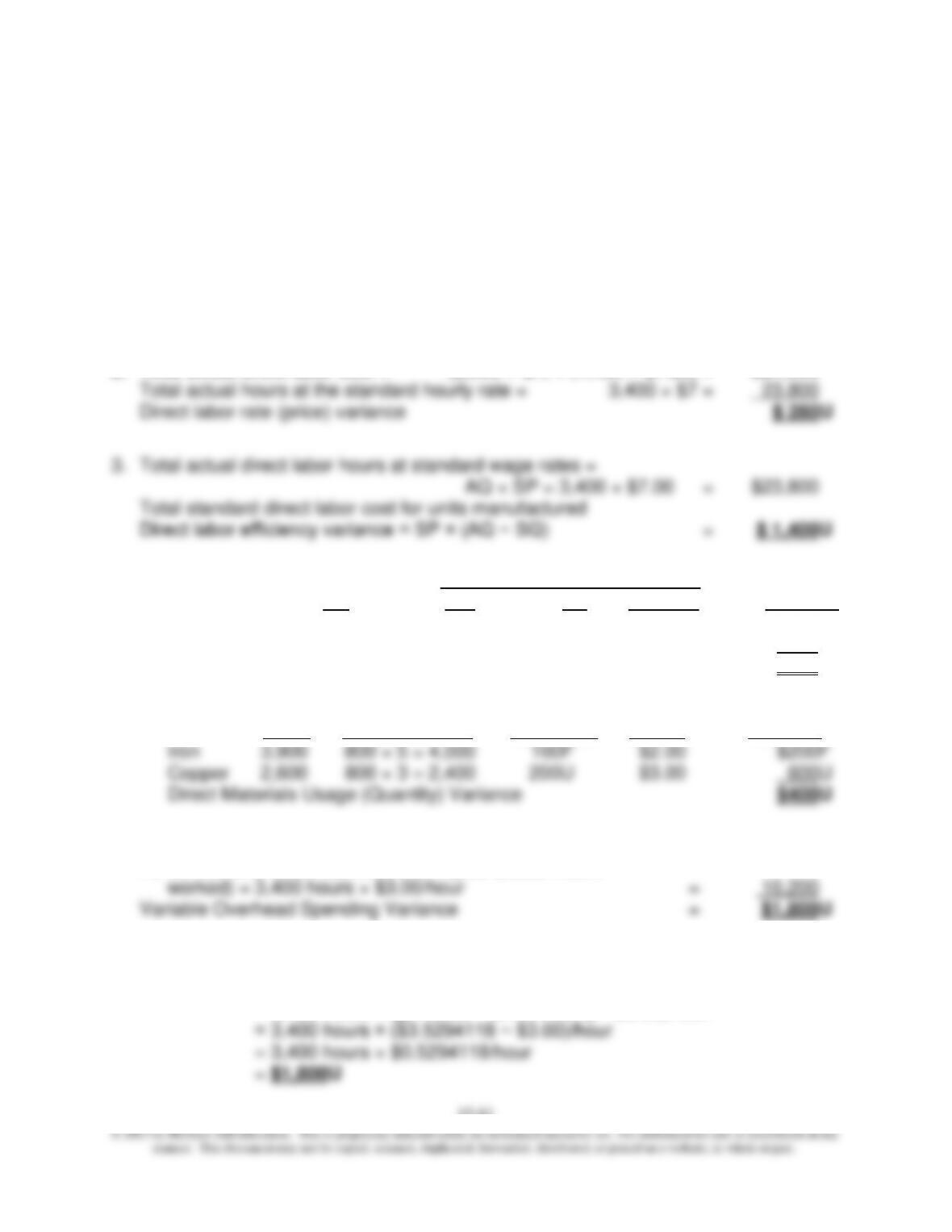

15–57 All Manufacturing Variances (50–60 minutes)

1. At the time of purchase. Recording the price variance for materials at time of

purchase recognizes the variance at the point it occurs. Further, if the organization in

question uses a standard cost system, then this practice results in the materials

inventory being carried at standard cost, which is consistent with the way WIP

Inventory and Finished Goods Inventory are carried. Finally, recognizing the price

variance at point of purchase provides management with timely information that,

presumably, can be used to correct any problems that arise.

2. Total actual direct labor cost = (2,000 × $7) + (1,400 × $7.20) = $24,080

4. Price Price

AQ AP SP AP − SP Variance

Iron 5,000 $2 $2 – 0 – – 0 –

Copper 2,200 $3.10 $3 $0.10 $220

Direct Materials purchase price variance $220U

5. Usage

AQ SQ (AQ − SQ) SP Variance

6. Actual variable overhead (given) = $12,000

FB for Variable Overhead based on Inputs (actual hours

Alternative formula for variable overhead spending variance:

Variance = AQ × (AP − SP)

= 3,400 hours × ([$12,000 ÷ 3,400 hours] − $3.00)/hour

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–82

15–57 (Continued)

7. FB for Variable Overhead based on Inputs (i.e., based on actual

hours worked—see 6 above) = $10,200

Total standard variable overhead applied for units

8. Actual fixed overhead (given) $8,800

9. Budgeted fixed overhead (see 8 above) $8,000

Fixed overhead applied to units manufactured

Variance = SP × (Denominator volume − Actual Units Produced)

= $8.00/unit × (1,000 units − 800 units) = $1,600U

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–83

Check Figures

15–24 1. At 4,000 machine hours, budgeted variable overhead = $84,000; budgeted fixed

overhead = $65,500; at 5,000 machine hours, budgeted variable overhead =

$105,000; budgeted fixed overhead = $65,500. 2. Estimated variable overhead

volume variance = $3,600U

15–34 1. Total flexible budget (controllable) variance = $3,200U; production volume

variance = $3,600U 2. Flexible budget variance = $3,200U; production volume

variance = $3,600U

$15,000F; Production Volume Variance = $18,000F.

15–38 1. Total overhead spending variance = $24,200U; Total Overhead Efficiency

Variance = $23,800U. 2. Total overhead spending variance = $32,200U; Total

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–84

overhead efficiency variance = $19,800U. 3. Total overhead spending variance =

$14,000U; Total overhead efficiency variance = $38,000U.

15–39 1. Budgeted cost per unit, S-101= $7.1535; C-110 = $10.11.61. 2. Allocated

$52,263 (Budgeted Capacity).

15–44 No check figure.

15–45 No check figure.

15–46 No check figure.

15–47 1a. 396,000; 1b. $33,000U; 1c. $22,000U; 1d. $25,000F; 1e. $594,000; 1f.

$6,000U.

TQM initiative = 57.14%.

15–53 1. Budgeted overhead application rates: variable overhead = $2,000/letter of credit

(given) + 1% of the amount of credit issued; fixed overhead = $1,120/letter of credit

issued. 2a. Total Overhead Controllable (Flexible-Budget) Variance = $32,000U;

2b. Overhead volume variance = $56,000U.

Chapter 15 – Operational Performance Measurement: Indirect-Cost Variances and Resource-Capacity Management

15–85

15–55 1. E(Advertising) = $13,800,000; E(No Advertising) = $12,400,000. 2. Indifference

probability = 16.67%. 3. EVPI = $600,000.

15–56 1. Payoffs: Investigate an in-control process = $20,000; Investigate an out-of–