Chapter 3 – Basic Cost Management Concepts

3-1

Chapter 3

Basic Cost Management Concepts

Teaching Notes for Cases

3-1. Strategy; Critical Success Factors, Cost Objects, and Performance Measures

Increasingly, students in accounting and business courses are expected to actively engage in give and

take with the instructor and other students and to integrate new knowledge with old. The objective of

this teaching case is to assist instructors of management accounting to promote such interactive and

integrative learning and to increase students’ mastery of basic cost terms and concepts.

This case reduces psychological and technical barriers to student participation by (1) using a

small business with which students are likely to be familiar, and by (2) keeping technical details to a

minimum. The case is simple enough so that it can be presented verbally in the first class meeting

without students having read it before hand. (The discussion questions are listed as a group to facilitate

use by instructors who wish to assign the case ahead of time.) Invariably, the students have responded

with active and broad-based participation.

The case has enough facets to support an active, 100-minute class session or two 50-minute

sessions. The time requirement can be decreased or increased by using more or less-focused questions.

The type of business used in the example also can easily be changed to one that is more common in the

local environment, for example, a taco shop.

The first two questions are aimed at getting the students to view the situation from a manager’s

(as opposed to accountant’s ) perspective:

1. What is the competitive strategy of Vincent’s business?

While the case information is very brief, a preliminary assessment of competitive strategy is possible.

Most likely, the firm has succeeded at least initially by its unique product offering in combination with its

desirable location. This would imply a focus or differentiation strategy; Vincent succeeds by offering

2. What are the critical success factors of The Cappuccino Express?

Students typically have no difficulty coming up with a rather long list of critical success factors, including

location, the price that The Cappuccino Express charges per cup, the cost of coffee beans, the extent of

ease with which they can make their purchases.

You can close this part of the discussion after putting up six to eight of the students’ suggested factors.

Then summarize the discussion by noting that some of these factors, such as location and pricing, are

Chapter 3 – Basic Cost Management Concepts

3-2

impending threats and opportunities and to align the factors within his control to respond to these factors.

3. What major tasks does Vincent have to undertake in managing The Cappuccino

Express?

This question starts to focus attention on the factors within the firm manager’s control. The following

items are among the most often suggested:

a) Evaluating whether he should stay in business (that is, whether the business is sufficiently

profitable)

b) Evaluating each site to make sure that it continues to be profitable

h) Maintaining service and product quality

After putting up six to eight items, ask the class to assume that the list on the board is all-

inclusive. If the students had not suggested monitoring and motivating of each site manager as one of the

tasks, guide them in this direction by asking: “If you were Vincent, would you make all of these

service and product quality. Based on these suggestions, the monitoring and motivating of each site

manager can easily be added to the list.

The next question follows logically from the preceding discussion:

4. What are the major operating costs that need to be incurred?

The students’ responses will vary across class sections, as will the way that they label some cost items.

Nevertheless, the suggested list generally includes the following items:

a) Vincent’s assistant’s salary

b) Rent at each site

c) Business license for each site

i) Cost of coffee beans

j) Cost of supplies

Sometimes the students correctly include Vincent’s forgone salary as a cost of The Cappuccino

Chapter 3 – Basic Cost Management Concepts

3-3

operating The Cappuccino Express. This discussion helps the students to appreciate the nature and

relevance of opportunity costs.

Also, you can ask: “Do you think that running one’s own business is the same as working for

someone else?” The students usually suggest differences such as the greater satisfaction from being one’s

relevant. Letting the students develop these points helps them appreciate the need for managerial

information systems which go beyond simply following a set of rules developed for a different purpose

(e.g. generally accepted accounting principles for external reporting).

The next question moves the discussion to yet another level of detail:

5. Vincent would like to monitor the performance of each site manager. What measure, or measures, of

performance should he use?

An item that always comes up early is the site’s profitability. When this measure is first

suggested, briefly discuss the need to differentiate between the performance of the site and that of its

manager. Students readily accept that while each site’s profitability is likely to be affected by factors that

or inexperienced employees, and that lower customer satisfaction will likely lead to lower future sales.

Related to measuring customer satisfaction, their suggestions may range from conducting surveys to

giving out discount coupons for repeat purchases and then counting the number of such coupons

redeemed.

Two points emerge from this discussion. The first is that accounting numbers often lag other

measures in reflecting some aspects of operating conditions. Thus, while customer dissatisfaction and

only a subset of the information needed for effective management. It is important to collect and consider

nonfinancial data, some of which are not easily quantified (e.g. customers’ written feedback on comment

forms).

After developing these two points, bring the focus back to accounting data by asking:

6. If you had suggested more than one measure to measure the performance of each

Site manager, which of these should Vincent select if he could use only one?

The students will likely select profitability. At this point, put up the simple profit formula:

Profit = Total revenues minus total costs

And ask whether it would be difficult to determine the total revenues from each site. The answer

is obviously “no” since the two sites are operated independently. Thus, the focus quickly shifts to

Chapter 3 – Basic Cost Management Concepts

3-4

determining each site’s costs. Returning to the list of costs already on the board, I ask the students to

identify those costs that can be readily traced to each site. The students will agree that many items, such

class to assume that such costs are relatively small for The Cappuccino Express; therefore, Vincent has

decided to only consider each site’s total revenues and direct costs. Also tell the students that since The

Cappuccino Express advertises only in each site’s neighborhood newspaper, advertising expenses are

substantially traceable to each site.

Then ask how the typical accounting system would treat each site’s advertising expenses. The

asset, it is useful to briefly consider how Vincent might decide on the expense and asset components.

You might conclude this discussion by noting that the choice is between being precisely wrong (i.e.,

expensing the entire advertising expenditures) and being only approximately right.

The treatment of advertising expenses also can be used to introduce another important role of

accounting data. Ask the students: “Suppose that you were manager of the original site and that your

3-5

3-2. Cost Drivers; Strategy

Joe’s business competes on the basis of differentiation, the unique organic and specialty foods he

provides. The differentiation strategy requires attention to customer issues, changing tastes and

preferences. Joe needs a cost management system which will inform him promptly of changes in

customer preferences. A balanced scorecard might be useful⎯to outline the specific goals in each of the

key areas; financial, operating, customers, and employees. Since the chain is growing, the financial

factors are important, particularly attention to cash flow to manage cash flow so that the firm is able to

pay its bills in a timely manner. Cash flow problems are common for growing firms. Joe would also

watch the financial section of his balanced scorecard to assess his company’s progress in increasing

revenues and earnings. Are the trends for these financial factors meeting his expectations?

The key cost drivers would also appear in the financial section of the scorecard. Students will

have a number of different ideas here. The key cost drives are likely to include, among others:

• ability to accurately forecast customer demand, so that food products are not wasted or spoiled

• manage the cost of purchases by appropriate contracting with key suppliers

In the operations area, Joe uses the balanced scorecard to measure important operating variables,

such as those which measure the freshness and quality of his produce and meat department products.

Since his stores compete on differentiation, these quality-related factors will be critical success factors for

him.

The customer section of the balanced scorecard is likely to be the most important of the

scorecard, because of the differentiation strategy. In this section, Joe keeps track of changing customer

tastes by sampling customers, by survey, and by carefully logging customer requests and complaints. Joe

Chapter 3 – Basic Cost Management Concepts

3-6

3-3. Virtues in Conflict

This case involves a classic conflict of ethical principles, also called “virtues.” On the one hand, the CFO

is responsible to the bank. They value her integrity, honesty, and diligence. On the other hand, she has

compassion and cares for the company’s 300 employees and their families. She has worked hard to

become an effective member of the upper management team and now sees the potential for losing the

teamwork relationship she enjoys. Her objectivity is eroding.

These competing virtues of compassion, teamwork, honesty, responsibility, and objectivity cause

tension. When teaching ethical decision making, it is important to focus on the underlying virtues

required to make the decision. Students who understand and desire to model virtues are able to analyze

ethics cases more effectively. By using the term “virtues,” the intent is to convey the positive character

traits that bring about ethical decisions. Examples of virtues included in IMA’s Statement of Ethical

Professional Practice are honesty, fairness, objectivity, and responsibility. IMA describes these as

“overarching ethical principles.”

This case involves budgeting and revenue recognition for long-term contracts. Appropriate

settings for this case include:

1. A college-level intermediate accounting course

The optimum result of this case analysis is to have students put themselves in the place of the

CFO. Their study of accounting for the construction industry, and other industries with long-term

projects, should lead them to understand that the CFO has substantial flexibility when recognizing

revenue for projects-in-process. Ideally, they will sift through the competing virtues and suggest a

decision of which they are personally proud.

First, encourage your students to think of the relevant accounting standards and ethical guidelines

for solving this case. Have them describe the competing virtues.

Second, ask them to specifically address the overarching ethical principles as defined by IMA in

credibility in that the CFO must deal with fair and objective communication of information, disclosure of

relevant information, and whether a delay of information would be appropriate.

Finally, since there is no formal organizational policy for resolving ethical conflict, you may also

prompt your students to create a course of action that is recommended by the IMA in the Statement of

Ethical Professional Practice.

Chapter 3 – Basic Cost Management Concepts

3-7

Structured questions for the case write-up include:

1. Does Sarah have all of the facts? What accounting standards and ethical guidelines are

available to her?

2. Why does she feel pressured? How do the virtues compete to make this decision

difficult?

3. What are her alternatives and the consequences?

4. What do the rules say? Specifically research and address IMA’s Statement of Ethical

Professional Practice as a guide to your answer.

5. Which overarching virtues are most important in this decision?

6. What are the possible steps to resolve the problem?

Chapter 3 – Basic Cost Management Concepts

3-8

Teaching Strategies For Readings

3-1 “Managing Costs Through Complexity Reduction at Carrier Corporation,”

This article, based on the experience of Carrier Corporation, a United Technologies company, and one of

the world’s largest manufacturers of heating and air conditioning products, explains how product

complexity is a key driver of total costs. The article also explains how product complexity can be

measured and some techniques for reducing complexity.

Discussion Questions:

1. Why does product complexity lead to increased costs?

Complexity is a key cost driver because is slows the manufacturing process, increases inspection and

2. Explain 3-4 useful measures of product complexity.

• number of products

• number of components in the product

See also Table 1 in the article.

3. Identify and explain 2-3 techniques for reducing product complexity and cost.

• product standardization

• careful engineering and design to reduce cost and simplify the manufacturing process

• outsourcing

scorecard

The article goes into greater detail on each of these.

Chapter 3 – Basic Cost Management Concepts

3-9

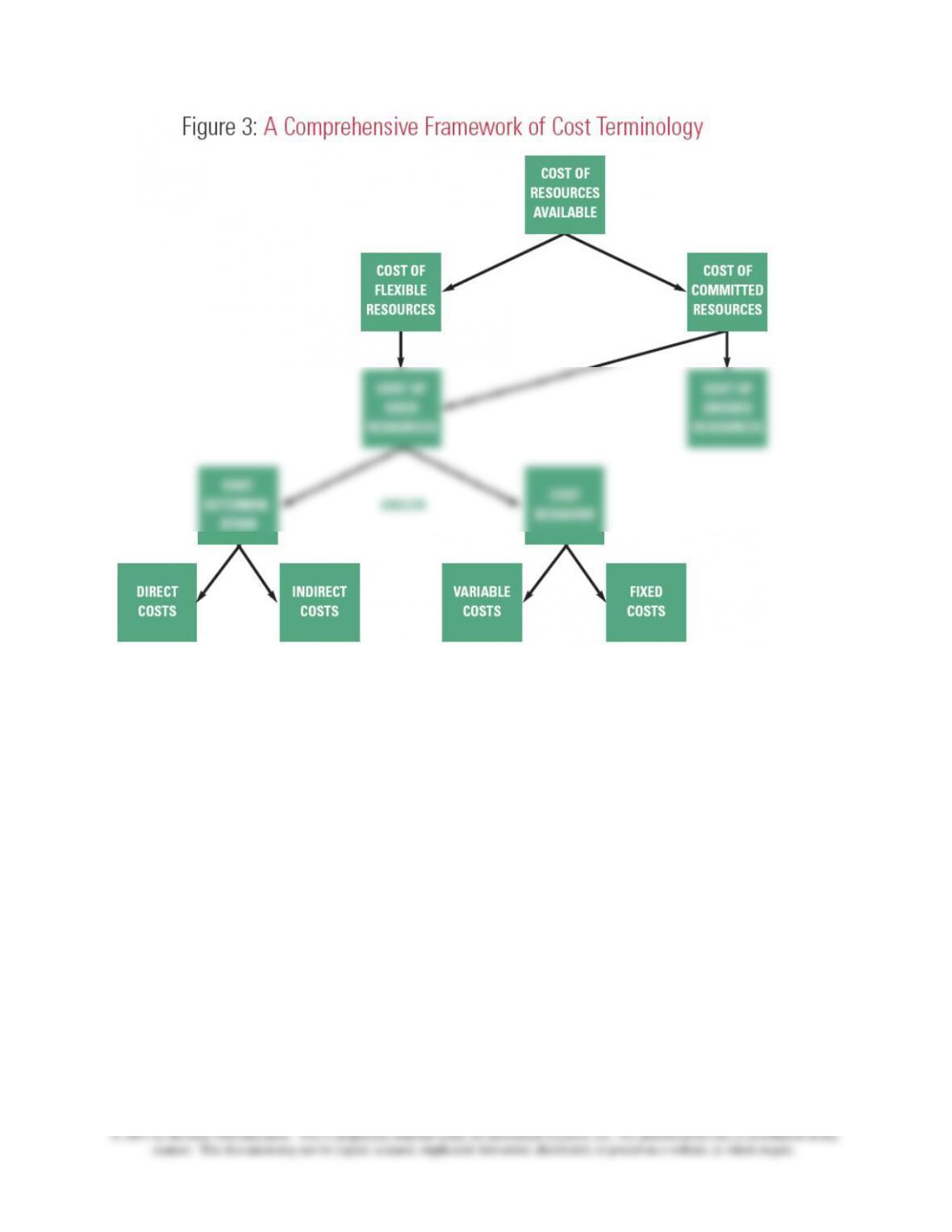

3-2: “Using Direct Labor Cost in a Cost vs. Resources Framework” by Parvez Sopariwala

This article explains the traditional approach to usage of cost terms and proposed a new approach

based on the concept of distinguishing the use of resources, cost of resources, and capacity of

resources available.

Discussion Questions:

1. What are the key cost categories in the traditional view?

The traditional cost categories are:

relevant (or avoidable) or irrelevant (or not avoidable)

2. Why is it important to distinguish flexible and committed resources?

The importance of this distinction is that for short term decision making the committed

resources must be considered sunk costs, while the flexible resources are relevant.

idle time on that activity unless the resource is flexible and capacity can be reduced.

3. Explain the relationship between the costs of flexible and committed resources, usage of

resources, cost behavior, and cost determination.

Chapter 3 – Basic Cost Management Concepts

3-10