Chapter 17 – The Management and Control of Quality

17–74

some public information available on its efforts to address global warming.

17–58 (Continued-2)

4. As indicated in the referenced HBR piece (October 2007, pp. 30, 34), companies that

have sub-par performance in the environmental area face potential risks for four

reasons:

a) Reputation risk

backlashes)

5. Role of the management accountant: environmental performance, as evidenced by

the corporate-performance scorecard used by Climate Counts, fundamentally

involves measurement, reporting, and analysis. Presumably, the management

accountant has a competitive advantage in these areas and, therefore, should be

able to add value to the organization by participating in the design of a

comprehensive management accounting and control system—one that includes

Chapter 17 – The Management and Control of Quality

17–75

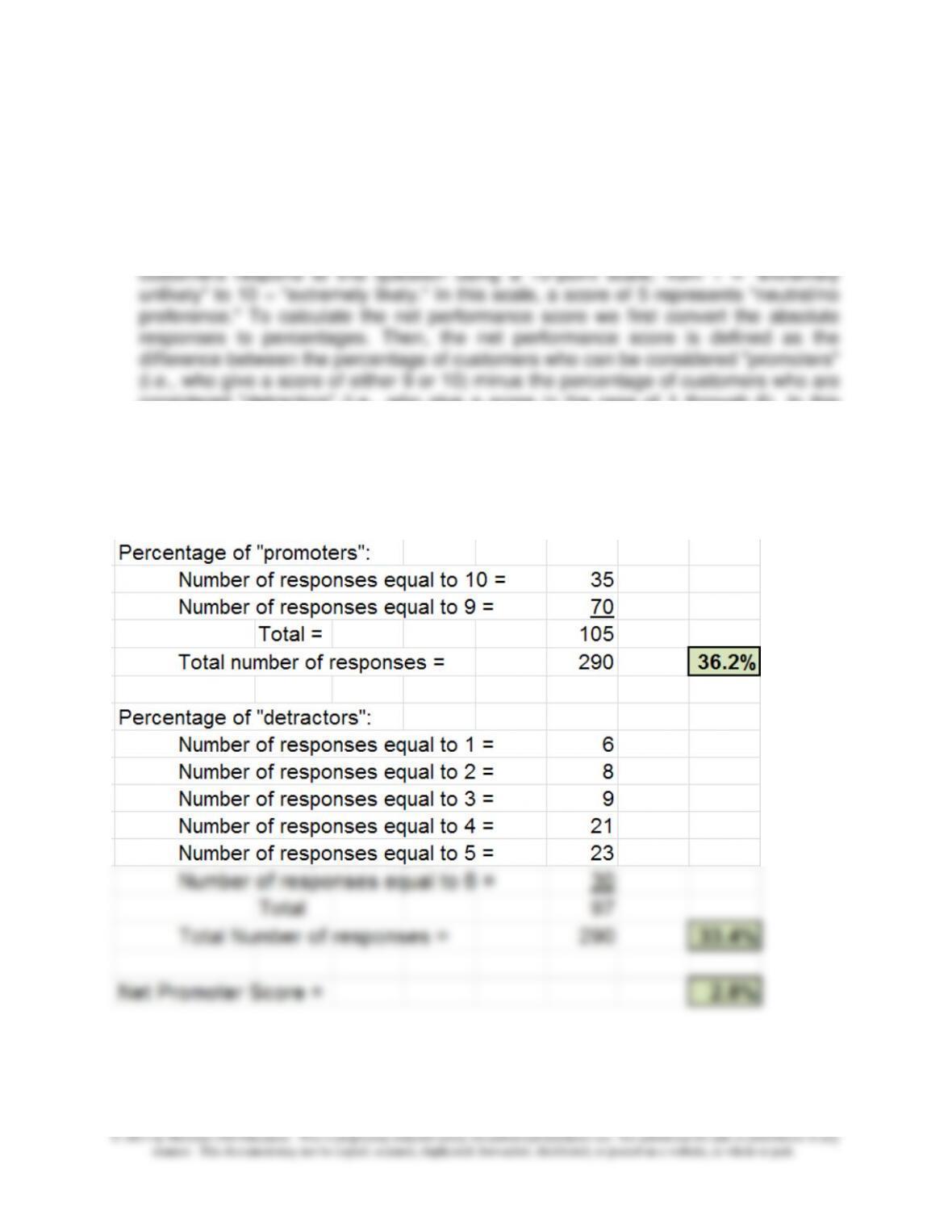

17–59 Net Promoter Score (30 minutes)

1. The “net promoter score” is an example of a non-financial customer-related

performance indicator. It is calculated based on responses to the following question

posed to an organization’s customers: “How likely is it that you would recommend

our firm/company to a friend or to a colleague?” As indicated in this exercise,

considered “detractors” (i.e., who give a score in the rage of 1 through 6). In this

calculation, scores of 7 and 8 are ignored—these are assumed not to provide

information regarding customer loyalty.

2. Net promoter score based on the assumed data/customer responses is 2.8%, as

follows:

Chapter 17 – The Management and Control of Quality

17–76

17–59 (Continued)

3. The net promoter score is recommended as a nonfinancial customer-related

performance measure based on research that indicates that a customer’s

willingness to recommend a company is positively correlated with future growth and

profitability of the company. The net promoter score can be viewed as a measure of

customer loyalty. The underlying argument is that a traditional measure of customer

loyalty, customer retention, is not a good indicator of a customer’s loyalty. This is

because customers may remain as a customer either because there are no

loyalty.

The basic argument regarding the strategic importance of non-financial

performance indicators is best embodied in a comprehensive strategic

management system, such as the Balanced Scorecard (BSC). While it is true that

managing customer relationships requires financial performance indicators (e.g.,

from ABC systems), it is also true that such measures are incomplete. For one

thing, financial indicators are lagging indicators of performance. For another,

operating personnel and marketing personnel many times find non-financial

performance indicators more informative than financial indicators. Finally, non–

financial performance indicators, including customer-related metrics, provide

guidance for improving operations, processes, customer relationships, etc.—

information that is unavailable with financial performance indicators.

Source Documents for the Net Promoter Score:

1. F. Reichheld, The Ultimate Question: Driving Good Profits and True Growth (Boston,

MA: Harvard Business Press, 2008).

2. F. Reichheld, “The One Number You Need to Grow,” Harvard Business Review

(December 2003), pp. 46-54.

Chapter 17 – The Management and Control of Quality

17–77

17–60 Expected Quality Cost, Confidence Intervals, and Sample Size (45-60 Minutes—

requires some material from Chapter 8: Cost Estimation)

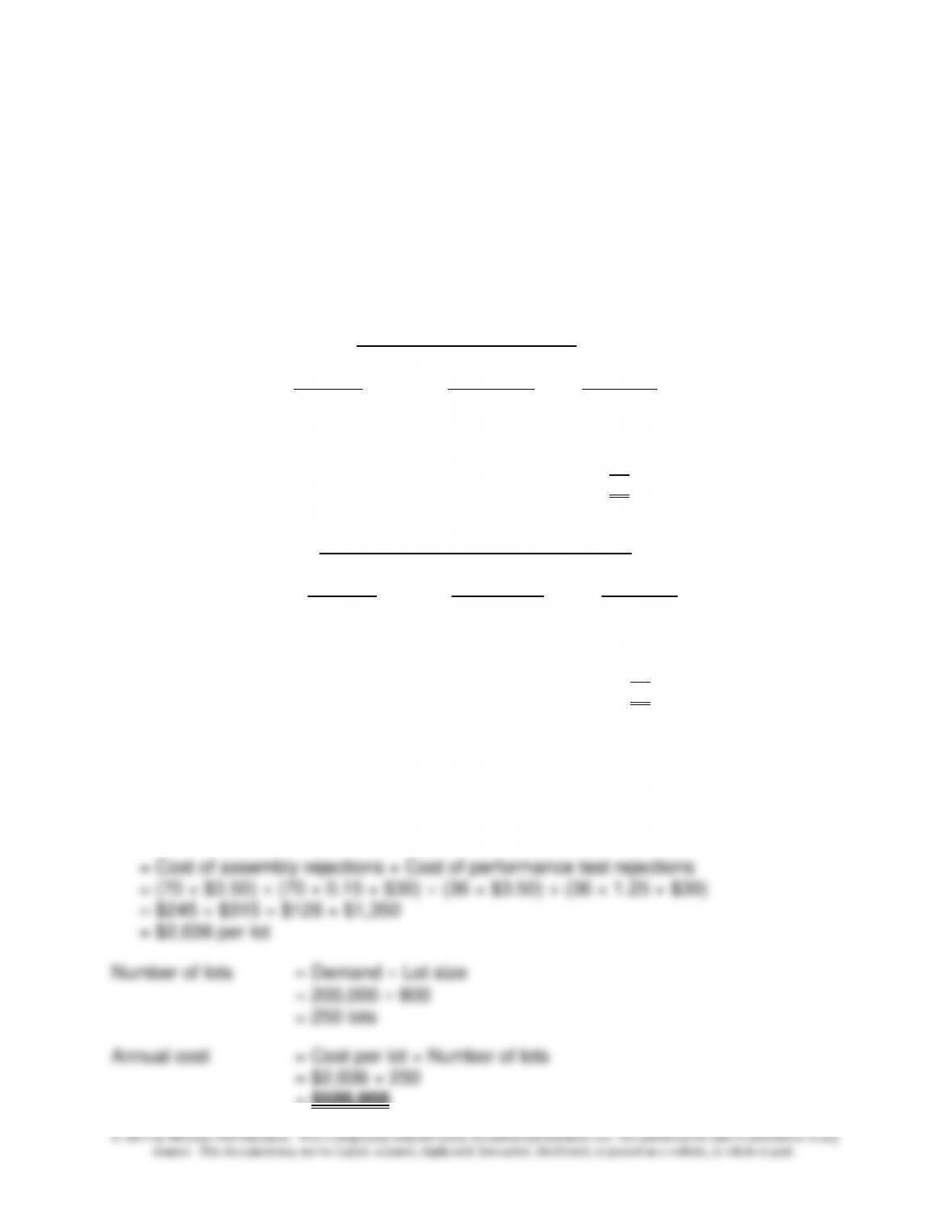

1. Paragon Manufacturing would be willing to spend $509,000 annually to implement

quality control inspection of the housings before assembly begins. This amount is

equal to the expected cost of rejections and repairs without quality control

inspection, calculated as follows.

Expected Value of Housings

Rejected During Assembly

(1) (2) (1) × (2)

Quantity Probability Outcome

90 0.40 36

70 0.30 21

50 0.20 10

30 0.10 3

70

Expected Value of Housings

Rejected During Performance Testing

(1) (2) (1) × (2)

Quantity Probability Outcome

50 0.50 25

40 0.15 6

20 0.15 3

10 0.20 2

36

Cost/direct labor hour = $12.00 + 18.00 = $30.00 per hour

Cost of repair material = $7.00 × 0.5 = $3.50 per housing

Rejection/repair cost per production lot

= $509,000

17–78

17–60 (Continued)

2. The sample size that Ross Webster should select from a lot of 800 housings is 265

units, calculated as follows:

nc = [(2.00)2 × (0.01) × (0.99)] ÷ (0.01)2

= 0.0396 0.0001

= 396

3. a. Two defective housings in a sample of 240 is a 0.0083 rejection (error)

Chapter 17 – The Management and Control of Quality

17–79

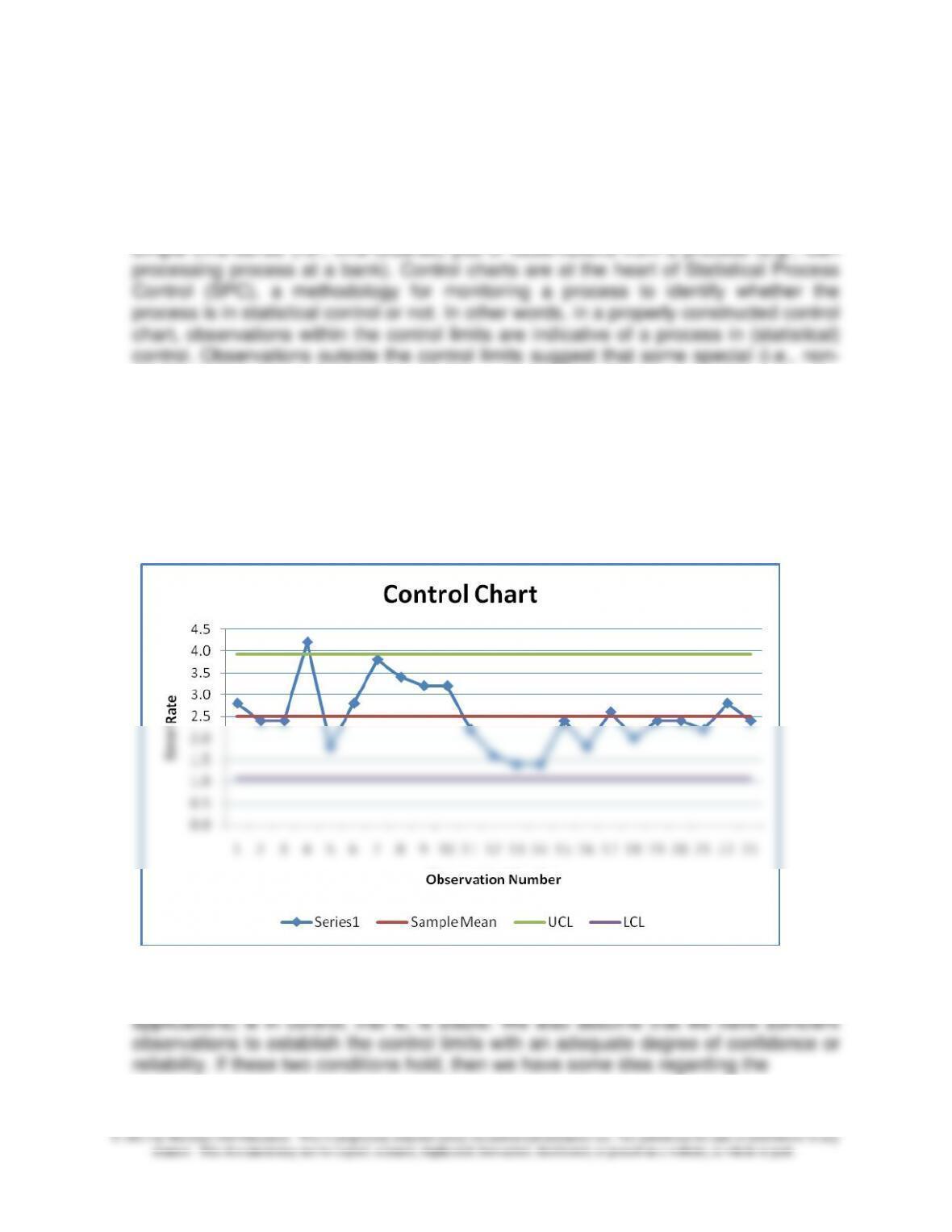

17–61 Constructing and Interpreting a Control Chart (45-60 Minutes)

1. A “control chart” might best be thought of as a time-series run chart with statistically

determined upper and lower control limits, around a target value (usually defined as

the mean value of the characteristic under examination). By contrast, a run chart is a

random) factor is at work.

2. Construction of Control Chart:

Sample mean of process = 2.50

Sample standard deviation = 0.72

No. of standard deviations = 2

Upper-Control Limit (UCL) = 3.94 (i.e., 2.50 + [2.0 × 0.72])

Lower-Control Limit (LCL) = 1.07 (i.e., 2.50 − [2.0 × 0.72])

3. Interpretation of control limits: we assume that the sample observations were

obtained during the time that the underlying process (in this case, processing of loan

Chapter 17 – The Management and Control of Quality

17–80

“normal” or inherent variation of the process we are observing. We know that any

process is subject to variation over time. Our goal in constructing the Control Chart is

to develop a tool that will provide an indication of when, going forward, the process is

likely in or out of statistical control. Because we are working with some uncertainty,

control limit, there is very little chance that random causes are at work. That is, there

is a greater chance that something about the process might be awry.

4. As indicated above in (3), the basic approach to judging process control is statistical

in nature. That is, on the basis of whether or not actual observations fall within the

control limits we draw a conclusion as to whether the process is in control (i.e., the

variations we are observing have random, or non-systematic, causes) or out-of–

control. This approach is sometimes referred to as the “outlier” approach to

interpreting results from a Control Chart.

Another approach would be to look for what appear to be an abnormal number of

runs. The likelihood of a stable process generating, say, eight points in a row on the

same side of the centerline is like tossing a coin and getting “tails” eight times in a

explain the trend may be desirable.

Finally, we might look for cycles, or repeating patterns of observations. Again, rules–

of-thumb might be useful. We might, for example, look at 14 or 15 data points to see

whether these points alternate in an “up” and “down” fashion. Such repeating results

(cycles) might reflect shift–to-shift or operator-to-operator or machine–to-machine

variation.

5. Some plausible quality measures for non-manufacturing companies:

a) Hospitals—lab test accuracy, insurance claim accuracy, on-time delivery of meals

and medications

Chapter 17 – The Management and Control of Quality

17–81

17–61 (Continued)

d) Police Department—incidence of crime in the precinct, number of traffic violations

17–62 Research: Applying Lean Principles to “Knowledge Work” (60 minutes,

including reading time)

1. The term “lean,” as derived from the Toyota Production System, can be taken to

mean “relentless attention to detail, commitment to data-driven experimentation, and

charging employees with the ongoing task of increasing efficiency and eliminating waste

2. The term “knowledge work” is used by the authors of this article to mean any decision

process (or operation) that involves judgment and expertise (so–called “tacit

knowledge”—that is, knowledge “locked inside the worker’s head). Unlike many

manufacturing contexts (in which work processes can more or less be defined

unambiguously and therefore modeled), conventional wisdom holds that “knowledge–

principles.

3. Perhaps the most significant assertion is stated at the very end of the article (p. 110):

turning a knowledge operation into a lean system is difficult, but possible; this very

difficulty implies that the system will be hard for competitors to replicate. In other words,

similar to projects for which lean principles were not applied). On average, lean projects

were completed in 5% less time and 9% under budget (comparable non-lean projects,

on average, finished on time and 2% under budget).

4. The authors believe (based on their experience of over 1,800 projects at Wipro

Chapter 17 – The Management and Control of Quality

17–82

17-81 (Continued-1)

Continually Root Out/Eliminate Waste

The authors assert that even in knowledge work, there are routine activities that do not

involve judgment or expertise and that are therefore candidates for application of “lean

principles.”

The key, according to the authors, is to (p. 103) “get everyone in the organization to

systematically make waste visible and (then to) do something about it.” To accomplish

this, the authors offer the following specific strategies: teach everyone in the

organization to ask “the five whys” (as practiced at Toyota); encourage employees to

look for small forms of waste, not just big ones; use value-stream mapping to identify

both value-added activities and waste; and, periodically review the structure and content

of every job (thereby reinforcing the point of continuous improvement or the

organization’s long–term commitment to “lean”).

Strive to Make Tacit Knowledge Explicit (i.e., Specify the Work)

Basically, this objective challenges the notion that all knowledge (in knowledge-based

work) is inherently tacit. Rather, it implies that (p. 105) a “surprisingly large amount of

knowledge work can be specified.” In this regard, the authors offer a four-step process

to specifying knowledge work:

(a) Look for and then codify repeatable parts of the process.

(b) Don’t try to specify everything initially, if ever.

(c) Use data to get employee/worker buy-in (i.e., many highly trained

repetitive in nature and therefore capable of being codified)

Structure Communications (i.e., how workers should communicate with one

another)

The workplace today is truly global in nature: work teams may have members from all

over the world. Thus, an effective employee communication plan or structure should be

in place to determine how employee communications should take place.

Three suggestions are offered by the authors in terms of structuring communications:

Chapter 17 – The Management and Control of Quality

17–83

17-81 (Continued-2)

(a) Define who should be communicating, how often, and how (Wipro used

something called a “design structure matrix” to help in this regard)

(b) Create a shared understanding of what work is required and by whom—this,

in turn, allows employees to (p. 107) “spend time solving problems rather

than trying to figure out the job at hand.”

(c) Resolve disagreements with facts, not opinions

Use the Scientific Method to Solve Problems as Soon as Possible (i.e., Address

Problems Quickly and Directly)

To adapt the “scientific method” to knowledge work, the authors suggest the following:

(a) If a problem arises, ideally the person who created the problem should fix it

(people closest to a problem typically know the most about it; therefore,

(c) Solve problems as soon as possible after they emerge (the fresher the

information about a problem, the less subject it is to distortion and the easier

it becomes to find a fix for the problem)

Plan for an Incremental Journey: A Lean System Takes Years to Build

(a) Start small (e.g., use pilot projects, to explore for your organization whether a

lean approach is a viable option)

(b) Codify lessons learned

at hand is visionary and/or experimental don’t classify and view time needed

to come up with “wild ideas” as wasteful, and therefore subject to elimination)

Chapter 17 – The Management and Control of Quality

17–84

17-81 (Continued-3)

Engage Your Managers—Leaders Must Blaze the Trail

In the end state, frontline workers generate and implement new ideas. However, during

the developmental process (implementation of lean), the involvement and support of

middle and senior managers are critical:

(a) Project managers and other mid-level leaders should be heavily engaged in

Thus, senior management must treat the lean initiative as a long-term

change program that ultimately will make the organization more competitive.

Chapter 17 – The Management and Control of Quality

17–85

CHECK FIGURES

17–22 1 sigma = 317,310.51 defects per million; 3 sigma = 2,699.80 defects per million

17–23 No check figure.

17–24 No check figure.

implementation of JIT = $822,000; difference = $732,000

17–35 No check figure.

17–36 No check figure.

17–37 No check figure.

17–38 No check figure.

17–39 No check figure.

17–40 1. Manufacturing cost savings associated with the reduction in rework costs =

$119,700; 2. Financing cost savings associated with inventory reduction =

$18,000; 3. Total estimated savings due to quality-improvement program =

$137,700.

2013 = $955, 2014 = $405; Total Internal Failure Costs: 2013 = $930, 2014 =

$540; Total Cost of Quality (COQ): 2013 = $3,485, 2014 = $2,045.

17–86

17–51 1. Total Prevention Costs: 2013 = $220, 2014 = $530; Total Appraisal Costs:

2013 = $955, 2014 = $405; Total Internal Failure Costs: 2013 = $930, 2014 =

$540; Total Cost of Quality (COQ): 2013 = $3,485, 2014 = $2,045; 7. Revised

2014 ratios: Prevention Costs to Sales = 2.85%; Appraisal Costs to Sales =

2.06%; Internal Failure Cost to Sales = 1.10%; External Failure Costs to Sales =

1.45%.

$1,500,000; Annual Net Financial Benefit (Cost) of switching to JIT = $712,900.

17–58 No check figure.

17–59 2. Net promoter score = 2.8% (i.e., 36.2% − 33.4%)

17–60 1. Maximum amount Paragon Manufacturing would be willing to spend

annually= $509,000 (which is equal to the expected cost of rejections and

repairs without quality control inspection); 2. Sample size, nf = 265 units; 3a.