Chapter 11 – Decision Making with a Strategic Emphasis

11-1

CHAPTER 11: DECISION MAKING WITH A STRATEGIC EMPHASIS

QUESTIONS

11-1 Relevant costs are costs to be incurred at some future time and differ for each

option available to the decision maker.

Relevant costs in replacing equipment would include the cost of purchasing and

decision.

11-2 Decisions where relevant cost analysis might be used effectively include:

1. The special-order decision

6. Profitability analysis: evaluating programs

7. Determining the optimum short-term product (or service) mix

11-3 The only relevant cost is the incremental cost incurred for the additional

11-4 Strategic factors include:

1. The level of capacity usage of the plant

7. Service after the sale

11-5 A well-known problem in business today is the tendency of managers to focus on

short-term goals and neglect the longer-term strategic goals, because their

compensation is based upon short-term accounting measures such as net

income. This issue has been raised by many critics of relevant cost analysis. As

noted throughout the chapter, it is critical that the relevant cost analysis be

Chapter 11 – Decision Making with a Strategic Emphasis

firm’s image in the marketplace, and perhaps a negative effect on sales of the

other products. The important message for managers is to keep the strategic

concerns in mind, and to start with the strategic objectives in any decision

situation.

11-6 The limitations of relevant cost analysis include:

1. Excessive focus on short-term decisions

2. Tendency to focus on quantitative factors only, and to not include the

and then to perhaps not find the strategically correct analysis

11-7 Strategic analysis requires a more integrative focus, as noted in the chapter:

11-8 Some of the behavioral, implementation, and legal issues in using relevant cost

analysis include:

1. The tendency of managers to focus on short term goals, and to not attend

satisfactorily to longer-term strategic goals of the firm. The techniques

described in relevant cost analysis can have the effect of encouraging this

RELEVANT COST ANALYSIS STRATEGIC COST ANALYSIS

Financial Focus Customer Focus

Not Linked to Strategy Linked to the Firm’s Strategy

Precise and Quantitative Broad and Subjective

Focused on Individual Integrative;

Product or Decision Considers all Customer-related

Situation Factors

Short-term Focus Long-term Focus

Chapter 11 – Decision Making with a Strategic Emphasis

11-3

3. Researchers have shown a strong human tendency to rely upon and use

provisions of the Robinson-Patman Act.

11-9 When there is only one production constraint and excess demand it is generally

best to produce only one of products to maximize income, and that is the product

with the highest contribution per unit of scarce resource. When the production

technique.

11–10 Relevant cost analysis and cost-volume-profit (CVP) analysis (Chapter 9) are

similar in that they both rely on the distinction of variable versus fixed costs and

they both use the contribution margin (price less unit variable cost) as the focal

Chapter 11 – Decision Making with a Strategic Emphasis

11-4

BRIEF EXERCISES

11–11 $35 – ($33 − $5) = $7

11–12 The contribution on the order is $3,000 – (10 × $100) = $2,000, or $200 per

sofa. Therefore, Adams should accept the order.

batch, which would be a relevant cost for the special order. Setup costs are

ignored in the above volume-based solution.

11–13 Wings will make a profit by selling at any price above variable cost of $2.50,

which in this case is the incremental cost.

11–14 Relevant Costs:

Repair:

Variable Costs:

Labor = $0.50 × 10,000= $5,000

Fixed Costs:

Total Costs $7,500

Relevant Cost Difference = $7,500 − $6,000= $1,500 more to replace than repair

Decision: Williams should repair the existing machine

11–15 Contribution Margin= $100,000

Overhead that can be eliminated= $90,000

Chapter 11 – Decision Making with a Strategic Emphasis

11-5

11-16 The AAA batteries have a higher contribution per unit and since both the AAA

and AA batteries require the same processing time, ElecPlus should accept the

11-17 Cost with machine: $200,000 + ($5 × 10,000) = $250,000

Cost without machine: $20 × 10,000 = $200,000

Jackson would recover the cost in 1 and 1/3 years, as follows:

11-18 [($0.10 − $0.05) × 100,000] − $1,000 = $4,000

11–19 The special-order price should cover variable costs (which in this case are the

incremental costs), so it should be greater than $3.50 per meal or $3.50 × 200 =

Chapter 11 – Decision Making with a Strategic Emphasis

11-6

EXERCISES

11-21 Special Order; Opportunity Costs (20-30 min)

1. The costs fall from $11 to $10 because of the fixed overhead costs

which are the same at each level of production, so that the unit fixed costs

decrease as production level increases.

2. The relevant costs are:

Materials $2 ($80,000 ÷ 40,000)

Labor 3 ($120,000 ÷ 40,000)

× ($9 − $8) = $20,000

CHECK: Is there sufficient capacity so that opportunity cost = zero?

Current Total Capacity (in units) = 80,000 units

Current Capacity Usage (in units) = 40,000 units

Available Capacity (in units) = 40,000 units

Are opportunity costs = zero? Yes—there is sufficient excess capacity to

accept the special order

3. Other factors to consider:

• Is the order likely to lead to further regular business with this

customer?

• Is the order in the strategic best interest of the firm, for example, will it

Chapter 11 – Decision Making with a Strategic Emphasis

11-7

etc. Also, are there alternative uses of the capacity which will produce

a greater contribution?

11-21 (Continued)

4. Opportunity cost incurred if sales of 5,000 units to regular customers are

lost by accepting the special sales order:

Lost contribution margin, sales to regular customers:

Selling price per unit =

$20.00

Variable cost per unit:

Direct materials =

$2.00

Direct labor =

$3.00

Contribution margin per unit =

$15.00

× Lost sales (in units) =

5,000

Total opportunity cost =

$75,000

Chapter 11 – Decision Making with a Strategic Emphasis

11-8

11-22 Special Order (30-35 min)

1. Current Special Order

Revenue per unit $ 45 $ 35

Variable costs per unit:

Direct materials $ 9 $ 9

Direct labor $ 8 $ 8

Variable factory overhead $ 4 $ 4

Variable nonmanufacturing costs $ 8 29 $ 4 25

Contribution margin per unit $ 16 $ 10

Alternatively, the following relevant cost analysis can be used:

to produce the special order is based on the comparison of current

and special-order production. If there were additional capacity, the

proper decision would be to accept the special order since it has a

positive contribution of $50,000.

2. The minimum price would be $28.20.

At 16,000 units of current output and 20,000 units of capacity, Alton

does not have enough capacity to produce the entire order for SHC.

Revenue from the special sales order (@ $35 per unit offering price) = $175,000

Less: Relevant cost to fill the special sales order:

Out-of-pocket costs ($9 + $8 + $4 + $4 = $25 per unit) = $125,000

Opportunity costs:

# units of lost sales (to regular customers) = 5,000

cm per unit on regular sales ($45.00 – $29.00) =

$16.00 $80,000

Impact on operating income, accepting the special order = ($30,000)

Chapter 11 – Decision Making with a Strategic Emphasis

11-9

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

get an order for 4,000 units. Then the special order could be

accepted without a loss of regular sales.

11-22 (Continued-1)

If SHC insists on the full order of 5,000 units, then Alton must figure

the contribution margin on lost sales ($16.00 × 1,000 units =

$16,000). This loss of contribution margin is less than the contribution

margin on the special order ($50,000), so the special order would still

In general, the minimum selling price = relevant cost = out–of–

pocket costs + opportunity cost, as shown below:

Out-of-Pocket Costs:

Direct materials

$9.00

Direct labor

$8.00

Variable manufacturing overhead

$4.00

Variable nonmanufacturing costs

$4.00

$25.00

Opportunity Cost:

No. units of lost sales

1,000

CM per unit—regular sales

($45.00 − $9 − $8 − $4 − $8)

$16.00

Total opportunity cost

$16,000

No. units in special order

5,000

$3.20

Minimum acceptable price

$28.20

Chapter 11 – Decision Making with a Strategic Emphasis

11–10

11-22 (Continued-2)

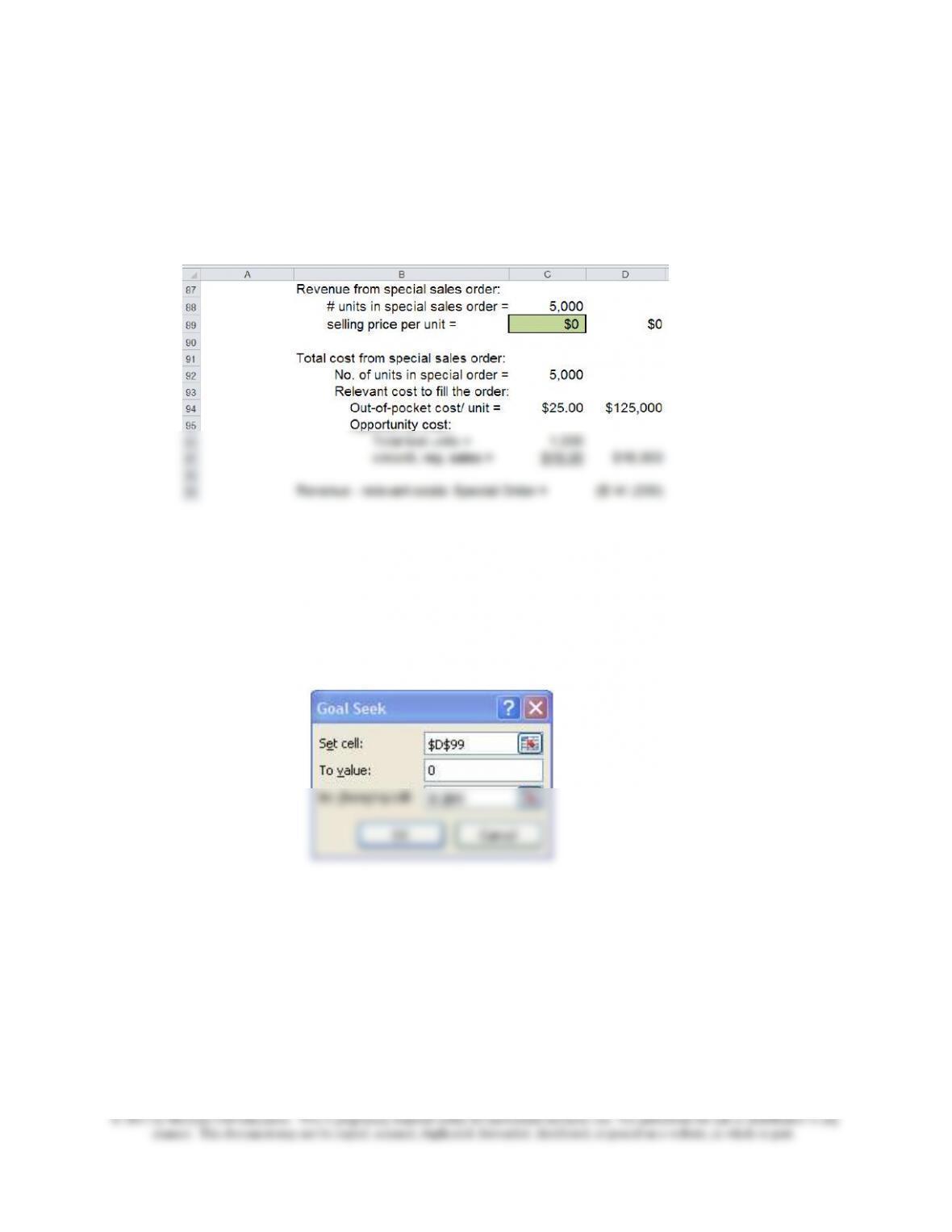

3. Goal Seek Solution:

Step One: Set up the Equation

Cell D99 contains the appropriate equation: =D89-D94-D97

Step #2: Run Goal Seek (i.e., change the selling price per unit, cell

C89) until the value in Cell D99 equals zero)

Chapter 11 – Decision Making with a Strategic Emphasis

11–11

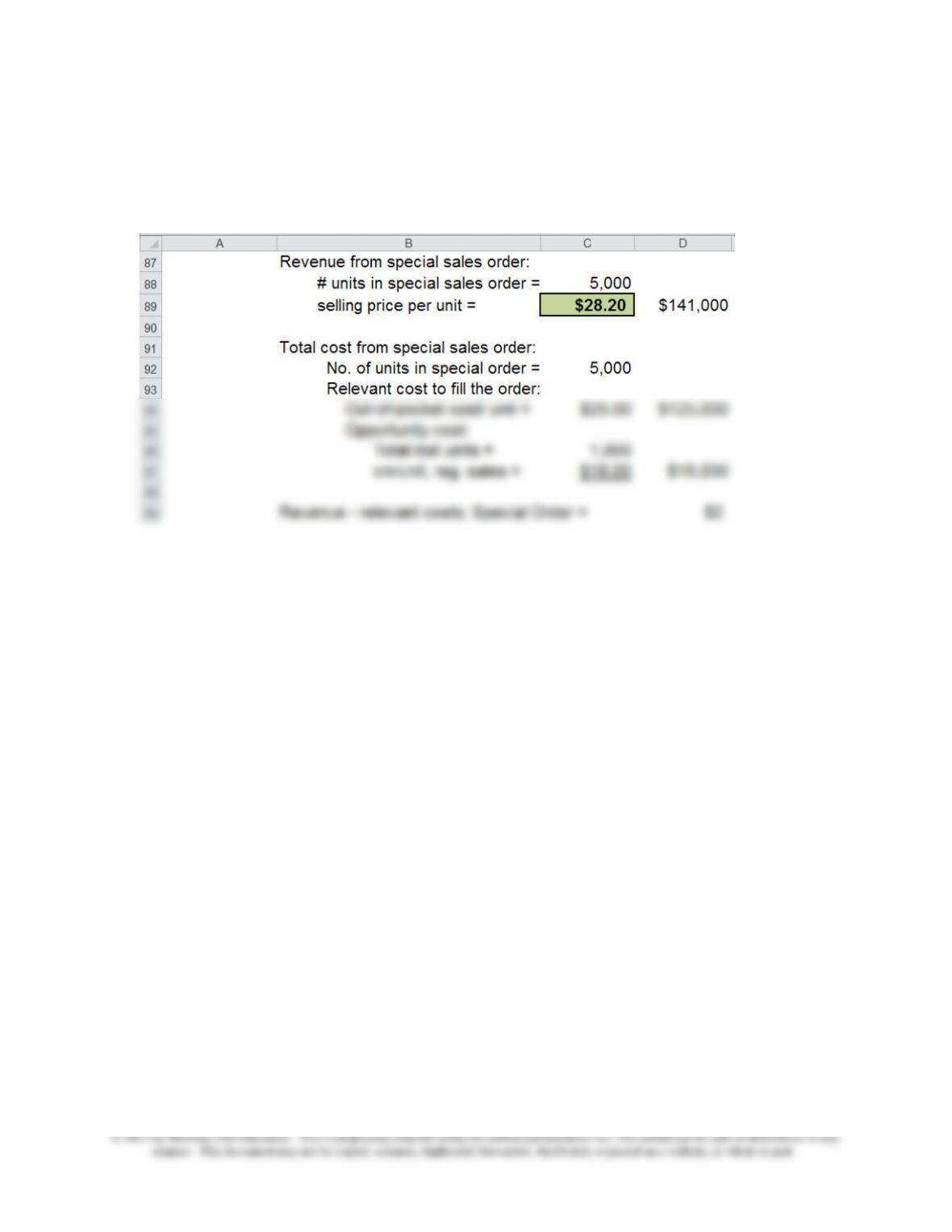

11-22 (Continued-3)

Step #3: Results

Chapter 11 – Decision Making with a Strategic Emphasis

11–12

11–23 Special Order; Use of Opportunity Cost Information (15 min)

1. The special order should have been accepted since the relevant cost is

$3.50 − $1.50 = $2.00 per cap, or $2.00 × 15,000 = $30,000 total cost.

mistaken reliance on full cost, instead of relevant costs.

2. Research studies have consistently found that decision makers often

ignore opportunity costs. For this reason, it is particularly important that the

development of decision-making skills place particular emphasis on

identifying and incorporating opportunity costs. Interestingly, a recent study

found that decision makers with greater expertise in developing

comparative income statements appeared to ignore fixed costs more than

costs.

Other studies have shown that the decision maker’s cognitive style, the

presence of unused capacity, or the relative amount of the opportunity cost

can affect the use of opportunity cost information by the decision makers in

experimental studies. Overall, these results show that in practice, decision

makers have a difficult time using opportunity cost information properly and

consistently.

References: Sandra C. Vera-Munoz, “The Effects of Accounting

Knowledge and Context on the Omission of Opportunity Costs in Resource

Allocation Decisions,” The Accounting Review, January 1998, pp. 47–72.

Steve Buchheit, “Reporting the Cost of Capacity,” Accounting,

Organizations and Society, August 2003, p. 549; Robert E. Hoskin,

“Opportunity Cost and Behavior,” Journal of Accounting Research, Spring

1983, p. 78; Robert Chenhall and Deigan Morris,” The Effect of Cognitive

Style and Sponsorship Bias on the Treatment of Opportunity Costs in

Resource Allocation Decisions,” Accounting, Organizations and Society 16,

Issue 1, pp. 27–46.

Chapter 11 – Decision Making with a Strategic Emphasis

11–13

11–24 Special Order (10-15 minutes)

To begin the analysis, Fred Stanley, the Earth Baby CFO, should recognize

that the $3.00 full cost for its product includes $1.00 of irrelevant fixed

overhead. Only the variable costs of $2.00 per unit are relevant. From this

However, the agreement with GDI could be a potentially serious strategic

liability for Earth Baby. Earth Baby’s reputation is built upon differentiation

and product superiority, features which make it attractive to a small, but

important segment of the baby products market. To sell its products

through a discount retailer, even under another brand name, could harm

the differentiated image of Earth Baby’s product line, and cause it to lose

market share in its usual distribution channels (the high-end grocery stores

and specialty baby retail stores). This is especially true given that GDI has

the limited right to market the product as “manufactured by Earth Baby.”

Chapter 11 – Decision Making with a Strategic Emphasis

11–14

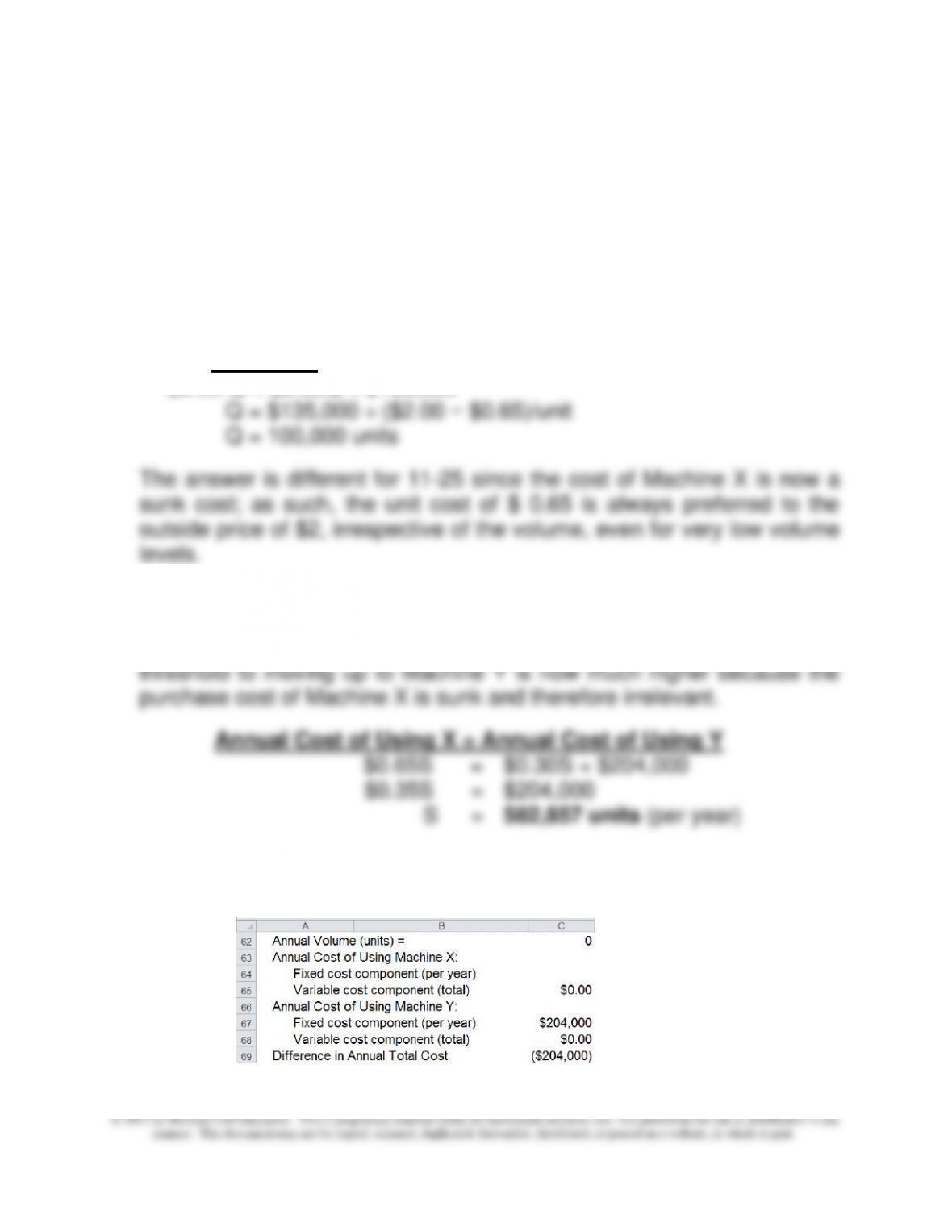

11-25 Make or Buy; Continuation of Problem 9-25 (15 min)

1. The answer is zero. In contrast to 9-25, for which Machine X was a

relevant cost (it had not been purchased yet), the proper analysis was to

compare the cost of purchasing Machine X versus the cost of

purchasing from the outside vendor. The analysis was as follows,

showing that Calista should purchase Machine X if volume is expected

to exceed 100,000 units:

Machine X

$2.00 Q = $0.65Q + $135,000

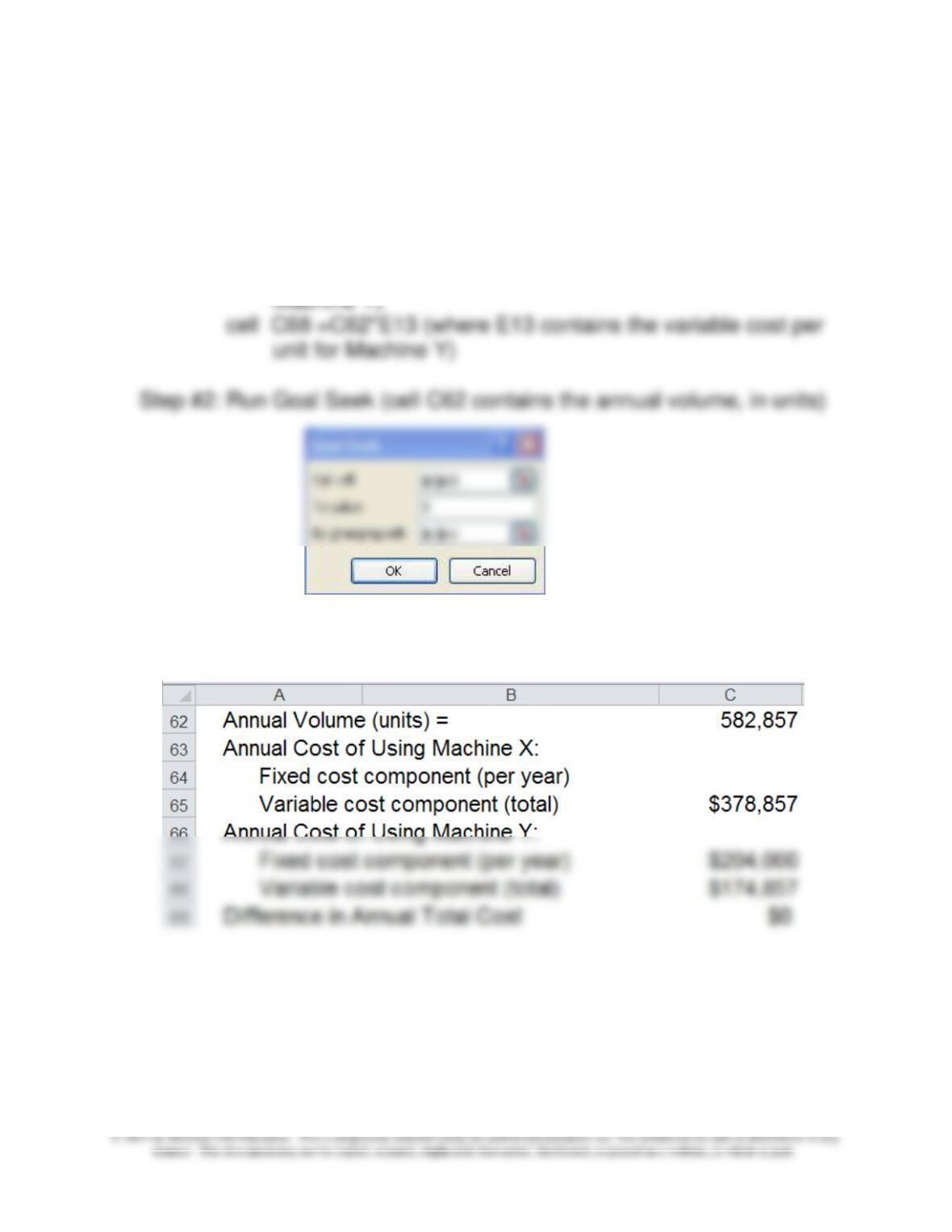

2. Here we use an approach similar to that used in 9-25, except that the

$135,000 purchase cost of Machine X is irrelevant. The answer for 9–25

was 197,143 units, but now it is much higher, 582,857 units. The

3. Using Goal Seek to Calculate the Above Volume-Indifference Level

Step #1: Define the Cost-Differential Equation

Chapter 11 – Decision Making with a Strategic Emphasis

11–15

11-25 (Continued)

Note: cell C69 contains the formula =(C64+C65)−(C67+C68)

cell C65 =C62*C13 (where C13 contains the variable cost per

unit for Machine X)

cell C67 =E12 (where E12 contains the fixed cost per year for

Step #3: Results (the indifference volume is 582,857, the same as

calculated above in Part 2)