Chapter 11 – Decision Making with a Strategic Emphasis

11–46

11-35 (Continued-2)

Re: The purchase of attic fans from Harris Products:

• What are the alternative uses of Martens’ production capacity, in

addition to pumps and attic fans that might produce higher

contribution?

• How reliable is Martens’ information that Harris is a reliable producer

of quality products?

• How will Martens’ customers react, if at all, to know that the attic fans

are not manufactured by Martens?

11–47

11–36 Make or Buy; Strategy (30 min)

1. GianAuto is in a high-growth, highly competitive industry. Auto makers

are increasingly outsourcing the manufacture of parts and entire brake

or seating systems to low-cost producers throughout the world. In

North America, many of these plants are located in Mexico and

throughout Latin America. To be competitive in this business, Gian

must continue to be cost competitive and to also provide the customer

service and reliability that is expected by the auto makers. Gian can

coverings from outside suppliers. GianAuto could more easily alter the

coverings’ design and change the quantities produced, especially if

long term contracts are required with outside suppliers. GianAuto

should also consider the economic impact that closing Denver Cover

will have on the community and how this might affect GianAuto’s other

operations in the region.

Chapter 11 – Decision Making with a Strategic Emphasis

11–48

Other items that should be considered by GianAuto before making a

decision include:

• The disposal value or alternate uses of the plant and equipment.

• Any income tax implications including tax rates applicable to

• Should GianAuto continue to manufacture the covers, but in a

new, cost-efficient plant; the location could be anywhere in the

world.

Chapter 11 – Decision Making with a Strategic Emphasis

11–49

11-36(continued-1)

2. The net cost savings from closing the plant are estimated as $55,200,

as follows:

Gross Cost Savings (Cost Avoided)

Materials $32,000

Labor

Additional Plant-Closing Charges

Termination charges on cancelled material orders

($32,000 × 0.15) 4,800

Employment assistance 1,000

Total $68,800

Net relevant costs (savings to close the plant) $55,200

The following costs are not relevant to the decision since they are

unavoidable costs:

Depreciation-equipment $5,000

Depreciation-building 3,000

Continuing pension expense

• The depreciation amounts are not relevant to the decision

because they represent portions of sunk costs that are being

written off during 2013.

• Three-fourths of the annual pension expense ($3,000) is not

relevant because this amount would continue whether or not the

plant is closed.

Chapter 11 – Decision Making with a Strategic Emphasis

11–50

11-36 (Continued-2)

• The amount for plant manager and staff is not relevant because

Vosilo and his staff would continue with GianAuto and administer

three remaining plants.

with an associated increased demand for automobiles. Also, the company

needs to consider how the cost of outsourcing production might change as

a result of the current difficult economic times. Will wage rates in the U.S.

fall relative to other countries to make the Denver plant more competitive?

If so, then closing the plant at this time might be unwise, irrespective of the

analysis of costs; the company would then need the plant for future low-

cost production. The analysis of the decision regarding the Denver plant

requires a complex and comprehensive consideration of global economic

trends as well as the costs in the plant itself.

Chapter 11 – Decision Making with a Strategic Emphasis

11–51

11–37 Make or Buy; Strategy; Ethics (45 min)

1. An analysis of per unit and total costs for 32,000 units shows that the

Midwest Division should purchase the parts for a saving of $15,440

($575,040 − $559,600).

Cost per unit

Total Cost

Cost to purchase MTR-2000 from Marley:

Bid price from Marley

$17.3000

$553,600

Equip. lease penalty [($36,000÷12) × 2 × 1]

0.1875

6,000

Total cost to purchase

$17.4875

$559,600

Cost for Midwest to Make MTR-2000:

Direct material ($195,000 ÷ 30,000) × 1.08

7.02

$224,640

Direct labor ($120,000 ÷ 30,000) × 1.05

4.20

134,400

Factory space rental ($84,000 ÷ 32,000)*

2.625

84,000

Equipment leasing ($36,000 ÷ 32,000)*

1.125

36,000

Variable manufacturing overhead

3.00

96,000

Total cost to make

$17.97

$575,040

*Total production required in 2013 is 32,000 units; 30,000 units in

2012. Unit variable costs are based on 2012 costs and units; fixed

costs in total are the same in 2013 as in 2012.

2. Strategic factors that the Midwest Division and Paibec Corporation

should consider before agreeing to purchase MTR-2000 from Marley

Company include the following:

• The quality of the Marley component should be equal to, or better

than, the quality of the internally made component, or else the

labor problems or affect the company’s position in the community,

In addition, there may be termination costs which have not been

factored into the analysis.

11–52

11–37 (continued)

3. Referring to the specific standards for ethical practice by a

management accountant

(http://www.imanet.org/PDFs/Statement%20of%20Ethics_web.pdf),

Lynn Hardt should consider the ethical standards of competence,

integrity, and objectivity:

Competence

• Prepare complete and clear reports and recommendations after

appropriate analysis of relevant and reliable information. John has

asked Lynn to adjust and falsify her report and leave out some

manufacturing overhead costs.

Integrity

• Refrain from either actively or passively subverting the attainment

of the organization’s legitimate and ethical objectives, Paibec has

a legitimate objective of trying to obtain the component at the

• Refrain from engaging in or supporting any activity that would

discredit the profession. Falsifying the analysis would discredit

Hardt and the profession.

Credibility

• Communicate information fairly and objectively. Hardt needs to

to fully disclose the analysis and the expected cost increases.

Chapter 11 – Decision Making with a Strategic Emphasis

11–53

11–38 Outsourcing Call Centers (40 min)

1. The corporate overhead cost is irrelevant since in total it will not

change whether or not the call center is returned to Atlanta (i.e., it is

not an avoidable cost).

Naftel

Present Value

Annual Costs First 3 Yrs Yrs 4-5 Factor (6%) Naftel Atlanta

Naftel Contract 4,200,000$ – – 4.21200 17,690,400$

Lease Opportunity cost, Yr 4 – – 100,000$ 0.79209 – 79,209$

Lease Opportunity cost, Yr 5 – 100,000 0.74726 – 74,726

Salaries – $2,300,000 2,300,000 4.21236 – 9,688,437

Equipment (leased) – $850,000 850,000 4.21236 – 3,580,509

Telecommunications – $500,000 500,000 4.21236 – 2,106,182

Administrative – $600,000 600,000 4.21236 – 2,527,418

Naftel, per-year amount 4,200,000$ 17,690,400$

Present Value

Atlanta

discount the amounts applicable to all five years, while single sum discount

factors are used for the lease opportunity cost in years 4 and 5 (0.792 and

0.747 for Year 4 and Year 5, respectively). The present value tables are

located at the end of Chapter 12. (NOTE: the results reported above are

based on exact present-value factors; if the factors from the text, which are

rounded, are used, the answer will be slightly different from that presented

above.)

The analysis shows that the Naftel contract would save MB $50,000 per

year in each of the first three years, and $150,000 in each of years 4 and 5.

Whether you consider the undiscounted or the present-value analysis, it is

clear that the Naftel contract has the lower cost. But, the difference is not

great relative to total cost, so that strategic issues are important in making

the final decision. Some of these strategic issues are discussed in parts 2

and 3 below. In addition:

11–54

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

11-38 (continued)

• Since customer service is very important for MB’s success,

would the location of the call center in Atlanta or at Naftel provide

• Given the difficult times predicted (at the time) for the banking

industry, would it not have been especially important to

differentiate the company from others? Customer service is one

important way to do that. If customer service in Atlanta could be

carefully managed so that it provides very high quality service,

this could be an important competitive advantage.

2. At the time of the decision (late 2008), the value of the dollar had

been increasing relative to most other currencies. This means that

the cost to MB of the service by Naftel would decrease in currency–

services as MB grows.

3. The ethical issues in the decision here include the consideration of a

community obligation that MB has for providing jobs, when possible,

in a local economy that had been suffering from high unemployment.

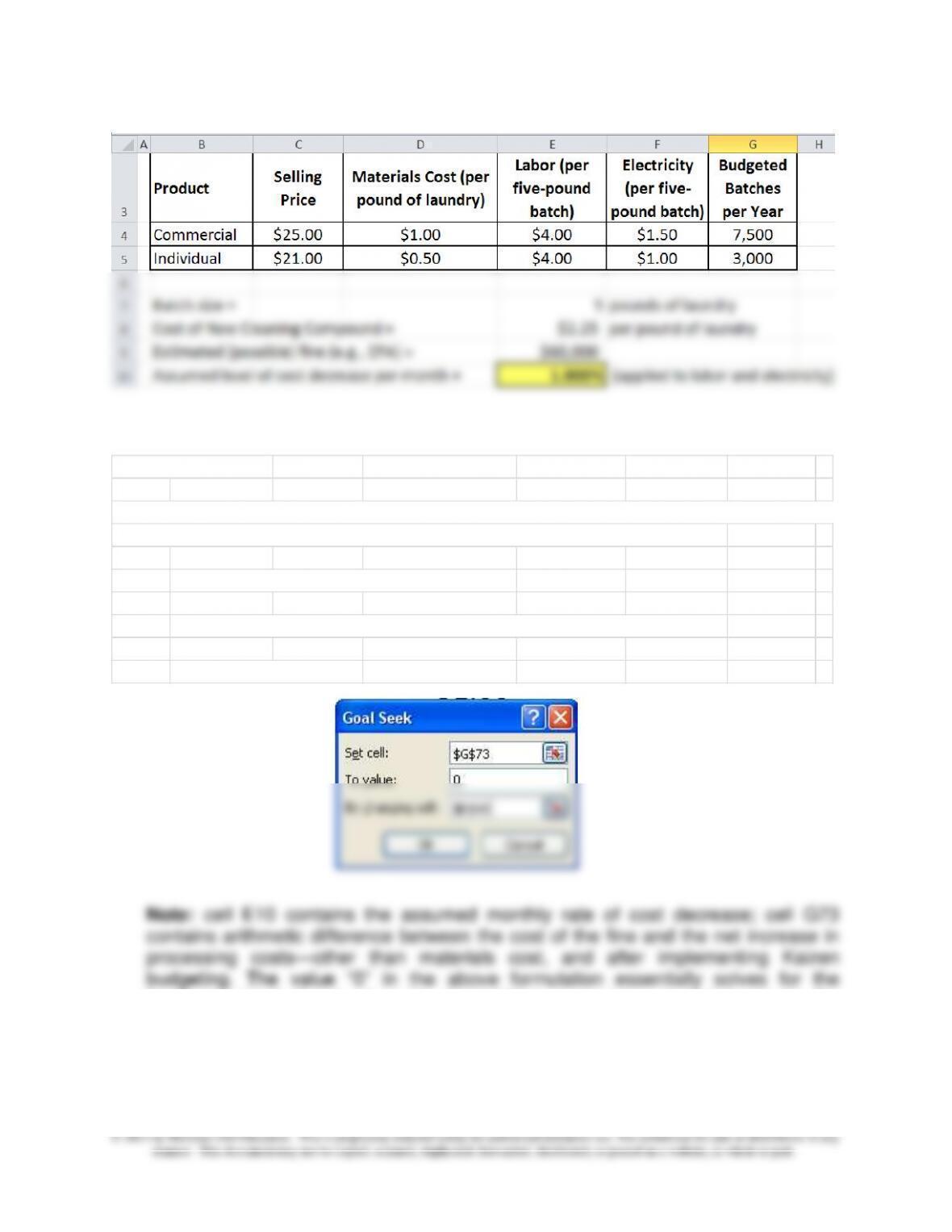

11–39 Budgeting and Sustainability (60-75 minutes) (note: this is Pr. 10–58)

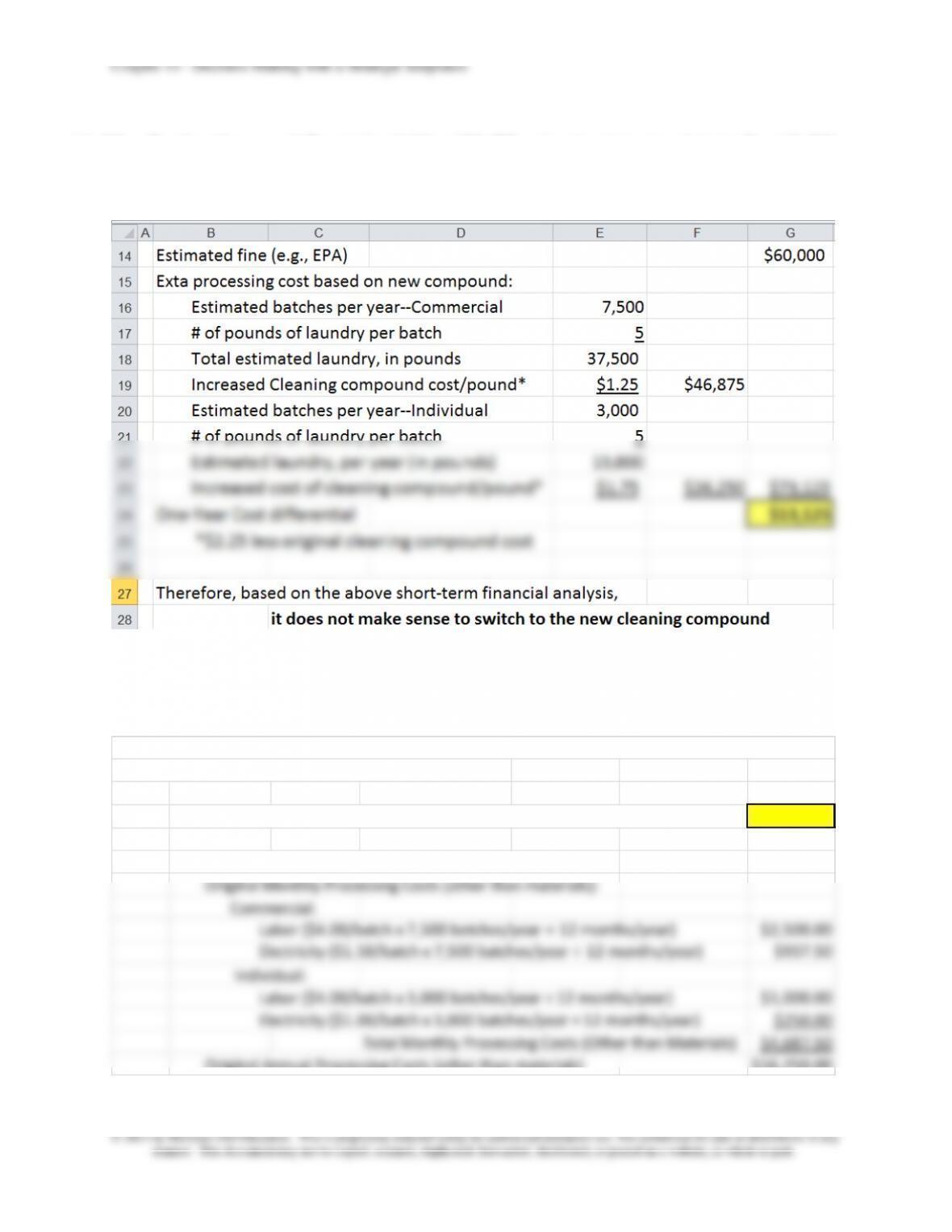

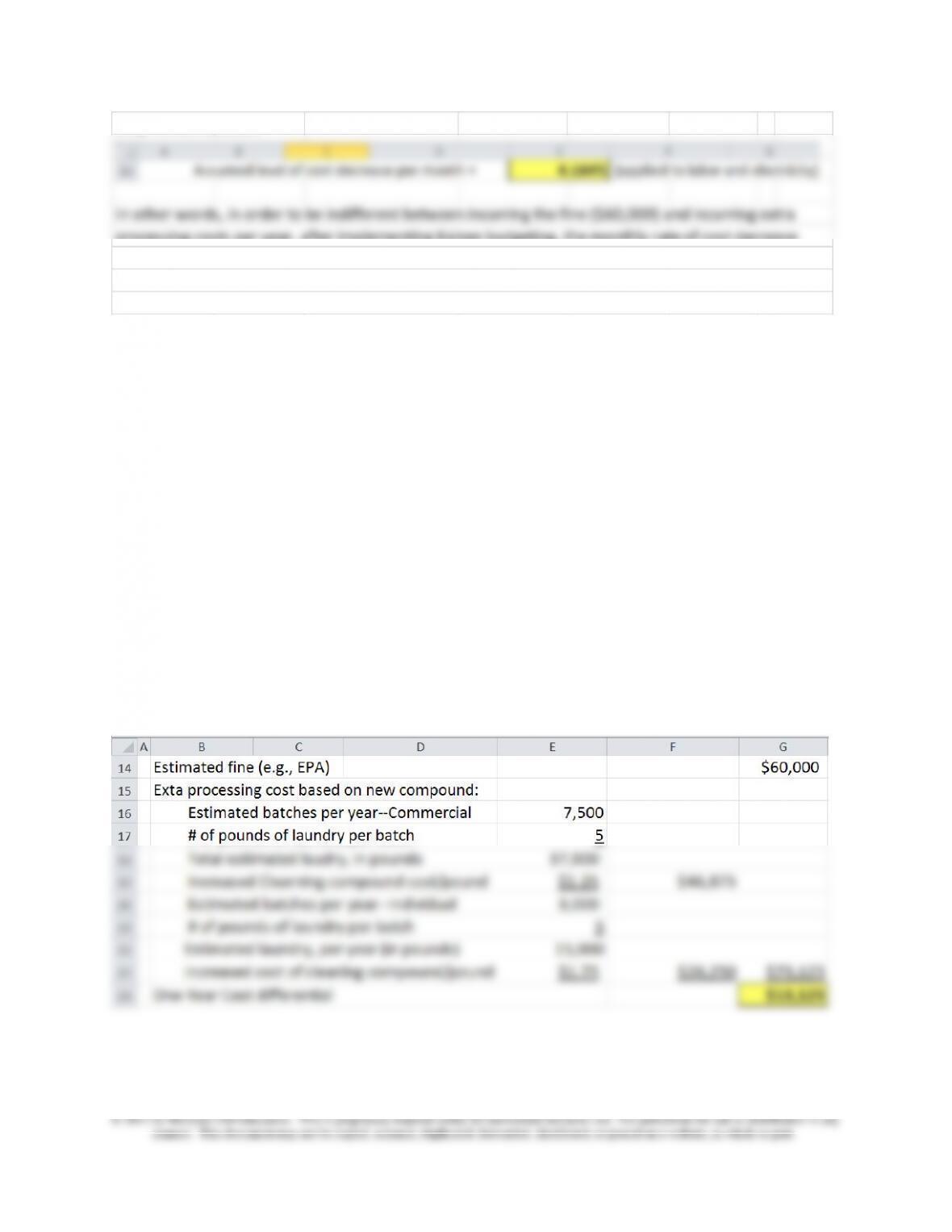

Requirement 1: Short-Term Financial Analysis

For purposes of illustration (and for Requirement 3 below), the cell

reference for $13,125 (above) is G24; the cell reference for $60,000

(above) is G14.

Requirement #2: Assume the Switch to the New Compound and the Introduction of Continuous-

Improvement (Kaizen) Budgeting

Estimated increase in processing cost, per year with new compound (from above) =

$73,125

Estimated annual cost savings, per Kaizen budget:

Original Monthly Processing Costs (other than materials):

Commercial:

Labor ($4.00/batch x 7,500 batches/year ÷ 12 months/year) $2,500.00

Electricity ($1.50/batch x 7,500 batches/year ÷ 12 months/year) $937.50

Individual:

Labor ($4.00/batch x 3,000 batches/year ÷ 12 months/year) $1,000.00

Electricity ($1.00/batch x 3,000 batches/year ÷ 12 months/year) $250.00

Chapter 11 – Decision Making with a Strategic Emphasis

Cell references: $73,125 = cell G32 (=G23); $4,687.50 = cell G42 (=SUM(G37:G41));

$56,250.00 = cell G43.

11–39 (Continued–1)

Revised Level of Monthly Processing Costs (other than materials):

Month Labor Electricity

1 $3,465.00 $1,175.63

2 $3,430.35 $1,163.87

3 $3,396.05 $1,152.23

4 $3,362.09 $1,140.71

5 $3,328.47 $1,129.30

6 $3,295.18 $1,118.01

7 $3,262.23 $1,106.83

8 $3,229.61 $1,095.76

9 $3,197.31 $1,084.80

10 $3,165.34 $1,073.95

11 $3,133.68 $1,063.21

12 $3,102.35 $1,052.58

Total–-Yr. 1 $39,367.64 $13,356.88 $52,724.52

Chapter 11 – Decision Making with a Strategic Emphasis

11–57

11–39 (Continued–2)

Requirement 3

a. Determine the Monthly Cost-Reduction Rate that would Equate the net increase in year-one total

processing costs (materials + labor + electricity) with the anticipated fine

Step One: Define the Breakeven Cost Equation

Difference between the fine and net increase in year-one processing costs $9,599.52

Step Two: Run Goal Seek

breakeven level: that is, the rate of monthly cost savings needed to equate the

value of the fine and the increased processing costs due to the new compound, but

after implementing Kaizen. As shown below, Goal Seek provides the answer:

4.164% per month.

Chapter 11 – Decision Making with a Strategic Emphasis

11–58

Step Three: Solution

In other words, in order to be indifferent between incurring the fine ($60,000) and incurring extra

processing costs per year, after implementing Kaizen budgeting, the monthly rate of cost decrease

must be 4.164%. At this level, the year-one Kaizen-based cost savings would be $13,125, while the net

year-one processing cost increase would be $60,000 ($73,125 – $13,125)--an amount exactly equal to

the estimated fine. Note, however, that such a dramatic increase in productivity is highly questionable.

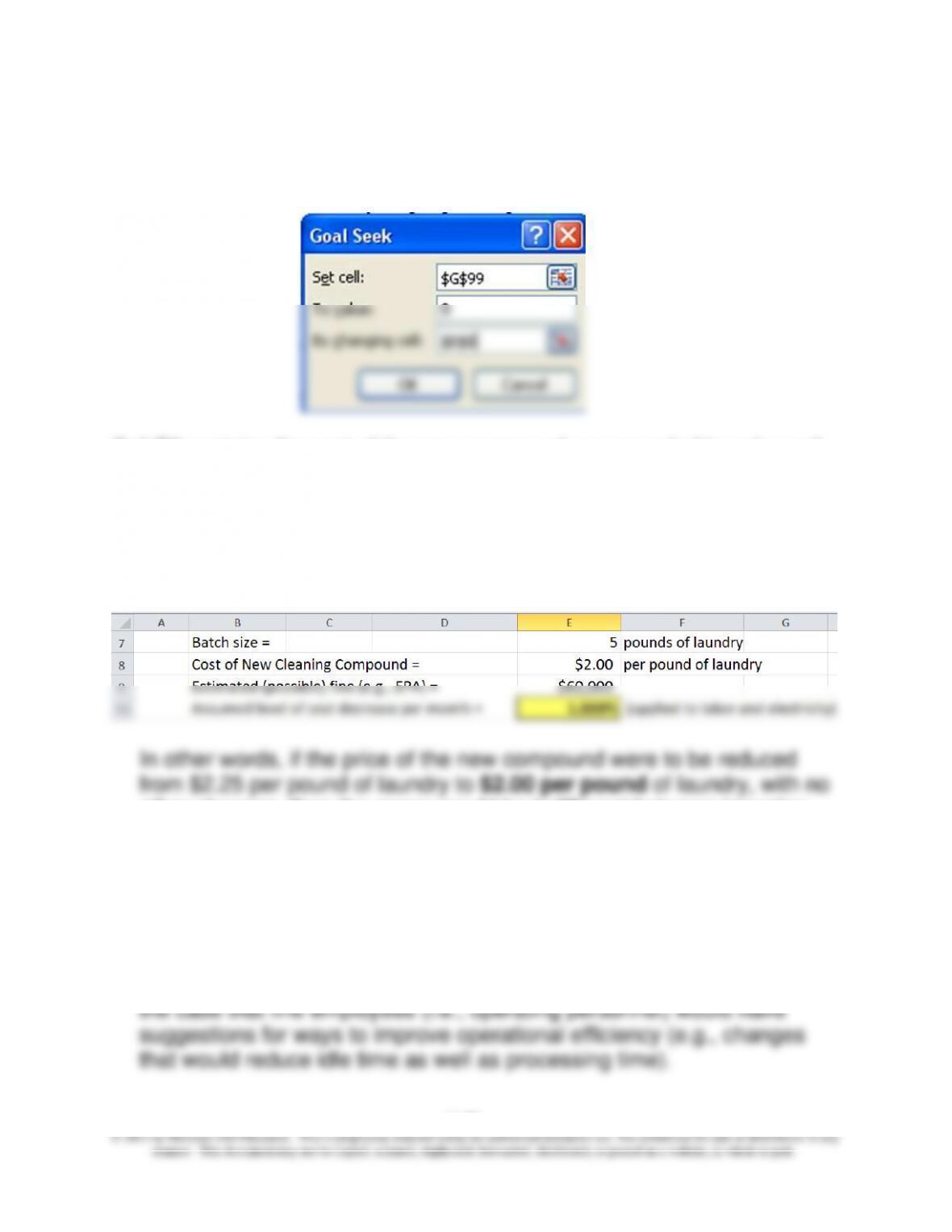

b. The cost per pound for the new compound that would equate the anticipated fine with

the net year-one costs, assuming no Kaizen budgeting plan (i.e., no reduction per

month in processing costs):

11–39 (Continued–3)

Step One: Set Up the Cost Equation

Cost differential: anticipated fine and net one-year processing costs, with

no Kaizen budgeting plan = $13,125

Note: the above value is contained (in this example) in cell G99, which

in turn is defined as the contents from cell G24. G24 contains the

difference between the anticipated cost of the fine, $60,000 (entered in

cell G14) and the expected increase in material cost associated with the

use of the new compound (G23), as shown below:

Chapter 11 – Decision Making with a Strategic Emphasis

11–59

Step Two: Run Goal Seek

Cell E8 contains the cost of the new compound, per pound of laundry; cell

G99 contains the cost difference: the anticipated fine versus the increased

processing cost attributable to the use of the new compound.

11–39 (Continued–4)

Step 3: Results

other changes, then the owner would be indifferent between incurring

the estimated fine and using the new (higher-priced) compound. Of

course, other considerations may affect the ultimate decision.

4. Operational Changes Needed to Ensure Kaizen Cost Savings

The reduction in labor time might be realized by improving the efficiency

of operations, including a decrease in machine downtime. It is probably

Chapter 11 – Decision Making with a Strategic Emphasis

11–60

To achieve aggressive cost reductions in labor, however, it might be

necessary to institute some type of employee incentive program.

Savings in electricity consumption may be more difficult to achieve.

Some reduction would likely accompany any planned-for reductions in

chain. David Duncan is more likely to achieve his cost-reduction goals

by working with his suppliers. As indicated above, if the cost of the new

compound can be decreased by only $0.25 per pound of laundry

processed, David would be indifferent (solely on an expected cost basis)

11–39 (Continued-5)

5. Other (qualitative) Considerations that Might Affect the Ultimate

Decision:

• What impact, perhaps negative, will the Kaizen budgeting approach

have on employee morale?

• Will the quest to achieve aggressive levels of cost reduction have a

negative effect on service quality?

• Will the use of the new, environmentally friendly cleaning compound

have a beneficial effect on the image of the business and therefore

on sales?

• Would the use of the new cleaning compound have a beneficial

impact on employee health/working conditions?

• If the existing cleaning compound were to continue to be used, would

it require any special handling costs/preventative measures (e.g.,

employee health and safety)?

• Would incurring a fine (rather than incurring increased operating

costs) negatively affect the image of the business, and therefore