1) the coefficient of determination is a number between:

a.0 and 1

b.-1 and 1

c.-2 and 2

d.the coefficient of determination can be any number

2) which of the following is not a way for a management accountant to resolve an

ethical conflict?

a.bring the matter to the attention of the company’s auditor

b.consult an attorney concerning the ethical conflict

c.initiate a confidential discussion with an ima ethics counselor

d.discuss the issue with the management accountant’s immediate supervisor except

when the supervisor is involved

3) the management accountant who planned to improve an organization’s operations by

developing models of consumer behavior would be using which of the following

contemporary management techniques:

a.target costing

b.benchmarking

c.business intelligence

d.lean accounting

e.focus on the customer

4) which of the following is not an advantage of using a “highly achievable target”

when constructing budgets?

a.increasing managers’ commitment to achieving budget targets

b.increasing the risk that managers will engage in “earnings management” behavior

c.improving predictability of earnings or operating results

d.decreasing the cost of achieving organizational control

e.enhancing the usefulness of a budget as a planning and coordinating tool

5) staley co. manufactures computer monitors. the following is a summary of its basic

cost and revenue data:

assume that staley co. is currently selling 600 computer monitors per month and

monthly fixed costs are $80,000.

what is staley co.’s degree of operating leverage (dol) at this sales volume? (round your

answer to three decimal places.)

a.5.118

b.4.405

c.5.630

d.5.000

e.4.846

6) auto engines have become more complex over the past twenty years, partly as a

result of environmental concerns about exhaust contaminants. engineers have

developed two basic approaches to solving the contaminant problem. the first

emphasized the catalytic converter, a modification of the auto exhaust system designed

to break down pollutants. the second emphasized redesign of the auto engine’s

combustion process, which adds more than twice the cost of the catalytic converter

alone. however, redesigning the combustion process usually results in improved full

efficiency.

required:

(a) comment on the strategic advantage of redesigning the combustion process versus

simply adding a catalytic converter.

(b) what are the ethical questions, if any, that should be addressed in the above

decision?

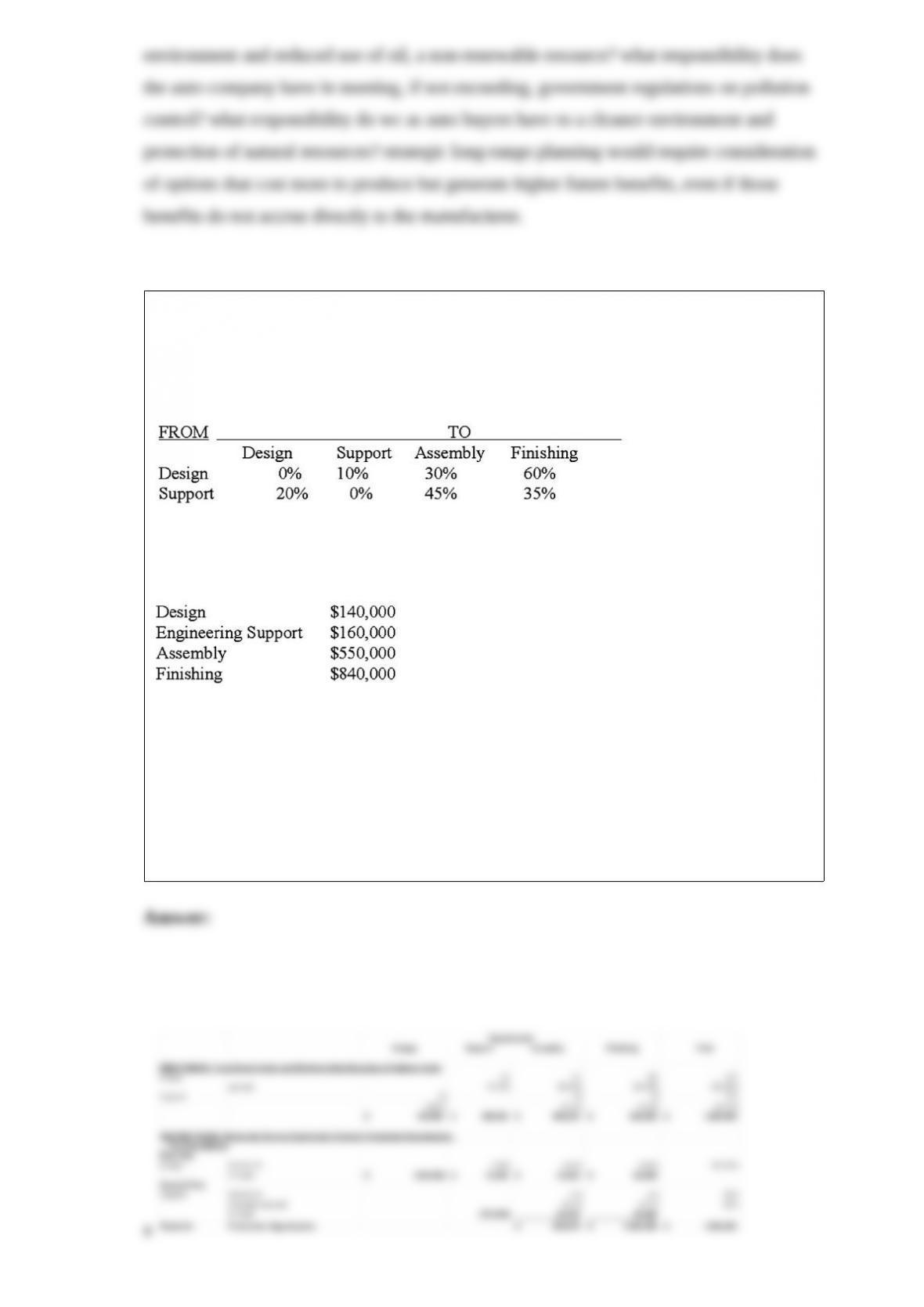

7) barstow manufacturing company has two service departments product design and

engineering support, and two production departments assembly and finishing. the

distribution of each service department’s efforts to the other departments is shown

below:

the direct operating costs of the departments (including both variable and fixed costs)

were as follows:

the total cost accumulated in the finishing department using the step method is

(calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and

round all dollar amounts to the nearest whole dollar):

a.$1,000,125

b.$1,890,000

c.$689,875

d.$642,000

e.$923,000

8) important concepts in resource consumption accounting include all of the following

except:

a.variable costing

b.resource interrelationships

c.activity interrelationships

d.detail level cost information

e.treatment of idle capacity

9) the sum of units transferred out and ending inventory units, assuming no spoilage,

determines the:

a.units completed during the period

b.units spoiled

c.units transferred in during the period

d.units accounted for

e.units started during the period

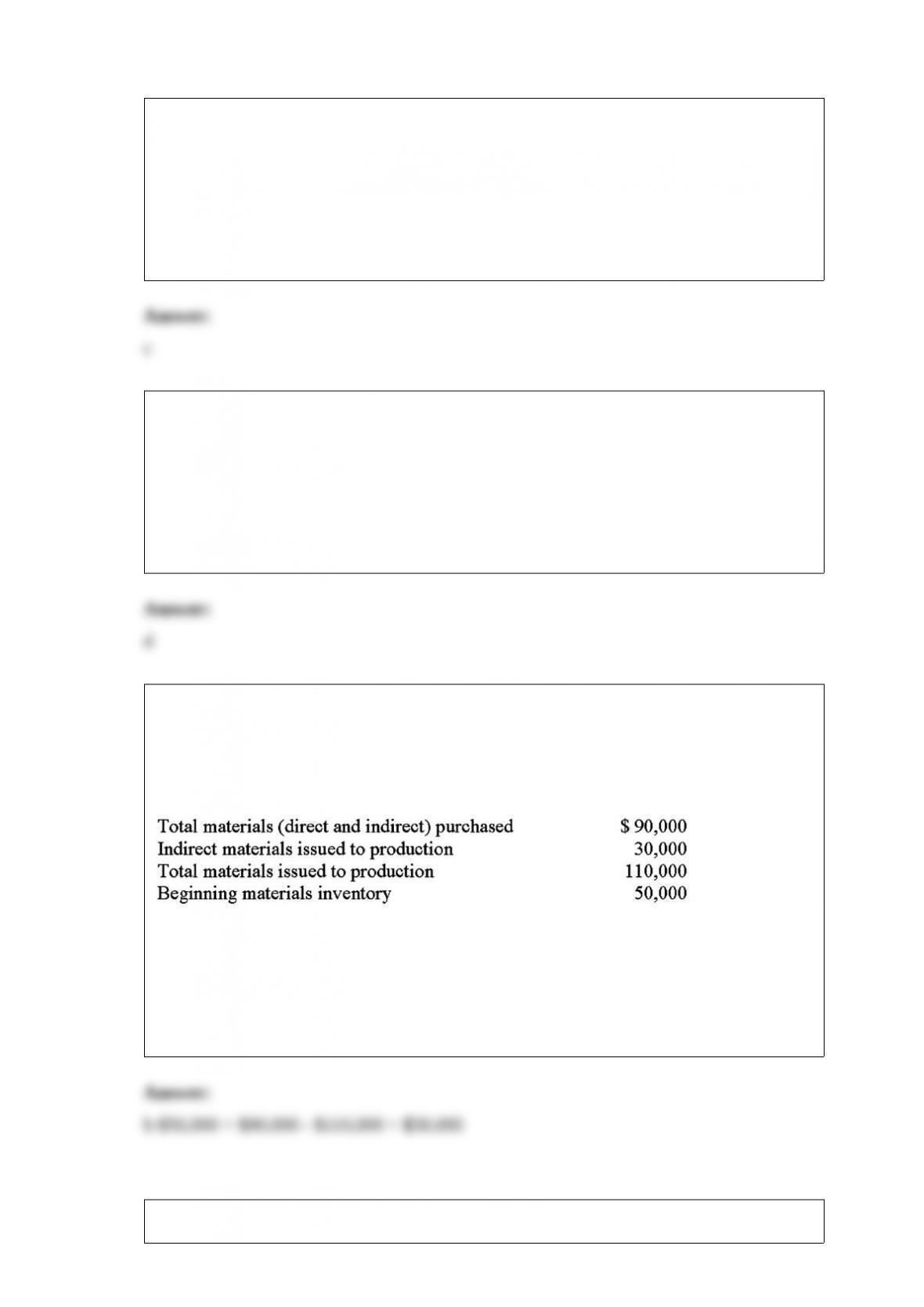

10) abc company uses a materials inventory account to record both direct and indirect

materials. abc charges direct materials to wip, while indirect materials are charged to

the factory overhead account. during the month of april, the company has the following

cost information:

the ending materials inventory cost is:

a.$110,000

b.$30,000

c.$90,000

d.$80,000

e.$50,000

11) relevant costs in a make-vs.-buy decision of a part include:

a.corporate headquarter costs that will be allocated differently depending on the

decision option chosen

b.setup overhead costs for the manufacture of the product using the outsourced part

c.currently used manufacturing capacity that has alternative uses if the part is

outsourced

d.factory-related insurance cost

e.corporate (i.e., headquarter) salaries

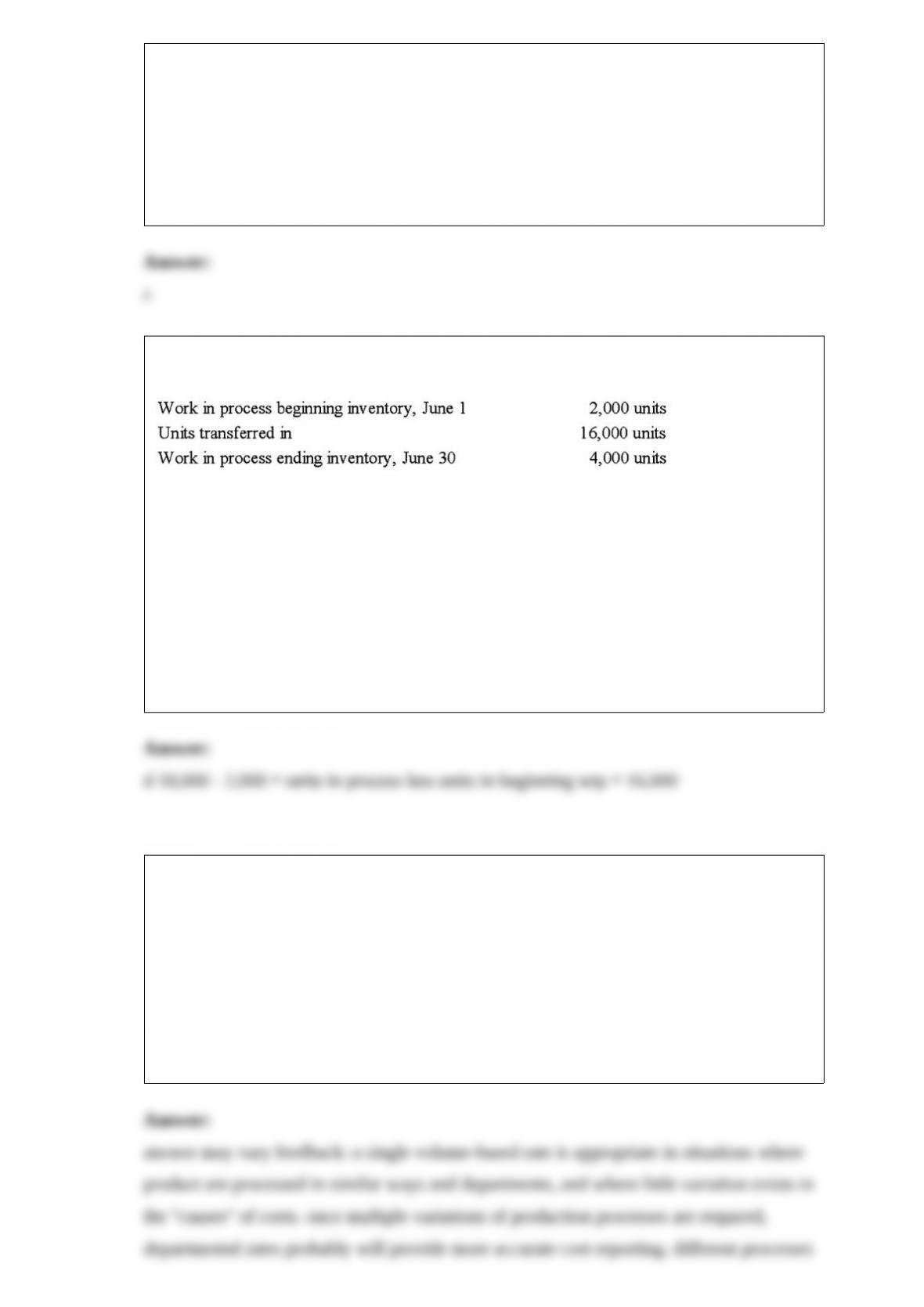

12) stoltenberg co. had the following information for the month of june:

beginning work-in-process inventory is 30 percent complete as to conversion. ending

work-in-process inventory is 50 percent complete as to conversion. materials are added

at the end of the process.

the equivalent units for transferred-in costs under the fifo method are calculated to be:

a.12,000

b.10,000

c.14,000

d.16,000

e.18,000

13) certo health products was formed two years ago to produce and distribute a

newly-patented protein supplement. two variations of the original supplement have

since been developed and introduced for general sale. the three products are processed

in essentially the same way, but ann marshall, the owner of certo, anticipates that a

half-dozen new products will be developed for sale in the next two years. these products

will not be variations of the patented supplement, and will require a different production

process other than the one currently used. ann has asked you to review the current use

of a single volume-based rate and explain the arguments for using departmental rates

with activity-based drivers.

14) helen auger has seen the centicle group, a not-for-profit, in-home health care

organization, grow during the past ten years to a $500 million revenue, multi-state

organization. helen was promoted to her controller position six months ago, after

serving capably in several financial accounting positions at the centicle group.

at a budget review committee meeting last friday, several committee members

expressed frustration with the pace of the budget development. they described the

newly introduced “bottom up” system of participative budgeting as “unwieldy,”

‘slow-paced,” and “repetitive.” helen’s objective in introducing the participative

approach was to involve to a much greater extent lower level supervisors and

employees. helen is meeting with the budget review committee again tomorrow when

she plans to explain the advantages of “bottom up” versus “top down” approaches to the

budgeting process.

required: helen has asked you to help her prepare for tomorrow’s meeting by preparing

the following:

1> a 40 -50 word description of participative budgeting, including some basic

advantages of this approach to budgeting.

2> a brief, one-paragraph explanation of the concept of “budget ownership,” one of the

values that participative (“bottom up”) budgeting is said to have.

15) two students in a cost accounting class were arguing about the need to gather good

unit cost information for manufacturing. one student, travis, maintained that a firm

producing and selling large quantities of relatively few products would have no need for

an abc system, since an abc system is usually more expensive to implement than a

volume-based system. alicia countered that even firms with high-volume homogeneous

products could benefit from a cost management technique like activity-based costing

(abc).

required: choose sides in this discussion and present justifications for your choice.

16) levis strauss and co, maker of levi’s familiar 501 and 505 brands of jeans, also make

a new brand that was introduced for discount retailers such as walmart. levi’s strategy

with the new jeans was to sell a competitively priced pair. the jeans will be about

one-half the price of the familiar 501 and 505 jeans. to get costs down levi’s will:

use cheaper fabrics and materials.

shun costly mass-market advertising.

strictly limit the number of fits, styles, and colors.

required:

1> assess the new strategy at levi. what do you think are the potential benefits and

risks?

2> how will the firm’s value chain and balanced scorecard change as a result of the new

strategy?

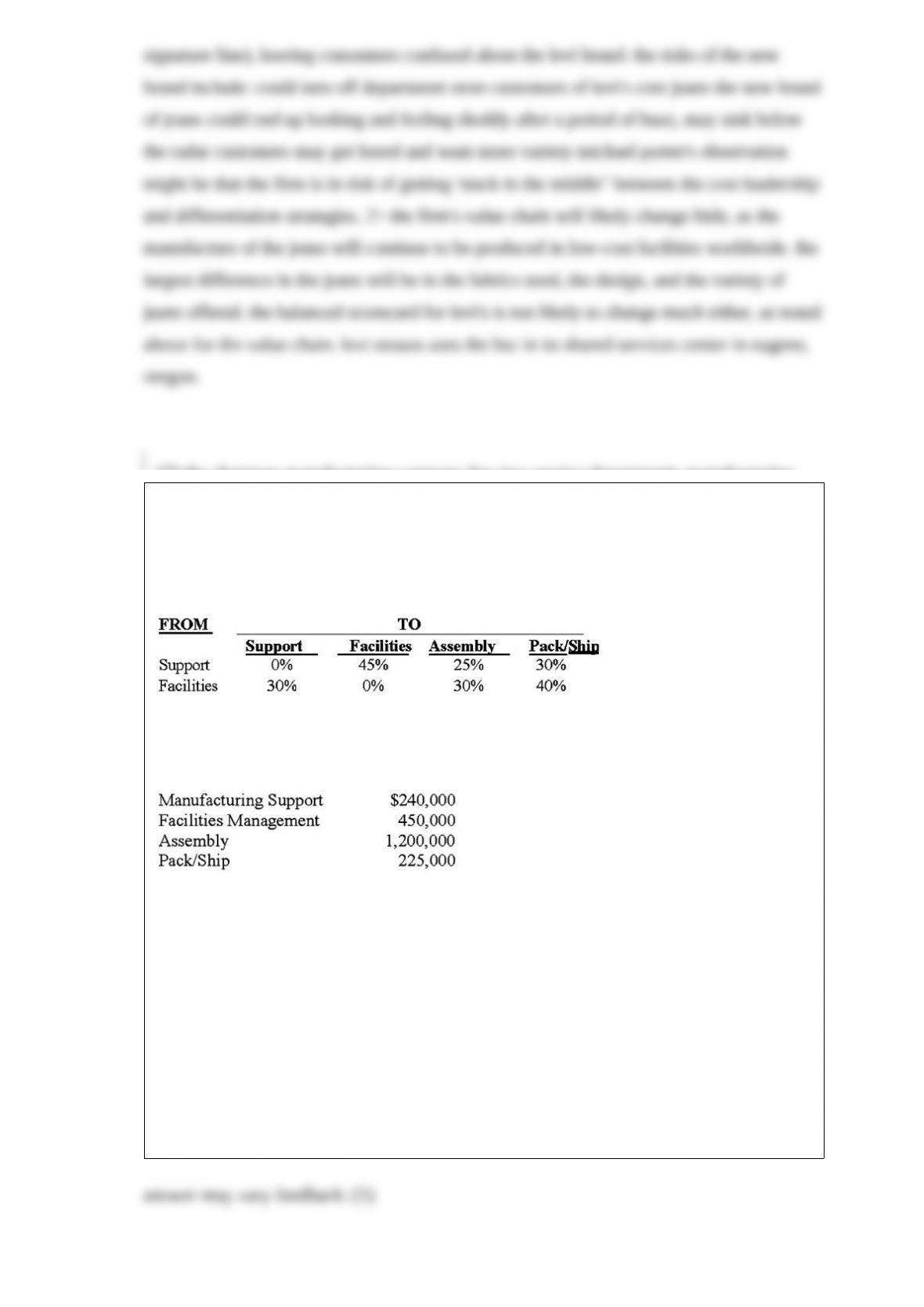

17) the chapman manufacturing company has two service departments manufacturing

support and facilities management, and two production departments assembly and

packing/shipping. the distribution of each service department’s efforts to the other

departments is shown below:

the direct operating costs of the departments (including both variable and fixed costs)

were as follows:

required:

(calculate all ratios and percentages to 2 decimal places, for example 33.33%, and

round all dollar amounts to the nearest whole dollar):

(1) allocate the service department costs to the production departments using the direct

method.

(2) allocate the service department costs to the production departments using the step

method with the support department going first.

(3) allocate the service department costs to the production departments using the

reciprocal method.

18) feel the difference, inc. manufactures bath and beauty products such as soaps, skin

creams, lotions, and other products primarily for people with dry and sensitive skin. it

has just introduced a new line of product that removes the spotting and wrinkling in

skin associated with aging. it sells these products in pharmacies and department stores

at prices slightly higher than those of other brands because of feel the difference’s

excellent reputation for quality and effectiveness.

feel the difference currently has very low utilization of plant capacity. two years ago, in

anticipation of rapid growth, the company opened a new large manufacturing plant,

which has yet to be utilized more than 50 percent. partly for this reason, feel the

difference has sought new partners and was able, with the help of financial analysts, to

locate suitable business partners. the first potential partner identified in this search was

a large supermarket chain, all-mart, which is interested in the partnership because it

wants feel the difference to manufacture an age cream to sell in its stores. the product

would be essentially the same as the feel the difference product but would be packaged

in the all-mart brand name. the agreement would pay feel the difference $2.00 per unit

and would allow all-mart a limited right to advertise the product as manufactured for

all-mart by feel the difference. feel the difference’s cfo has made some calculations and

has determined that the direct materials, direct labor and other variable costs needed for

the all-mart order would be about $1.00 per unit as compared to the full cost of $2.50

(materials, labor, and overhead) for the equivalent feel the difference product.

required:

should feel the difference accept the proposal from all-mart? why or why not? (include

strategic considerations)

19) patterson equipment inc. produced a pilot run of 20 units of a recently developed

motor used in the finished products. the pilot run required an average of 12 direct labor

hours per motor. patterson has an eighty percent learning curve on the direct labor hours

needed to produce new motors.

required:

calculate the average direct labor hours per unit for the first 640 motors (including the

pilot run) produced.