Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-16

In practice, TOC accounting is similar to variable costing, and like variable costing, “Emphasis is

placed on short-run differential or incremental costs rather than on long-run full costs” (Usry &

Calvasina, p. 8) The difference is that TOC accounting treats materials as the only variable cost, and

arbitrary allocations are avoided by not doing any allocations or applying all operating costs to the

constraining resource. TOC emphasizes maximizing throughput per unit of time. Non-bottleneck

resources are allowed to remain idle because excess production creates unnecessary inventory.

TOC is a short-term focused tool that considers direct materials and energy to be the only product

cost. While this approach promotes greater pricing flexibility, it does not consider fixed costs to be

product costs. This means that TOC is short-term focused and is much like the contribution per unit of

number of parts on rack and also on the conveyor belt. (E.g. a bumper is easier to paint than a luggage

rack as there is more uniform surface area.) Coatings (high or low gloss) vary in first pass yield. The

production scheduler must consider these factors, so maybe they could take a more strategic approach to

bidding by offering price levels that can fluctuate based on promised delivery time. Such a bidding

approach would have to consider more than just the variable costs of production, and ABC attempts

(ideally) to assign costs associated to making a product to that product, including fixed costs.

ABC is a full costing model in that all costs of performing an activity are assigned to the activity,

and eventually to a cost object based on the use of selected cost drivers. Through this process, ABC

analysis draws attention to the full cost of a product by estimating the long-term costs of products over

The ABC cost information is not irrelevant, however, for the ABC information has already served

two purposes: directing management’s attention to the varying demand products places on various

resources and a refined calculation of the profit each product generates. What remains is using the

information to make strategic decisions.

ABC and TOC can be complementary; while ABC is an accounting model, TOC is a

manufacturing philosophy. TOC may be able to tell you what to make today, but is the day’s production

in line with long-term objectives? Many units pass through booths 3 and 4 but do not receive and

treatment in those booths, which cuts into available capacity because the items stay on the conveyor than

identify areas to target for improvement – which has a direct relationship to TOC because of the focus on

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-17

managing activities. ABC, in conjunction with ABM can effect changes in activity that can reduce

consumption, but there may be a time lag before spending follows usage. Also, ABC is a model based on

consumption rather than spending so it can help analyze the cost of used versus unused capacity. With its

process-improvement focus, TOC can be useful in identifying waste, which ABC calls non-value-added

activities. Identifying and reducing waste at constrained resources elevates the constraint and reduces

capacity of the resources into account and can highlight the cost of unused capacity, but capacity is

acquired in lumpy amounts and ABC does not adequately model this situation. Resource consumption

accounting, however, has provided some new notions to solve these problems.

RCA is a comprehensive, integrated cost system that can provide an identification of cost affected

by decisions at different management levels. Most notably, RCA has a strong planning emphasis that can

be beneficial in a proactive culture, and allows management to integrate prospective and actual results

into the organizational control system.

According to Keys and VadDer Were (1999), RCA provides managers with cost information for

short-term and long-term time horizons and for tactical and strategic decision making. While drawing a

clear distinction between resource cost drivers and activity drivers, a RCA system can use both types of

drivers in tandem. As Van Der Merwe and Keys (2001, pp 31-32) summarize: RCA effectively addresses

some of the shortfalls of the ABC perspectives on resources by:

1. Providing the resource output measure as a consistent and uniform measure of

resource capacity.

2. Accurately accounting for short- to medium-term fluctuations in capacity use and

information.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-18

Keys and VanDer Merwe (2002) offer the RCA cube and an alternative to the ABC cross to

overcome their perceived weaknesses of the ABC/M model. The RCA approach explicitly considers the

operational information needs of line managers, the tactical information needs of middle managers, and

the strategic information needs of top management.

From a control perspective, RCA provides input-side and output-side variances, which reflect

whether variances are caused by resource acquisition issues (resource cost and quality), process issues

(scrap and quantity variances), and production (lot size and production volume variances).

From a planning perspective, RCA explicitly accounts for idle capacity while Activity based

budgeting (which uses ABC as its foundation) does not adequately handle idle capacity. PPS dos not

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-19

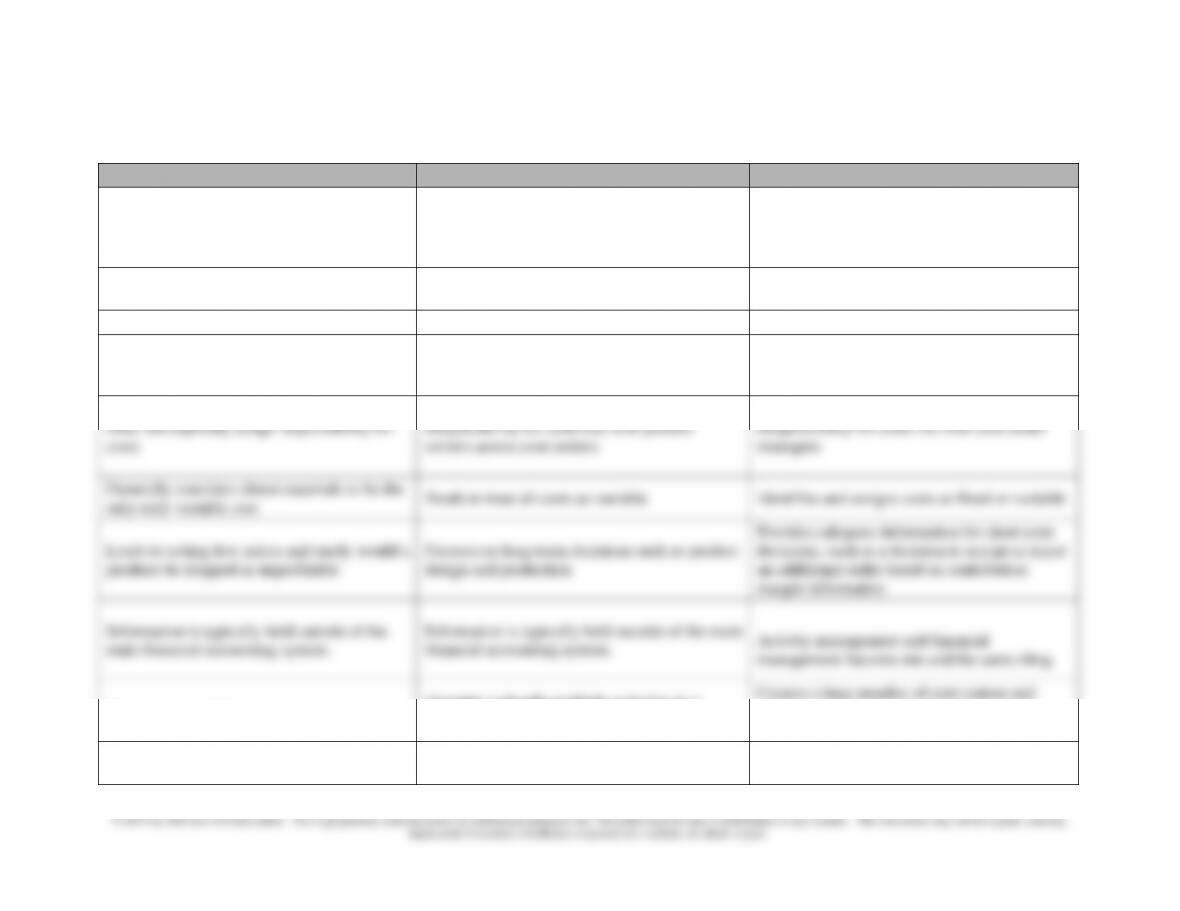

Highlights some of the key characteristics of the three methods.

TOC

ABC

GPK/RCA

A production philosophy that provides

insights into manufacturing process and how

resource consumption and capacity impact

production decisions

Models the economic aspects of how resources

are transformed into products.

Attributes cost of excess capacity to person

responsible for influencing the level of resource

available, but does not allocate it to products

Tactical

Strategic/tactical – depending on its focus on

resource usage.

Strategic

Ignores cost of fixed resources

Uses historical cost

Uses replacement cost depreciation

Ignores cost allocations

Aims at allocating all the costs required to

produce and market a product in the long run.

Applies the marginal costing principle and,

accordingly, allocates only variable costs to

products.

Does not explicitly assign responsibility for

costs

Responsibility for costs lies with process

owners across cost centers

Responsibility for costs lies with cost center

managers

Generally considers direct materials to be the

only truly variable cost

Tends to treat all costs as variable

Identifies and assigns costs as fixed or variable

Leads to setting low prices and rarely would a

produce be dropped as unprofitable

Focuses on long-term decisions such as product

design and production

Provides adequate information for short-term

decisions, such as a decision to accept or reject

an additional order based on contribution

margin information

Information is typically held outside of the

main financial accounting system.

Information is typically held outside of the main

financial accounting system.

Activity management and financial

management become one and the same thing

Ignores cost centers

Attempts to handle multiple activities in a

single cost center.

Creates a large number of cost centers and

splitting and segmenting costs and activities

down to their primary elements.

Short-term perspective to obtain greatest

marginal benefit.

Long-term perspective gives recommendations

for product design and log-run production

Superior to ABC for making short-term

decisions, primarily for short-run production

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-20

programs, yet long-term investment decisions

actually require net present value analysis.

decisions as well as short-run pricing,

particularly for manufacturing companies.

Uses expected consumption of a limited

amount of capacity

Traditionally uses expected consumption, but

can use some capacity measure

Supports capacity analysis through the use of

theoretical volume cost rates

Tends to focus on subset of a process (the

bottleneck resource)

Addresses process owners across functions

Focuses on cost centers

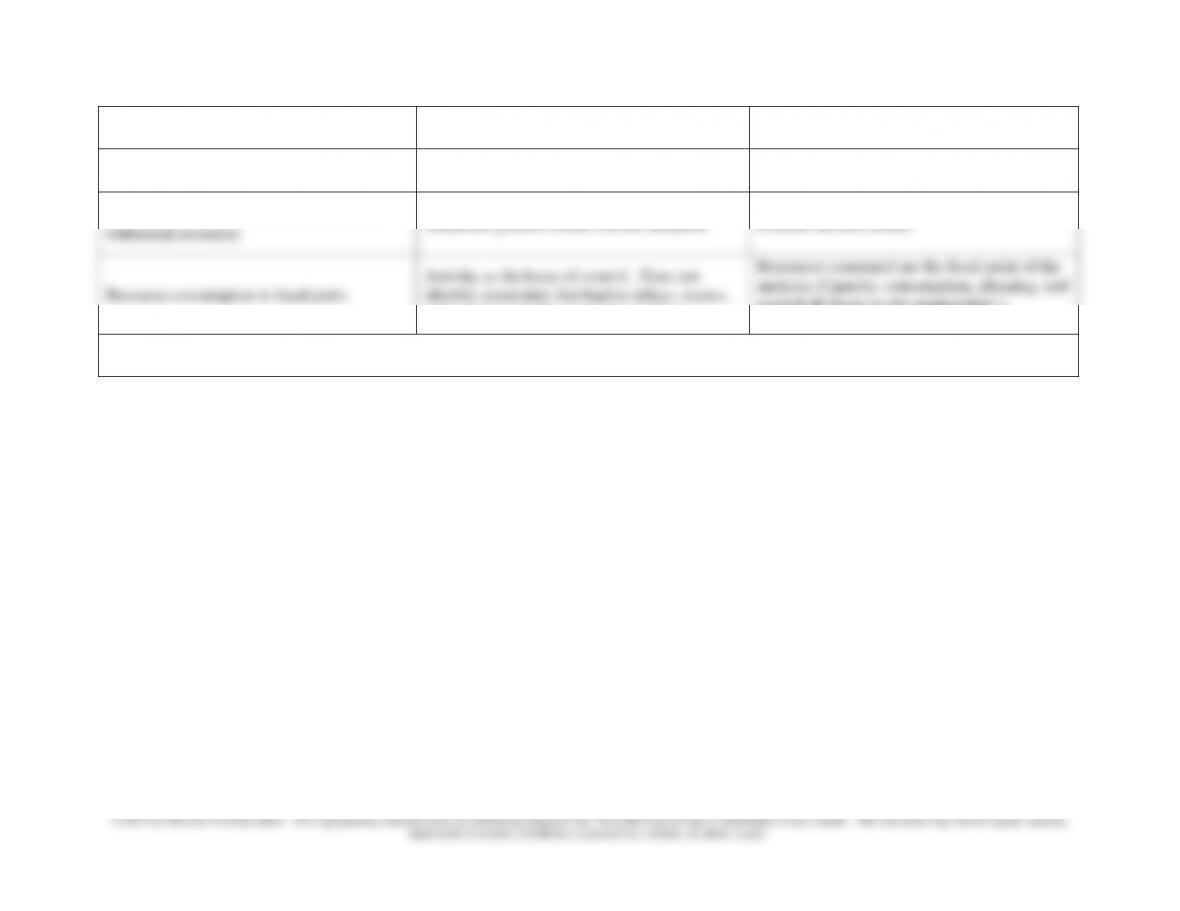

Resource consumption is focal point.

Activity as the locus of control. Does not

identify constraints that lead to delays, excess,

and variations in the production process

Resources consumed are the focal point of the

analysis; Capacity, consumption, planning, and

control all focus on the organization’s

resources – not the activities performed.

Some of the material in this table was taken from Clinton, B. D., and S. A. Webber. (2004) RCA at Clopay. Strategic Finance. October 2004, pp.

20-26.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-21

The following questions were not part of the requirements in the case competition. The questions

could serve as the basis for the final question in the live presentations at the Annual Meeting. Also,

the suggested solutions might give you ideas as to what represents a more in-depth or insightful

analysis of the case, which may help judges evaluate the teams.

Additional possible questions

Question 2 could be revised to give a more directed focus by changing the wording as follows:

“Management of Customer Paint Shop used ABC to obtain a better understanding the “true” cost of the

products. Management is now working toward a more proactive approach to capacity utilization, and

TOC costing has been suggested and some additional cost analysis was done. Discuss the potential

strategic value of the ABC versus TOC cost information in making decisions about the use of existing

capacity.” This wording offers the opportunity to spend time focusing on ABC and TOC would allow the

instructor to avoid or delay dealing with RCA if desired.

Possible solution: TOC promotes focusing on the contribution margin per unit of scare resource,

given the production environment that management has put into place.

TOC may not be appropriate for all organizations, but there are some conditions that indicate

TOC may be useful: 1) frequent expediting and 2) large WIP inventory in terms of number of days sales.

Also, TOC is not a panacea. For example, TOC looks at the constrained resource while a technique like

JIT looks to improve all processes, not just the process related to the constrained resource. The JIT

approach allows for a deeper understanding of all processes and their interrelationships that may not be

gained from a strict TOC approach. Thus potentials for uncovering opportunities may also be missed

from a strict TOC approach. Also, TOC takes only a short-term view of capacity utilization, whereas a

process like activity-based costing takes a longer-term perspective.

Other possible questions:

The case states the change to ABC “was made to better understand the costs associated with

painting the various products.” How effective is ABC in supporting such an objective as compared to

TOC and RCA. This question changes the context of the comparison to highlight that different tools

might be preferred for different purposes and reinforce the need to understand more than one costing

concept in order to be able to decide when a tool might be most effective.

The instructor could ask the students to identify the characteristics that make an organization’s

processes a candidate for the use of RCA and comment on whether PPS meets each of those

characteristics.

Possible solution: Grasso (2005, p.16)

The approach assigns resource elements to resource centers using the following criteria

4. The cost center’s size should be limited, and it should be geographically compact.

The paint booths along the conveyor line display these characteristics, making PPS a candidate for RCA.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-22

References

Grasso, LawrenceP., 2005, Are ABC and RCA Accounting Systems Compatible with Lean

Management?, Management Accounting Quarterly, Fall, 2005, Vol. 7, No. 1, pp.12-27

Johnson, H. Thomas, Relevance Regained: From Top-down Control to Bottom-up Empowerment, Free

Press, New York, NY, 1992, p.139.

Keys, D. E., and A. Van der Merwe. (2002). Gaining Effective Organizational Control with RCA.

Strategic Finance. May 2002, pp. 41-47.

Keys, D. E., and A. Van der Merwe. (1999). German vs. United States Cost Management. Management

Accounting Quarterly. Fall 1999, pp. 19-26.

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-23

5-4 Forest Hill Paper Company

1. What is the competitive environment facing FHPC? What is and/or should be FHPC’s

competitive strategy?

Questions to generate discussion:

1. What is the competitive strategy of the company? What should it be? (Of the industry?)

2. How would you change the competitive strategy of the company? What is the role of cost

information in determining the strategy of the company?

GO TO QUESTION 2 and come back to this…..

Reduce product variety

Batch size

Slitting, or charge appropriately for it

Reduce the number of grades

The industry

Paper products, generally a commodity → cost leadership

“Capital intensive, mature industry” → cost leadership

overhead is 105% of materials cost

Very cyclical; down in the 1980s and early 1990s, at present demand exceeds supply

Effect on customer order pattern; exaggerates swings in demand

Importance of the cost/management of unused capacity

Firms in the industry do not readily increase capacity

FHPC market share down from 35 to 25%

Customers move to plastic and environmentally sound products (where is FHPC

In these products??)→ cost leadership

Paperboard manufacturing is a continuous process; hard to trace costs to individual

units of output; also this points up speed (cycle time) as a key cost driver

Producers cannot control prices; “selling price reflect spot market prices,”

→ cost leadership

The company

Focus on full range of products – 19 different grades of paperboard; also

widths (slitting) and coatings.

Focus on offering special services (slitting) → differentiation???

Wide range of batch sizes

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-24

2. Describe FHPC’s current costing system, and explain the type of costing system you would

recommend for FHPC and why. For products A, B, C and D shown in the case, what are product

costs using the current and your recommended costs system?

Overall cost problem: We have 4 batches, one each of products A,B,C and D; there are several

reels of product in each batch. What is the cost per reel, cost per batch and total production cost?

Gross margin per batch?

Note, you cannot focus your costing on reels only, because you would miss the importance of batch

level costs (grade change and slitting) and the influence of these batch related costs on total costs.

Good starting questions:

1. What are the cost drivers in this case

2. Just looking at Exhibits 1 and 2, which products do you think will be over costed with the current

costing system and why?

Product B has so few reels, so batch costs of grade change will strongly effect it

Product D has a large number of reels per batch, and no slitting, it is over costed.

3. How would you describe the current cost system

4. Show the current cost per reel and per batch of the current cost system

5. What are the activities in the ABC system

6. Show the costs under the ABC system

Cost Drivers

Volume: how do we measure it??? The firm uses tons of materials in costing, feet in

pricing

Tons of materials, or

Linear feet of paperboard produced

Grade; a combination of both:

Caliper (thickness)

Coated/uncoated

Grade changes (see below re: scheduling) – scrap; almost ½ reel is lost after

each grade change (process instability); partially offset by recycling the

scrap paper

Scheduling; sequence runs for minor changes in grade

Batch size

Slitting

Not included in the case….

Cycle time (because it is a continuous process industry and there is now excess demand)

Quality of raw materials

Effectiveness of scheduling so as to reduce the cost impact of grade changes

Current Cost System

Slitting cost is shared among all grades of paperboard; customers are charged a small

amount for slitting (presumably not enough to recover the cost of slitting)

Volume based drivers are used – materials cost, with the idea that thicker material takes

longer to process (slower machine rate) and longer to dry

overhead rate = 105% x materials cost

Note however (not in case) that while tons of materials produced drives costs, the

industry practice is to set price by linear foot

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-25

Calculating the FHPC Overhead Rate (One Step)

First, total materials cost

• Product A 50 x $4,800 = $240,000

• Product B 2 x $5,200 = 10,400

• Product C 35 x $5,600 = 196,000

• Product D 175 x $7,400 = 1,295,000

Total $1,741,400

Second, the overhead rate

Total Overhead Costs $ 1,828,470

Total Materials Costs $ 1,741,400

= $1.05 per dollar of materials cost

(or 105% of materials cost)

Third, Overhead Cost for Product A per reel:

$4,800 x 1.05 = $5,040

Total Cost for Product A per reel

$4,800 + $5,040 = $9,840

One Step Cost per Batch = 50 x $9,840 = $ 492,000

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-26

ABC Costing – Product A

First, Overhead rate for Other Overhead:

Total Other Overhead Costs $1,586,470

Third, Total Cost for Product A per reel

• Materials $4,800

• Overhead

• Other OH $4,800 x .911= 4,373

• Slitting 2,294

• Grade Change $11,750/50 235

• Total Overhead 6,902

Total $11,702

Compare to One Step solution of $9,840

Also,

ABC cost per batch = $11,702 x 50 = $585,100

ABC Cost per Batch of Product A, figured directly

Materials $4,800 x 50 $240,000

Overhead

Other $240,000 x .911 218,640

(small difference due to rounding)

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

One Step

Materials Applied Total Total Batch Batch

Average No. cost per Price per Total Direct Overhead Cost Cost Total Gross

Product Slit Reels/Batch Reel Reel Materials Labor* per Reel per Reel per Batch Revenues Margin

A y 50 4,800$ 12,600$ 240,000$ 5,040$ 9,840$ 492,000$ 630,000$ 138,000$

B n 2 5,200 13,500 10,400 5,460 10,660 21,320 27,000 5,680

C y 35 5,600 14,200 196,000 5,880 11,480 401,800 497,000 95,200

D n 175 7,400 19,500 1,295,000 7,770 15,170 2,654,750 3,412,500 757,750

1,741,400$ 3,569,870$ 4,566,500$ 996,630$

Overhead Total Grade Change Slitting Net

Depreciation 800,000$ 8,000$ 70,000$ 722,000$

Indirect Labor 300,000 3,000 25,000 272,000

Energy 500,000 5,000 80,000 415,000

Other 198,470 1,000 20,000 177,470

Unrecoverable Clay,.. 30,000 30,000 –

Total 1,828,470$ 47,000$ 195,000$ 1,586,470$

Overhead Rate 1.05 = Total overhead divided by total materials

*little or no direct labor, omitted from cost calculations

Chapter 5 – Activity-Based Costing and Customer Profitability Analysis

5-28

ABC

Materials Total Total Batch Batch

Average No. cost per Price per Total Direct Grade Other Cost Cost Total Gross

Product Slit Reels/Batch Reel Reel Materials Labor* Change Slitting Overhead per Reel per Batch Revenues Margin

A y 50 4,800$ 12,600$ 240,000$ 235$ 2,294$ 4,373$ 11,702$ 585,103$ 630,000$ 44,897$

B n 2 5,200 13,500 10,400 5875 4,737 15,812 31,625 27,000 (4,625)

C y 35 5,600 14,200 196,000 335.71 2,294$ 5,102 13,332 466,606 497,000 30,394

D n 175 7,400 19,500 1,295,000 67.14 6,742 14,209 2,486,536 3,412,500 925,964

1,741,400$ 3,569,870$ 4,566,500$ 996,630$

Overhead Total Grade Change Slitting Net

Depreciation 800,000$ 8,000$ 70,000$ 722,000$

Indirect Labor 300,000 3,000 25,000 272,000

Energy 500,000 5,000 80,000 415,000

Other 198,470 1,000 20,000 177,470

Unrecoverable Clay,.. 30,000 30,000 –

Total 1,828,470$ 47,000$ 195,000$ 1,586,470$

ABC driver quantity 4 85 1,741,400$

ABC overhead rate 11,750$ 2,294$ 0.9110$

ABC Cost Drivers

Overhead Applied,per Reel