Chapter 19 – Strategic Performance Measurement: Investment Centers

19–31

Totals

$1,500,000

$1,000,000

$500,000

$500,000

$0

19–36 (Continued-3)

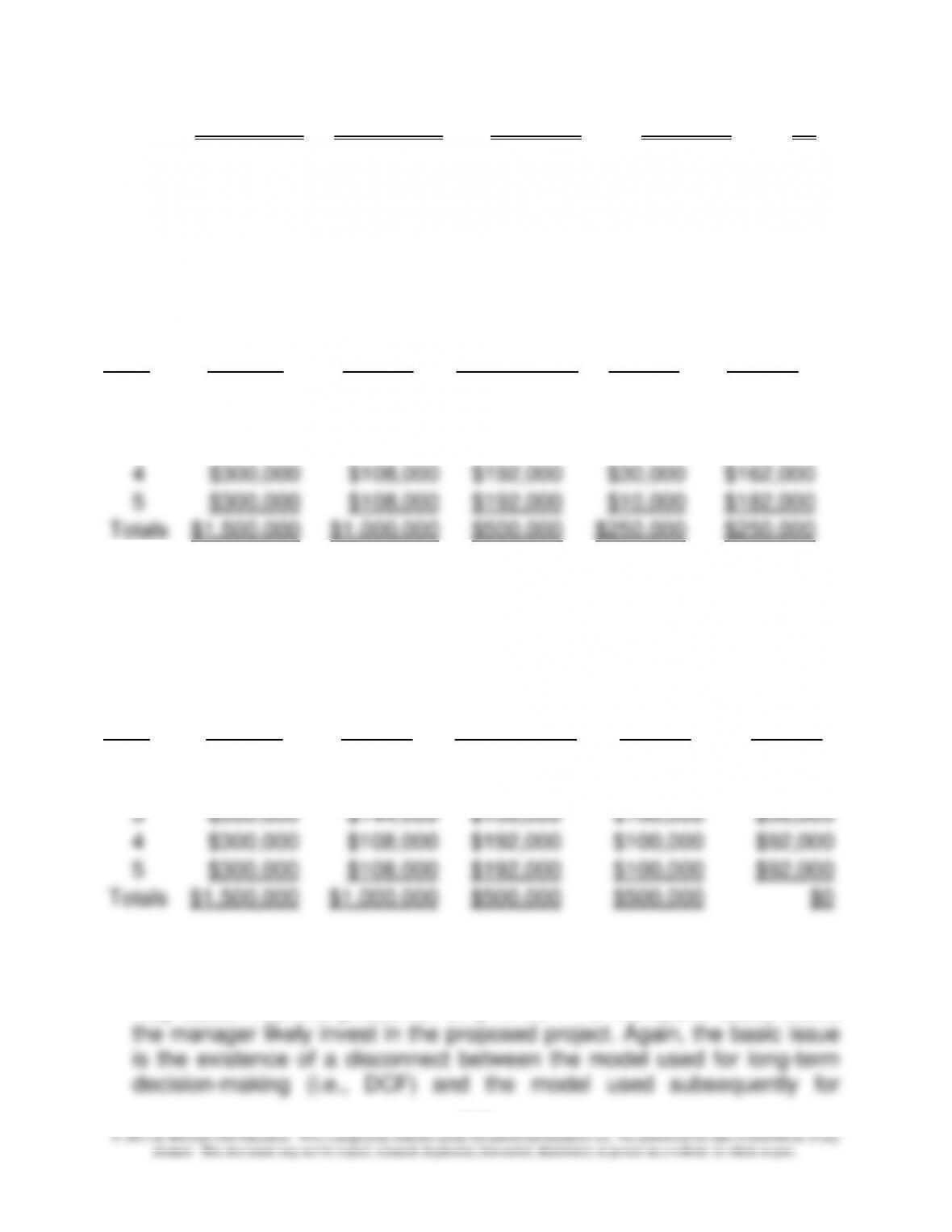

c. Using NBV as the investment base and DDB depreciation (per

requirement 4(1) above):

Year

Income

Prior to

Deprec.

Depreciation

Charge

Operating

Income

After

Depreciation

Less:

Imputed

Capital

Charge

Residual

Income

1

$300,000

$400,000

($100,000)

$90,000

($190,000)

2

$300,000

$240,000

$60,000

$70,000

($10,000)

3

$300,000

$144,000

$156,000

$50,000

$106,000

4

$300,000

$108,000

$192,000

$30,000

$162,000

5

$300,000

$108,000

$192,000

$10,000

$182,000

Totals

$1,500,000

$1,000,000

$500,000

$250,000

$250,000

d. Using GBV as the investment base and DDB depreciation (per

requirement 4(2) above):

Year

Income

Prior to

Deprec.

Depreciation

Charge

Operating

Income

After

Depreciation

Less:

Imputed

Capital

Charge

Residual

Income

1

$300,000

$400,000

($100,000)

$100,000

($200,000)

2

$300,000

$240,000

$60,000

$100,000

($40,000)

3

$300,000

$144,000

$156,000

$100,000

$56,000

4

$300,000

$108,000

$192,000

$100,000

$92,000

5

$300,000

$108,000

$192,000

$100,000

$92,000

Totals

$1,500,000

$1,000,000

$500,000

$500,000

$0

As shown by the results above, the use of accounting (i.e., accrual–

based) earnings numbers into the calculation of ROI introduces bias and

may cause incentive problems. Only in the 1st of the above cases would

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–32

assessing financial performance. One possibility, as discussed in the

text, would be to use “present-value” depreciation as a way to achieve

convergence between the two models. Another important lesson is the

19–36 (Continued-4)

need to supplement financial analysis with non-financial information

when making long-term investments and subsequently evaluating actual

performance.

An Excel file solution for this assignment is embedded (below) into this

Word solution file. To access the Excel file solution, place the cursor

anywhere over the object, right-click, choose “Worksheet Object,” then

choose “open.”

Pr. 19-36.xlsx

19–33

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

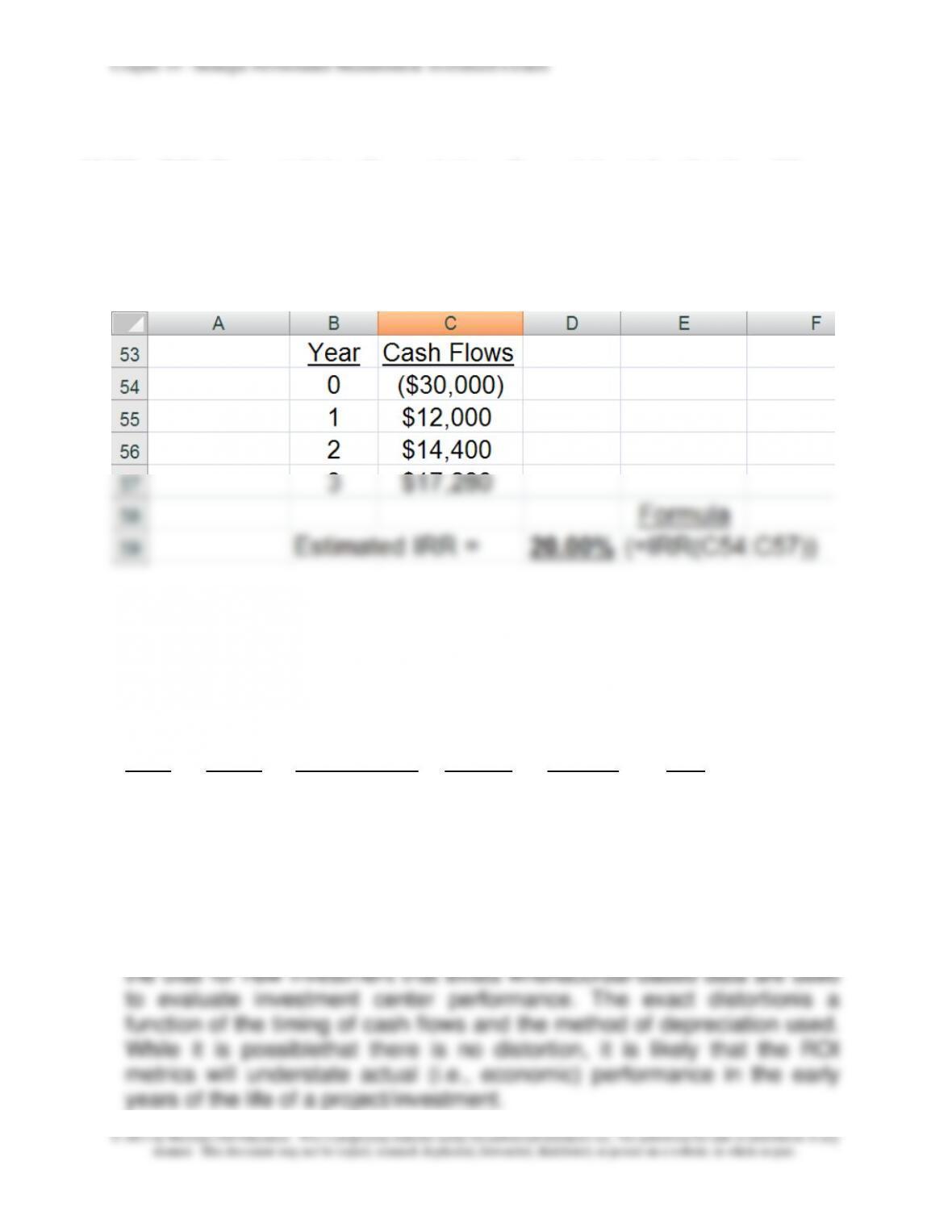

19–37 ROI, Present-Value Depreciation; Spreadsheet Application (60

Minutes)

1. Determining the IRR of the proposed investment (using the built-in

function in Excel):

2. Year-by-Year Accounting Rate of Return (SL depreciation);

Investment measured as beginning-of-year book value

BOY

Book

SL

Cash

Operating

Year

Value

Depreciation

Inflows

Income

ROI

0

1

$30,000

$10,000

$12,000

$2,000

6.67%

2

$20,000

$10,000

$14,400

$4,400

22.00%

3

$10,000

$10,000

$17,280

$7,280

72.80%

Given the required rate of return for this company (15%), this project will

appear unsatisfactoryin Year 1. The point of this example is to illustrate

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–34

19–37 (Continued-1)

3. Year-by-Year ROI, Present-Value Depreciation:

PV of Cash

Decrease

Cash

Inflows (@

in PV of

Year

Flows

20%)

the Asset

0

($30,000)

$30,000

1

$12,000

$24,000

$6,000

2

$14,400

$14,400

$9,600

3

$17,280

$0

$14,400

BOY Book

PV

Cash

Operating

Year

Value

Depreciation

Inflows

Income

ROI

1

$30,000

$6,000

$12,000

$6,000

20.00%

2

$24,000

$9,600

$14,400

$4,800

20.00%

3

$14,400

$14,400

$17,280

$2,880

20.00%

Summary:The use of present-value (i.e., “economic”) depreciation

reduces the negative incentive effects illustrated above in part 2.

4. Estimated Year-by-Year Residual Income (RI), Present-Value

Depreciation:

Year

1

2

3

Cash Inflows

$12,000

$14,400

$17,280

Present Value

Depreciation

$6,000

$9,600

$14,400

Imputed Capital Charge:

$30,000 × 0.10 =

$3,000

$24,000 × 0.10 =

$2,400

$14,400 × 0.10 =

$1,440

Residual Income (RI) =

$3,000

$2,400

$1,440

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–35

19–37 (Continued-2)

Using the built-in function (NPV) in Excel, we estimate the following:

Estimated NPV of RIs, at 10% =

$5,793

Estimated NPV of Investment, at 10% =

$5,793

Summary: For an economically desirable project (as in the case here:

IRR > 10%), the RI for each year of a project’s life will be positive so

long as present-value depreciation is used in the calculations. That is, if

PV depreciation is used, then the RI each year will be > $0 when we

accept an economically desirable investment. The use of RI(with PV

depreciation) for assessing financial performance is analogous to the

use of NPV for capital budgeting purposes, as illustrated above. This

brings together the twomodels: one for making the investment decision

(NPV), and the other for evaluating subsequent performance (RI, with

PV depreciation).

An Excel file solution for this assignment is embedded (below) into this

Word solution file. To access the Excel file solution, place the cursor

anywhere over the object, right-click, choose “Worksheet Object,” then

choose “open.”

Pr. 19-37.xlsx

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–36

19–38 Return on Customer; Review of Chapter 5 (15-20 minutes)

ROC for Customer X:

ROC = $25,000 + ($75,000 – $150,000)

$150,000

ROC for Customer Z:

While there are currently more profits on customer X sales, the future is

much more promising for customer Z. The CLV for customer Z has

increase by $50,000, while the CLV for customer X has fallen by $75,000.

The ROC measure can be used to target sales manager’s attention to

important changes in customer values. In this case, perhaps rewards are

in order for the sales people who have developed customer Z, and some

attention should be directed to correcting an unfavorable change in the

expected sales profits from customer X; are we losing X as a customer, or

has there been an unfavorable change in the sales mix to this customer,…

Source: Don Peppers and Martha Rogers, Return on Customer,

Doubleday, New York, 2005.

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–37

19–39 Research Assignment, Strategy (60 minutes, including reading time)

1. As the authors note on page 123 of their article, “Globalization has left

only one true path to profitabilityfor firms operating in high-wage,

developed nations: to base their competitive strategy on exceptional

human capital management (HCM).” In the past, these same firms may

have been able to secure sustainable competitive advantage by

managing their financial or physical capital. Performance-measurement

systems for managing such assets are well-developed and key to

traditional managementaccounting and control systems. The

2. The overall purpose of the framework proposed by the authors is to

establish empirical linkagesbetween “people” (or, the quality of HCM)

and organizational performance (e.g., sales revenue, factory safety,

student scores on standardized tests, or stock-market returns).

Conceptually, the authors aretrying to model key HCM drivers of

organizational performance. These drivers fall into the followingfive

used to rate theorganization on the range of HCM practices across the

five major categories.

From the standpoint of a management accounting and control system,

the key imperative is tofocus, for the given organization, on the most

important HCM drivers of organizational success. This requires a

statistical analysis between HCM scores over time (or across

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–38

organizational units) and keyorganizational outcomes (such as

employee commitment or financial performance). Such analysis can

19–39 (Continued-1)

take various forms, from the simple (e.g., looking for statistically

significant differences betweenorganizational subunits) to the complex

(e.g., using nonlinear, multiple regression). Once the mostthe key

driver.

3. Examples:

Example #1—Improving Sales and Safety Performance at American

Standard Companies (manufacturer):survey data were gathered from

more than 300 corporate locations.

Drivers of Sales Performance: By analyzing survey scores across

different units, the company was able to determine that the following

three HCM factors were most highly correlated with sales

performance: executive and supervisory skills (both of which were in

the “Leadership Practices” category), information sharing (in the

“Knowledge Accessibility” category), and innovation (in the

“Learning Capacity” category).

Drivers of Plant Safety Performance: A similar study revealed a

relationship between certain HCM practices and accident rates.

Safer plants excelled in three major areas: (1) supervisory skills (in

the “Leadership Practices” category), (2) information sharing (in the

“Knowledge Accessibility”category), and (3) supporting employee

skill development (in the “Learning Capacity” category).

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–39

19–39 (Continued-2)

Example #2—Improving Student Test Scores (public school system):

survey data in this case were collected from South Carolina’s Beaufort

County School District, which was realizing below-average scores on

state achievement tests taken by its students. The goal was to identify

and manage the HCM practices that had the most positive effect on

(mean) student performance scores.Cross-sectional data from various

school districts in the state indicated a positive relationship between total

Specific drivers of performance, uncovered during the statistical analysis

of results, included items such as teachers’ overall work culture, learning

culture, and the school’s ability to reinforce and retain talent.

Example #3—Increasing Stock Returns in Financial Services Firms: the

authors collected total HCMsurvey scores from 11 different publicly

traded financial services firms and correlated these scoreswith one-year

ahead stock-market performance (total returns) of these firms. This

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–40

19–40 Research Assignment: Employee Wellness Programs;

Sustainability (60 minutes, including reading time)

1. On page 106 the authors define “workplace wellness” as “an organized,

employer-sponsored program that is designed to support employees

2. The following evidence regarding the ROI of employee wellness

programs is offered by the authors of the article:

a. For Johnson & Johnson, over the period 2002 to 2008, the ROI on

such expenditures is estimated as $2.71 to $1.00 ($2.71 of savings for

every dollar spent); in absolute terms, these cost savings are

estimated as $250 million.

reduction in health-related lost days of work, $1.5 million; 50%

reduction in workers compensation premiums.

3. What do the authors of this article cite as important non-financial

performance indicators associated with corporate wellness programs?

a. J&J: reduction in number of employees that smoke, 2/3.

b. For the participants in the program referenced above in 2b, 57% of

those classified as “high–risk” (in terms of blood pressure, % body fat,

e. Increased employee productivity (p. 109)

f. Increased employee morale (p. 109)

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–41

19-40 (Continued-1)

g. See “Dashboard for Workplace Wellness Programs” (p. 111) for one

comprehensive model for capturing key benefits, both to employees

and to the company.

4. Six pillars of a successful, strategically integrated wellness program:

1. Multilevel Leadership (i.e., engaged leadership at multi levels,

including C-suite [e.g., Johnson & Johnson, MD Anderson Cancer

Center], middle management, wellness program managers, and

“wellness champions” [e.g., supermarket chain H-E-B]). Page 108:

testing and lifestyle surveys, development of signature wellness

programs, making such programs “fun” (examples: Healthwise,

Lowes, SAS), maintaining high standards (e.g., Comporium, SAS).

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–42

19-40 (Continued-2)

4. Accessibility—Page 109: “Convenience matters.” Focus on

eliminating reasons why employees would not take advantage of

programs and facilities.

5. Partnerships—both internal (e.g., with the Finance function, to vet

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–43

19–41 ROI and Sustainability; Internet-Based Research (time varies)

1. Alternative definitions are possible. In his book Making Sustainability

Work: Best Practices in Managing and Measuring Corporate Social,

Environmental, and Economic Impacts (San Francisco, CA: Berrett-

Koehler Publishers, Inc., 2008) Marc Epstein defines corporate

sustainability (p. 19) as the integration of corporate social,

environmental, and economic impacts into day–to-day management

financial performance.” (emphasis in original)

2. This question is designed to motivate a connection in the student’s mind

between the “corporate sustainability” movement (or at least philosophy)

and the design of management accounting systems. Ideally, students

should mention topics covered elsewhere in the course, e.g., activity–

based costing (ABC), life-cycle costing, financial performance measures

Alternatively, or in conjunction with the above point, the instructor can

offer to students the following statement from Epstein (2008, p. 51),

which highlights a leading role that management accounting can play in

terms of supporting corporate sustainability programs and initiatives:

“An effective performance evaluation system (is needed) to integrate

economic, environmental, and social objectives and (to) reward the

19–44

19–41 (Continued-1)

3. Student answers (based on individual internet searchers conducted)

should differ. The purpose of this question is to motivate discussion

regarding the financial benefits of sustainability projects and programs,

which benefits can be impounded in traditional decision models such as

ROI and NPV. Following are some “talking points” or sample responses:

a. financial benefits associated with product/process designs: reduction

in water and energy usage; decreased cost of waste handling and

d. avoidance of loss sales, loss market share, and other negative

reputation effects such as diminished brand value, customer boycotts,

or protests (again, while determining the precise value here is

Chapter 19 – Strategic Performance Measurement: Investment Centers

19–45

4. Again, student answers will differ here. The main point is to have

students think of a broader set of evaluation criteria—both financial and

non-financial in nature—in terms of evaluating corporate sustainability

projects and programs. Presented below is a set of sample responses.

a. risk (social, environmental, and political) reduction

19–41 (Continued-1)

e. listing on the Dow Jones Sustainability Group Indexes

(http://www.sustainability-index.com/), the FTSE4Good Index Series

(http://www.ftse.com/Indices/FTSE4Good_Index_Series/index.jsp),

MSCI ESG Indices, which (according the following website) “are

designed to help clients incorporate environmental, social and

governance (ESG) factors into their investment decisions”

(http://www.msci.com/products/indices/thematic/esg/), or the

AccountAbility ratings provided by AccountAbility

(http://www.accountability.org/) (these ratings are designed to

measure the extent to which companies have integrated sustainability

into their business practices—ratings are based on scores in six

categories: three external drivers (public disclosure, assurance, and

stakeholder engagement) and three internal drivers (governance,

strategic intent, and performance measurement).