Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–62 (continued -2)

The formulas for the above spreadsheet are as follows:

Total Net Sales ($6,875,000 Hartford; $5,625,000 Boston) 12500000

Fixed Costs

Partly Traceable and Controllable 400000

Partly Traceable but Noncontrollable 350000

Nontraceable Costs 325000

=SUM(D3:D5)

Total Net Sales

Boston 5625000

Hartford Total Sales 6875000

Hartford Clothing 0.6

=A10 Cycle&Run 0.4

Cost of Goods Sold (Variable) Percent of Sales

=A8 0.6

=A10 =B10 0.7

=A11 =B11 0.5

Variable Operating Costs Percent of Sales

=A14 0.3

=A15 =B15 0.25

=A16 =B16 0.35

Total Variable Costs Percent of Sales

=A19 =D14+D19 =60% + 30%

=A20 =B20 =D15+D20 =70% + 25%

=A21 =B21 =D16+D21 =50% + 35%

Fixed Controllable Costs Percent of Total Cost

=A19 0.45

=A20 Total 0.4

=B10 0.5

=B11 0.3

Could not be Traced to Clothing or Cycling at Hartford 0.2

Could not be Traced to Boston or Hartford 0.15

Fixed Noncontrollable Costs Percent of Total Cost

=A14 0.4

=A15 Total 0.5

Income Statement by Business Unit

Combined

Company Not Allocated =A8 =A10

Net Sales =E48+F48 =D8 =D9

Variable Costs:

COGS =E50+F50 =E48*D14 =((D10*D15)+(D11*D16))*F48

Operating Costs =E51+F51 =D19*E48 =((D10*D20)+(D11*D21))*F48

Less: Noncontrollable Fixed Costs =D4 =D4*D42 =D4*D37 =D4*D38

Contribution by Profit Center =C56-C58 =C59-E59-F59 =(E56-E58) =(F56-F58)

Less: Nontraceable Costs =D5

Operating Income =C59-C61

Breakdown of contribution: =F47

=F47 Not Allocated =B10 =B11

Net Sales =F48 =F48*D10 =F48*D11

Variable Costs:

COGS =F50 =D15*E68 =D16*F68

Variable Operating Costs =F51 =D20*E68 =D21*F68

Total Variable Costs =F52 =SUM(E70:E71) =SUM(F70:F71)

Contribution Margin =F53 =(E68-E70-E71) =(F68-F70-F71)

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–85

18-62 (continued -3)

2. The results of the contribution income statement analysis shows

that both stores are profitable and approximately equally

profitable as measured by contribution by profit center ($242,500

for Boston and $283,750 for Hartford). After nontraceable fixed

costs OWI’s operating income is $106,250, less than 1% of total

sales, a relatively low operating profit. The profit breakdown for

the Hartford store shows that the contribution of the Cycle & Run

center accounts for most of the profit for the store. Given the cost

estimates, this is not surprising. Note that the variable cost

percentages for the two stores is as follows. Adding the variable

The analysis shows that management needs to look for ways to

control variable costs, both in cost of purchases for resale and in

operating costs. A good start might be to research industry

publications and trade organizations to find benchmark data for

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–86

18-63 Choice of Strategic Business Unit (20 min)

1. The new office of sustainability is a support department and as such

should be evaluated as a cost center, and since the outputs of the

department will be difficult to measure, at least initially, it should be

established as a discretionary cost center. The department would

likely search for alternatives in the size and type of engines in the

A different approach would be to consider the department a

profit center based on the idea that effective steps to reduce carbon

emissions could not only save the firm fuel costs, but could also be

used to generate revenue. This could be accomplished by using

achievements in sustainability to attract new customers who value the

reduced costs and also value the positive effects on the environment.

2. This new department would best be evaluated as a profit center since

its mission is to develop new products and to refine existing products

in order to attract new customers and increase sales. The costs of

new department should be matched against the increased revenues

3. This department is best evaluated as a discretionary cost center. The

goal of the department is to identify risk and to make plans

accordingly. It would be difficult to tie this activity to revenues.

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–87

18-64 Research Assignment; Sustainability (45 min)

The project upon which the article is based is a research project funded by

the Institute of Management Accountants (IMA). Suggested solutions for

each of the discussion questions follow:

1. What is the difference between local and corporate decision making,

and what is the significance of the difference for sustainability?

In the article, Epstein et. al. refer to local versus corporate decision making.

Local decision making is done at the level of business units, geographical

units (such as the State of Ohio), or facilities. The corporate level is at the

company headquarters. The difference is important because, as the

article suggests, many sustainability-related decisions are made at the local

executive responsible for corporate sustainability goals will set the tone and

the objectives, but ultimately many of the decisions that involve

sustainability are made at the local level.

Corporate decisions would include the decision to replace a fleet of less

efficient vehicles with more efficient vehicles, or to refit a plant for more

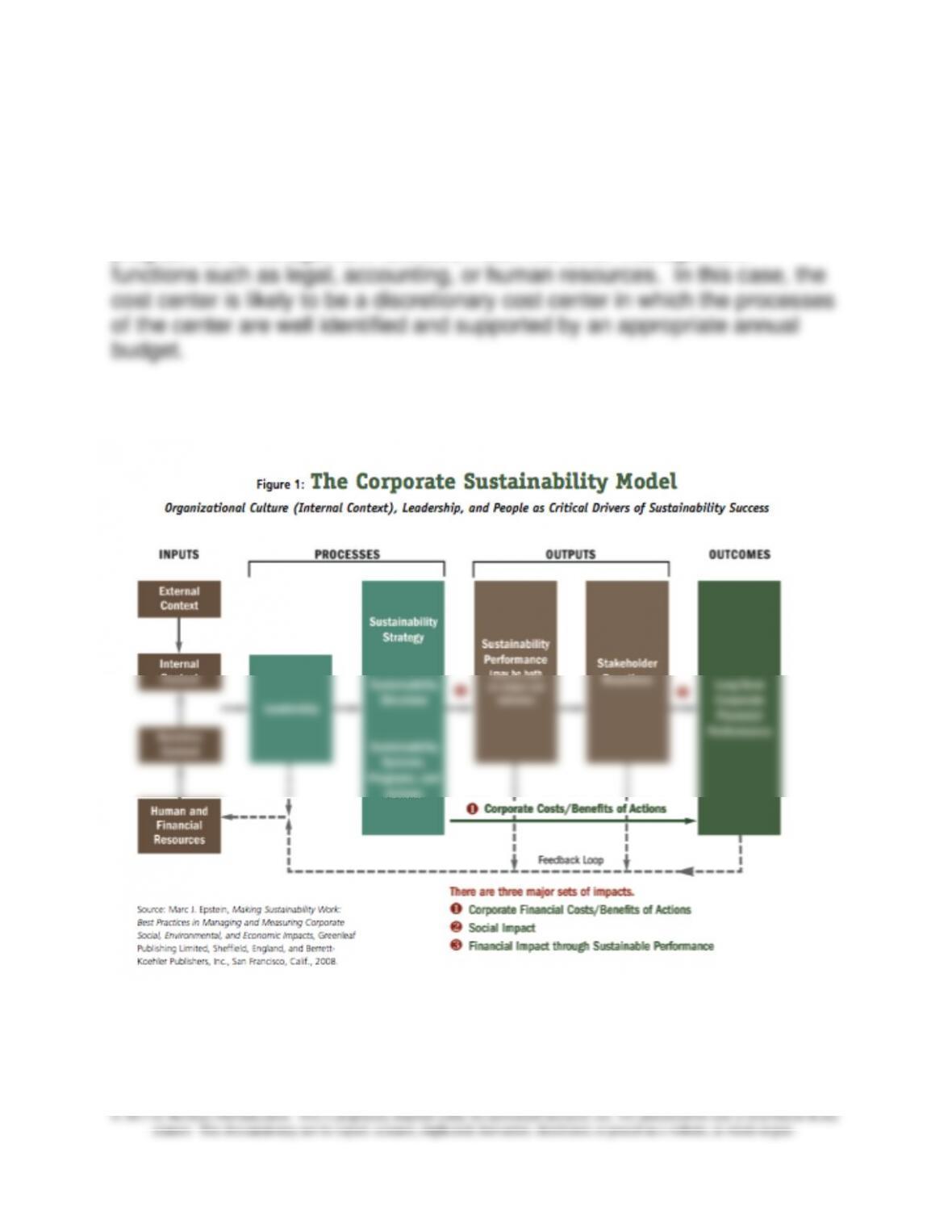

2. Study the Corporate Sustainability Model in Figure 1. Based on this

study, do you think sustainability should be managed by means of a

cost center, profit center, the balanced scorecard, or some other

method, and why? (Figure 1is shown on the following page.)

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–88

18-64 (continued –1)

Each of these options could be supported in some ways. The cost center

would be appropriate for an organization that is managing its sustainability

program as a management function, much like other management

18–89

18-64 (continued –2)

A profit center approach would recognize that, as many companies have

discovered, the efforts to improve sustainability have a positive impact on

profitability. In this case, a variation of the cost center, the processes of

the center are carefully defined. The difference is that the sustainability

profit center is expected to provide improvements in operations that reduce

measures could simply be part of the scorecard along with the

environmental and other sustainability measures.

3. Identify two of the leading companies in the area of sustainability and

explain why you think each of these companies has chosen to take a

leadership role in sustainability.

The article identifies four companies: Nike, Procter & Gamble (P&G), The

Home Depot and Nissan. The articles notes that these companies have a

reputation for leadership in sustainability and therefore the authors chose

18–90

18-64 (continued –3)

At The Home Depot and Nissan, sustainability was top-down, driven by

strategic planning, coordinated with the business units, with the goal of

both corporate responsibility and cost reduction.

4. Review Exhibit 18.4 in the text. Do you think sustainability is best

managed as part of an informal or a formal type of management

control system? Briefly explain your answer.

5. Explain briefly the role of leadership in sustainability management.

Leadership is critical, as noted in the article. Setting a clear tone and

policy at the corporate level can reduce conflicts and miscommunication at

6. Explain briefly the role of organization culture in sustainability

management.

The company’s culture, throughout the organization also plays a critical role

in achieving the company’s sustainability objectives. At Home Depot for

example, the culture of willingness to take a risk and the passion for

Chapter 18 – Strategic Performance Measurement: Cost Centers, Profit Centers, and the Balanced Scorecard

18–91

18-64 (continued -4)

Additional Source: See also an excellent coverage of sustainability at

P&G in the article by Cristiano Busco, Mark. L. Frigo, Emilia L. Leone, and

Angelo Riccaboni, “Cleaning Up,” Strategic Finance, July 2010, pp. 29-37.