Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-1

CHAPTER 14: OPERATIONAL PERFORMANCE MEASUREMENT:

SALES, DIRECT-COST VARIANCES, AND THE ROLE OF

NONFINANCIAL PERFORMANCE MEASURES

QUESTIONS

14-1 A master budget represents forecasted operating profit based on a single output

level (“planned sales”) for an upcoming period. As such, this budget is also

referred to as a static budget.

Pro-forma budgets represent budgeted operating income for various output

levels (production or sales). Pro-forma budgets can be prepared for any output

level within the relevant range.

flexible-budget variance. For this reason, some accountants refer to this budget

as a “control budget.”

14-2 Standard costs (and selling prices), and their use in the construction of flexible

budgets (prepared after the current operating period is over), establish targets or

unit, and total fixed costs.

14–3 Management time is scarce. According to the philosophy of management by

exception, managers give primary attention to things (operations, sales

promotions, production, revenue growth, productivity gains, etc.) that are not

going according to plan, or at least are departing materially from plan. The

part of managers is needed. On the other hand, when a variance is consider

“abnormal” (i.e., an “exception”) it may trigger the need for an investigation to

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-2

uncover the underlying cause, which in turn may lead to some type of

intervention or change.

14-4 The performance of a division should not be considered as less than satisfactory

simply because all variances are “unfavorable.” For example, a company

expects unfavorable variances if it uses an ideal performance standard. As long

as there is making satisfactory progress toward the standard, unfavorable

and every operation.

14-5 Direct material price variances can be caused by any of the following factors:

purchasing material of a different quality than that envisioned in the standard

material cost; inapplicability of the standard cost per unit of raw material (i.e.,

outdated standards—the market price may have changed); purchasing was done

through a new supplier; delivery terms for purchases were different (and

therefore either more or less costly) than the terms envisioned when the standard

material costs were set; skill (or lack thereof) of the purchasing manager in

Direct materials usage variances can be caused by: poorly supervised

employees; inadequately maintained machinery and equipment; inappropriate

standard (e.g., standard is out–of-date, or the standard was set incorrectly); or,

the use of non-standard raw materials. Normally, the Production Manager is in

the best position to influence the direct materials usage (quantity) variance. Note,

however, that this variance might also be affected by decisions made by the

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-3

14-6 Direct labor rate (price) variances could be caused by: highly skilled (and paid)

labor used in place of lower-skilled labor; standard is out of date (e.g., new labor

contract); or, overtime work that is included in direct labor cost (rather than

manufacturing overhead). In some cases, the Production Manager is in the best

position to influence the direct labor rate (price) variance because this individual

relates to how labor is deployed in the organization (e.g., skilled workers who are

paid more may be assigned to do tasks meant for lower-paid workers). In other

labor usage (efficiency) variance. However, this variance (as noted in 14–5

above) may be assigned to the Purchasing Manager if the purchase of inferior

materials caused excess labor-hour consumption.

One particularly interesting situation that students should be aware of is the

potential for overemphasizing labor efficiency variances when labor is essentially

a short-term fixed cost. In this case, the labor efficiency variance can be largely

attributable to lack of orders (i.e., lack of sales demand), not worker efficiency.

For this reason, some writers suggest that when labor is essentially a short-term

14–7 The answer depends on how overtime premium is treated by the accounting

system. If overtime premium is included as part of factory overhead, then the

higher wages paid due to overtime premium should not affect any direct labor

variances. However, for firms that include overtime premium in the total wages,

prospects of the firm. In short, the labels “favorable” and “unfavorable” are

defined solely on the basis of the impact of the variance (positive or negative) on

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-4

short-term operating profit. It is a value judgment as to whether such variances

are positive or negative.

14-8 Of the three, for motivation and control purposes, standards based on the

average of recent historical performance are the least desirable. Many firms

prefer to use standards based on attainable performance in their standard cost

14-9 Establishing a standard cost system and identifying variances from the standard

are steps in gaining a better understanding of the operations and improving

operations. The focus of a standard cost system should be on influencing

excessive pressure, inflexibility, uneven reward systems, or excessive emphasis

on short-term financial results (profits) can all compromise the benefits of a

standard cost system.

14–10 Organizations engage in a variety of processes in order to deliver the stated

value proposition to its targeted customers and in order to achieve its stated

financial objectives. These processes, for expository purposes, might be grouped

materials from supplier firms; producing finished goods and services; and,

distributing the finished product to customers.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-5

14–11 A JIT system is very different from a conventional manufacturing system. In a JIT

system, a good or service is produced or delivered only when a customer

requires it. Some describe this as “demand pull” rather than “push.”

JIT production requires a product layout with a continuous flow once

production starts. Underlying the JIT system is a continuous improvement

philosophy of eliminating or reducing delay, error, and waste, such as materials

goods. All types of inventories are kept on hand in case unforeseen events

occur. Little attention is given to studying efficient and inefficient activities, and

materials movement, storage, rework, and waiting time are part of the

conventional work environment.

Financial benefits resulting from a shift to cellular manufacturing, just–in–time

production, or continuous quality improvements may include the following:

1. Increased sales because the short production cycle time enables a

company to win customers by cutting the delivery time.

5. Reduced clerical costs for keeping inventory records.

6. Reduced financing costs of inventories

The adoption of a JIT philosophy affects the organization’s management

accounting and control system in two primary ways:

1. To support the move to JIT, the accounting system needs to monitor

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-6

14–12 We might define total customer response time as the amount of time between

the time a customer places an order and the time when that order is received by

the customer. Manufacturing (production) cycle time can be defined as the

time-lapse between when the manufacturing department receives the order and

when the order is completed (i.e., when finished goods are created). (Note:

PCE = processing time ÷ total manufacturing time

PCE = processing time ÷ (processing time + moving time + storage

time + inspection time)

Alternatively, we can view PCE as the ratio of “value–added time” to the sum of

“value–added time” + “non-value-added time.” These terms are defined, and

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-7

BRIEF EXERCISES

14–13 Budgeted (Pro-forma) Operating Profit = (cm/unit × #units) − FC

14–14 Total static (master) budget variance = actual operating income − static (master)

budget operating income

14–15 Sales volume variance = budgeted cm/unit × (actual sales volume − master budget

sales volume)

14–16 Sales price variance = actual sales volume × (actual − budgeted) selling price/unit

= AQ × (AP − SP)

14–17 Total static (master) budget variance in operating profit = actual operating profit −

static (master) budget operating profit

Sales volume variance in operating income = flexible-budget operating income −

master budget operating income

Flexible-budget variance = actual operating income − flexible-budget operating

income

= $30,000 − $35,000 = $5,000U

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-8

14–18 Direct materials usage (quantity) variance for PVC = Standard price/lb. × (actual lbs.

used – standard quantity of lbs. that should have been used, given the actual

output for the period)

14–19 Purchase price variance for PVC = actual pounds purchased × (actual – standard)

price/lb.

14–20 Flexible-budget variance for PVC = actual PVC cost for units produced – FB cost

= (actual price/lb. × actual lbs. used) – (actual output × standard #lbs./unit of

output × standard price/lb.)

14–21 Direct labor efficiency variance = standard wage rate/hr. × (actual – standard) direct

labor hours= SP × (AQ − SQ)

14–22 Direct labor rate (price) variance = actual hours worked × (actual – standard) wage

rate/hr.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14-9

EXERCISES

14-23 Financial versus Operational Control; Behavioral Considerations in the

Standard-Setting Process (20 minutes)

As indicated in the text, we use the term “management accounting and control

system” to refer to the entire set of procedures and systems used by an organization

to monitor activities and guide actions in support of the overall goals and objectives

of the organization. As such, a comprehensive management accounting and control

While terminology may differ across textbooks and organizations, one useful way to

conceptualize feedback/performance evaluation systems is to view such systems as

consisting of two primary components: a financial control system and an operational

control system. The goal of the former system is to monitor financial results to

determine whether the organization is on-track in terms of its specified financial

One dimension of a financial control system is the use of flexible-budgets, standard

costs, and variance analysis—covered in Chapters 14, 15, and 16 of the text. In

essence, such procedures assess both effectiveness (e.g., did we attain budgeted

operating profits or budgeted sales volume for the period) and efficiency aspects of

financial performance (e.g., whether the purchasing department secured a favorable

price for materials purchased for production, or whether the organization used labor

No management accounting and control system is good or bad per se. Each is

judged, at least conceptually, by comparing costs and benefits. Among the more

important considerations are behavioral considerations. For example, one

consideration relates to the standard-setting process. Should standards be imposed

(authoritative), should employees whose performance will be judged develop the

standards (participative), or should the organization use a consultative process in

developing such standards?

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–10

14–24 Financial versus Nonfinancial Performance Indicators for Operational Control

(15 minutes)

Repetitive operations, such as consumption of power (or direct materials) in an

automated manufacturing facility, require constant feedback and data to ensure that

the underlying process is “in control.” That is, the managers of such operations

cannot wait for financial reports in order to correct (put back into control) a

malfunctioning process. In this context, real-time nonfinancial performance

operating personnel are familiar with.

On the other hand, managers are likely to be more interested in financial operating

results, for several reasons. One, the performance of managers is often judged on

the basis of financial results. Two, financial metrics provide decision-makers with a

common unit that can be used to evaluate the economic effects of different courses

of action (e.g., changes in sources of supply, product mix, etc.). Operating

personnel might also be interested in financial performance indicators. For

example, such measures communicate to such individuals the “bottom–line” impact

of their decisions and operating efficiencies.

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–11

14–25 Behavioral Considerations (40- minutes)

1. Managerial time can be considered a scare resource. Time spent in terms of

securing operational control detracts from time spent dealing with issues of a more

strategic (or long-term) nature. For this reason, many managers embrace a

managerial philosophy known as “management by exception.” When variances

(e.g., labor cost variances) are considered immaterial, no intervention on the part

of management is required: the underlying system is considered to be “in control.”

When the variances are considered “large” or “material,” some kind of intervention

operating problems. Assuming standards are “internalized,” they may properly

motivate employees to work more efficiently, an important element of “control.”

2. A standard cost system can have a negative impact on worker motivation if the

standards are too “loose” (i.e., too easily attainable) or too “tight” (i.e., too difficult

to attain). In the former case, the standards tend to reduce productivity; in the latter

case, in the extreme, employees simply ignore the standards—that is, they do not

“internalize” the standards as legitimate goals. Some research in management

should not, as in the case of Chen, Inc., be used to assign “blame.” Rather, they

should be used positively to motivate continual operating improvements.

3. The purpose of this question is to get students to think about the strategic role of

standard costs and flexible budgets in a comprehensive management accounting

and control system. In this regard, students should think about both the costs and

benefits of using these elements of a traditional financial control mechanism.

Finally, the question should expose students to some of the current controversies

surrounding the use of standard costs and flexible budgets in “the new

manufacturing environment.” As such, students (particularly undergraduate

Criticisms/Limitations of Conventional Standard Cost Variance Analysis

1. Variances are too aggregated and concentrate on consequences rather than

the causes of problems. This criticism, in fact, gets to the heart of the issue:

whether traditional standard cost variance analysis provides useful information

for operational control purposes.

2. Traditional standard cost variance reports are too late to be useful. In order to

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–12

take prompt managerial action, accounting information should be timely. Due to

the use of modern scanning technologies, manufacturers can now monitor in

14–25 (Continued-1)

real time the consumption of resources (e.g., labor and materials). Traditional

3. Standard costing systems tend to focus too heavily on cost minimization. For

companies competing on the basis of cost (i.e., those pursuing a cost–

4. Standard costing systems take a departmental perspective rather than a

process perspective. The point here is that traditional standard costing systems

are not “integrated.” As such, each department or cost center tends to focus on

can be viewed either as one of goal congruency or of local vs. global

optimization.

5. Too much emphasis is placed on the cost and efficiency of direct labor.

Traditional systems focus on the analysis of labor and material cost variances,

6. JIT Manufacturing: JIT is a strategy that requires continuous working to improve

quality and reduce costs. Some question whether traditional standard cost

7. Standard costs become out-dated quickly due to shorter product life cycles.

8. Some critics maintain that the use of standard costs and variances (via flexible

budgets) is misplaced in terms of securing operational control. These critics

maintain that operating personnel perform or participate in one or more

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–13

Benefits/Advantages of Using a Standard Cost System

1. Provides a good basis for cost comparisons. To the extent that “cost” is a

critical variable on which the organization competes, a standard cost system

14–25 (Continued-2)

2. Enables managers to use management by exception. As noted above, a

standard cost system can be viewed as a “diagnostic control system,” which

monitors itself and therefore frees management to attend to more strategic

issues confronting the organization.

3. Provides a basis for performance evaluation and determining bonuses. Again,

the key here is that managers who decide to use standard costs and variances

5. Standard costs can be used for external reporting purposes (as long as such

standards do not deviate significantly from actual costs).

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–14

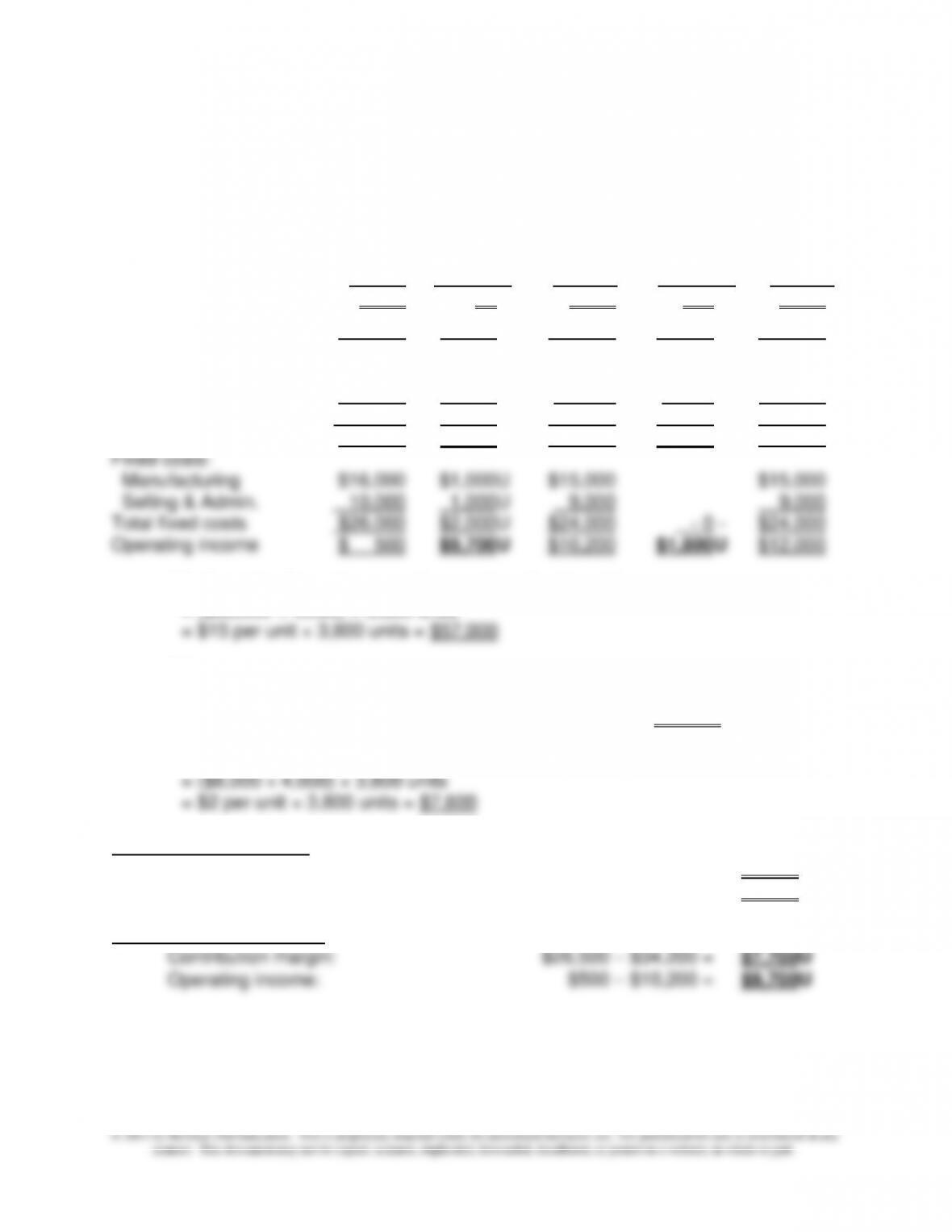

14–26 Flexible Budgets and Operating Income Variance Analysis; Spreadsheet

Application (45 minutes)

1. Flexible- Sales

Budget Flexible Volume Master

Actual Variance Budget Variance Budget

Units 3,800 – 0 – 3,800 200U 4,000

Sales $53,200 $3,800U $57,000 1 $3,000U $60,000

Variable costs:

Manufacturing $19,000 $3,800U $15,200 2 $800F $16,000

Selling & Admin. 7,700 100U 7,600 3 400F 8,000

Total variable costs $26,700 $3,900U $22,800 1,200F $24,000

Contribution margin $26,500 $7,700U $34,200 $1,800U $36,000

1 Budgeted selling price per unit × number of units sold

= ($60,000 ÷ 4,000) × 3,800 units

2 Standard variable manufacturing cost per unit × number of units sold

= ($16,000 ÷ 4,000) × 3,800 units

= $4 variable manufacturing cost per unit × 3,800 units = $15,200

3 Standard variable selling and administrative expense per unit x number of units

Sales volume variances

In terms of contribution margin: $34,200 − $36,000 = $1,800U

In terms of operating income: $10,200 − $12,000 = $1,800U

Flexible-budget variances

Chapter 14 – Operational Performance Measurement: Sales, Direct-Cost Variances, and the Role of Nonfinancial

Performance Measures

14–15

14–26 (continued)

2. The company reduced its selling price (from $15 per unit to $14 per unit) to compete

in the market, suggesting the pursuit of a cost-leadership, not a differentiation,

competitive strategy for the product. However, the company failed to exercise proper

control of its operating costs, as indicated by unfavorable variances for

The company has unfavorable selling price and sales-volume variances. Even

though the company reduced its selling price, it failed to attain the budgeted sales

volume. The strategy of competing through reduced selling prices to gain sales has

apparently failed.

3.

Note: An Excel spreadsheet solution file is embedded below. You can open this

“object” by doing the following:

Flexible Flexible Master

Budget Budget Budget

Units 3,750 4,150 4,000

Sales $56,250 $62,250 $60,000

Variable costs:

Manufacturing $15,000 $16,600 $16,000

Selling and Admin. $7,500 $8,300 $8,000

Total variable costs $22,500 $24,900 $24,000

Contribution margin $33,750 $37,350 $36,000