Chapter 12 – Strategy and the Analysis of Capital Investments

12–61

12–50 (Continued-2)

PV of Cash Inflows, at t = 0:

High: (=NPV(0.15,70,70,70)) ÷ (1 + 0.15) = $138.9789 million

Medium: (=NPV(0.15,50,50,50)) ÷ (1 + 0.15) = $99.2707 million

Low: = $0 (do not invest in this situation) $0 million

PV of Cash Outflows, at t = 0:

High: $100 million ÷ (1 + 0.05) = $95.2381 million

Chapter 12 – Strategy and the Analysis of Capital Investments

12–62

12–51 Real Options and Sensitivity Analysis(60 Minutes)

1.

ORIGINAL ASSUMPTION:

WACC =0.15

Risk-Free Rate =0.05

Scenario

p

Year 1

Year 2

Year 3

Year 4

@ t = 0

PV of

Outflows

@ t = 0

PV of

Inflows

Weighted

NPV (@ t =0)

High

0.25

($100.00)

$70

$70

$70

($95.2381)

$138.9789

$10.935

Medium

0.50

($100.00)

$50

$50

$50

($95.2381)

$99.2707

$2.016

Low

0.25

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

Expected NPV =

$12.951

WACC =0.15

Risk-Free Rate = 0.05

Scenario

p

Year 1

Year 2

Year 3

Year 4

@ t = 0

PV of

Outflows

@ t = 0

PV of

Inflows

Weighted NPV

(@ t =0)

High

0.20

($100.00)

$70

$70

$70

($95.24)

$138.98

$8.748

Medium

0.50

($100.00)

$50

$50

$50

($95.24)

$99.27

$2.016

Low

0.30

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

Expected NPV =

$10.764

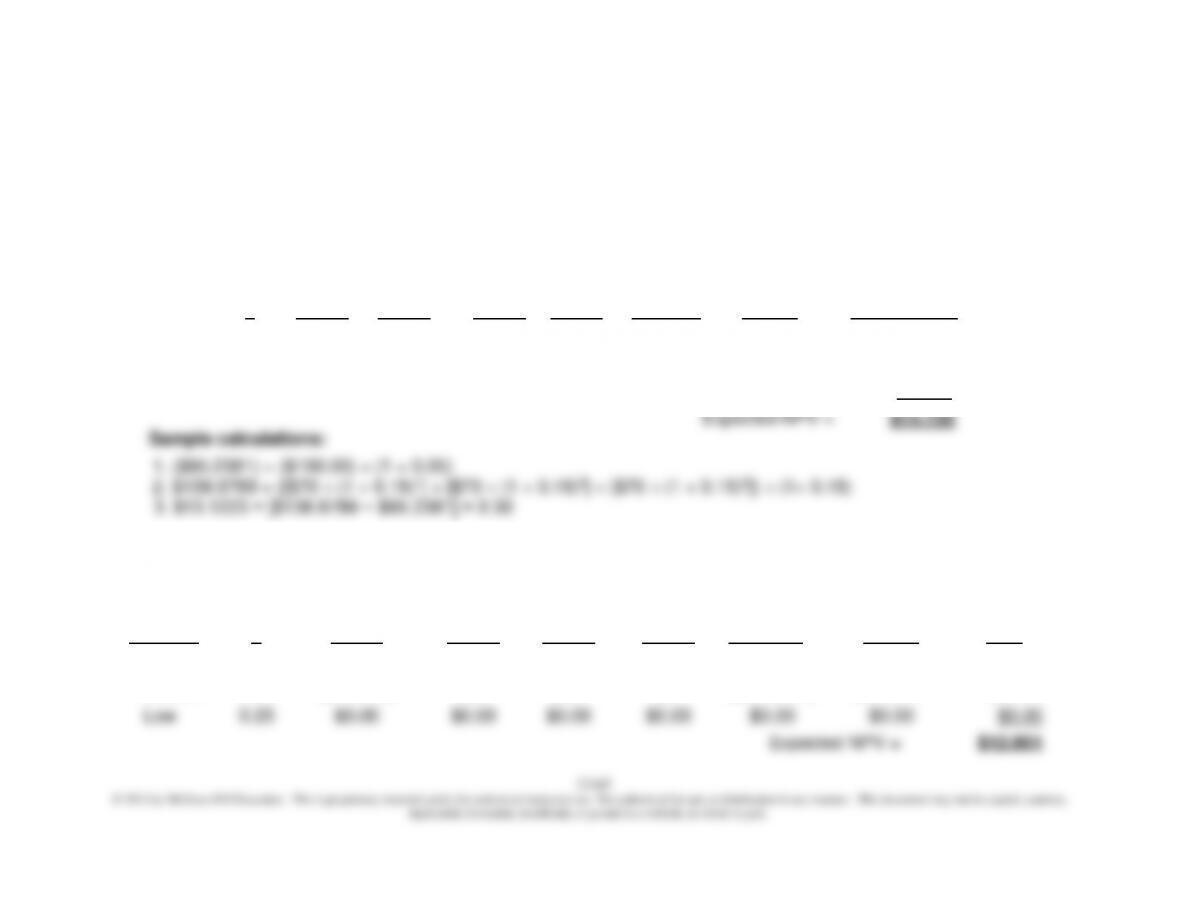

Sample calculations:

1. ($95.2381) = ($100.00) ÷ (1 + 0.05)

2. $138.9789 = [($70 ÷ (1 + 0.15)1) + ($70 ÷ (1 + 0.15)2) + ($70 ÷ (1 + 0.15)3)] ÷ (1 + 0.15)

Chapter 12 – Strategy and the Analysis of Capital Investments

3. $8.75 = [$138.9789 − $95.2381] × 0.2012–51 (Continued-1)

2. Demand Probabilities: 30%, 40%, 30%

WACC =0.15

Risk-free rate = 0.05

Scenario

p

Year 1

Year 2

Year 3

Year 4

@ t = 0

PV of

Outflows

@ t = 0

PV of

Inflows

Estimated

NPV (@ t =0)

High

0.30

($100.00)

$70

$70

$70

($95.2381)

$138.9789

$13.122

Medium

0.40

($100.00)

$50

$50

$50

($95.2381)

$99.2707

$1.613

Low

0.30

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.000

Expected NPV =

$14.735

Sample calculations:

1. ($95.2381) = ($100.00) ÷ (1 + 0.05)

2. $138.9789 = ([$70 ÷ (1 + 0.15)1] + [$70 ÷ (1 + 0.15)2] + [$70 ÷ (1 + 0.15)3]) ÷ (1+ 0.15)

3. $13.1223 = [$138.9789 − $95.2381] × 0.30

3. Sensitivity Analysis: Assumptions Regarding Discount Rates

@ t = 0

@ t = 0

Weighted

Cash Flows

PV of

PV of

NPV @

Scenario

p

Year 1

Year 2

Year 3

Year 4

Outflows

Inflows

t =0)

High

0.25

($100.00)

$70

$70

$70

($95.2381)

$138.9789

$10.935

Medium

0.50

($100.00)

$50

$50

$50

($95.2381)

$99.2707

$2.016

Low

0.25

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

$0.00

Expected NPV =

$12.951

Chapter 12 – Strategy and the Analysis of Capital Investments

12–64

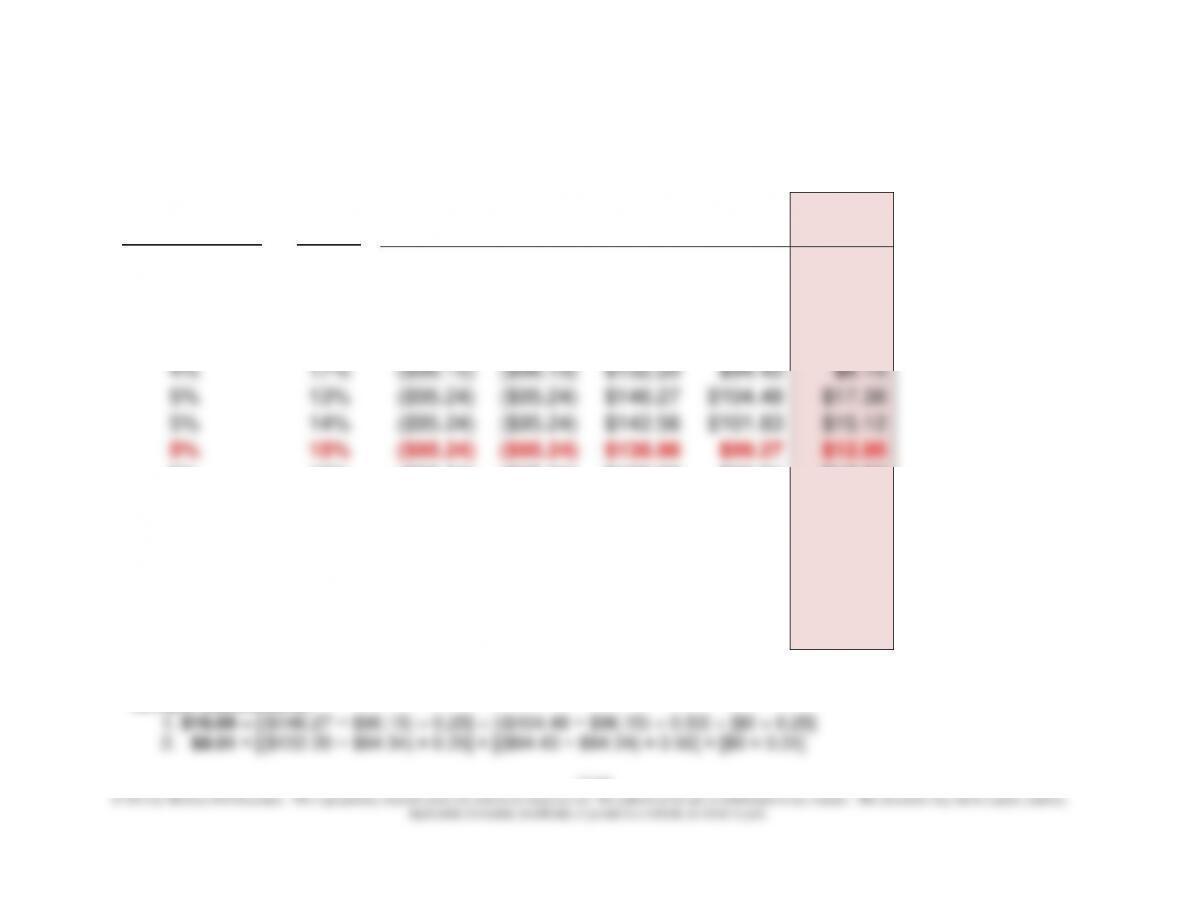

12-51 (Continued–2)

PV of Outflows

PV of Inflows

Expected

Risk-Free Rate

WACC

High

Medium

High

Medium

NPV

4%

13%

($96.15)

($96.15)

$146.27

$104.48

$16.69

4%

14%

($96.15)

($96.15)

$142.56

$101.83

$14.44

4%

15%

($96.15)

($96.15)

$138.98

$99.27

$12.26

4%

16%

($96.15)

($96.15)

$135.53

$96.81

$10.17

4%

17%

($96.15)

($96.15)

$132.20

$94.43

$8.15

5%

13%

($95.24)

($95.24)

$146.27

$104.48

$17.38

5%

14%

($95.24)

($95.24)

$142.56

$101.83

$15.12

5%

15%

($95.24)

($95.24)

$138.98

$99.27

$12.95

5%

16%

($95.24)

($95.24)

$135.53

$96.81

$10.86

5%

17%

($95.24)

($95.24)

$132.20

$94.43

$8.83

6%

13%

($94.34)

($94.34)

$146.27

$104.48

$18.05

6%

14%

($94.34)

($94.34)

$142.56

$101.83

$15.80

6%

15%

($94.34)

($94.34)

$138.98

$99.27

$13.63

6%

16%

($94.34)

($94.34)

$135.53

$96.81

$11.53

6%

17%

($94.34)

($94.34)

$132.20

$94.43

$9.51

Sample Calculations:

12–65

12–51 (Continued-3)

Sensitivity Analysis Summary: Estimated NPVs at Time t = 0

Risk-Free Rate

WACC

4%

5%

6%

13%

$16.69

$17.38

$18.05

14%

$14.44

$15.12

$15.80

15%

$12.26

$12.95

$13.63

16%

$10.17

$10.86

$11.53

17%

$8.15

$8.83

$9.51

On the basis of the above summary results, we can conclude that the

decision to delay the project one year (to gain better information regarding

the level of consumer demand) is relatively insensitive to assumptions

12–52 Real Options (60 Minutes)

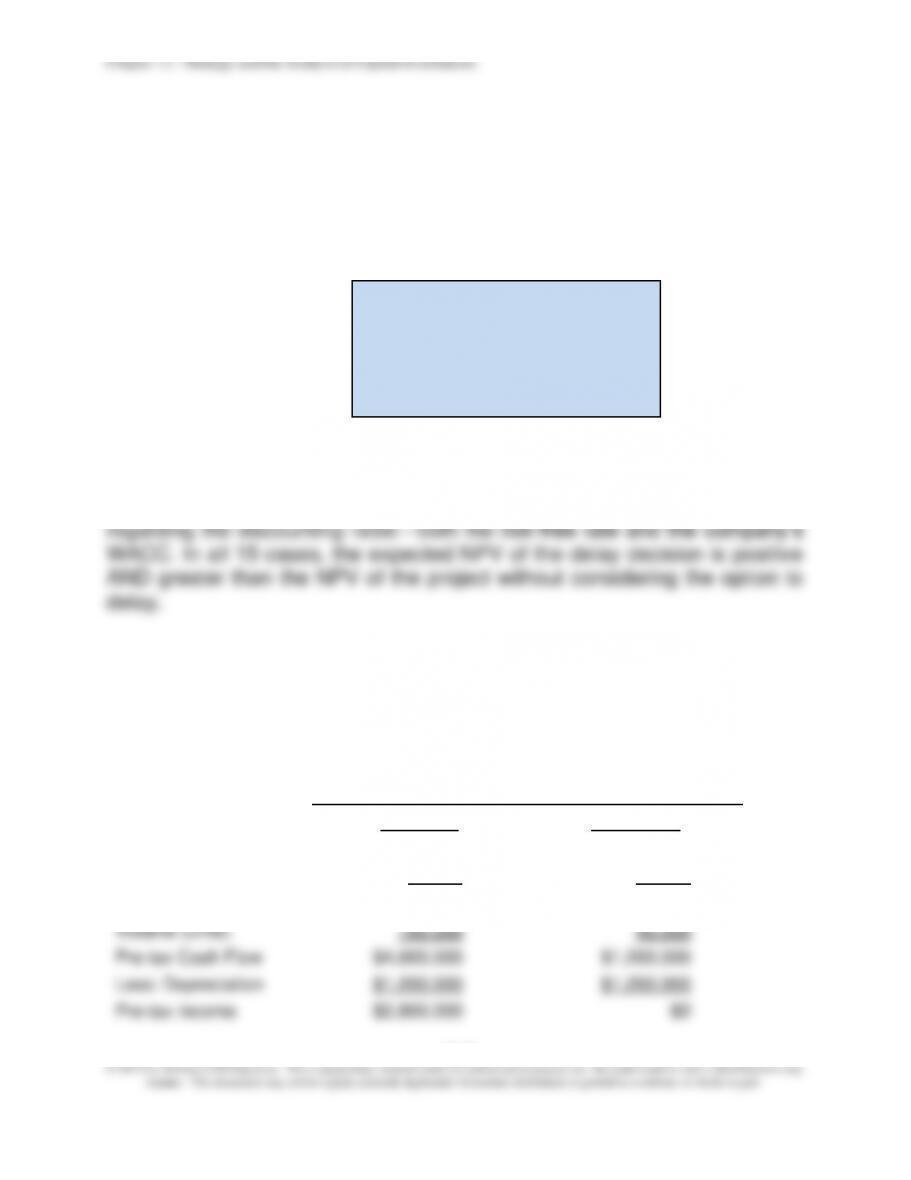

1. Annual after-tax cash flows, both scenarios (possible outcomes):

Product Demand

Optimistic

Pessimistic

Selling price/unit

$80.00

$70.00

Variable cost/unit

$40.00

$40.00

CM/unit

$40.00

$30.00

Volume (units)

100,000

40,000

Pre-tax Cash Flow

$4,000,000

$1,200,000

Less: Depreciation

$1,200,000

$1,200,000

Pre-tax Income

$2,800,000

$0

Chapter 12 – Strategy and the Analysis of Capital Investments

12–66

Taxes

$933,333

$0

After-tax Income

$1,866,667

$0

Plus: Depreciation

$1,200,000

$1,200,000

Net Cash Inflow

$3,066,667

$1,200,000

2. Expected NPV of Proposed Investment:

PV of Cash Inflows

$17,327,3511

$6,780,2682

Initial Investment Outlay

$12,000,000

$12,000,000

NPV

$5,327,351

($5,219,732)

Calculations:

1$3,066,667 × Annuity Factor (10 years, 12%) (NOTE: Above answer was

obtained using built-in Excel function, “NPV,” and therefore will be slightly

different if you use the annuity factor from Appendix C, Table 2.)

2$1,600,000 × Annuity Factor (10 years, 12%)

Expected NPV = (0.50 × $5,327,351) + (0.50 × ($5,219,732))

=

$53,809

Strictly speaking, the project would be accepted because its expected NPV is

positive. However, the expected NPV is close to zero; in fact, it’s basically a

“toss up” as to whether or not this project is profitable in a present-value

sense.

12–52 (Continued)

3. Sensitivity Analysis Results:

WACC

Expected NPV

10%

$1,108,410

11%

$563,695

12%

$53,809

13%

($424,014)

14%

($872,287)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–67

Sample Calculation:

$1,108,410 = ([PV of Optimistic Cash Inflows × Annuity Factor, 10 years, 10% × 0.50] +

[PV of Pessimistic Cash Inflows × Annuity Factor, 10 years, 10%]) − $12,000,000

Note: the figures reported above were generated in Excel, using the built-in NPV

function. Because the annuity factors in Table 2 are rounded (to three decimal places),

your answers will be slightly different from the above if you use the annuity factors

rather than the built-in Excel function.

As can be seen from the above results, the Expected NPV (given the indicated

probabilities for each outcome/state-of-nature) is sensitive to the assumption regarding

the discount rate.

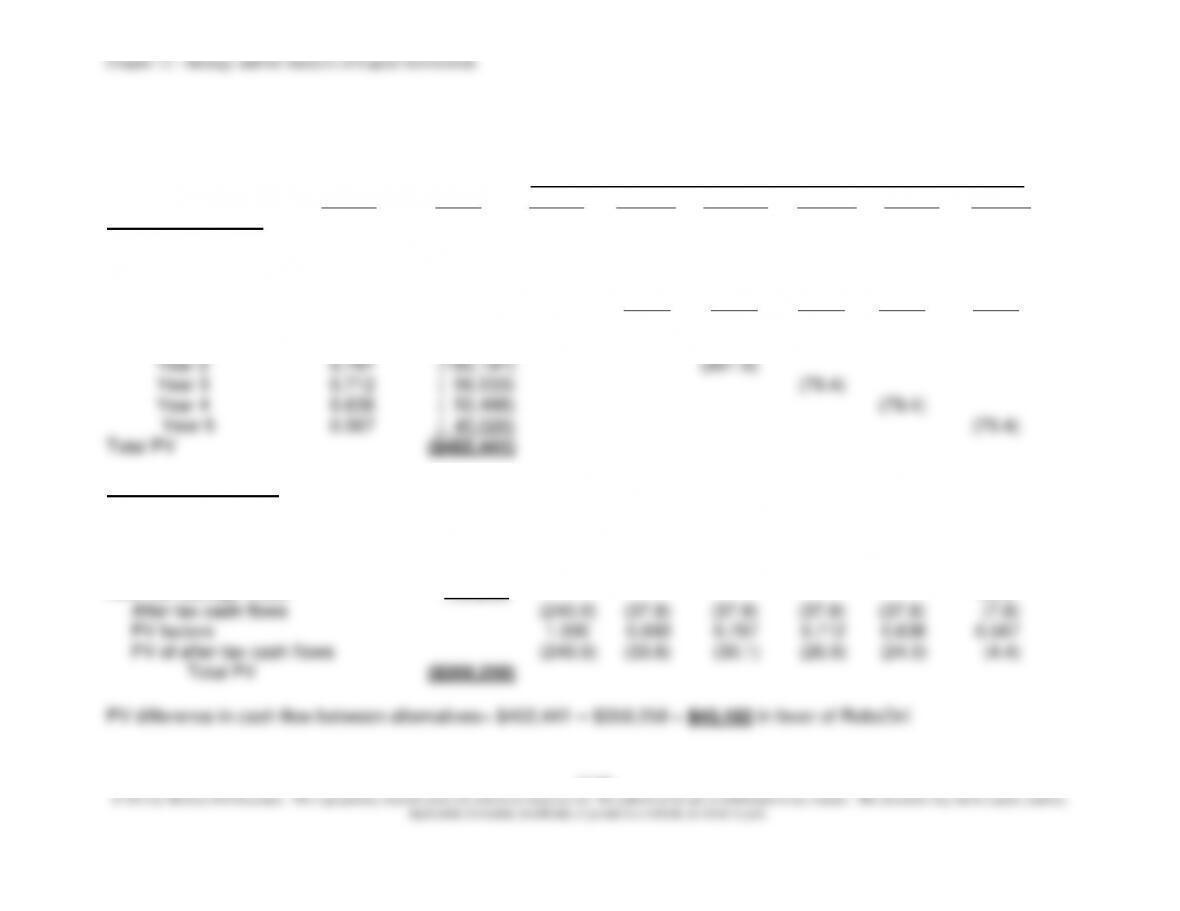

4. Inclusion of abandonment option:

Abandonment value, end of year 1

$10,400,000

Cash flow, end of year 1:

After-tax operating cash flow

$1,200,000

Gross proceeds, equipment

$10,400,000

Less: NBV, end of year 1

$10,800,000

Gain (Loss) on Sale

($400,000)

Tax Effect of Sale

($133,333)

$10,533,333

Total cash flow, end of year 1

$11,733,333

PV (t = 0) of Total Cash Flow, Year 1 =

$10,476,190

12–52 (Continued-2)

NPV of project, with abandonment option:

PV of Total Cash Flow, Year 1

$10,476,190

Less: Investment Outlay, t = 0

$12,000,000

NPV, abandonment scenario =

($1,523,810)

Expected NPV of investment, with abandonment option:

Scenario

Prob.

NPV

Weighted NPV

Optimistic

0.50

$5,327,351

$2,663,676

Chapter 12 – Strategy and the Analysis of Capital Investments

12–68

Pessimistic

0.50

($1,523,810)

($761,905)

Expected NPV =

$1,901,771

Note that the abandonment option adds considerable value to the proposed

investment: if demand turns out to be “pessimistic,” then the company can minimize

its losses by abandoning the project at the end of year 1. As you can see, the NPV in

the abandonment scenario is negative $1,523,810. Compare this amount to the

12–69

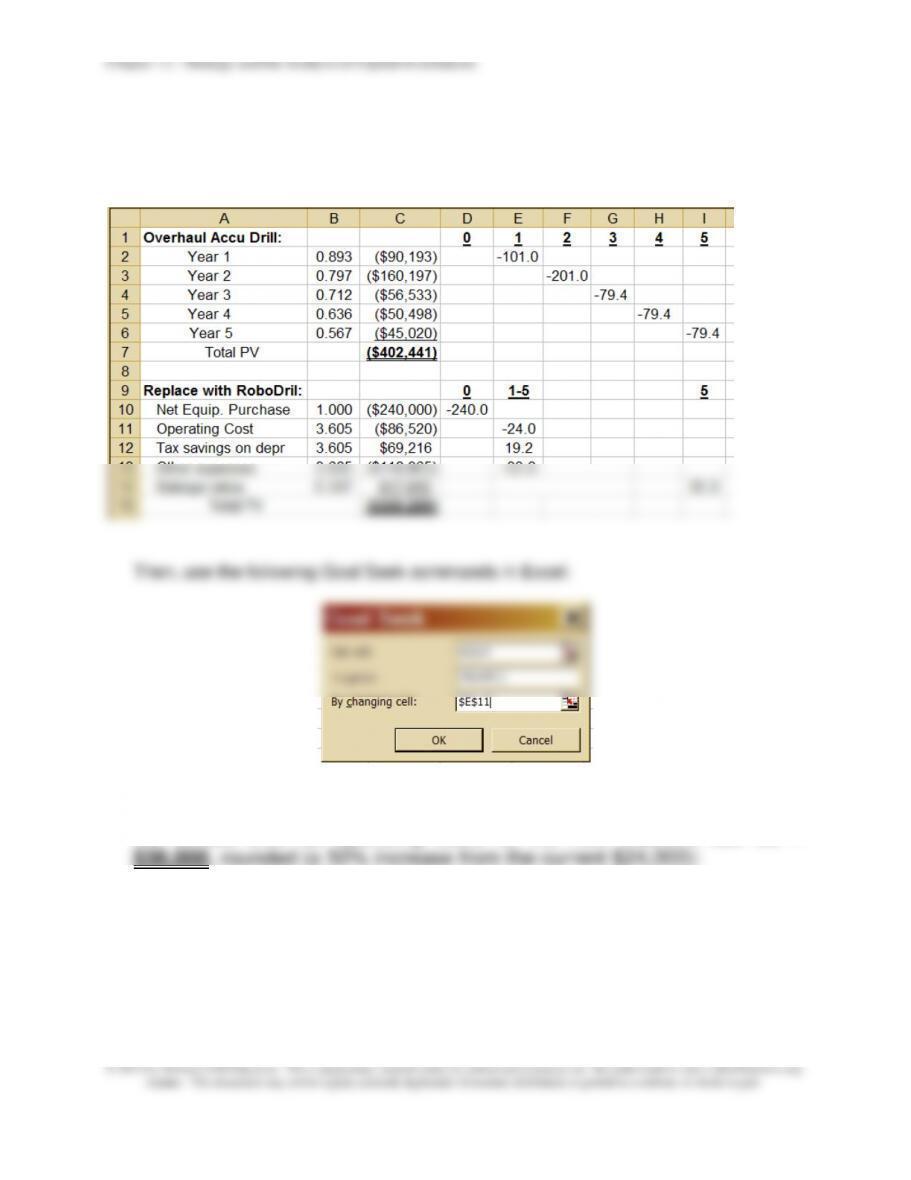

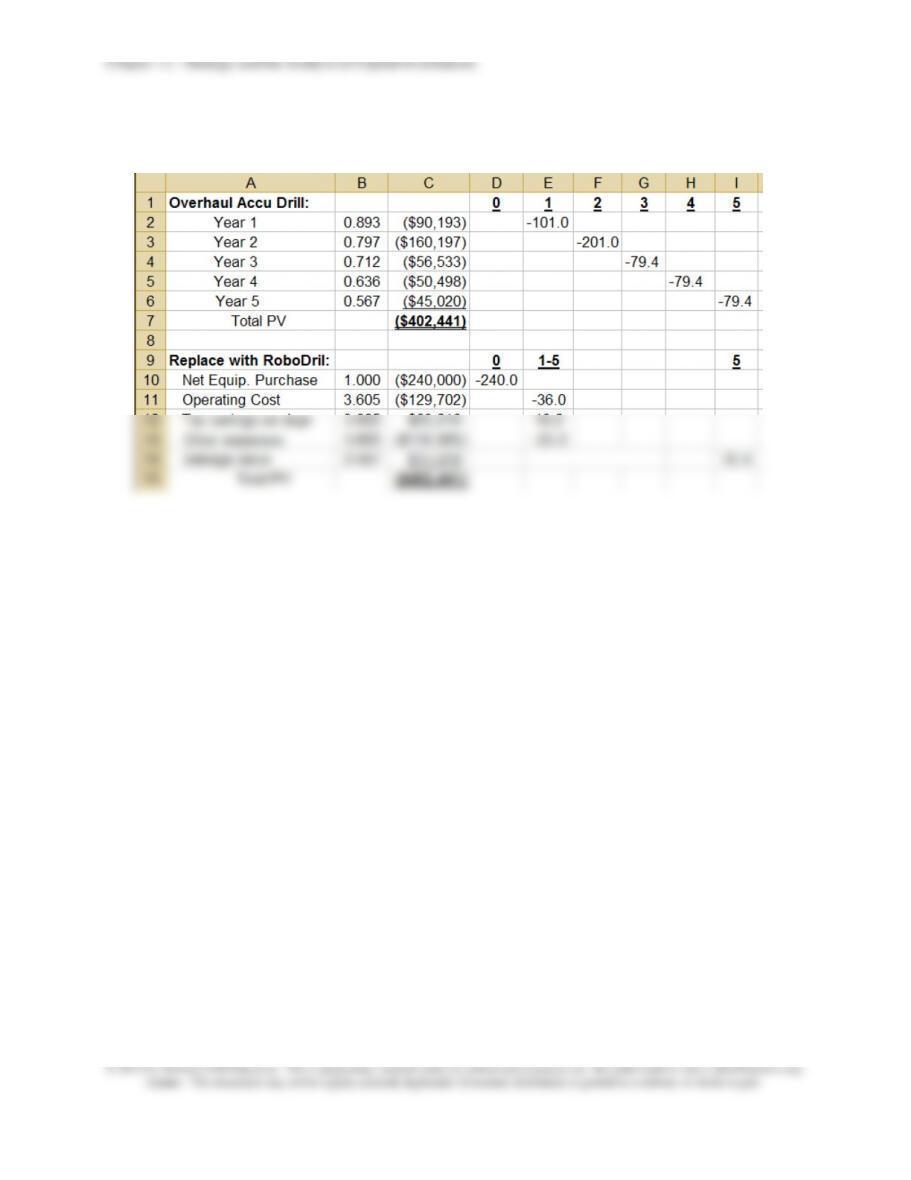

12–53 Equipment-Replacement Decision; Strategy (60 min)

1. & 3.

PV Present After-tax Cash Flows (000s)

Factor Value 0 1 2 3 4 5

Overhaul AccuDril

Operating Cost1 (48.0) (48.0) (38.4) (38.4) (38.4)

Overhaul cost (capitalized) (100.0)

Tax savings on deprec.2 4.0 4.0 16.0 16.0 16.0

Other cash expenses, after tax3 (57.0) (57.0) (57.0) (57.0) (57.0)

After-tax cash flows:

Year 1 0.893 ($90,193) (101.0)

Buy RoboDril 1010K

Net Equip. Purchase4 ($240,000) (240.0)

After-tax cash operating costs5 (86,520) (24.0) (24.0) (24.0) (24.0) (24.0)

Tax savings on depr.6 69,216 19.2 19.2 19.2 19.2 19.2

Other cash expenses, after tax7 (118,965) (33.0) (33.0) (33.0) (33.0) (33.0)

After-tax salvage value8 17,010 30.0

12–70

12–53(Continued–1)

NOTES

1Years 1 and 2: $10 per hour × 8,000 hours × (1 − t) = $48,000

Years 3, 4, and 5: $48,000 × (1 − 20%) = $38,400

2Years 1 and 2:

Depreciation expense per year (SL basis):

($120,000 − $20,000) 10 = $10,000

Income Tax Rate (t) × 0.40

Tax savings on depreciation, Years 1 and 2 $ 4,000

Years 3, 4, and 5:

Book value before overhaul (end of original useful life) $ 20,000

Overhaul cost, Year 3 100,000

Total amount to be depreciated $120,000

Number of years 3

6 Depreciation expense per year: $240,000 5 Years = $48,000

Income Tax Rate (t) × 0.40

Annual Tax savings on depreciation deduction $19,200

7 $55,000 × (1 – t) = $55,000 × 0.60 = $33,000

8 ($50,000 – $0) × (1 – t) = $50,000 × 0.60 = $30,000

Chapter 12 – Strategy and the Analysis of Capital Investments

12–71

12–53(Continued-2)

2. Net After-tax Cash Flows Difference in Cumulative

Year AccuDril RoboDril Cash Flows Difference

0 $0 ($240,000) ($240,000) ($240,000)

1 ($101,000) ($37,800) $63,200 ($176,800)

2 ($201,000) ($37,800) $163,200 ($13,600)

4. Among other factors that the firm should consider before the final decision are:

▪ Changes in technology for equipment

▪ Changes in market, especially demand for the product and competitors

▪ Reliability of the new machine and the expected effects of overhaul

12–72

12-54 Sensitivity Analysis; Spreadsheets (75 minutes)

1. Difference in PV between the two alternatives = $402,441 – $359,259 =

$43,182. We focus on the reduction in variable operating cost needed

each year (3 through 5) after the old machine is overhauled.

The equivalent annuity factor needed to convert this stream of after-tax

cash flows (cost savings) to a present value is found in either of two

ways:

(1) Annuity factor (@12%) for three years = 2.402; this annuity factor

needs to be brought back two years, to get a present value of the

Thus, the additional annual after-tax operating cost savings needed from

improvement to make the overhaul of AccuDril a financially attractive

choice = $22,561, as follows:

$43,182 ÷ 1.914 = $22,561

On a before-tax basis (given an income tax rate of 40%), the required

47%.

12–73

12–54 (Continued–1)

2. The beginning spreadsheet contains the PV of each alternative:

This produces the following result (cell E11): the maximum amount that

the annual after-tax operating costs for the new machine can be =

12–74

12–54 (Continued–2)

Chapter 12 – Strategy and the Analysis of Capital Investments

12–54 (Continued-3)

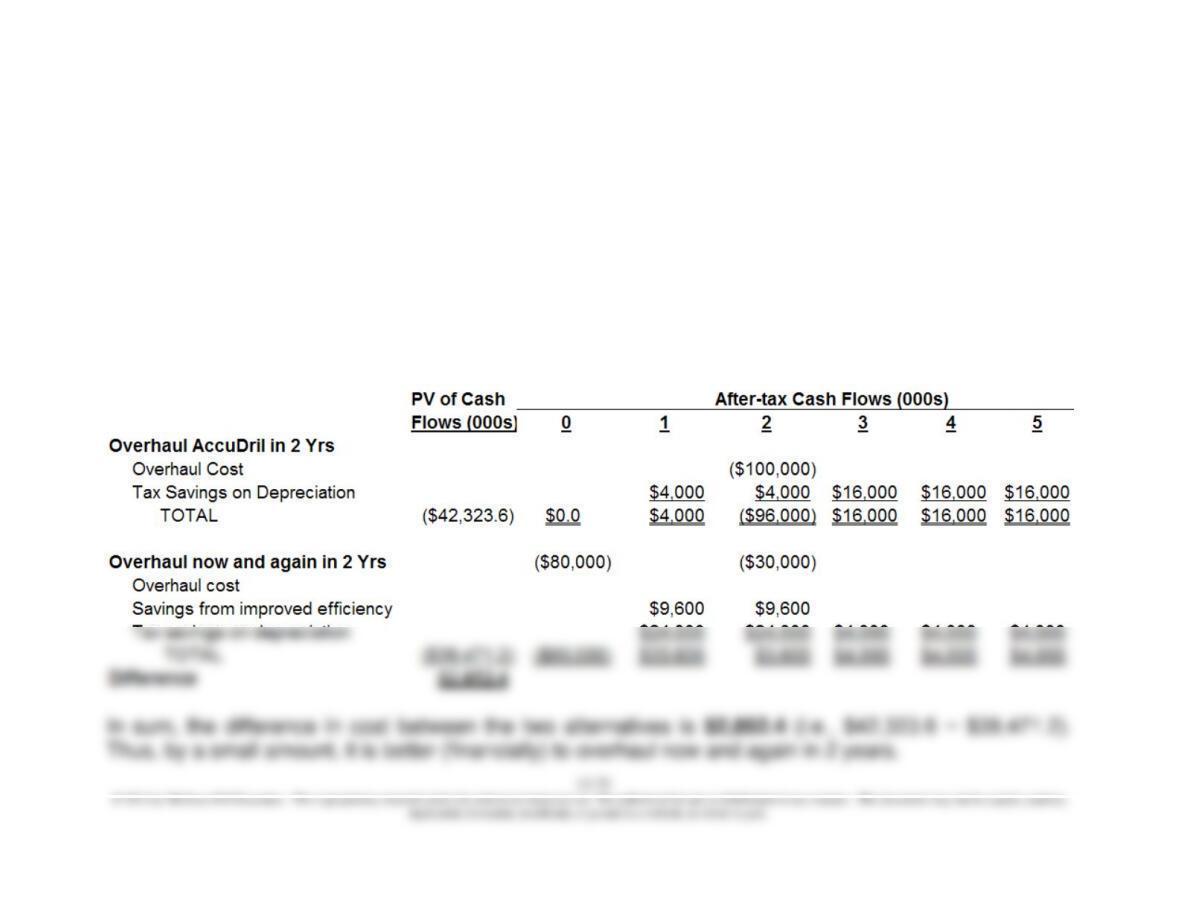

3. Alternative facts:

Revised overhaul cost =

$80,000

Life after first overhaul (in years) =

2

Revised overhaul cost, 2 years hence

$30,000

Life after second overhaul (in years) =

3

Note: the PV cash-flow amounts listed below (viz., ($42,323.6) and ($39,471.2)) were generated using

the NPV built-in function in Excel