Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–16

13-35 Pricing (25 min)

The price, contribution, and profit information is as follows.

1. $214.190 = ($7,385,875 × 1.45) ÷ 50,000

2. $222.926 = ($8,917,020 × 1.25) ÷ 50,000

Total Investment in Product Line

22,350,000

Expected Sales (units)

50,000

Total Variable Costs

$ 5,535,650

=

$4,680,000

+

855,650

Total Fixed Costs

3,381,370

=

2,345,875

+

675,495

+

360,000

Total Manufacturing Cost

7,385,875

=

$4,680,000

+

2,345,875

+

360,000

Total Selling and Administrative

1,531,145

=

855,650

+

675,495

Total Life Cycle Cost

8,917,020

Per unit Manufacturing Cost

147.72

=

7,385,875

÷

50,000

Per unit Life Cycle Cost

178.34

=

8,917,020

÷

50,000

Desired

Rate

Contribution

Gross

Operating

Method:

for Markup

Price

Margin*

Margin*

Profit

Markup on full manufacturing cost

45%

$ 214.190

$5,173,900

$3,323,675

1,792,530

Markup on life cycle costs

25%

222.926

$5,610,650

$3,760,425

2,229,280

Price to Achieve Desired GM %

40.00%

246.196

$6,774,150

$4,923,925

3,392,780

Price to Achieve Desired LCC %

25.00%

237.787

$6,353,750

$4,503,525

2,972,380

Price to Achieve Desired ROA of

15%

37.60%

245.390

$6,733,850

$4,883,625

3,352,480

* Contribution margin and gross margin computed after price is rounded to 3 decimal places

6. The contribution margin, gross margin, and operating profit are shown in

0the right-hand portion of the table above.

The pricing methods yield prices from $214.19 to $246.20. The next

about maintaining or improving market share during turns in the business

cycle for its customers. This latter concern is especially important given

that the demand for the firm’s product is a derived demand, and there is

little that Williams can do to influence total auto sales.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–17

13–36 Pricing Military Contracts (10 min)

This is a complex issue which Pentagon officers and congressional leaders

continue to squabble over. In this particular case, Senator McCain argued

that the contract should be re-written to reduce the fixed fee from 10% to

As for whether the performance fee is too low or too high is a matter of

perspective. While Congress might think the old 5% incentive was too low,

contractors might think the new 12% incentive fee is too big a proportion of

the overall potential fee.

Source: “The Right Stuff for the GIs of the Future,” BusinessWeek, August

15, 2005, pp. 74-75.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–18

13-37 Life-Cycle Pricing (20 min)

Total Fixed Costs $ 2,300

3,000

5,400

6,920

6,000

21,000

$ 44,620

Total variable costs $2.50 + .50 + .50 = $3.50

Life-Cycle Costs =

$ 21,000 for fleet of canoes

Price per Rental for 20% profit margin = $864,000 ÷ 64,000 rentals in

ten years = $13.50

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–19

PROBLEMS

13-38 Target Costing in a Service Firm (20 min)

1.

ICU 100

ICU 900

Unit Cost

Quantity

Cost

Quantity

Cost

Video camera

$ 150

1

$150

3

$450

Video monitor

75

1

75

1

75

Motion detector

15

5

75

8

120

Floodlight

8

3

24

7

56

Alarm

15

1

15

2

30

Wiring

.10/ft

700

70

1,100

110

Installation

20/hr

16

320

26

520

Total

$729

$1,361

Price

$810

$1,520

Profit

$81

$159

ICU 100: $81÷$ 810 = 10% profit margin

ICU 900: $159÷$1,520 = 10.46% profit margin

2.

Price $750 $1,390

Profit $21 $29

ICU 100: $21÷ $750 = 2.80% profit margin

ICU 900: $29÷$1,390 = 2.09% profit margin

3. The installation costs are the largest component of cost and this

category could have room for improvement. By redesigning the

layout of the systems or finding components that integrate more

readily, the installation times could then be reduced. Also, costs

systems.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–20

13-39 Target Costing; Review of Chapter 11 (20 min)

1. The target cost, at the price of $1,500 and the desired margin of 20%

would be

TC = $1,500 – (.2 x $1,500) = $1,200

2.

Currently

With Cost

Reductions

Savings

Manufacturing

Cost

$1,000

$835

($85-$25)+$105=

$165

Marketing Cost

200

200

GSA Cost

225

175

$50

Total Cost

$1,425

$1,210

$215

The cost savings of $215 are not sufficient to get the product total cost

($1,210) down to the desired target cost of $1,200. Given that National

might be willing to pay a higher price, and since the cost difference is

relatively small, it seems that Morrow should in fact pursue the order. Here

are some other considerations:

a. Morrow should consider the short versus the long term issues of taking

on the order. In the short term, as noted in chapter 3, the fixed costs of

manufacturing the order will not change and therefore can be considered

irrelevant for the order if it is a one-time special order. Thus, for a short

term analysis, Morrow should determine that portion of manufacturing,

marketing, and GSA costs that are fixed and exclude them from the

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–21

13-39 (continued –1)

b. Morrow appears to compete in what Robin Cooper calls the

“confrontation” strategy (When Lean Enterprises Collide, Harvard Business

School Press, 1995) wherein each competitor must simultaneously

compete on the basis of price, quality and functionality. In Morrow’s case,

functionality refers not only to meeting product specifications but also to

and choosing the proper “bundle” of the three aspects of competition:

price, quality and functionality. For example, to be most competitive,

Morrow must spend extra dollars to ensure that there are few if any billing

and shipping errors, while at the same time reducing the costs of

manufacturing the product, and maintaining or improving product quality.

c. The problem notes that the manufacturing costs are “standard” full costs.

Since the costs are given at standard, this means that there are no

Should the standards be revised?

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–22

13-40 Target Costing; Health Care (20 min)

1. The average cost is $256.068 = $262,069,095÷1,023,437

The current profit per enrollee is $368 – $256.068 = $111.932

The target cost is $213.068 = $325 – $111.932 to maintain the same

contribution per enrollee

Enrollment

in 2013

Projected

Enrollment

in 2014

Average

Monthly Cost

in 2013

Avg

Cost in

2013

Age

Cost in

2014

(+6%)

Projected

Cost in 2014

Age %

in 2014

Age %

in 2014

1 to 4

45,688

48,977

$ 11,147,872

244

258.640

$12,667,411

4.5%

4.6%

5 to 14

82,456

84,663

10,059,632

122

129.320

10,948,619

8.1%

8.0%

15 to 19

95,873

95,887

8,436,824

88

93.280

8,944,339

9.4%

9.1%

20 to 24

66,246

67,882

9,539,424

144

152.640

10,361,508

6.5%

6.4%

25 to 34

133,496

132,554

26,432,208

198

209.880

27,820,434

13.0%

12.5%

35 to 44

166,876

175,446

38,882,108

233

246.980

43,331,653

16.3%

16.6%

45 to 54

85,496

90,889

22,741,936

266

281.960

25,627,062

8.4%

8.6%

55 to 64

99,624

101,923

28,691,712

288

305.280

31,115,053

9.7%

9.6%

65 to 74

156,288

161,559

48,918,144

313

331.780

53,602,045

15.3%

15.3%

75 to 84

67,895

72,465

33,132,760

488

517.280

37,484,695

6.6%

6.8%

85 years and

older

23,499

26,849

24,086,475

1025

1086.500

29,171,439

2.3%

2.5%

TOTAL

1,023,437

1,059,094

$262,069,095

$291,074,259

100.0%

100.0%

1,023,437

1,059,094

Average Cost

$ 256.068

$ 274.833

Current Price

$368

Current Profit Per Enrollee

(Desired Profit)

$111.932

=368-256.068

$ 111.932

New Market Price

$325

$ 340.000

Target Cost

$213.068

=325-111.932

$ 228.07

Required Cost Reduction Per

Enrollee

$ 46.765

=$274.833 – $228.068

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–23

2. The target cost for 2014 is $228.068 = $340 – $111.932; this calculation

uses the new price and the same profit per enrollee as in 2013. The

required reduction in cost per enrollee is $46.765 as shown in the above

table. Note that the cost per enrollee is determined by taking the average

cost per enrollee for each age group (Col E) in order to determine total

and H), and in particular, the two oldest age groups, the most expensive

groups, have increased slightly in number and percentage. Since the

coverage rate of $340 is applicable to all age groups, it is important for VIP-

13-40 (continued)

MD to study the actual pattern of increase in cost, across all age groups as

the number of enrollees in each group change.

3. A critical success factor is the relationship with network providers.

Establishing a good working relationship with its providers improves the

likelihood that the clinicians will follow the HMO’s protocols. Customer

satisfaction is essential, so VIP-MD should measure and monitor the

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–24

13-41 Target Cost; Warehousing (20 min)

Current Year Operating Income

Sales ($20 x 100,000) =

$2,000,000

Costs:

Purchase ($10 x 100,000)

$1,000,000

Purchasing order ($150 x 1,000)

150,000

Warehousing ($30 x 8,000)

240,000

Distributing ($80 x 500)

40,000

Fixed operating cost

250,000

1,680,000

Operating income

$320,000

Determination of Target Cost:

Sales ($20.00 x 100,000 x 0.90)

$1,800,000

Desired profit (above)

320,000

Costs:

Purchase (2% discount)

$980,000

Purchasing order ($150 x 680)

102,000

Distributing ($77 x 500)

38,500

Fixed operating cost

250,000

1,370,500

Maximum allowable costs for warehousing

$109,500

Warehousing costs must be reduced from $240,000 to $109,500, a reduction of

$130,500.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–25

13–42 Target Costing; International (20 min)

1. Target manufacturing cost = Current manufacturing cost + “U.S.

Differential”

= $56 + Price differential – Cost differential

2. The cost differential is $62 – $56 = $6

Harpers cannot add the lighter weight feature, though it is the

most desired, as the cost of $6.75 is greater than the cost differential

3. Strategically, the decision to sell shoes in the United States makes

very good sense. To compete effectively in a competitive global

market such as shoes, a firm has to have an effective presence in all

the key markets, which would include the United States. The

Note: the currency exchange rate used in the problem is based on the

exchange rate of $1.6523/ £but the actual exchange rate varies on a daily

basis.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–26

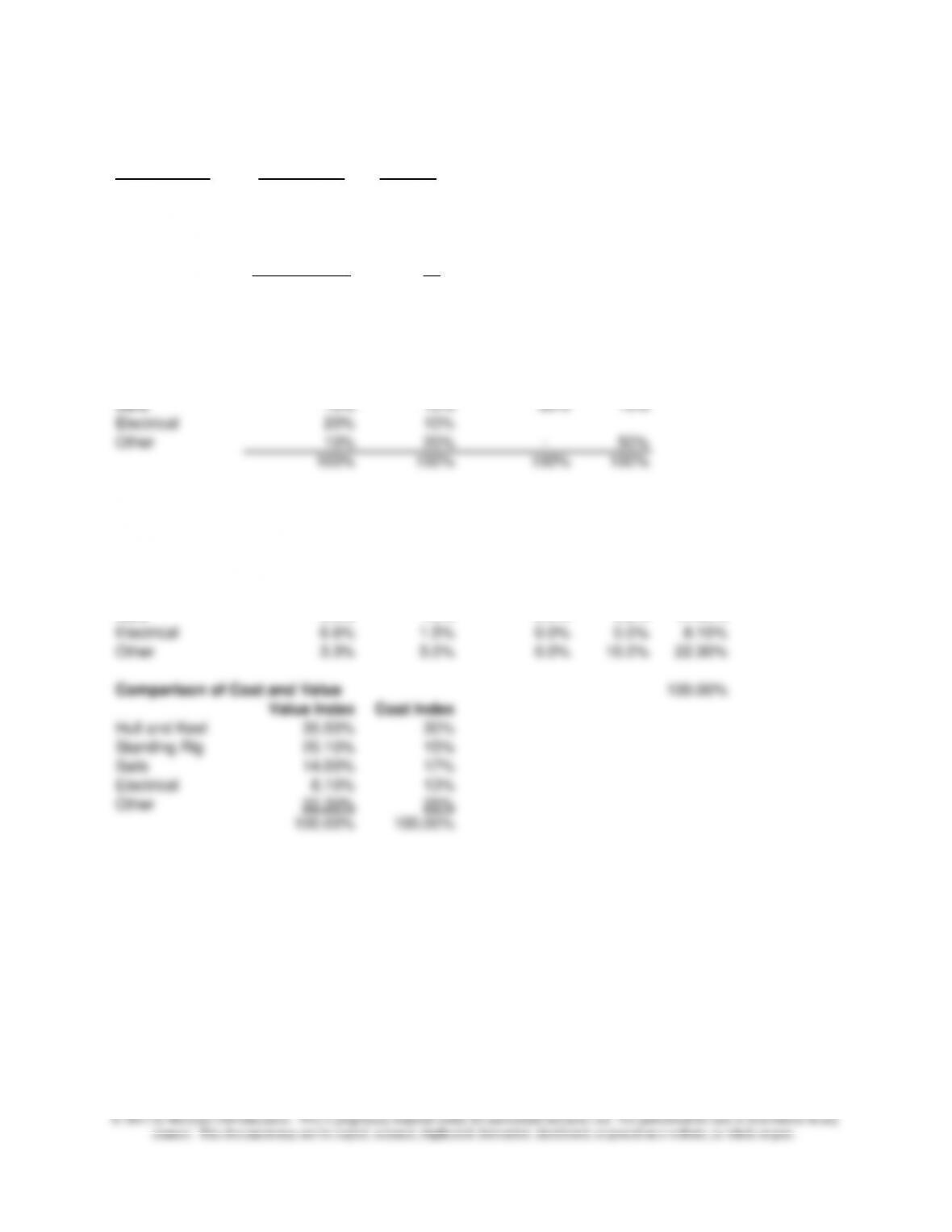

13-43 Target Costing; Quality Function Deployment (QFD) (30 min)

1.

Components Target Cost Percent

Hull and Keel 36,000$ 30%

Standing Rig 18,000 15%

Sails 20,000 17%

Electrical 16,000 13%

Other 30,000 25%

120,000$ 100%

Component/

Criteria Safety Styling Performance Comfort

Hull and Keel 30% 40% 50% 30%

Standing Rig 30% 20% 20% 10%

Sails 10% 10% 30% 10%

Electrical 20% 10%

Other 10% 20% – 50%

100% 100% 100% 100%

Component/ Value

Criteria Safety Styling Performance Comfort Index

Criteria Value 33.0% 15.0% 20.0% 32.0% 100%

Hull and Keel 9.9% 6.0% 10.0% 9.6% 35.50%

Standing Rig 9.9% 3.0% 4.0% 3.2% 20.10%

Sails 3.3% 1.5% 6.0% 3.2% 14.00%

Electrical 6.6% 1.5% 0.0% 0.0% 8.10%

Other 3.3% 3.0% 0.0% 16.0% 22.30%

Standing Rig 20.10% 15%

Sails 14.00% 17%

Electrical 8.10% 13%

Other 22.30% 25%

100.00% 100.00%

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–27

13-43 (continued)

2. When the value index is compared to the target cost, the percentage

investment in hull & keel and standing rig looks too low–

The value index for hull & keel is 35.5% while the cost index is 30%; the

that consideration be given to redesign of the boat to bring it more in line

with customer value.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–28

13-44 Target Costing: Quality Function Deployment

The QFD analysis shows that BPI should consider spending more time and

money on the planning meeting and less on the photography done the day

of the wedding, to put their costs more in line with the customer criteria.

Customer

Criteria

Rating

Percent

Fast Service

30

10.0%

Getting Good Photos

120

40.0%

Quality of Photo Finishing

60

20.0%

Quality of Photo Books

90

30.0%

300

100.0%

Activities

Target Cost

Percent

Planning Meeting

$ 800

16.0%

Take Photos

2,400

48.0%

Prepare Proofs

600

12.0%

Prepare Photo Book

1,200

24.0%

$ 5,000

100.0%

Activity/Criteria

Fast Service

Good Photos

Finishing

Book Quality

Planning Meeting

30%

40%

0%

35%

Take Photos

5%

60%

0%

15%

Prepare Proofs

35%

0%

50%

0%

Prepare Photo Book

30%

0%

50%

50%

100%

100%

100%

100%

Activity/Criteria

Fast Service

Good Photos

Finishing

Book Quality

Importance

Index

Criteria Value

10%

40%

20%

30%

100%

Planning Meeting

3%

16%

0%

11.5%

29.50%

Take Photos

0.5%

24%

0%

4.5%

29.00%

Prepare Proofs

3.5%

0%

10%

0%

13.50%

Prepare Photo Book

3%

0%

10%

15%

28.00%

100.00%

Comparison of Cost and Value

Importance

Index

Cost Index

Ratio

Planning Meeting

29.50%

16.00%

1.84

Spend More

Take Photos

29.00%

48.00%

0.60

Spend Less

Prepare Proofs

13.50%

12.00%

1.13

No clear action

Prepare Photo Book

28.00%

24.00%

1.17

No clear action

100.00%

100.00%

2. A limitation of the above analysis is that there are certain costs of taking

the photos on the day of the wedding (additional lighting, backup

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–29

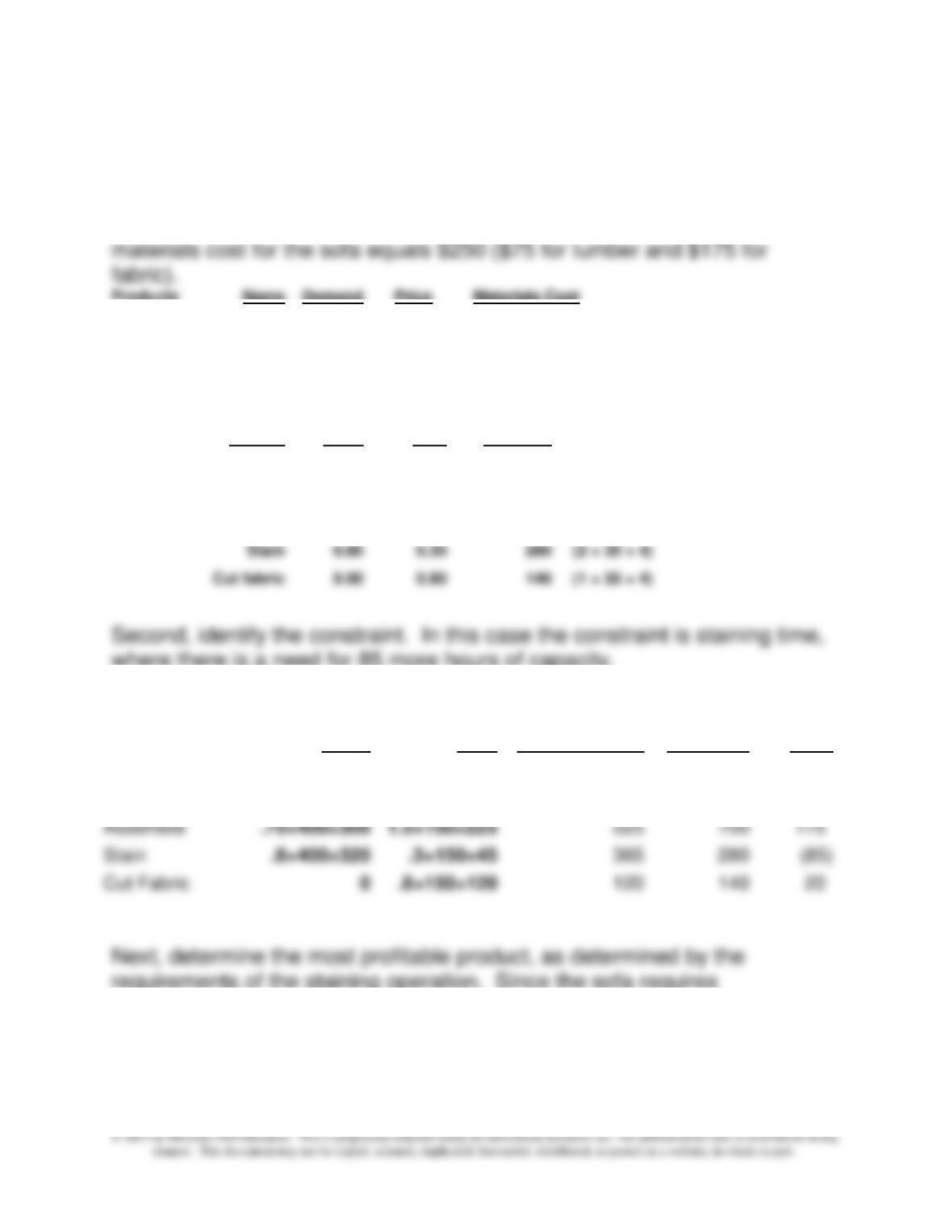

13-45 Theory of Constraints; Strategy (30 min)

First, summarize key information and obtain hours capacity in each

process. The materials cost for the table is $100 of lumber, while the

Products

Name

Demand

Price

Materials Cost

First

Table

400

$250.00

$100.00

Second

Sofa

150

$450.00

$250.00

Time Req’d for

Each Product

Time (hrs.)

Activity

Table

Sofa

Available

Cut lumber

0.50

0.20

280

(2 × 35 × 4)

Sand

0.50

0.50

280

(2 × 35 × 4)

Assemble

0.75

1.50

700

(given)

Stain

0.80

0.30

280

(2 × 35 × 4)

Cut fabric

0.00

0.80

140

(1 × 35 × 4)

where there is a need for 85 more hours of capacity.

Step Two, Part 1: Identify the Constraint

Total Time

Time

Slack

Table

Sofa

Required (hrs)

Available

Time

Cut

.5×400=200

.2×150=30

230

280

50

Sand

.5×400=200

.5×150=75

275

280

5

Assemble

.75×400=300

1.5×150=225

525

700

175

Stain

.8×400=320

.3×150=45

365

280

(85)

Cut Fabric

0

.8×150=120

120

140

20

Next, determine the most profitable product, as determined by the

requirements of the staining operation. Since the sofa requires

substantially less staining time, and because it has higher throughput, it is

the most profitable product.

Chapter 13 – Cost Planning for the Product Life Cycle: Target Costing, Theory of Constraints, and Strategic Pricing

13–30

13–45 (continued)

Part Two: Identify Most Profitable Product

Table

Sofa

Price

$250

$450

Materials Cost

$100

$250

Throughput Margin

$150

$200

Constraint time (staining)

0.80

0.30

Throughput/hour

$187.50

$666.67

Finally, determine the most profitable product mix. Since sofas are the

most profitable through the staining constraint, we fill the sofa demand first,

and then with the remaining staining capacity, fill as much of the table

demand as possible. See below for calculations.

Table

Sofa

Demand

400

150

Production of Sofas

150

Availability, Usage of Staining hours

235

45

280

Production of Tables

293

Throughput/unit (see above)

$150.00

$200.00

Total Throughput

$43,950

$30,000

$73,950

Note: Sofas are most profitable and go first; total time for sofas = 150 × .3 = 45hrs; Total hours available for

Tables = 280-45 = 235 hours; total tables that can be manufactured = 235 ÷ .8 = 293 tables.

2. Part one above solves the first two steps of the TOC, to identify the

constraint and determine the most profitable product mix. The third step, to

maximize flow through the constraint, would require Colton to look for ways