Chapter 6 – Process Costing

6-31

6-47 Weighted-Average Method; FIFO Method (70-80 min)

1. Porter Company — Department A

Production Cost Report

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 500

Materials 100%

Conversion 30%

Units started 1,500

Total to account for 2,000

Units Finished or Trans out 1,600 1,600 1,600

Ending WIP 400

Materials 100% 400

Conversion –

20% 80

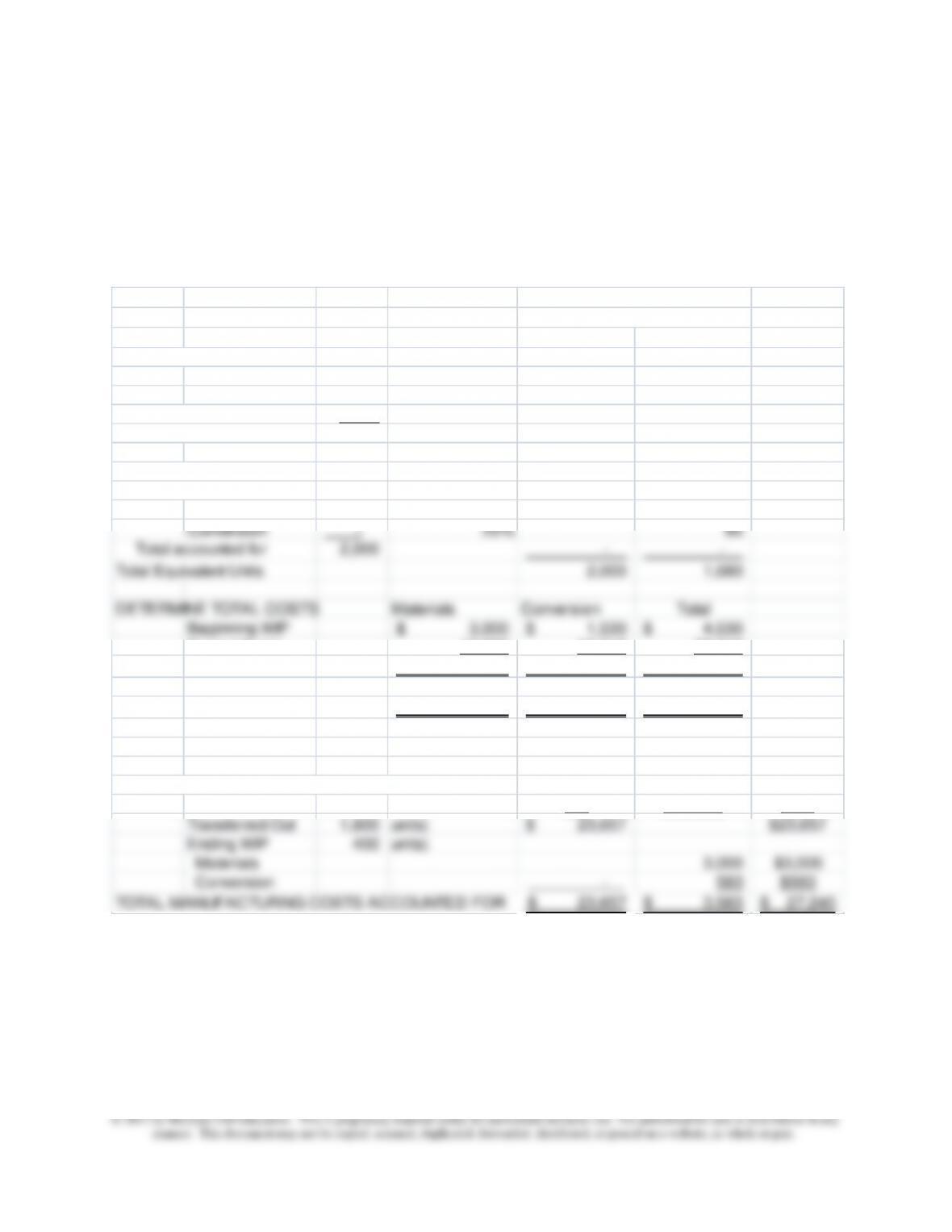

Total accounted for 2,000 – –

Total Equivalent Units 2,000 1,680

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP 3,000$ 1,530$ 4,530$

Current Costs 12,000 10,710 22,710

TOTAL 15,000$ 12,240$ 27,240$

WTAVG Cost per EU 7.500$ 7.286$ 14.786$

Units Completed

Units in Ending

COST ASSIGNED –WEIGHTED AVERAGE and Transferred WIP

Out Inventory Total

Transferred Out 1,600 units) 23,657$ $23,657

Weighted Average

Equivalent Units

Chapter 6 – Process Costing

6-32

6-47 (continued –1)

2. Porter Company — Department B

Production Cost Report

Physical Percent Transferred

Units

Completion

in Costs Materials

Conversion

Beginning WIP 300 100%

Materials 0%

Conversion 40%

Units started or Trans-in 1,600 100%

Total to account for 1,900

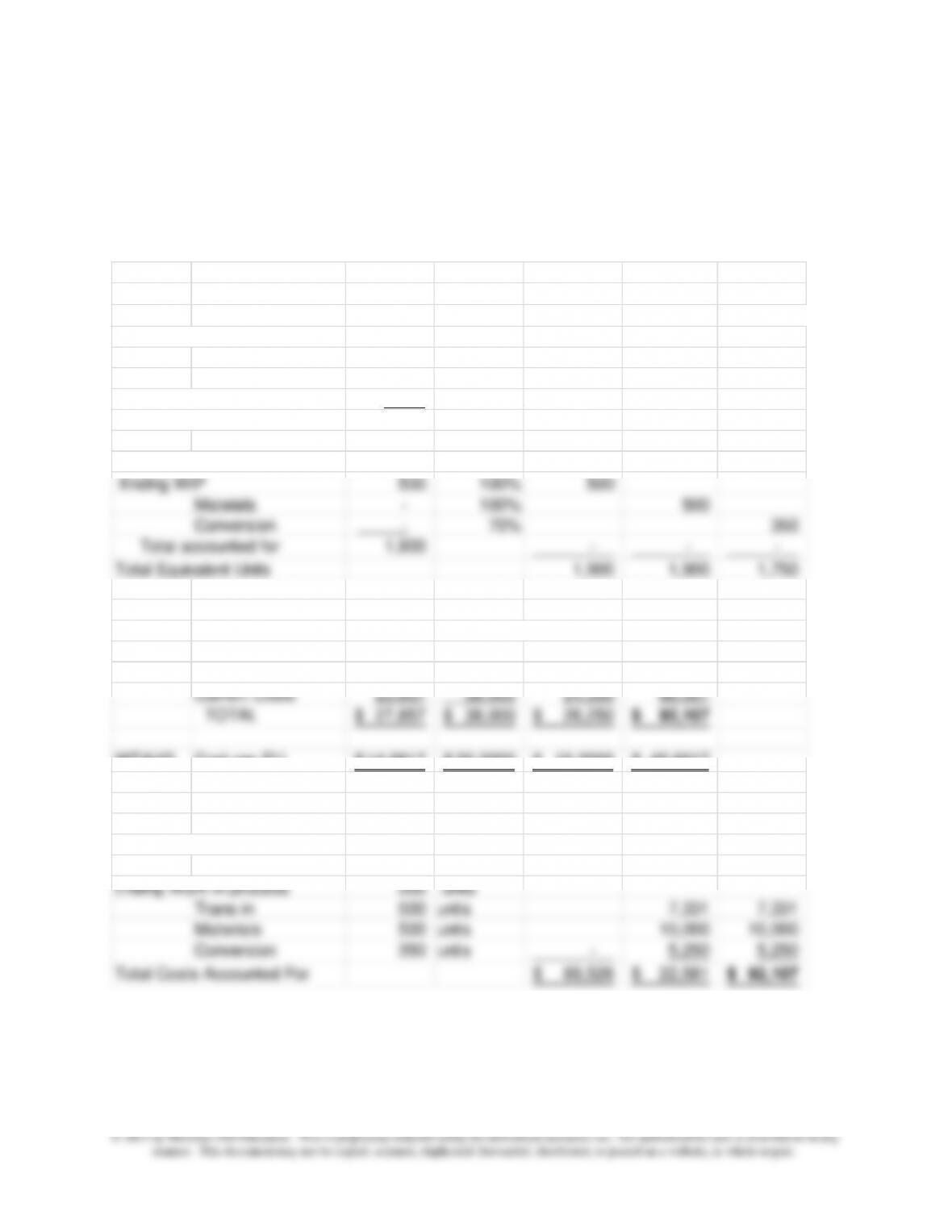

Units Finished or Trans-out 1,400 100% 1,400 1,400 1,400

Ending WIP 500 100% 500

Mateials – 100% 500

Conversion –

70% 350

Total accounted for 1,900 – – –

Total Equivalent Units 1,900 1,900 1,750

COST ADDED

Trans-in Materials Conversion Total

Beginning WIP 4,200$ –$ 1,900$ 6,100$

Current Costs 23,657 38,000 24,350 86,007

TOTAL 27,857$ 38,000$ 26,250$ 92,107$

& Trans-out in Process Total

Finished Goods

1,400 units 69,526$ 69,526$

Ending Work-in-process

500 units

Trans-in 500 units 7,331 7,331

Materials 500 units 10,000 10,000

Total Costs Accounted For 69,526$ 22,581$ 92,107$

——–This Dept-–—–

6-33

6-48 Weighted Average Process Costing; Spoilage (50 min)

1.

Whole Percent

Units

Completion

Materials Conversion

Beginning WIP 2,000 100%

Materials 100%

Conversion 30%

Units started or Trans-in 30,000 100%

Total to account for 32,000

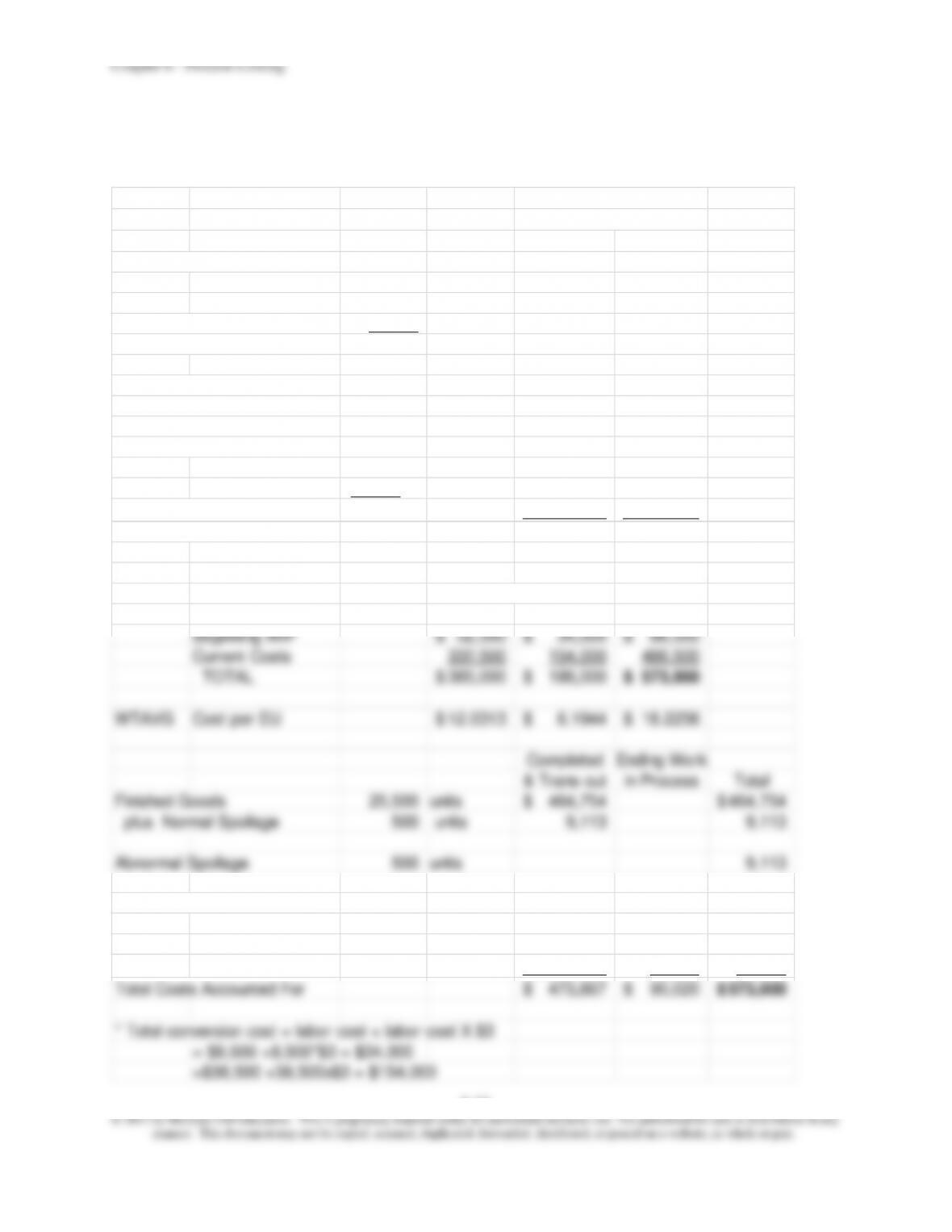

Units Finished or Trans-out 25,500 100% 25,500 25,500

Normal spoilage 500 100% 500 500

Abnormal spoilage 500 100% 500 500

Ending WIP 5,500 100%

Materials – 100% 5,500

Conversion –

70% 3,850

Total accounted for 32,000 – –

Total Equivalent Units 32,000 30,350

COST ADDED

Materials Conversion* Total

Beginning WIP 52,500$ 34,000$ 86,500$

Current Costs 332,500 154,000 486,500

TOTAL 385,000$ 188,000$ 573,000$

WTAVG Cost per EU 12.0313$ 6.1944$ 18.2256$

Completed

Ending Work

& Trans-out in Process Total

* Total conversion cost = labor cost + labor cost X $3

= $8,500 +8,500*$3 = $34,000

=$38,500 +38,500x$3 = $154,000

——–This Dept-——

Weighted Average

Equivalent Units

Chapter 6 – Process Costing

6-34

6-48 (continued –1)

2. The new capacity will allow the company to grow which is a positive

for future revenues and profits, but it also has apparently caused two

significant problems. One is the increase in work in process

inventory, which is costly and can lead to waste, especially since the

product is paint. The quality of paint can erode if not properly sealed

and stored. Another is the significant amount of waste, 1,000

the company’s customers expect the highest quality in paint. The

spoilage issues are a threat to the continued success of that strategy.

Alexander needs to review the implementation of the new process,

and perhaps make some significant changes.

3. The spoiled paint could be an environmentally harmful chemical, and

if so, should be disposed of in an environmentally appropriate way.

This could be costly to the company, and the cost should be captured

Chapter 6 – Process Costing

6-35

6-49 Spoilage; Weighted-Average Method;

Transferred-in Costs (40 Min)

1.

a. Normal amount of defective or spoiled bikes

Bikes passing through assembly 48,000

Less:

Bikes not inspected during current year

Beginning work–in-process inventory

(inspected in prior year – 80% complete) 3,000

Ending work–in–process inventory

b. Abnormal amount of defective/spoiled bikes

Total bikes lost 4,000

Chapter 6 – Process Costing

6-36

6-49 (continued –1)

2.

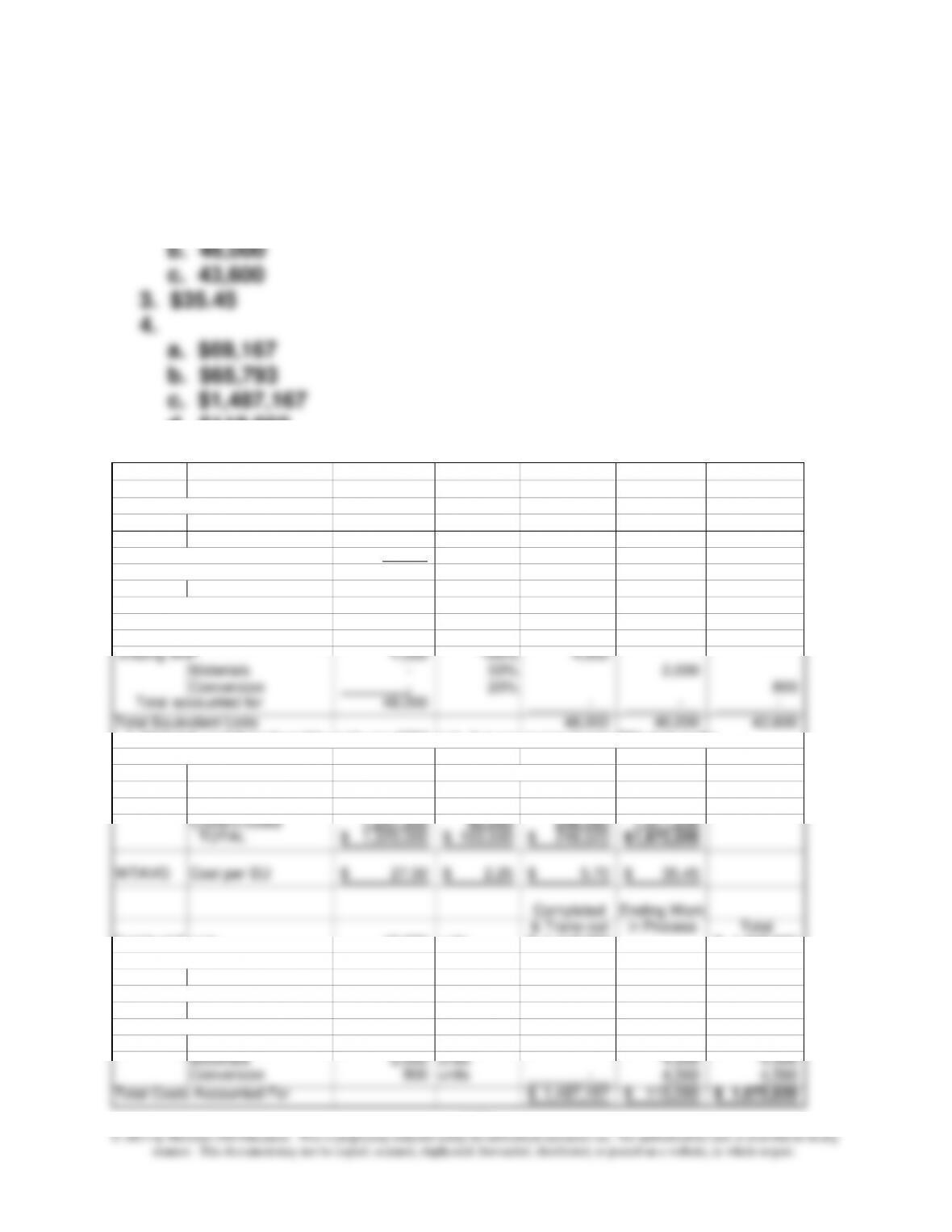

a. 48,000

d. $119,060

Whole Percent Transferred

Units Completion in Costs Materials Conversion

Beginning WIP 3,000 100%

Materials 100%

Conversion 80%

Units started or Trans-in 45,000 100%

Total to account for 48,000

Units Finished or Trans-out 40,000 100% 40,000 40,000 40,000

Normal spoilage 2,050 * 2,050 2,050 1,435

Abnormal spoilage 1,950 * 1,950 1,950 1,365

Ending WIP 4,000 100% 4,000

Materials – 50% 2,000

Conversion – 20% 800

Total accounted for 48,000 – – –

Total Equivalent Units 48,000 46,000 43,600

* Materials and Transferred in costs are 100% lost; but conversion is only 70% lost, to the

inspection point

COST ADDED

Trans-in Materials Conversion Total

Beginning WIP 82,200$ 6,660$ 11,930$ 100,790$

Current Costs 1,237,800 96,840 236,590 1,571,230

TOTAL 1,320,000$ 103,500$ 248,520$ 1,672,020$

WTAVG Cost per EU 27.50$ 2.25$ 5.70$ 35.45$

Completed Ending Work

& Trans-out in Process Total

Finished Goods

40,000 units 1,418,000$ 1,418,000$

plus Normal Spoilage

2,050 units 69,167 69,167

Abnormal Spoilage

1,950 units 65,793

Ending Work-in-process

4,000 units

Trans-in 4,000 units 110,000 110,000

Materials 2,000 units 4,500 4,500

Conversion 800 units – 4,560 4,560

Total Costs Accounted For 1,487,167$ 119,060$ 1,672,020$

—–This Dept—–

Chapter 6 – Process Costing

6-37

6-49 (continued –2)

5. a. The cost of the normal spoiled units of $69,167 would be

transferred to the Packing Department as a portion of the cost of

the 40,000 good units transferred out. Thus, this amount would be

b. The abnormal losses of $65,793 would appear as a period

expense on the company’s income statement.

c. The cost of the good units completed and transferred to the

Packing Department ($1,487,167) would be included in the

Chapter 6 – Process Costing

6-38

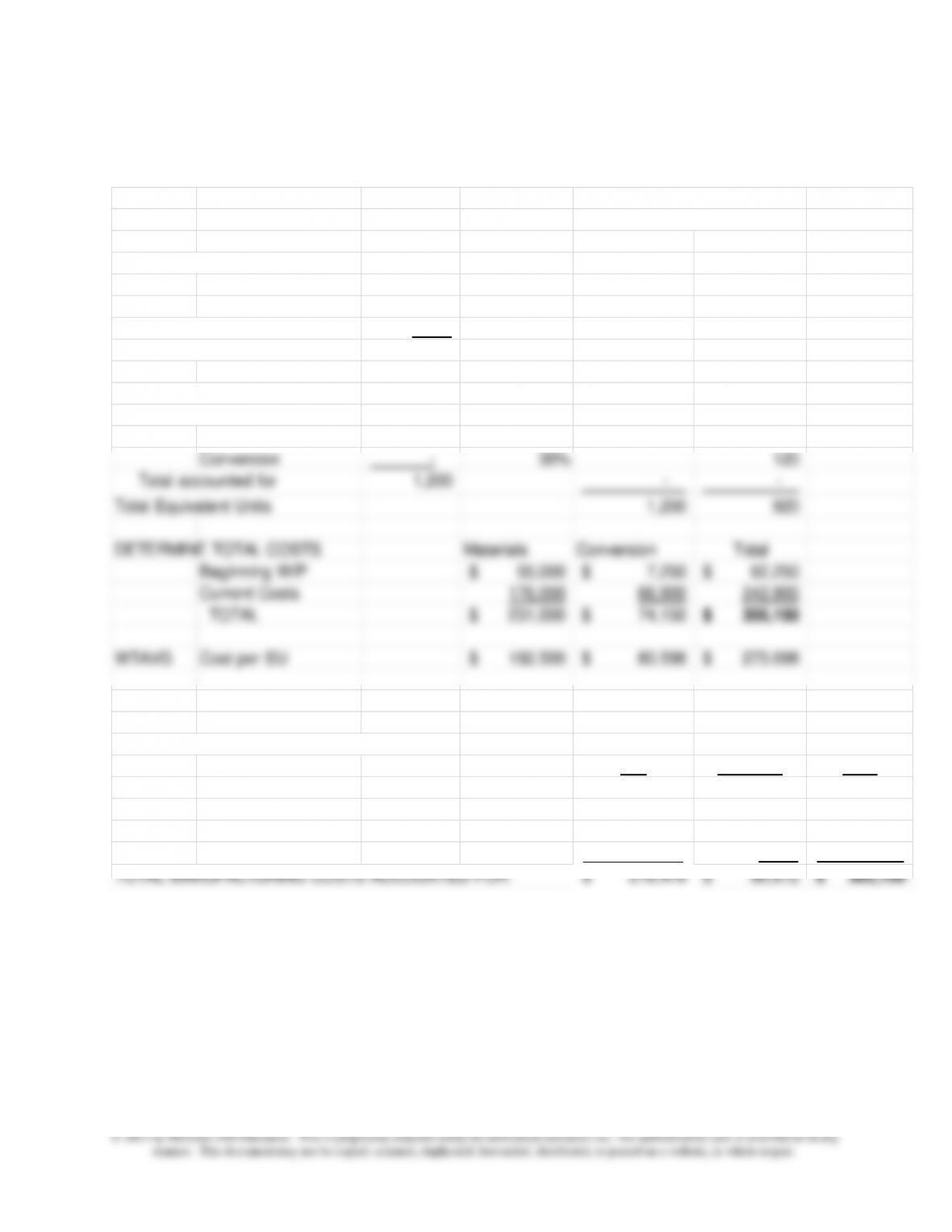

6-50 Process Costing and Activity Based Costing (40 min)

1.

Physical Percentage

Units Completion Materials Conversion

Beginning WIP 200

Materials 100%

Conversion 60%

Units started 1,000

Total to account for 1,200

Units Finshed 800 800 800

Ending WIP 400

Materials 100% 400

Conversion –

30% 120

Total accounted for 1,200 – –

Total Equivalent Units 1,200 920

DETERMINE TOTAL COSTS Materials Conversion Total

Beginning WIP 55,000$ 7,250$ 62,250$

Current Costs 176,000 66,900 242,900

TOTAL 231,000$ 74,150$ 305,150$

WTAVG Cost per EU 192.500$ 80.598$ 273.098$

Units Completed

Units in Ending

COST ASSIGNED -WEIGHTED AVERAGE and Transferred WIP

Out Inventory Total

Finished Goods 800 units 218,478$ 218,478$

Equivalent Units

Weighted Average

Chapter 6 – Process Costing

6-50 (continued –1)

2.

Physical Percentage Number of

Units Completion Materials Conversion Batches

Beginning WIP 200

Materials 100%

Conversion 60%

Units started 1,000

Total to account for 1,200

Units Finished 800 800 800 25

Ending WIP 400 75

Materials 100% 400

Conversion –

30% 120

Total accounted for 1,200 – – –

Total Equivalent Units 1,200 920 100

Total Number of Batches

DETERMINE TOTAL COSTS Materials Conversion Batch Total

Beginning WIP 55,000$ 7,250$ 62,250$

Current Costs 176,000 38,400 28,500 242,900

TOTAL 231,000$ 45,650$ 28,500$ 305,150$

WTAVG Cost per EU 192.5000$ 49.6196$ 285.0000$ 242.1196$

Units Completed Units in Ending

COST ASSIGNED -WEIGHTED AVERAGE and Transferred WIP

Out Inventory Total

Finished Goods

800 units 193,696$ 193,696$

Batch Costs 25 batches 7,125 7,125

Ending WIP

400 units –

Materials 77,000$ 77,000

Conversion – 5,954 5,954

Batch costs 75 batches – 21,375 21,375

Total Mfg. Costs Accounted For 200,821$ 104,329$ 305,150$

Weighted Average

Equivalent Units