Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-1

Chapter 7

Cost Allocation: Departments, Joint Products, and By-Products

Teaching Notes for Cases

7-1. Revenue Allocation; Utility Industry; Strategy

This case concerns the process used in the state of Texas to subsidize companies in the heavily

regulated telecommunications industry so that the historical goal of providing universal telephone service

at reasonable rates may be achieved in the state. The subsidization of local service, particularly in high

cost rural areas, by long distance and other more profitable services, is a cornerstone of telephone

regulation. Prior to its 1984 breakup, AT&T made enough profit from the long distance market it

dominated to subsidize local service throughout the country. Since divestiture of the seven regional

telephone companies, local exchange carriers (LECs) in Texas have been subsidized by not only

interexchange carriers (IXCs) such as AT&T, MCI, and Sprint but also by the state’s largest LEC,

Southwestern Bell Telephone Company (SWBT).

The Texas Public Utilities Commission (PUC) sets telephone rates for individual LECs based on

projections of revenues needed by them to earn target rates of return. These rates are functions of

investment community requirements. In addition to settlement payments from SWBT, LECs receive

access payments from other carriers for use of their facilities in the completion of calls. They also earn

revenues from intraLATA roll calls and local telephone service.

When a telephone company predicts its revenues will be insufficient to achieve its allowable rate

of return, it may petition the PUC for a rate increase. The commission then must decide how much

additional revenue, if any, to allow the company, and from what category(s) of service. If, for example,

the PUC decides to allow an LEC to bill its customers an additional $100,000 for local telephone service,

it will adjust the company’s rate structure to provide the increase. Due to the size of SWBT (it has

approximately 80% of the telephones in Texas), its intraLATA toll rates are assigned to all local exchange

carriers in the state; consequently, a toll rate increase granted to SWBT improves the earnings and rates of

return of all 59 companies.

The PUC monitors the earnings of LECs. It may take action against those whose rates of return

exceed their allowable rates. Thus, if a company is successful in efforts to substantially reduce operating

costs it may find itself in the odd position of being called before the PUC to justify the “excess” earnings

that result.

The case questions relate to the perceived need of Southwestern Bell managers to either change

the process by which the company subsidizes the other Texas LECs or replace it with procedures which

would result in a more equitable distribution of revenues. Instead of trying to provide the correct answer

to each question, students should focus on the relative merits of alternative courses of action. Also, they

should recognize that what has been labeled “the accountant’s creed” ⎯a more complex solution is a

better solution⎯is not necessarily true in this situation. The FCC’s process is very complex; students may

recommend simpler procedures which they believe would be preferable.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-2

Answers to Questions

1. For the perspective of SW Bell management accountants, the separation of non-traffic-sensitive (NTS)

costs by the frozen 1982 intrastate toll factor of 20% is the primary source of inequities in the current

pooling procedures. This factor greatly understates the current portion of SWBT’s expense and

investment amounts related to intrastate long distance service. If allocation factors based on actual current

even suggest that subsidies should be discontinued. They argue that although some smaller carriers might

not survive, the market system will attract companies that can provide telephone service profitably with

today’s new low-cost technology.

2. SW Bell officials could go to the PUC and ask for additional supervision and regulation to correct the

perceived inequities in the current system. They could point out that although the costs of telephone

technology have been declining steadily in recent years, the poolable expenses of the other LECs have

been increasing. SWBT representatives could argue that the relatively high costs of those companies may

be explained to some extent by the toll revenue sharing arrangement, which gives them little incentive to

reached among the larger companies, the smaller ones would have little choice but to accept a new

arrangement. Regardless of the direct negotiation approach selected, the companies involved would have

considerable flexibility in deriving an equitable settlement plan, although it necessarily would mean lower

payments to some if not most of them.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-3

3. The students’ answers to this question could vary as their attitudes toward governmental versus free

market solutions, big versus small companies, gradual versus rapid change, and the rights of a company’s

shareholders versus the rights of the customers. The focus of the case and wording of the questions

probably will lead many students to recommend some change that would reduce the subsidies SWBT

pays to the other LECs but stop short of immediately discontinuing them. Students should expect the

actual solution to be a compromise that is not entirely satisfactory to any of the affected parties.

SW Bell and several of the other large LECs recently informed the TECA and the PUC that they were

withdrawing from the pool. SWBT then reached separate agreements with the larger and smaller

PUC data indicate that the reduced subsidies to be paid under the new arrangement are sufficient to

maintain universal service in the state. Finally, the large companies now have additional incentives to

control costs, although incentives for the smaller companies remain inadequate. SWBT managers would

like to move the latter LECs to fixed payments after the agreement expires, and then gradually “wean”

them away from financial dependence on the company.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-4

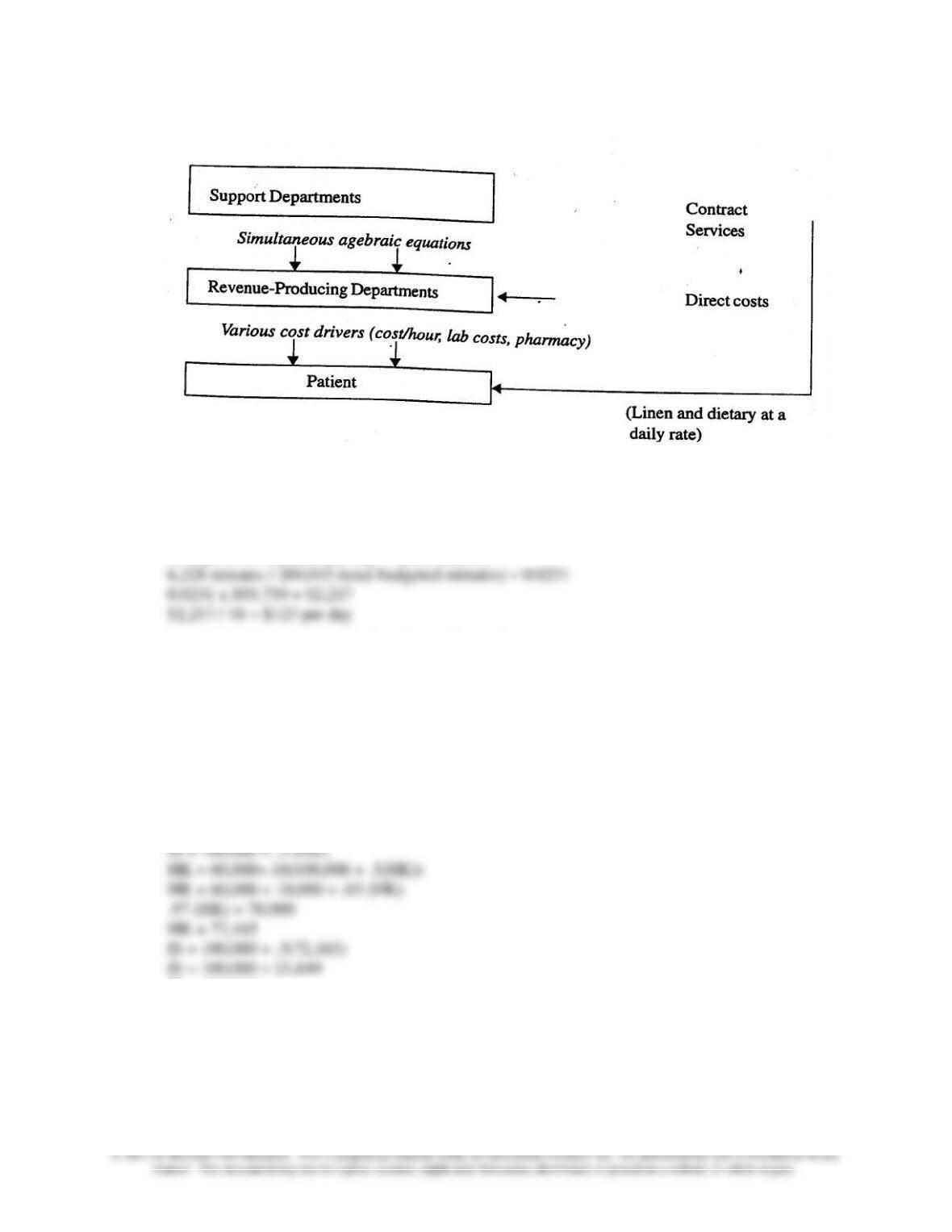

7-2. Brookwood Medical Center

The Brookwood Medical Center (BMC) case focuses on the new TSI accounting system. Concepts such

as direct and indirect costs and simultaneous algebraic allocations are addressed in a strategic context.

• Look at the quote from Carolyn Johnson at the beginning of the case. She states that upon losing

the bid for open hear surgeries, she did not know whether to be disappointed or relieved.

Ask the students to explain the basis for her reaction. Link the discussion to the Introduction case, CCR,

cost averaging. Managers at Brookwood did not have a clue about the cost of procedures. Ask the

students to think about the implications of long-term contracts. What if Brookwood acquires a contract at

a price below cost because the cost system is inadequate to help them accurately determine procedure

costs?

Answers to Questions

1. Costs were evaluated in aggregate. Also, the system focused on “charges” (a meaningless concept for

cost management purposes).

2. Consider the impact of variation in practice patterns across individual physicians. The managers at

Brookwood also were concerned with the cost of appropriate care. For example, some physicians ordered

out is that 80% of a person’s lifetime health care costs are spent in the final 90 days of life.

3. Draw a chart of the TSI system and point out the key principles as in the schematic below. The major

point is to stress that the indirect costs are allocated to revenue-producing departments using simultaneous

algebraic equations. In the second stage, both indirect and direct costs are applied to the patient using a

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-5

4. Consider how the daily rate (case Table 2) is determined for the Nursing Med/Surg department acuity

level 1 (based on information in case Table 3).

18 days x 346 minutes per day = 6,228 minutes

Acuity level 2 ($140) is calculated in an identical manner.

Why do we adjust for minutes of care? This captures the level of care required by different acuity levels.

Discuss intensive care with around the clock attention versus a step-down level of care with periodic

nursing visits. Consider the different rates at which resources are consumed.

5. At this point, you can begin the analysis by discussing the logic of the simultaneous algebraic equation

method. Case Table 4 illustrates an example of an iteration from the accounting system. Also, you can

work a simple manual example as follows:

HK = 60,000 + .10 (IS)

IS = 121,649

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-6

Solve the allocation using the allocation percentages as follows:

IS

HK

OR

ER

100,000

60,000

-0-

-0-

(121,649)

12,165

60,824

46,660

21,649

(72,165)

28,866

21,650

-0-

-0-

89,690

70,310

Case Table 5 is a printout from Brookwood’s TSI system. Notice that both revenue-producing and service

departments are included in the list. Education costs are allocated to the emergency room as follows: ER

= 124,212/4,886,856 = .0254

.0254 x $500,000 = $12,708

Iterations such as this would continue until all service department costs were allocated to revenue–

producing departments.

6. This question permits a discussion of the key elements found in ABC systems according to Cooper’s

hierarchy (unit level, batch level, product sustaining, and facility sustaining). Interestingly, we observed

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-7

Case 7-3 Business Services Corporation

The case involves the allocation of the indirect costs associated with holding and distributing replacement

parts used in servicing the computer and other business products sold to customers under a service

agreement. The company has two business units, the computer division and the business products

division. The source of the issue in the case is the determination of an appropriate method for allocating

the indirect costs of holding and distributing replacement parts used by both divisions. The costs

involved are significant. The company stocks 100,000 different parts in 40,000 locations. Further,

although a small number of parts may never be needed, the firm feels it must have at least a few units of

every part on hand so that it could service every customer’s need. This policy leads to obsolescence of

parts, an additional cost to that of storing and distributing the parts. At the time of the meeting described

in the case, parts overhead was averaging 70% of the cost of the parts charged directly to the product.

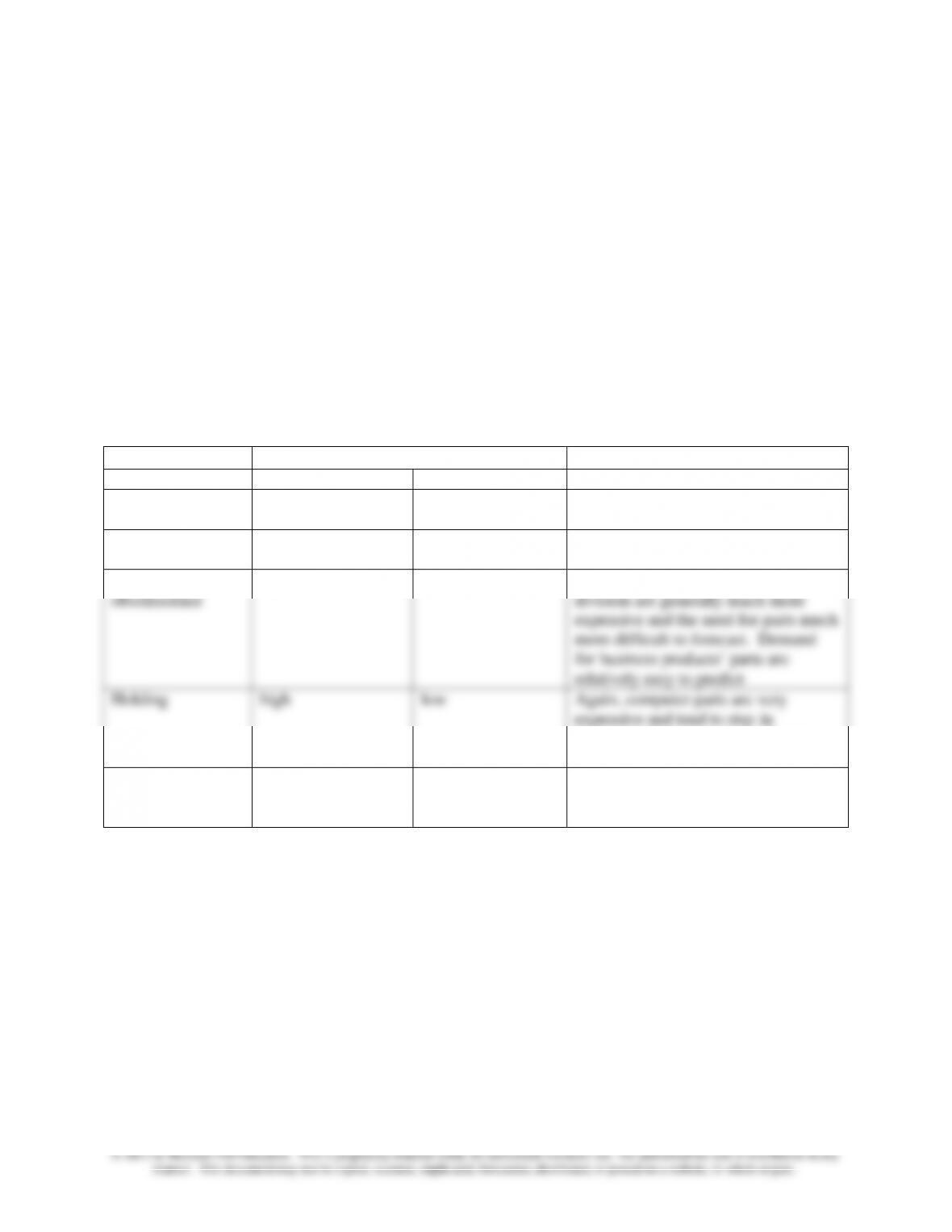

To put the issue in perspective, Exhibit 1 shows how each item in parts overhead is related to the

activity in the two divisions.

Exhibit 1: Relationship of parts overhead costs to activities in the two divisions.

Association With (usage by..)

Cost

Computer Division

Business Products

Explanation

Non-product usage

low

high

Most of the low value parts are used

by the business products division

Inventory variance

low

low

These are random costs and small in

amount

Parts scrap,

obsolescence

high

low

The parts needed for the computer

division are generally much more

expensive and the need for parts much

more difficult to forecast. Demand

for business products’ parts are

relatively easy to predict

Holding

high

low

Again, computer parts are very

expensive and tend to stay in

inventory for long periods. Business

products’ parts turn over quickly

Distribution

low

high

Very large volumes of business

products’ parts flow through the

system

Note that the current allocation method allocates all overhead on the basis of the cost of those parts (in

excess of $10 per part) actually used. The computer division feels this approach over charges the unit for

obsolescence and holding costs. Both divisions, in effect, are arguing that the allocation method does not

capture cause-and-effect relationships.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-8

Answers to questions:

1. The objectives of cost allocation are to motivate managers to work hard, to make decisions that

are consistent with top management’s strategy, and to provide a cost allocation method that

managers perceive to be fair.

2. What are the options to the current method? One option would be to trace all direct parts costs

(including cost of parts costing less than $10) to products and allocate overhead on this more

comprehensive measure of direct costs. This would solve one of the object is of the computer

division. Another possibility is to allocate on the basis of the number of parts used instead of

parts inventory, identifying those parts which are used exclusively by one division and summing

the costs of those unique parts for each division. In contrast, distribution and non-product usage

costs appear to vary with volume of activity. A volume measure such as the number of jobs

performed by each division might be satisfactory for these costs.

What the firm actually did:

The meeting ended with the president appointing a task force headed by the direct of accounting.

The task force recommended the following actions that were then implemented. First, all parts, including

low-value parts, that can be directly t4raced to a product or group of products are now charged to those

remaining obsolescence costs and the costs of carrying inventory are now allocated based on an estimate

of the dollar value of average inventory carried for each product line.

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-9

Teaching Strategy for Readings

“Managing Shared Services with ABM”

This article outlines the benefits of using shared services (i.e., finance and accounting services) in

large companies such as Ford Motor company, Sun Microsystems and Marriott. There is also a

discussion of how activity-based management (ref: Chapter 5) is used to manage the costs of these shared

services.

Discussion Questions:

1. How do the concepts of cost management for shared services differ from the concepts and methods

presented in chapter 7?

The concepts for cost management of shared services (chapter 5) differ from the concepts and

methods presented in Chapter 7 in the following way. The concepts for cost management of shared

services focus on identifying the cost drivers of the services, and on reducing these costs through

support department costs when activity-based costing is unlikely to be applied because of low complexity

of the manufacturing process, homogeneity of cost flows to products, or for other reasons.

2. Who are the customers referred to in the article?

The customers are the internal users of the firm’s support activities, in contrast to the

3. What do you think is the best way to manage the costs of shared services such as finance and

accounting?

7-10

7-2 “Simpler than ABC New Ideas for Using Microsoft Excel for Allocating Costs”

This article looks at a new method for service department cost allocation using Excel. It includes

important tips about making a useful Excel spreadsheet and it also factors in alternative methods to

compare against accounting for service department costs.

Discussion Questions:

1. Define an argument against the use of service department allocations.

Many reasons against allocating these costs refer to the arbitrary nature of the allocation method and the

distorting influence of these costs. The accuracy of the assignment of cost is in large part a function of the

2. In what cases should service department allocations be used instead of activity-based costing?

service cost allocations remain in use

3. What are some key factors in making a useful Excel worksheet?

1. Start by constructing formulas that take into account all cost flows in and out of the service department

to other service departments only.

5. If summed, the columns should equal 1.

6. The coefficient matrix forms the basis for the remaining matrices. There will be one matrix for each

service department plus the coefficient matrix. Service department matrices are constructed by replacing

Chapter 7 – Cost Allocation: Departments, Joint Products, and By-Products

7-11

8. Divide the individual service department. Determinants by the determinant for the coefficient matrix (

Cramer’s Rule). The result(s) are your allocated reciprocal costs for each service department. Summing

9. When allocating the costs from the service departments to the production departments, use the total

4. Explain why the matrix method can be seen as more efficient than the traditional method.

The matrix method demonstrated here avoids the double counting problem of the traditional method and

provides an intermediate cost, which can be directly associated with each service department. In addition,