Archives

978-0078025525 Appendix E Lecture Note

Appendix – Capital Investment Decisions: An Overview App-1 Appendix Capital Investment Decisions: An Overview Appendix Outline I. INTRODUCTION II. ANALYZING CASH FLOWS FOR PRESENT VALUE ANALYSIS ♦ Distinguishing between revenues, costs, and cash flows III. NET PRESENT VALUE ♦ Applying […]

978-0078025525 Chapter 1 Lecture Note Part 1

Chapter 01 – Cost Accounting: Information for Decision Making 1-1 Chapter 1 Cost Accounting: Information for Decision Making Learning Objectives 1. Describe the way managers use accounting information to create value in organizations. 2. Distinguish between the uses and users […]

978-0078025525 Chapter 1 Lecture Note Part 2

Chapter 01 – Cost Accounting: Information for Decision Making 1-10 • As seen in Exhibit 1.4, the managers of the retail and the wholesale operations are responsible for their own Center Margin, the difference between revenues and costs attributable to […]

978-0078025525 Chapter 1 Solution Manual Part 2

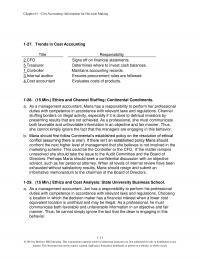

Chapter 01 – Cost Accounting: Information for Decision Making 1-11 1-27. Trends in Cost Accounting Title Responsibility 2 CFO Signs off on financial statements. 5 Treasurer Determines where to invest cash balances. 1 Controller Maintains accounting records. 3 Internal auditor […]

978-0078025525 Chapter 1 Solution Manual Part 3

Chapter 01 – Cost Accounting: Information for Decision Making 1-17 amount is so small that differential profit probably would not be the deciding factor. Errors in estimation alone could change the decision easily. c. Other factors would include (1) whether […]

978-0078025525 Chapter 1 Solution Manual Part 1

Chapter 01 – Cost Accounting: Information for Decision Making 1-1 Chapter 1 Cost Accounting: Information for Decision Making Solutions to Review Questions 1-1. Financial accounting is designed to provide information about the firm to external users. External users include investors, […]

978-0078025525 Chapter 10 Lecture Note Part 1

Chapter 10 – Fundamentals of Cost Management 10-1 Chapter 10 Fundamentals of Cost Management Learning Objectives 1. Describe how activity-based cost management can be used to improve operations. 2. Use the hierarchy of costs to manage costs. 3. Describe how […]

978-0078025525 Chapter 10 Lecture Note Part 2

Chapter 10 – Fundamentals of Cost Management 10–11 • Since the traditional income statement only shows resources supplied, a more informative report for managing capacity costs will include the following in an activity- based income statement (see Exhibit 10.11): Resources […]

978-0078025525 Chapter 10 Lecture Note Part 3

Chapter 10 – Fundamentals of Cost Management 10–17 • If a cost of quality system is not comprehensive, there is a danger that decisions will be distorted as managers focus on the costs the system includes but ignore unreported quality […]

978-0078025525 Chapter 10 Solution Manual Part 1

Chapter 10 – Fundamentals of Cost Management © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025525 Chapter 10 Solution Manual Part 2

Chapter 10 – Fundamentals of Cost Management 10–27. (15 min.) Activity-Based Costing of Customers: Rock Solid Bank & Trust. a. RSB&T can use this information to change the way banking services are priced. Managers at the bank may want to […]

978-0078025525 Chapter 10 Solution Manual Part 3

Chapter 10 – Fundamentals of Cost Management 10–45. (30 min.) Trading-off Costs of Quality: Nuke-It-Now. Nuke-It-Now Corporation Cost of Quality Report Year 1 % Year 2 % Sales revenue ………………………….. $3,500,000 $3,800,000 Prevention: Redesign process ………………………….. $ 29,000 $ 37,000 […]

978-0078025525 Chapter 10 Solution Manual Part 4

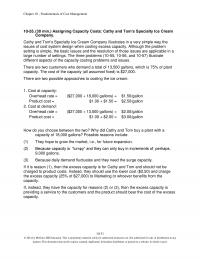

Chapter 10 – Fundamentals of Cost Management 10–55. (30 min.) Assigning Capacity Costs: Cathy and Tom’s Specialty Ice Cream Company. Cathy and Tom’s Specialty Ice Cream Company illustrates in a very simple way the issues of cost system design when […]

978-0078025525 Chapter 11 Lecture Note Part 1

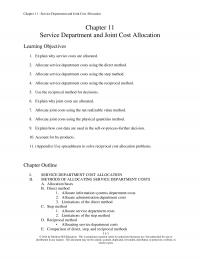

Chapter 11 – Service Department and Joint Cost Allocation 11-1 Chapter 11 Service Department and Joint Cost Allocation Learning Objectives 1. Explain why service costs are allocated. 2. Allocate service department costs using the direct method. 3. Allocate service department […]

978-0078025525 Chapter 11 Lecture Note Part 2

Chapter 11 – Service Department and Joint Cost Allocation 11–11 a $240,000 = $1,200,000 × 20.0%. b $200,000 = $500,000 × 40.0%. S1 To S2: $240,000 To P1: $360,000 To P2: $480,000 To P3: $120,000 S2 To S1: $200,000 To […]

978-0078025525 Chapter 11 Lecture Note Part 3

Chapter 11 – Service Department and Joint Cost Allocation 11–20 • It is important to note that the allocation of the joint costs is irrelevant for the current decision. The only costs and revenues relevant to the decision are those […]

978-0078025525 Chapter 11 Solution Manual Part 1

Chapter 11 – Service Department and Joint Cost Allocation 11-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, […]

978-0078025525 Chapter 11 Solution Manual Part 2

Chapter 11 – Service Department and Joint Cost Allocation 11-11 11–27. (20 min.) Cost Allocation—Step Method: University Printers Maintenance Personnel Printing Developing Service department costs ….………………………. $ 15,000 $36,000 NA NA Maintenancea ………………….………. (15,000) 3,000 $3,000 $ 9,000 Personnelb ……………………..…… […]

978-0078025525 Chapter 11 Solution Manual Part 3

Chapter 11 – Service Department and Joint Cost Allocation © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025525 Chapter 11 Solution Manual Part 4

Chapter 11 – Service Department and Joint Cost Allocation © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025525 Chapter 11 Solution Manual Part 5

Chapter 11 – Service Department and Joint Cost Allocation © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025525 Chapter 11 Solution Manual Part 6

Chapter 11 – Service Department and Joint Cost Allocation 11-51 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, […]

978-0078025525 Chapter 12 Lecture Note Part 1

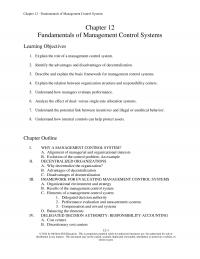

Chapter 12 – Fundamentals of Management Control Systems 12-1 Chapter 12 Fundamentals of Management Control Systems Learning Objectives 1. Explain the role of a management control system. 2. Identify the advantages and disadvantages of decentralization. 3. Describe and explain the […]

978-0078025525 Chapter 12 Lecture Note Part 2

Chapter 12 – Fundamentals of Management Control Systems 12–11 (2) The quality of services provided and their costs are not clearly linked. • For revenue centers, the obvious performance measure is the amount of revenues earned. Alternatively, for managers with […]

978-0078025525 Chapter 12 Lecture Note Part 3

Chapter 12 – Fundamentals of Management Control Systems 12–18 • Companies’ emphasis on short-term results motivates managers to take a chance on the future to make the current period look good. • A large and widely decentralized organization depends on […]

978-0078025525 Chapter 12 Solution Manual Part 1

Chapter 12 – Fundamentals of Management Control Systems 12-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025525 Chapter 12 Solution Manual Part 2

Chapter 12 – Fundamentals of Management Control Systems 12–11 The NBC Dateline report included about one minute of crash footage that showed how the gas tanks of certain old GM trucks could catch fire in a sideways collision. After hiring […]

978-0078025525 Chapter 12 Solution Manual Part 3

Chapter 12 – Fundamentals of Management Control Systems 12–17 12–35. (40 min.) Cost Allocations—Comparison of Dual and Single Rates: Pacific Hotels. a. Allocations based on time usage: (1) Department Proportion of Total Time Allocated Cost Luxury …………………………..………………………….. .15a $180,000b Resort […]

978-0078025525 Chapter 13 Lecture Note Part 1

Chapter 13 – Planning and Budgeting 13-1 Chapter 13 Planning and Budgeting Learning Objectives 1. Understand the role of budgets in overall organization plans. 2. Understand the importance of people in the budgeting process. 3. Estimate sales. 4. Develop production […]

978-0078025525 Chapter 13 Lecture Note Part 2

Chapter 13 – Planning and Budgeting 13–11 • An easy and inexpensive way is to start with a previous period’s actual or budgeted amounts and make adjustments for inflation, changes in operations, and similar changes between periods. • Exhibit 13.7 […]

978-0078025525 Chapter 13 Lecture Note Part 3

Chapter 13 – Planning and Budgeting 13–18 _____ 1. A statement of cash on hand at the start of the budget period, expected cash receipts, expected cash disbursements, and the resulting cash balance at the end of the budget period. […]

978-0078025525 Chapter 13 Solution Manual Part 1

Chapter 13 – Planning and Budgeting 13-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025525 Chapter 13 Solution Manual Part 2

Chapter 13 – Planning and Budgeting 13–11 13–28. (15 min.) Estimate Cash Collections: Duluth Company. Duluth Company Schedule of Cash Collections For the Month Ended December 31 Collections in December for sales prior to November ……. $ 24,000 November sales […]

978-0078025525 Chapter 13 Solution Manual Part 3

Chapter 13 – Planning and Budgeting 13–21 Solutions to Problems 13–40. (30 min.) Prepare Budgeted Financial Statements: Dancer Components. Dancer Components Budgeted Income Statement For Year 2 Calculations Sales revenue ……………………………………..…….. $6,389,700a $5,700,000 x 1.18 x .95 Manufacturing costs: Materials […]

978-0078025525 Chapter 13 Solution Manual Part 4

Chapter 13 – Planning and Budgeting © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025525 Chapter 14 Lecture Note Part 1

Chapter 14 – Business Unit Performance Measurement 14-1 Chapter 14 Business Unit Performance Measurement Learning Objectives 1. Evaluate divisional accounting income as a performance measure. 2. Interpret and use return on investment (ROI). 3. Interpret and use residual income (RI). […]

978-0078025525 Chapter 14 Lecture Note Part 2

Chapter 14 – Business Unit Performance Measurement 14–11 Example 3 (Continued from Example 1): Health Quest faces 12% of cost of capital. The Western Division of Health Quest currently earns an after-tax income of $400,000 based on assets of $2,000,000. […]

978-0078025525 Chapter 14 Lecture Note Part 3

Chapter 14 – Business Unit Performance Measurement 14–17 _____ 11. Sales income Operating . Answers 1. G 2. C 3. E 4. J 5. B 6. A 7. D 8. K 9. F 10. I 11. H © 2014 by […]

978-0078025525 Chapter 14 Solution Manual Part 1

Chapter 14 – Business Unit Performance Measurement 14-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025525 Chapter 14 Solution Manual Part 2

Chapter 14 – Business Unit Performance Measurement 14–11 14–30. (25 min.) Compare Historical Cost, Net Book Value To Gross Book Value: Caribbean Division. a. Net Book Value b. Gross Book Value Year 1 ($15,000,000 – $6,000,000) ($15,000,000 – $6,000,000) ($60,000,000 […]

978-0078025525 Chapter 14 Solution Manual Part 3

Chapter 14 – Business Unit Performance Measurement 14–21 14–39. (30 min.) Economic Value Added: Pitt, Inc. (In thousands of dollars) a. Residual Income $3,750 – 0.12 x ($4,000 + $5,000 – $1,500 – $1,250) = $3,000 b. ($3,750 – $3,500a) […]

978-0078025525 Chapter 14 Solution Manual Part 4

Chapter 14 – Business Unit Performance Measurement 14–30 14–46. (35 min.) Economic Value Added: Biddle Company. After-tax income ……………………………………………………… $400,000 Add back advertising expense for year 3 ……………………. 240,000 $640,000 Less amortization of advertising: Year 1 advertising: 10% x $100,000 […]

978-0078025525 Chapter 15 Lecture Note Part 1

Chapter 15 – Transfer Pricing 15-1 Chapter 15 Transfer Pricing Learning Objectives 1. Explain the basic issues associated with transfer pricing. 2. Explain the general transfer pricing rules and understand the underlying basis for them. 3. Identify the behavioral issues […]

978-0078025525 Chapter 15 Lecture Note Part 2

Chapter 15 – Transfer Pricing 15–11 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025525 Chapter 15 Lecture Note Part 3

Chapter 15 – Transfer Pricing 15–18 2. Cost-based transfer price at 105% of the full absorption cost per motor. 3. Negotiated transfer price of $18.5 per motor. Solution: Market-based transfer price @ $20 Cost-based transfer price @ $17.85 Negotiated transfer […]

978-0078025525 Chapter 15 Solution Manual Part 1

Chapter 15 – Transfer Pricing 15-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025525 Chapter 15 Solution Manual Part 2

Chapter 15 – Transfer Pricing 15–11 Solutions to Problems 15–29. (30 min.) Transfer Pricing With Imperfect Markets—ROI Evaluation, Normal Costing: Athena Company. a. ROI for Spartan Division. Income: [450,000 x ($28 – $8)] – [$14 x 500,000] = $2,000,000 ROI […]

978-0078025525 Chapter 15 Solution Manual Part 3

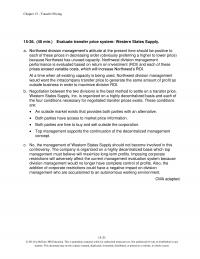

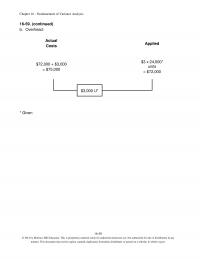

Chapter 15 – Transfer Pricing 15–21 15–36. (40 min.) Evaluate transfer price system: Western States Supply. a. Northwest division management’s attitude at the present time should be positive to each of these prices in decreasing order (obviously preferring a higher […]

978-0078025525 Chapter 16 Lecture Note Part 1

Chapter 16 – Fundamentals of Variance Analysis 16-1 Chapter 16 Fundamentals of Variance Analysis Learning Objectives 1. Use budgets for performance evaluation. 2. Develop and use flexible budgets. 3. Compute and interpret the sales activity variance. 4. Prepare and use […]

978-0078025525 Chapter 16 Lecture Note Part 2

Chapter 16 – Fundamentals of Variance Analysis 16–11 • Managers who are responsible for price variances would not be held responsible for efficiency variances and vice versa. • The total cost variance is the difference between budgeted and actual results […]

978-0078025525 Chapter 16 Lecture Note Part 3

Chapter 16 – Fundamentals of Variance Analysis 16–20 a Favorable variances should be credited; unfavorable variances should be debited. The variances are debited here for illustration only. • Direct labor Work–in–process inventory xx Direct labor price variance xx Direct labor […]

978-0078025525 Chapter 16 Solution Manual Part 1

Chapter 16 – Fundamentals of Variance Analysis 16-1 Chapter 16 Fundamentals of Variance Analysis Solutions to Review Questions 16–1. For performance evaluation purposes, the costing format should identify the actual costs for comparison with expected costs during the relevant period. […]

978-0078025525 Chapter 16 Solution Manual Part 2

Chapter 16 – Fundamentals of Variance Analysis 16–11 16–24. (45 min.) Sales Activity Variance: Data-2-Go. Flexible Budget (based on actual of 750,000 units) Sales Activity Variance Master Budget (based on budgeted 800,000 units) Sales revenue …………………………………..……….. $2,812,500 $187,500 U $3,000,000 […]

978-0078025525 Chapter 16 Solution Manual Part 3

Chapter 16 – Fundamentals of Variance Analysis © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, […]

978-0078025525 Chapter 16 Solution Manual Part 4

Chapter 16 – Fundamentals of Variance Analysis 16–31 16–41. (continued) (a) 1,500 units from actual column. (b) $1,500 U = $40,500 – $39,000. (c), (d) Budgeted sales price per unit = $40,500 ÷ 1,500 units = $27. Master budget = […]

978-0078025525 Chapter 16 Solution Manual Part 5

Chapter 16 – Fundamentals of Variance Analysis 16–41 16–50. (15 min.) Direct Materials: Clearwater Company. Actual Costs Price Variance Actual Inputs at Standard Price AP x 900 $20 x 900 = $18,000 $7,200 F 900 x AP = $18,000 – […]

978-0078025525 Chapter 16 Solution Manual Part 6

Chapter 16 – Fundamentals of Variance Analysis 16–50 16-59. (continued) b. Overhead: Actual Costs Applied $72,000 + $3,000 = $75,000 $3 x 24,000* units = $72,000 $3,000 U* * Given © 2014 by McGraw-Hill Education. This is proprietary material solely […]

978-0078025525 Chapter 17 Lecture Note Part 1

Chapter 17 – Additional Topics in Variance Analysis 17-1 Chapter 17 Additional Topics in Variance Analysis Learning Objectives 1. Explain how to prorate variances to inventories and cost of goods sold. 2. Use market share variances to evaluate marketing performance. […]

978-0078025525 Chapter 17 Lecture Note Part 2

Chapter 17 – Additional Topics in Variance Analysis 17–11 • A sales quantity variance occurs in multiproduct companies from the change in volume of sales, independent of any change in sales mix. Sales quantity variance = Standard contribution margin per […]

978-0078025525 Chapter 17 Lecture Note Part 3

Chapter 17 – Additional Topics in Variance Analysis 17–18 • Variances may occur because conditions change during the year but the standards do not. • Planned variance is one that is expected to occur if certain conditions affect operations. • […]

978-0078025525 Chapter 17 Solution Manual Part 1

Chapter 17 – Additional Topics in Variance Analysis 17-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025525 Chapter 17 Solution Manual Part 2

Chapter 17 – Additional Topics in Variance Analysis 17–11 17–24. (35 min.) Labor Mix and Yield Variance: Matt’s Eat ‘N Run. a. and b. Efficiency Variance Actual (AP x AQ) Purchase Price Variance (SP x AQ) Mix Variance (SP x […]

978-0078025525 Chapter 17 Solution Manual Part 3

Chapter 17 – Additional Topics in Variance Analysis 17–21 17–33. (30 min.) Nonmanufacturing Cost Variances: Springfield Bank. Incidental office costs comprise the variable costs. Salaries and the fixed office costs are all fixed. Variance analysis for the two classes of […]

978-0078025525 Chapter 17 Solution Manual Part 4

Chapter 17 – Additional Topics in Variance Analysis © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025525 Chapter 18 Lecture Note Part 1

Chapter 18 – Performance Measurement to Support Business Strategy 18-1 Chapter 18 Performance Measurement to Support Business Strategy Learning Objectives 1. Explain why management accountants should know the business strategy of their organization. 2. Explain why companies use nonfinancial performance […]

978-0078025525 Chapter 18 Lecture Note Part 2

Chapter 18 – Performance Measurement to Support Business Strategy 18–11 LO 18-6 Identify examples of nonfinancial performance measures and discuss the potential for improved performance resulting from improved activity management. ♦ Performance measures must be based on the organization’s responsibilities, […]

978-0078025525 Chapter 18 Lecture Note Part 3

Chapter 18 – Performance Measurement to Support Business Strategy 18–17 – reflect individual unit’s role in the organization. (3) Management must ensure that the performance measures are applied consistently and accurately. ♦ Companies benefit from using nonfinancial performance measures, but […]

978-0078025525 Chapter 18 Solution Manual Part 1

Chapter 18 – Performance Measurement to Support Business Strategy 18-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, […]

978-0078025525 Chapter 18 Solution Manual Part 2

Chapter 18 – Performance Measurement to Support Business Strategy 18–11 18–35. (20 min.) Manufacturing Cycle Time and Efficiency. Manufacturing cycle efficiency = Processing time Processing time + Moving time + Storing time + Inspection time = 5 hrs. 5 hrs. […]

978-0078025525 Chapter 18 Solution Manual Part 3

Chapter 18 – Performance Measurement to Support Business Strategy 18–17 18–43. (20 min.) Functional measures. Answers will vary, but might include any of the functional measures shown in Exhibit 18.7. The following is one example. An important critical success factor […]

978-0078025525 Chapter 2 Lecture Note Part 1

Chapter 02 – Cost Concepts and Behavior 2-1 Chapter 2 Cost Concepts and Behavior Learning Objectives 1. Explain the basic concept of “cost.” 2. Explain how costs are presented in financial statements. 3. Explain the process of cost allocation. 4. […]

978-0078025525 Chapter 2 Lecture Note Part 2

Chapter 02 – Cost Concepts and Behavior 2-11 The inventory amounts at the end of an accounting period (i.e., Ending inventory) for direct materials, work in process, and finished goods will appear on the balance sheet as part of the […]

978-0078025525 Chapter 2 Lecture Note Part 3

Chapter 02 – Cost Concepts and Behavior 2-19 Demonstration Problem 4 The following information is available for each unit of the finished product produced and sold: Sales price $60 Variable manufacturing cost 20 Fixed manufacturing cost 12* Variable marketing and […]

978-0078025525 Chapter 2 Solution Manual Part 1

Chapter 02 – Cost Concepts and Behavior 2-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025525 Chapter 2 Solution Manual Part 2

Chapter 02 – Cost Concepts and Behavior 2-11 2-34. (10 min.) Prepare Statements for a Service Company: Jupiter Consultants Sales revenue …………………………….. $8,500,000 (Given) Cost of services sold (b) ……………….. 4,450,000 (Sales revenue – gross margin) Gross margin ………………………………. $4,050,000 […]

978-0078025525 Chapter 2 Solution Manual Part 4

Chapter 02 – Cost Concepts and Behavior 2-31 2-54. (30 min.) Prepare Statements for a Manufacturing Company: Butte Components. Butte Components Statement of Cost of Goods Sold For the Year Ended December 31 ($000) Work in process, Jan. 1 …………………………………… […]

978-0078025525 Chapter 2 Solution Manual Part 3

Chapter 02 – Cost Concepts and Behavior 2-21 2-44. (continued) d. Full cost: $21.00 + $24.00 + $12.00 + ($135,000 ÷ 30,000 units) + $5.00 + ($117,000 ÷ 30,000 units) = $70.40 e. Profit margin = Sales price – full […]

978-0078025525 Chapter 2 Solution Manual Part 5

Chapter 02 – Cost Concepts and Behavior 2-41 2-60. (40 Min.) Find the Unknown Information. a. Cost of goods sold = Finished goods beginning inventory + Cost of goods manufactured – Finished goods ending inventory = $22,320 + $611,650 – […]

978-0078025525 Chapter 3 Lecture Note Part 1

Chapter 03 – Fundamentals of Cost-Volume-Profit Analysis 3-1 Chapter 3 Fundamentals of Cost-Volume-Profit Analysis Learning Objectives 1. Use cost-volume-profit (CVP) analysis to analyze decisions. 2. Understand the effect of cost structure on decisions. 3. Use Microsoft Excel to perform CVP […]

978-0078025525 Chapter 3 Lecture Note Part 2

Chapter 03 – Fundamentals of Cost-Volume-Profit Analysis 3-10 Target volume in units = Fixed cost (F) + [After-tax target profit / (1 – t)] Unit contribution margin (P- V) , where [After-tax target profit / (1 – t)] determines the […]

978-0078025525 Chapter 3 Solution Manual Part 1

Chapter 03 – Fundamentals of Cost-Volume-Profit Analysis 3-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025525 Chapter 3 Solution Manual Part 2

Chapter 03 – Fundamentals of Cost-Volume-Profit Analysis 3-11 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025525 Chapter 3 Solution Manual Part 3

3-21 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in […]

978-0078025525 Chapter 3 Solution Manual Part 4

Chapter 03 – Fundamentals of Cost-Volume-Profit Analysis 3-31 3-52. (30 min.) Extensions of the CVP Model—Multiple Products: Sell Block. a. Individuals + Partnerships + Corporations 60,000 $200 + 4,000 $1,000 + 16,000 $2,000 = $48,000,000 PX 60,000 […]

978-0078025525 Chapter 4 Lecture Note Part 1

Chapter 04 – Fundamentals of Cost Analysis for Decision Making 4-1 Chapter 4 Fundamentals of Cost Analysis for Decision Making Learning Objectives 1. Use differential analysis to analyze decisions. 2. Understand how to apply differential analysis to pricing decisions. 3. […]

978-0078025525 Chapter 4 Lecture Note Part 2

Chapter 04 – Fundamentals of Cost Analysis for Decision Making © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, […]

978-0078025525 Chapter 4 Solution Manual Part 3

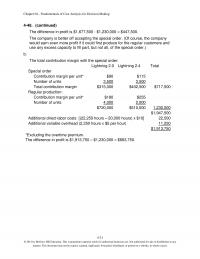

Chapter 04 – Fundamentals of Cost Analysis for Decision Making 4-21 4-48. (continued) The difference in profit is $1,677,500 – $1,230,000 = $447,500. The company is better off accepting the special order. (Of course, the company would earn even more […]

978-0078025525 Chapter 4 Solution Manual Part 1

Chapter 04 – Fundamentals of Cost Analysis for Decision Making 4-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, […]

978-0078025525 Chapter 4 Solution Manual Part 2

Chapter 04 – Fundamentals of Cost Analysis for Decision Making 4-11 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, […]

978-0078025525 Chapter 4 Solution Manual Part 4

Chapter 04 -Fundamentals of Cost Analysis for Decision Making 4-31 4-52. (continued) f. 6,000 Regular Stoves Produced Contract 2,000 Regular Stoves; Produce 1,600 Modified Stoves and 4,000 Regular Stoves In-house Regular (In) Regular (Out) Modified Total Revenue ………………………………. $2,220,000 $1,480,000 […]

978-0078025525 Chapter 4 Solution Manual Part 5

Chapter 04 -Fundamentals of Cost Analysis for Decision Making 4-41 4-57. (continued) e. At an increase in the cost of labor from $16 to $19, the contribution margins per constrained resource of labor (10,000 additional hours) would be as follows: […]

978-0078025525 Chapter 4 Solution Manual Part 6

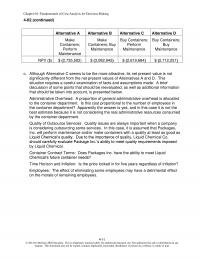

Chapter 04 -Fundamentals of Cost Analysis for Decision Making 4-51 4-62. (continued) Alternative A Alternative B Alternative C Alternative D Make Containers; Perform Maintenance Make Containers; Buy Maintenance Buy Containers; Perform Maintenance Buy Containers; Buy Maintenance NPV ($) $ (2,735,502) […]

978-0078025525 Chapter 5 Lecture Note Part 1

Chapter 05 – Cost Estimation 5-1 Chapter 5 Cost Estimation Learning Objectives 1. Understand the reasons for estimating fixed and variable costs. 2. Estimate costs using engineering estimates. 3. Estimate costs using account analysis. 4. Estimate costs using statistical analysis. […]

978-0078025525 Chapter 5 Lecture Note Part 2

Chapter 05 – Cost Estimation 5-11 • In addition to the cost-estimating equation, the regression program provides other useful statistics. (1) Correlation coefficient (R, or multiple R) is a measure of the linear relation between two or more variables, such […]

978-0078025525 Chapter 5 Lecture Note Part 3

Chapter 05 – Cost Estimation 5-18 Y = number of labor hours per unit required for the last single unit produced (when incremental unit-time learning model is adopted), a = number of labor hours required to produce the first unit, […]

978-0078025525 Chapter 5 Solution Manual Part 1

5 Cost Estimation Solutions to Review Questions 5-1. Common methods of cost estimation are engineering analysis, account analysis, and statistical analysis of historical data. 5-2. Engineering estimates are based on design specifications and industry and firm cost standards. 5-3. Engineering […]

978-0078025525 Chapter 5 Solution Manual Part 2

5-31. (15 min.) Methods of Estimating Costs—Scattergraph: Adriana Corporation. ©The McGraw-Hill Companies, Inc., 2014 Solutions Manual, Chapter 5 187 ©The McGraw-Hill Companies, Inc., 2014 188 Fundamentals of Cost Accounting 5-32. (15 min.) Methods of Estimating Costs—Scattergraph: Adriana Corporation. 5-33. (10 […]

978-0078025525 Chapter 5 Solution Manual Part 3

5-46 (continued) b. Scattergraph $500 $550 $600 $650 $700 $750 30 35 40 45 50 55 60 65 Calls Cost c. The scattergraph shows a reasonably linear pattern, but the high point would lie below a straight line that best […]

978-0078025525 Chapter 5 Solution Manual Part 4

5-51 (continued) b. Using the results from the “improved” regression, the cost equation for overhead costs can be written as: Monthly overhead = $9,777 + $11.69 x number of deliveries This implies a contribution margin per delivery of $8.31 (= […]

978-0078025525 Chapter 5 Solution Manual Part 5

5-55. (40 min.) Learning Curves (Appendix 5B). a. The learning rate coefficient is -0.152004, so the table in Exhibit 5-21 would be as follows for a learning rate of 90%. (Note: rounding errors might lead to slight differences from the […]

978-0078025525 Chapter 6 Lecture Note Part 1

Chapter 06 – Fundamentals of Product and Service Costing 6-1 Chapter 6 Fundamentals of Product and Service Costing Learning Objectives 1. Explain the fundamental themes underlying the design of cost systems. 2. Explain how cost allocation is used in a […]

978-0078025525 Chapter 6 Lecture Note Part 2

Chapter 06 – Fundamentals of Product and Service Costing 6-11 determined by the labor activity regardless of the seniority or skills of the employees, direct labor hours would be the better choice. • Allocation is inherently arbitrary and imprecise. The […]

978-0078025525 Chapter 6 Lecture Note Part 3

Chapter 06 – Fundamentals of Product and Service Costing 6-17 _____ 1. A system that provides information about the costs of processes, products, and services used and produced by an organization. _____ 2. Represents the cost per unit of the […]

978-0078025525 Chapter 6 Solution Manual Part 1

Chapter 06 – Fundamentals of Product and Service Costing 6-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, […]

978-0078025525 Chapter 6 Solution Manual Part 2

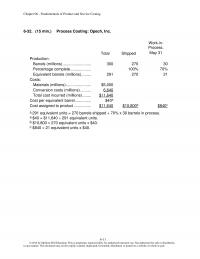

Chapter 06 – Fundamentals of Product and Service Costing 6-11 6-32. (15 min.) Process Costing: Opech, Inc. Total Shipped Work-in– Process, May 31 Production: Barrels (millions) …………………….. 300 270 30 Percentage complete ………………. 100% 70% Equivalent barrels (millions) ……… 291 […]

978-0078025525 Chapter 6 Solution Manual Part 3

Chapter 06 – Fundamentals of Product and Service Costing 6-20 b. The costs per patient are $114.75 per hospital patient hour and $29.44 per other patient. Hospital Patients Other Patients Total Equipment hours used ……………………….…. 240 120 360 Direct labor-hours […]

978-0078025525 Chapter 7 Lecture Note Part 1

Chapter 07 – Job Costing 7-1 Chapter 7 Job Costing Learning Objectives 1. Explain what job and job shop mean. 2. Assign costs in a job cost system. 3. Account for overhead using predetermined rates. 4. Apply job costing methods […]

978-0078025525 Chapter 7 Lecture Note Part 2

Chapter 07 – Job Costing 7-11 For underapplied overhead, Applied manufacturing overhead xx Work–in-process inventory xx Finished goods inventory xx Cost of goods sold xx Manufacturing overhead control xx The overhead accounts have no remaining balances after allocation. (3) Prorating […]

978-0078025525 Chapter 7 Solution Manual Part 1

Chapter 07 – Job Costing 7-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

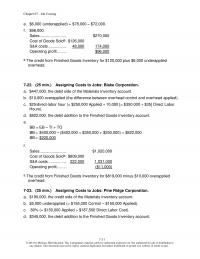

978-0078025525 Chapter 7 Solution Manual Part 2

Chapter 07 – Job Costing 7-11 e. $6,000 (underapplied) = $78,000 – $72,000. f. $96,000. Sales …………………….……. $270,000 Cost of Goods Solda .…………………………. $126,000 S&A costs ……………..…………… 48,000 174,000 Operating profit ………………………….. $96,000 a The credit from Finished Goods Inventory […]

978-0078025525 Chapter 7 Solution Manual Part 3

Chapter 07 – Job Costing 7-21 7-39. (50 min.) Assigning Costs—Missing Data. Materials Inventory Balance 11/1 45,400 (a) 86,200 Direct materials Purchases 113,600 (a) 16,400 Indirect materials Balance 11/30 56,400 Work-in-Process Inventory Balance 11/1 32,600 (given) Direct materials 86,200 (b) […]

978-0078025525 Chapter 7 Solution Manual Part 4

Chapter 07 – Job Costing 7-31 7-46. (55 min.) Tracing Costs In A Job Company: Dungan Cabinetry a. (1) Materials Inventory ………………………………………………. 53,700 Accounts Payable …………………………………………….. 53,700 (2) Manufacturing Overhead ………………………………………. 1,500 Materials Inventory ……………………………………………. 1,500 (3) Accounts Payable ………………………………………………… […]

978-0078025525 Chapter 7 Solution Manual Part 5

Chapter 07 – Job Costing 7-41 7-49. (continued) (e) Overhead applied = Ending manufacturing overhead – beginning manufacturing overhead + overapplied overhead = $434,000a – $369,800a + $2,400a = $66,600 (f) Loss = $172,400a + $140,628 + $135,400 + $66,600 […]

978-0078025525 Chapter 8 Lecture Note Part 1

Chapter 08 – Process Costing 8-1 Chapter 8 Process Costing Learning Objectives 1. Explain the concept and purpose of equivalent units. 2. Assign costs to products using a five-step process. 3. Assign costs to products using weighted-average costing. 4. Prepare […]

978-0078025525 Chapter 8 Lecture Note Part 2

Chapter 08 – Process Costing 8-11 Solution: 1. Work-in-process inventory account Beginning balance 1,000 Plus: Units started 5,000 Less: Units transferred out ? Ending balance 400 1,000 + 5,000 = Units transferred out (?) + 400. The number of units […]

978-0078025525 Chapter 8 Lecture Note Part 3

Chapter 08 – Process Costing 8-18 Mixing $220,000 $100,000 $120,000 Packaging 75,900 37,500 38,400 Total materials cost $295,900 $137,500 $158,400 Conversion: Mixing $219,000 $75,000 $144,000 Packaging 131,400 45,000 86,400 Total conversion cost $350,400 $120,000 $230,400 Total product cost $646,300 $257,500 […]

978-0078025525 Chapter 8 Solution Manual Part 5

Chapter 08 – Process Costing © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted […]

978-0078025525 Chapter 8 Solution Manual Part 2

Chapter 08 – Process Costing 8-11 8-24. (20 min.) Compute Equivalent Units—FIFO method: Santiago Company. Physical Units Conversion Eq. Units Flow of units: Units to be accounted for: Beginning WIP inventory ………………………………………. 22,500 Units started this period ………………………………………… 255,000 Total […]

978-0078025525 Chapter 8 Solution Manual Part 1

Chapter 08 – Process Costing 8-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025525 Chapter 8 Solution Manual Part 3

Chapter 08 – Process Costing 8-21 8-33. (20 min.) Assign Costs to Goods Transferred Out and Ending Inventory— FIFO Method: Pacific Ink. Physical Units Equivalent Units Materials Eq. units Conversion Costs Eq. units Flow of units: Units to be accounted […]

978-0078025525 Chapter 8 Solution Manual Part 4

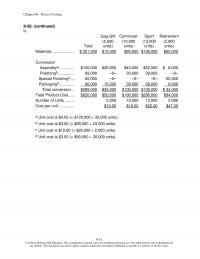

Chapter 08 – Process Costing 8-31 8-39. (continued) b. Total Gag-Gift (5,000 units) Commuter (10,000 units) Sport (13,000 units) Retirement (2,000 units) Materials ………………… $ 321,000 $15,000 $90,000 $156,000 $60,000 Conversion Assemblya ………….. $120,000 $20,000 $40,000 $52,000 $ 8,000 Polishingb […]

978-0078025525 Chapter 8 Solution Manual Part 6

Chapter 08 – Process Costing 8-51 8-48. (30 min.) Determine Degree of Completion—FIFO method: Saline Solutions. c. The ending work in process is at least 60% complete with respect to conversion costs. This is a problem that requires relatively few […]

978-0078025525 Chapter 8 Solution Manual Part 7

Chapter 08 – Process Costing 8-61 8-52. (continued) Cost of units transferred to finished goods: Product Unit Material Cost Stitching Department Unit Cost Customizing Department Unit Cost Unit Cost Rookie …… $30 + $ 42 + $ –0– = $ […]

978-0078025525 Chapter 8 Solution Manual Part 8

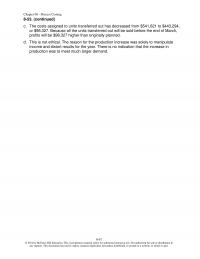

Chapter 08 – Process Costing 8-67 8-53. (continued) c. The costs assigned to units transferred out has decreased from $541,621 to $443,294, or $98,327. Because all the units transferred out will be sold before the end of March, profits will […]

978-0078025525 Chapter 9 Lecture Note Part 1

Chapter 09 – Activity-Based Costing 9-1 Chapter 9 Activity-Based Costing Learning Objectives 1. Understand the potential effects of using externally reported product costs for decision making. 2. Explain how a two-stage product costing system works. 3. Compare and contrast plantwide […]

978-0078025525 Chapter 9 Lecture Note Part 2

Chapter 09 – Activity-Based Costing 9-11 (3) product-related, and (4) facility-related. • Exhibit 9.12 provides example of costs and cost drivers associated with each of the four levels. • Not all activity-based costing systems need to have all four levels […]

978-0078025525 Chapter 9 Lecture Note Part 3

Chapter 09 – Activity-Based Costing 9-17 Matching A. Activity-based costing D. Death spiral B. Cost driver E. Department allocation method C. Cost hierarchy F. Plantwide allocation method _____ 1. Represents a classification of cost drivers into general levels of activity, […]

978-0078025525 Chapter 9 Part 1

Chapter 09 – Activity-Based Costing 9-1 © 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025525 Chapter 9 Solution Manual Part 3

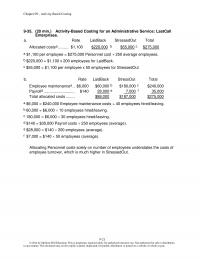

Chapter 09 – Activity-Based Costing 9-21 9-35. (20 min.) Activity-Based Costing for an Administrative Service: LastCall Enterprises. a. Rate LaidBack StressedOut Total Allocated costsa ………………………….. $1,100 $220,000 b $55,000 c $275,000 a $1,100 per employee = $275,000 Personnel cost ÷ […]

978-0078025525 Chapter 9 Solution Manual Part 2

Chapter 09 – Activity-Based Costing 9-11 9-28. (35 min.) Activity-Based versus Traditional Costing: Rodent Corporation. a. Rate Wired Wireless Total Direct labora ………………………….. $290,100 $ 109,900 $400,000 Direct materialsb ……..…………………… $187,500 $ 171,000 $358,500 Overhead costs Prod. runs ………………………….. $6,600 […]

978-0078025525 Chapter 9 Solution Manual Part 4

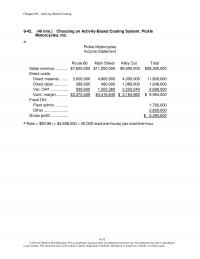

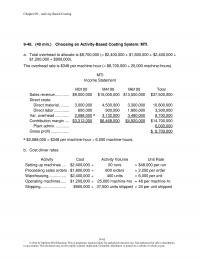

Chapter 09 – Activity-Based Costing 9-31 9-42. (40 min.) Choosing an Activity-Based Costing System: Pickle Motorcycles, Inc. a. Pickle Motorcycles Income Statement Route 66 Main Street Alley Cat Total Sales revenue ………………………….. $7,600,000 $11,200,000 $9,500,000 $28,300,000 Direct costs: Direct material […]

978-0078025525 Chapter 9 Solution Manual Part 5

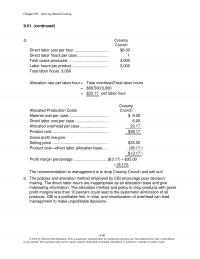

Chapter 09 – Activity-Based Costing 9-41 9-48. (40 min.) Choosing an Activity-Based Costing System: MTI. a. Total overhead to allocate is $8,700,000 (= $2,400,000 + $1,800,000 + $2,400,000 + $1,200,000 + $900,000). The overhead rate is $348 per machine-hour (= […]

978-0078025525 Chapter 9 Solution Manual Part 6

Chapter 09 – Activity-Based Costing 9-50 9-51. (continued) d. Creamy Crunch Direct labor cost per hour ………………………….. $6.00 Direct labor hours per case ………………………..… 1 Total cases produced ……………………………….… 3,000 Labor hours per product ……………………………… 3,000 Total labor hours: 3,000 […]

Accounting Chapter 1 1 The Set Activities That Transforms Raw

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 1 2 The Field Accounting That Depends Generally

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 1 3 Financial Accounting Provides Historical Perspective While

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 1 4 Cost Accounting Integral Part The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 1 5 Restaurant Deciding Whether Wants Update Its

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 1 6 Levis Strauss And Co Maker Levis

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 1 Activity Analysis One The First Stages

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 2 The Degree Which Good Service Meets

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 3 Enterprises Quality Control Report For August

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 4 Folly Beach Industries Decides Price Delivery

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 5 Chang Inc Has Developed The Following

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 6 Rogers Company Preparing Its Annual Profit

10-101 117. Rogers Company is preparing its annual profit plan. As part of its analysis of the cost of its purchasing activity, management estimates that the $125,000 for purchasing support should be assigned to the individual vendors from the information […]

Accounting Chapter 10 7 Julie King The Production Manager Mus sell

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 10 8 Burns Corporation Manufactures Large Kitchen Appliances

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 11 1 Service Department Costs Are Generally Treated

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 11 2 Net Realizable Value The Split off Point

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 11 3 The Following Information Relates Ray Corporation

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 11 4 Anchorage Company Manufactures Three Main Products

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 11 5 Byproduct Revenue Treated Other Revenue Instead

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 11 6 New London Corporation Has Two Production

11-101 123. Smalltown Hospital is a small hospital with two service departments and three revenue areas: The hospital wants to allocate the service department costs to the revenue areas. Housekeeping is allocated based on square footage; Laundry is allocated based […]

Accounting Chapter 11 7 Bruce Consulting Has Two Service Departments

11-120 141. Bruce Consulting has two service departments: S1 and S2 and three production departments: P1, P2, and P3. Data for a recent month follow: Required: (a) Determine the allocations to the production departments when the reciprocal method is used. […]

Accounting Chapter 12 1 Decentralization Refers The Delegation Decision making Authority

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 12 2 A manager makes a decision that is beneficial for a specific investment

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 12 3 The Document Creation Center DCC For

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 12 4 Peake Corporations Maintenance Department Provides Services

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 12 5 The Human Resources Department For Hammond

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 12 6 Blaster Drive in Fast food Restaurant That Sells

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 12 7 The Fixed Costs Operating The Maintenance

12-116 141. Traffic Services Company has recently expanded by acquiring two smaller companies in the transportation industry. Prior to these acquisitions, Traffic Services used a centralized style of organization because it was small enough that the top management team was […]

Accounting Chapter 13 1 Master Budget Consists A Organizational Goals B

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 13 2 Which One The Following Budgets Would

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 13 3 Rizzo Corporation Had 17000 Units Brake

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 13 4 National Telephone Company Has Been Forced

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 13 5 Mosbey Inc Working Its Cash Budget

13–81 103. The Carlquist Company makes and sells a product called Product K. Each unit of Product K sells for $24 dollars and has a unit variable cost of $18. The company has budgeted the following data for November: • […]

Accounting Chapter 13 6 Mccoo Inc Bases Its Manufacturing Overhead

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 13 7 Dengel Inc Preparing Its Cash Budget

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 1 Economic Value Added Eva Adjustments Are

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 2 How Will Increases The Following Items

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 3 What was B Division’s return on investment (ROI) last year

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 4 Residual Income Performance Evaluation That Used

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 5 Division A could reduce its investment so that its asset turnover

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 6 Deutsch Products Has The Following Data

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 14 7 Was The Companys Residual Income Last Year

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 15 1 Transfer Prices Would Used By Production

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 15 2 Division Can Sell Externally For 40

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 15 3 Company Has Two Divisions And Each

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 15 4 You Have Been Provided With The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 15 5 Division Harkin Company Has The Capacity

15–81 AACSB: Analytic AICPA FN: Measurement Blooms: Apply Difficulty: 3 Hard Learning Objective: 15-02 Explain the general transfer pricing rules and understand the underlying basis for them. Topic Area: Applying the General Principle 103. Division X makes a part that […]

Accounting Chapter 15 6 The Parts Division Now Producing And Selling

15-101 121. Meredith Motor Works has just acquired a new Battery Division. The Battery Division produces a standard 12volt battery that it sells to retail outlets at a competitive price of $20. The retail outlets purchase about 800,000 batteries a […]

Accounting Chapter 15 7 What is the range of transfer prices within which both the Divisions’

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 1 Operating Budget Would Not Include Cash

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 2 The General Model Price Variance Calculated

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 3 The Following Information Summarizes The Standard

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 4 Dickey Company Had Total Underapplied Overhead

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 5 The Kessler Company Has The Following

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 6 What is the variable overhead efficiency variance

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 16 7 Predetermined Variable Overhead Rate 175 Given Predetermined

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 1 If variances are not prorated at the end of the accounting period

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 2 What The Correct Journal Entry Record

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 3 The XYZ Company Had The Following

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 4 Tiger Company’s Direct Labor Cost For

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 5 When The Actual Amount Raw Material

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 6 Seiler Associates Consulting Firm Specializing Business

17-101 116. Seiler & Associates is a consulting firm specializing in business location studies. The results for last year, along with the budget, are as follows: Required: (Be sure to indicate whether the variance is favorable or unfavorable.) a. Prepare […]

Accounting Chapter 17 7 Predetermined Variable Overhead Rate 175 Given Predetermined

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 17 8 The Variances Are Too Aggregate Level And

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 1 Description Organizations Values Definition Its Responsibilities

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 2 Which The Following Typically Considered Objective

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 3 Which The Following Represents Value added Time

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 4 Firms Ability Implement Low Costs

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 5 The Alcatane Manufacturing Company Collected The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 6 Indicate How The Following Concepts Are

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 18 7 Companies Are Continuously Seeking Ways Improve

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 2 1 Which The Following Best Distinguishes Opportunity

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 2 2 The Term Gross Margin For Manufacturing

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 2 3 Laner Company Has The Following Data

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 2 4 Cheboygan Company Has The Following Unit

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 2 5 The Following Cost And Inventory Data

2-81 111. The Plastechnics Company began operations several years ago. The company purchased a building and, since only half of the space was needed for operations, the remaining space was rented to another firm for rental revenue of $20,000 per […]

Accounting Chapter 2 6 The Boyceville Machining Company Provided You

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 2 7 Standford Corporation Has Provided The Following

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 1 Cost volume profit CVP Analysis Simple But Powerful

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 2 Breakeven Point 400 Units Variable Costs

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 3 Sanfran Has The Following Data How

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 4 You Have Been Provided With The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 5 James Company Has Margin Safety Percentage

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 6 Required A Compute The Breakeven Point

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 7 Pines Inc Produces And Sells Two

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 3 8 Interior Masters Manufactures Decorative Iron Railings

3-134 148. Interior Masters manufactures decorative iron railings. In preparing for next year’s operations, management has developed the following estimates: Required: Compute the following items: a. Unit contribution margin. b. Contribution margin ratio. c. Break-even in dollar sales. d. Margin […]

Accounting Chapter 4 1 The Alternative Courses Action Make or buy Decision

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 4 2 Differential Costs Are CMA Adapted The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 4 3 The Speedy Delivery Service Considering The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 4 4 For The Past Five Years The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 4 5 Nationwide Discount Chain Has Approached Hi speed With

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 4 6 Tofte Industries Manufactures 30000 Components Per

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 4 7 The Memo Should Address The Following

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 5 1 The Quality The Cost Equation Depends

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 5 2 Given The Following Information Compute The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 5 3 Which The Following The Difference Between

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 5 4 The Learning Curve Equation AXB The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 5 5 What Additional Information Would You Like See

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 5 6 The Mallard Company’s Total Overhead Costs

5-92 103. The Mallard Company’s total overhead costs at various levels of activity are presented below: Assume that the overhead costs above consist of indirect labor, scheduling salaries, and maintenance. The breakdown of these costs for the month of November […]

Accounting Chapter 6 1 The Cost Flow Diagram For Product

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 6 2 Which The Following Would The Least

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 6 3 For Case B Above What The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 6 4 Which The Following Would Probably The

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 6 5 Roswell Refiners Restarted Operations September After

© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole […]

Accounting Chapter 6 6 Assume That The Following T accounts Represent