Archives

978-0134475585 Chapter 1 Solution 1

CHAPTER 1 THE MANAGER AND MANAGEMENT ACCOUNTING 1-1 How does management accounting differ from financial accounting? Management accounting measures, analyzes, and reports financial and nonfinancial information Financial accounting focuses on reporting to external parties such as investors, government agencies, and […]

978-0134475585 Chapter 1 Solution 2

SOLUTION (10–15 min.) Professional ethics and reporting division performance. 1. Mendez’s ethical responsibilities are well summarized in the IMA’s “Standards of Ethical Behavior for Practitioners of Management Accounting and Financial Management” (Exhibit 1-7 of text). Areas of ethical responsibility include […]

978-0134475585 Chapter 1 Solution 3

SOLUTION (30 min.) Pharmaceutical company, budgeting, ethics. 1. The overarching principles of the IMA Statement of Ethical Professional Practice are Honesty, Fairness, Objectivity and Responsibility. The statement’s corresponding “Standards for Ethical Behavior…” require management accountants to Perform professional duties in […]

978-0134475585 Chapter 10 Solution 1

CHAPTER 10 DETERMINING HOW COSTS BEHAVE 10-1 What two assumptions are frequently made when estimating a cost function? The two assumptions are 1. Variations in the level of a single activity (the cost driver) explain the variations in the 2. […]

978-0134475585 Chapter 10 Solution 2

.SOLUTION (20 min.) Various cost-behavior patterns. 1. K 2. B 3. G 10-24 Matching graphs with descriptions of cost and revenue behavior. (D. Green, adapted) Given here are a number of graphs. Required: The horizontal axis of each graph represents […]

978-0134475585 Chapter 10 Solution 3

SOLUTION (30min.) High-low method and regression analysis. 1. See Solution Exhibit 10-36. SOLUTION EXHIBIT 10-36 250 300 350 400 450 500 $22,000 $23,000 $24,000 $25,000 $26,000 $27,000 $28,000 $29,000 Number of Weekly Orders Weekly Total Costs 2. Number of Orders […]

978-0134475585 Chapter 10 Solution 4

SOLUTION (15-20min.) Interpreting regression results, matching time periods. 1. Here is the regression data for monthly operating costs as a function of the total freight miles travelled by Sprit vehicles: SUMMARY OUTPUT Regression Statistics ANOVA df SS MS F Significance […]

978-0134475585 Chapter 10 Solution 5

SOLUTION (20 min.) Cost-volume-profit and regression analysis. 1a. Average cost of manufacturing = Total manufacturing costs Number of drink bottles = $808,500 210,000 = $3.85 per bottle This cost is higher than the $3.75 per bottle that Kraff has quoted. […]

978-0134475585 Chapter 10 Solution 6

SOLUTION (30–40 min.) Cost estimation, cumulative average-time learning curve. 1. Cost to produce the 2nd through the 7th troop deployment boats: ´ $1,194,000 Direct manufacturing labor (DML), 61,8521 $42 ´ 2,597,784 Variable manufacturing overhead, 61,852 $26 ´ 1,608,152 Other manufacturing […]

978-0134475585 Chapter 10 Solution 7

SOLUTION (30 min.) Multiple regression (continuation of 10-42). 1. Solution Exhibit 10-43 presents the regression output for medical supplies costs using both number of procedures and number of patient-hours as independent variables (cost drivers). SOLUTION EXHIBIT 10-43 Regression Output for […]

978-0134475585 Chapter 11 Solution 1

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 11-1 Outline the five-step sequence in a decision process. The five steps in the decision process outlined in Exhibit 11-1 of the text are 1. Identify the problem and uncertainties. 11-2 Define relevant […]

978-0134475585 Chapter 11 Solution 2

SOLUTION (25 min.) Dropping a customer, activity-based costing, ethics. 1. CRS would not benefit from dropping Donnelly’s Pizza because it would lose $43,680 in revenues and save $43,344 in costs resulting in a $336 decrease in operating income. Difference: Incremental […]

978-0134475585 Chapter 11 Solution 3

SOLUTION (25 min.) Closing down divisions. 1. and 2. Division A Division B Sales $504,000 $948,000 Variable costs of goods sold ($440,000 ´ 0.90; $930,000 ´ 0.80) Division A Division B Fixed costs of goods sold ($440,000 ´ 0.10; $930,000 […]

978-0134475585 Chapter 11 Solution 4

SOLUTION (30 min.) Make versus buy, activity-based costing, opportunity costs. 1. Relevant costs under buy alternative: Relevant costs under make alternative: Direct materials $320,000 Direct manufacturing labor 160,000 Variable manufacturing overhead 80,000 Inspection, setup, materials handling 8,000 Machine rent 12 […]

978-0134475585 Chapter 11 Solution 5

SOLUTION (15-20 min.) Short-run pricing, capacity constraints. 1. Per pair of shorts: Fabric (3 yards ´ $12 per yard) If Fashion Fabrics can get all the fabric it needs and has sufficient production capacity, then the minimum price it should […]

978-0134475585 Chapter 11 Solution 6

SOLUTION (30 min.) Special order, activity-based costing. 1. Direct materials cost per unit ($600,000 10,000 units) = $60 per unit Reward One’s opera&ng income under the alterna&ves of accep&ng/rejec&ng the special order are: Without One-Time Only Special Order 10,000 […]

978-0134475585 Chapter 11 Solution 7

SOLUTION (20 min.) Choosing customers. If Newbury accepts the additional business from Kimberly, it would take an additional 800 machine-hours. If Newbury accepts all of Kimberly’s and Wallace’s business for February, it Wallace Kimberly Corporation Corporation Contribution margin per machine-hour […]

978-0134475585 Chapter 11 Solution 8

SOLUTION (20–25 min.) Relevant costs, contribution margin, product emphasis. 1. Cola Lemonade Punch Natural Orange Juice 2. The argument fails to recognize that shelf space is the constraining factor. There are only 12 feet of front shelf space to be […]

978-0134475585 Chapter 12 Solution 1

CHAPTER 12 STRATEGY, BALANCED SCORECARD, AND STRATEGIC PROFITABILITY ANALYSIS 12-1 Define strategy. 12-2 Describe the five key forces to consider when analyzing an industry. The five key forces to consider in industry analysis are: (1) competitors, (2) potential entrants into […]

978-0134475585 Chapter 12 Solution 2

SOLUTION (25–30 min.) Strategic analysis of operating income (continuation of 12-21). 1. Operating Income Statement 2016 2017 Revenues ($30 ´ 200,000; $31 ´ 225,000) $6,000,000 $6,975,000 2. The Growth Component Revenue effect of growth = Actual units of Actual units […]

978-0134475585 Chapter 12 Solution 3

SOLUTION (20 min.) Analysis of growth, price-recovery, and productivity components (continuation of 12-25 and 12-26). Effect of the industry-market-size factor on operating income Of the 10-unit increase in sales from 200 to 210 units, 3% or 6 (3% 200) […]

978-0134475585 Chapter 12 Solution 4

SOLUTION(30 min.) Balanced scorecard. 1. The market for color laser printers is competitive. Vic’s strategy is to produce and sell high-quality laser printers at a low cost. The key to achieving higher quality is reducing defects The scorecard correctly measures […]

978-0134475585 Chapter 12 Solution 5

SOLUTION EXHIBIT 12-42A Strategy Map for WrightAir On the business side of the balanced scorecard, WrightAir measures the motivation of ground crew (learning and growth perspective) that helps to reduce turnaround time of the planes on the ground (internal business […]

978-0134475585 Chapter 12 Solution 6

SOLUTION EXHIBIT 12-33B Strategy Map for Scott Company In the learning and growth perspective, Scott measures the percentage of employees trained in quality management and the percentage of manufacturing processes with real-time feedback. These objectives improve manufacturing processes, which has […]

978-0134475585 Chapter 13 Solution 1

CHAPTER 13 PRICING DECISIONS AND COST MANAGEMENT 13-1 What are the three major influences on pricing decisions? The three major influences on pricing decisions are 13-2 “Relevant costs for pricing decisions are full costs of the product.” Do you agree? […]

978-0134475585 Chapter 13 Solution 2

SOLUTION (20 min.) Target costs, effect of product-design changes on product costs. 1. and 2. Manufacturing costs of HJ6 in 2016 and 2017 are as follows: 2016 2017 Per Unit Per Unit Total (2) = Total (4) = (1) (1) […]

978-0134475585 Chapter 13 Solution 3

SOLUTION (25 min.) Considerations other than cost in pricing decisions. 1. Guest nights on weeknights: 18 weeknights × 100 rooms × 70% = 1,260 Guest nights on weekend nights: Total costs for June: Depreciation $ 25,000 Administrative costs 40,000 Fixed […]

978-0134475585 Chapter 13 Solution 4

SOLUTION (20 mins.) Anti-trust laws and pricing. 1. The company is not practicing price discrimination because all customers are being offered the same prices. The offer is simply restricting the times and locations that the promotion is available but not […]

978-0134475585 Chapter 13 Solution 5

SOLUTION (25 min.) Cost-plus, target return on investment pricing. ´ 2. Revenues* $4,800,000 Variable costs [($3.00 + $2.00) 400,000 cases ´ 2,000,000 Contribution margin 2,800,000 Fixed costs ($400,000 + $700,000 + $500,000) 1,600,000 Operating income (from requirement 1) $1,200,000 * […]

978-0134475585 Chapter 14 Solution 1

CHAPTER 14 COST ALLOCATION, CUSTOMER-PROFITABILITY ANALYSIS, AND SALES-VARIANCE ANALYSIS 14-1 “I’m going to focus on the customers of my business and leave cost-allocation issues to my accountant.” Do you agree with this comment by a division president? Explain. Disagree. Cost […]

978-0134475585 Chapter 14 Solution 2

Customer-Level Operating Income $126,45 0 $81,225 $1,050 $(15,300) $(25,050) -$60,00 0 -$30,00 0 $ 0 $30,00 0 $60,00 0 $90,00 0 $120,00 0 $150,00 0 Customers Custo mer-Le vel Opera ting Incom e Grainger Avery Okie Duran Wizard SOLUTION (20−30 […]

978-0134475585 Chapter 14 Solution 3

SOLUTION (25 min.) Cost allocation to divisions. Percentages for various allocation bases (old and new): Pulp Paper Fibers Total (1) Division margin percentages $6,000,000; $14,600,000; $19,400,000 ¸ ¸ 30.0 15.0 55.0 100.0 (3) Share of floor space 106,400; 70,680; 202,920 […]

978-0134475585 Chapter 14 Solution 4

SOLUTION (20 min.)Market-share and market-size variances (continuation of 14-27). In some editions of the text, the last sentence before “Required” reads “However, actual total sales volume in the western region was 1.5 million cartons.” The word “western” should be replaced […]

978-0134475585 Chapter 15 Solution 1

CHAPTER 15 ALLOCATION OF SUPPORT-DEPARTMENT COSTS, COMMON COSTS, AND REVENUES 15-1 Distinguish between the single-rate and the dual-rate methods. The single-rate (cost-allocation) method makes no distinction between fixed costs and variable 15-2 Describe how the dual-rate method is useful to […]

978-0134475585 Chapter 15 Solution 2

SOLUTION (20 min.) Revenue allocation, bundled products. 1a. Under the stand-alone revenue-allocation method based on selling price, Smarty will be allocated 40% of all revenues, or $36 of the bundled selling price, and Sublime will be allocated 60% of all […]

978-0134475585 Chapter 15 Solution 3

SOLUTION (50 min.) Support-department cost allocation, reciprocal method (continuation of 15-19). 1a. Support Departments Operating Departments AS I S Govt. Corp. Reciprocal Method Computation AS = $600,000 + 0.10 IS IS =$2,400,000 + 0.25AS IS = $2,400,000 + 0.25 ($600,000 […]

978-0134475585 Chapter 15 Solution 4

SOLUTION (20 min.) Fixed cost allocation. 1. i) Allocation using actual usage. Department (1) Actual Usage (2) Percentage of Total Usage (3) = (2) ÷ 130,000 Allocation (4) = (3) × $2,000,000a expense related to building. ii) Allocation using planned […]

978-0134475585 Chapter 15 Solution 5

SOLUTION (20-25 mins.) Stand-alone revenue allocation 1. Allocation using individual selling price per unit. Computer Hardware Component Individual Selling Price per Unit Percentage of Total Price Allocation % × $1,500 2. Allocation using cost per unit Computer Hardware Component Cost […]

978-0134475585 Chapter 15 Solution 6

SOLUTION (20 min.) Support-department cost allocations: direct, step-down, and reciprocal methods. 1 a. Allocate the total Support Department costs to the operating departments under the Direct Allocation Method: Eastern Department Western Department Departmental Overhead Costs $650,000 $ 920,000 From: Information […]

978-0134475585 Chapter 16 Solution 1

CHAPTER 16 COST ALLOCATION: JOINT PRODUCTS AND BYPRODUCTS 16-1 Give two examples of industries in which joint costs are found. For each example, what are the individual products at the splitoff point? Exhibit 16-1 presents many examples of joint products […]

978-0134475585 Chapter 16 Solution 2

SOLUTION (30 min.) Joint-cost allocation, sales value, physical measure, NRV methods. 1a. PANEL A: Allocation of Joint Costs using Sales Value at Splitoff Method Special B/ Beef Ramen Special S/ Shrimp Ramen Total Sales value of total production at splitoff […]

978-0134475585 Chapter 16 Solution 3

SOLUTION (25 min.) Methods of joint-cost allocation, ending inventory. 1. Net realizable value of human product: Net realizable value of veterinarian product: 500 gallons × ($450 – $20) = $215,000 Joint costs: $50,000 + $155,000 = $205,000 Joint costs charged […]

978-0134475585 Chapter 16 Solution 4

SOLUTION(40 min.) Joint-cost allocation, process further or sell. 1. a. Physical-measure method Red Rock White Rock Gravel Total .20; .30; .50 × $190,000 b. Sales Value at Split off method Red Rock White Rock Gravel Total Sales Value of total […]

978-0134475585 Chapter 16 Solution 5

SOLUTION EXHIBIT 16-23 (all numbers are in thousands) 16-24 Alternative joint-cost-allocation methods, further-process decision. The Tempura Spirits Company produces two products—methanol (wood alcohol) and turpentine—by a joint process. Joint costs amount to $124,000 per batch of output. Each batch totals […]

978-0134475585 Chapter 17 Solution 1

CHAPTER 17 PROCESS COSTING 17-1 Give three examples of industries that use process-costing systems. Industries using process costing in their manufacturing area include chemical processing, oil 17-2 In process costing, why are costs often divided into two main classifications? Process […]

978-0134475585 Chapter 17 Solution 2

SOLUTIO (10 min.) Journal entries (continuation of 17-36). 1. Work in Process––Assembly Department 4,635,000 Accounts Payable 4,635,000 Work in Process––Assembly Department Beginning inventory, October 1 1,489,650 1. Direct materials 4,635,000 2. Conversion costs 2,575,125 3. Transferred out to Work in […]

978-0134475585 Chapter 17 Solution 3

SOLUTION (20 min.) Operation costing. 1. Calculate the conversion cost rates for each department: Relax Refresh Total Budgeted Conversion Cost Cost Driver Budgeted Quantity of Cost Driver Conversion Cost Rate Mixing $11,760 Direct labor-hours 1,200 $9.80 per labor-hour Blending 20,160 […]

978-0134475585 Chapter 17 Solution 4

SOLUTION EXHIBIT 17-44B Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory; FIFO Method of Process Costing, Stitching Department of Spelling Sports for […]

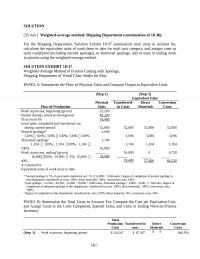

978-0134475585 Chapter 17 Solution 5

SOLUTION EXHIBIT 17-29B Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory; Weighted-Average Method of Process Costing for ZanyBrainy Corporation for October 2017. […]

978-0134475585 Chapter 18 Solution 1

CHAPTER 18 SPOILAGE, REWORK, AND SCRAP 18-1 Why is there an unmistakable trend in manufacturing to improve quality? 18-2 Distinguish among spoilage, rework, and scrap. Spoilage—units of production that do not meet the standards required by customers for good units […]

978-0134475585 Chapter 18 Solution 2

SOLUTION (2025 min.) Physical units, inspection at various stages of completion Inspection Inspection Inspection at 20% at 45% at 100% Work in process, beginning (25%)* Started during March 2,500 30 ,000 2,500 30 ,000 2,500 30 ,000 *Degree of completion […]

978-0134475585 Chapter 18 Solution 3

2. The cost per equivalent unit of beginning inventory and of work done in the current period differ substantially: Beginning Inventory Work Done in Current Period Direct Materials Conversion Costs Cost per equivalent unit (weighted-average) $204*$82* Cost per equivalent unit […]

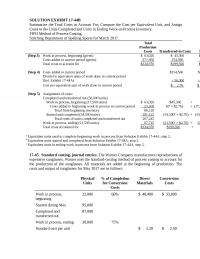

978-0134475585 Chapter 18 Solution 4

SOLUTION (35 min.) Weighted-average method, Shipping Department (continuation of 18-36). For the Shipping Department, Solution Exhibit 18-37 summarizes total costs to account for, calculates the equivalent units of work done to date for each cost category, and assigns costs to […]

978-0134475585 Chapter 18 Solution 5

SOLUTION EXHIBIT 18-24 Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign Costs to the Units Completed, Spoiled Units, and Units in Ending Work-in-Process Inventory; FIFO Method of Process Costing, MacLean Manufacturing Company, November […]

978-0134475585 Chapter 19 Solution 1

SCHAPTER 19 BALANCED SCORECARD: QUALITY AND TIME 19-1 Describe two benefits of improving quality. Quality costs (including the opportunity cost of lost sales because of poor quality) can be as 19-2 How does conformance quality differ from design quality? Explain. […]

978-0134475585 Chapter 19 Solution 2

SOLUTION (25 min.) Nonfinancial measures of quality and time. 1. 2016 2017 125 = 5% 400 = 4% Percentage of defective units shipped 2,500 10,000 Customer complaints as a percentage of units shipped 190 = 7.6% 2,500 250 = 2.5% […]

978-0134475585 Chapter 19 Solution 3

SOLUTION (25 min.) Costs of quality, quality improvements. 1. iCover’s managers plan to increase spending on design changes and process engineering to improve product quality. These are prevention activities. iCover’s managers plan to increase 2. Cost of making quality improvements […]

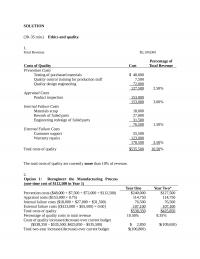

978-0134475585 Chapter 19 Solution 4

SOLUTION (30–35 min.) Ethics and quality. 1. Total Revenue $5,100,000 Costs of Quality Cost Percentage of Total Revenue Prevention Costs 127 ,500 2.50% Appraisal Costs Product inspection 153 ,000 153 ,000 3.00% Internal Failure Costs Materials scrap 18,000 Rework of […]

978-0134475585 Chapter 19 Solution 5

SOLUTION (25–30 min.) Waiting times, manufacturing cycle times. 1a. Average waiting time for an order of Z35 ( ) ( ) ( ) 2 Annual average number Manufacturing time of orders of Z35 per order of Z35 Annual machine Annual […]

978-0134475585 Chapter 2 Solution 1

CHAPTER 2 AN INTRODUCTION TO COST TERMS AND PURPOSES 2-1 Define cost object and give three examples. 2-2 Define direct costs and indirect costs. Direct costs of a cost object are related to the particular cost object and can be […]

978-0134475585 Chapter 2 Solution 2

SOLUTION (15–20 min.) Classification of costs, merchandising sector. Cost object: DVDs sold in movie section of store Cost variability: With respect to changes in the number of DVDs sold There may be some debate over classifications of individual items, especially […]

978-0134475585 Chapter 2 Solution 3

SOLUTION (20 min.) Total costs and unit costs Number of attendees 0 50 100 175 200 Variable cost per attendee (Materials $35 + Food, $75 Fixed Costs per session (Trainer, $11,000 + Materials, $2,500 + Catering, $5,000 − Offset for […]

978-0134475585 Chapter 2 Solution 4

SOLUTION (20 min.) Flow of Inventoriable Costs. (All numbers below are in millions). 1. Direct materials inventory 10/1/2017 $ 105 Direct materials used (385) Direct materials inventory 10/31/2017 $ 85 2. Total manufacturing overhead costs $ 450 Subtract: Variable manufacturing […]

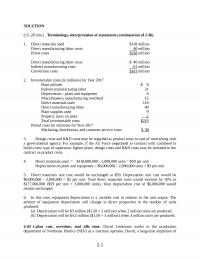

978-0134475585 Chapter 2 Solution 5

SOLUTION (15–20 min.) Terminology, interpretation of statements (continuation of 2-36). 1. Direct materials used $118 million 2. Inventoriable costs (in millions) for Year 2017 Plant utilities $ 8 Indirect manufacturing labor 21 Depreciation—plant and equipment 6 Miscellaneous manufacturing overhead 15 […]

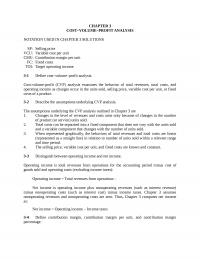

978-0134475585 Chapter 3 Solution 1

CHAPTER 3 COST–VOLUME–PROFIT ANALYSIS NOTATION USED IN CHAPTER 3 SOLUTIONS SP: Selling price VCU: Variable cost per unit CMU: Contribution margin per unit FC: Fixed costs TOI: Target operating income 3-1 Define cost–volume–profit analysis. Cost-volume-profit (CVP) analysis examines the behavior […]

978-0134475585 Chapter 3 Solution 2

SOLUTION (20 min.) CVP exercises. Revenues Variable Costs Contribution Margin Fixed Costs Budgeted Operating Income Orig. $11,000,000G$7,500,000G$3,500,000 $3,000,000G$500,000 1. 11,000,000 7,150,000 3,850,000a3,000,000 850,000 2. 11,000,000 7,850,000 3,150,000b3,000,000 150,000 9. Alternative 1, a 10% increase in contribution margin holding revenues constant, […]

978-0134475585 Chapter 3 Solution 3

SOLUTION (15 min.) CVP analysis, international cost structure differences. Variable Variable Sales Price Annual Manufacturing Marketing and Contribution Operating Income to Retail Fixed Cost per Distribution Cost Margin Breakeven Breakeven for Budgeted Sales Country Outlets Costs Rug per Rug Per […]

978-0134475585 Chapter 3 Solution 4

SOLUTION (15 min.) Contribution margin, decision making. 1. Revenues $600,000 Deduct variable costs: 2. Contribution margin percentage = $198,000 $600,000 = 33% 3. Incremental revenue (25% × $600,000) = $150,000 Incremental contribution margin (33% × $150,000) $49,500 Incremental fixed costs […]

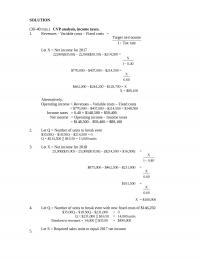

978-0134475585 Chapter 3 Solution 5

SOLUTION (30–40 min.) CVP analysis, income taxes. 1. Revenues – Variable costs – Fixed costs = rateTax 1 incomenet Target Alternatively, Operating income = Revenues – Variable costs – Fixed costs = $770,000 – $407,000 – $214,500 = $148,500 […]

978-0134475585 Chapter 3 Solution 6

SOLUTION (20-30 min.) CVP, alternative cost structures. 1. Variable cost per unit = $10 Contribution margin per unit = Selling price –Variable cost per unit Fixed Costs: Manager’s salary ($72,000 × 0.5) ÷12 $3,000 per month Rent 1,000 per month […]

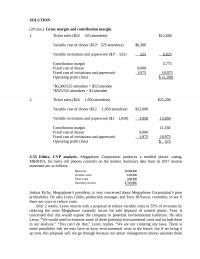

978-0134475585 Chapter 3 Solution 7

SOLUTION (20 min.) Gross margin and contribution margin. 1. Ticket sales ($24 ´ 525 attendees) $12,600 2. Ticket sales ($24 ´ 1,050 attendees) $25,200 Variable cost of dinner ($12 ´ 1,050 attendees) $12,600 Variable invitations and paperwork ($1 ´ 1,050) […]

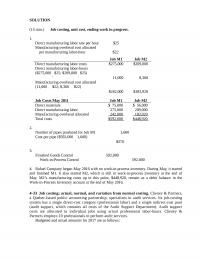

978-0134475585 Chapter 4 Solution 1

CHAPTER 4 JOB COSTING 4-1 Define cost pool, cost tracing, cost allocation, and cost-allocation base. Cost pool––a grouping of individual indirect cost items. 4-2 How does a job-costing system differ from a process-costing system? In a job-costing system, costs are […]

978-0134475585 Chapter 4 Solution 2

SOLUTION (20 -30 min.) Job costing, normal and actual costing. 1. Budgeted indirect- cost rate = Budgeted indirect costs (assembly support) Budgeted direct labor-hours = $8,800,000 220,000 hours = $40 per direct labor-hour Actual indirect- cost rate = Actual indirect […]

978-0134475585 Chapter 4 Solution 3

SOLUTION (10–15 min.) Accounting for manufacturing overhead. 1. Budgeted manufacturing overhead rate = $4,140,000 180,000 labor-hours = $23 per direct labor-hour 2. Work-in-Process Control 4,347,000 3. $4,337,000– $4,347,000 = $10,000 overallocated, an insignificant amount of difference compared to manufacturing overhead […]

978-0134475585 Chapter 4 Solution 4

SOLUTION (15 min.) Job costing, unit cost, ending work in progress. 1. Direct manufacturing labor rate per hour $25 Manufacturing overhead cost allocated per manufacturing labor-hour $22 Job M1 Job M2 ¸ ¸ 11,000 8,360 Manufacturing overhead cost allocated (11,000 […]

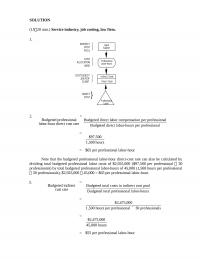

978-0134475585 Chapter 4 Solution 5

SOLUTION (1520 min.) Service industry, job costing, law firm. 1. Profession al La bor-Hou rs Lega l Support COST OBJECT: JOB FOR CLIENT INDIRECT COST POOL COST ALLOCATION BASE } DIRECT COST Ind irect Costs Direct Costs […]

978-0134475585 Chapter 4 Solution 6

Work in process inventory 12/31/2017 SOLUTION (35 min.) General ledger relationships, under- and overallocation. The solution assumes all materials used are direct materials. A summary of the T-accounts for Southwick Company before adjusting for under- or overallocation of overhead follows: […]

978-0134475585 Chapter 4 Solution 7

1/1/201 7 25,00 0 630,00 0 1/1/201 7 280,00 0 2,900,00 0 1/1/201 7 320,00 0 2,930,00 0 650,00 0 Dir. Man.Lbr 880,00 0 2,900,00 0 12/31/201 7 45,00 0 Dir. Matls. 630,00 0 12/31/201 7 290,00 0 OH Alloc. […]

978-0134475585 Chapter 5 Solution 1

CHAPTER 5 ACTIVITY-BASED COSTING AND ACTIVITY-BASED MANAGEMENT 5-1 What is broad averaging, and what consequences can it have on costs? Broad averaging (or “peanut-butter costing”) describes a costing approach that uses broad 5-2 Why should managers worry about product overcosting […]

978-0134475585 Chapter 5 Solution 2

SOLUTION (20 min.) Plantwide, department, and ABC indirect cost rates. 1. Actual plantwide variable MOH rate based on machine hours, $280,000 ¸ 5,000 $56 per machine hour Southern Motors Caesar Motors Jupiter Auto Total Variable manufacturing overhead, allocated based on […]

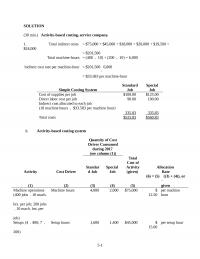

978-0134475585 Chapter 5 Solution 3

SOLUTION (30 min.) Activity-based costing, service company. 1. Total indirect costs = $75,000 + $45,000 + $18,000 + $20,000 + $19,500 + $24,000 Simple Costing System Standard Job Special Job Cost of supplies per job $100.00 $125.00 Direct labor cost […]

978-0134475585 Chapter 5 Solution 4

SOLUTION (50 min.) Activity-based costing. 1. Overhead allocation using a simple job-costing system, where overhead is allocated based on machine hours: Job 220 Job 330 Overhead allocateda$588.60 $1,373.40 a $19.62 per machine-hour × 30 hours; 70 hours 2. Overhead allocation […]

978-0134475585 Chapter 5 Solution 5

SOLUTION (40 min.) ABC, health care. 1a. Medical supplies rate = years-patient ofnumber Total costs supplies Medical = $242,000 110 = space offeet square ofamount Total costs maint. clinic andRent = $138,600 21,000 = $6.60 per square foot = years-patient […]

978-0134475585 Chapter 5 Solution 6

SOLUTION (50 min.) ABC, implementation, ethics. 1. Plum Electronics should not emphasize the Maximum model and should not phase out the Mammoth model. Under activity-based costing, the Maximum model has an operating income percentage of less than 3%, while the […]

978-0134475585 Chapter 6 Solution 1

CHAPTER 6 MASTER BUDGET AND RESPONSIBILITY ACCOUNTING 6-1 What are the four elements of the budgeting cycle? The budgeting cycle includes the following elements: a. Planning the performance of the company as a whole as well as planning the 6-2 […]

978-0134475585 Chapter 6 Solution 2

SOLUTION (30 min.) Revenues and production budget. 1. Selling Price Units Sold Total Revenues 12-ounce bottles $0.30 6,000,000a$1,800,000 2. Budgeted unit sales (12-ounce bottles) 6,000,000 Add target ending finished goods inventory 660,000 Total requirements 6,660,000 Deduct beginning finished goods inventory […]

978-0134475585 Chapter 6 Solution 3

SOLUTION (20–30 min.) Kaizen approach to activity-based budgeting (continuation of 6-30). 1. Budgeted Cost-Driver Rates Activity Cost Hierarchy January February March Ordering Batch-level $45.00 $44.82000a $44.64072b The March 2018 rates can be used to compute the total budgeted cost for […]

978-0134475585 Chapter 6 Solution 4

SOLUTION (40 min.) Budget schedules for a manufacturer. 1a. Revenues Budget Broncos Blankets Rams Blankets Total b. Production Budget in Units Broncos Blankets Rams Blankets Budgeted unit sales 140 195 Add budgeted ending fin. goods inventory 24 29 Total requirements […]

978-0134475585 Chapter 6 Solution 5

SOLUTION (15 min.) Responsibility of purchasing agent. The cost of the biscuits is usually the responsibility of the purchasing agent, and usually controllable by the Central Warehouse. However, in this scenario, Betty the cook has taken the Paula should not […]

978-0134475585 Chapter 6 Solution 6

4. Schedule 4: Direct Manufacturing Labor Budget for January 2018 Labor Category Cost Driver Units DML Hours per Driver Unit Total Hours Wage Rate Total 5. Schedule 5: Manufacturing Overhead Budget for January 2018 At Budgeted Level of 13,000 Direct […]

978-0134475585 Chapter 6 Solution 8

SOLUTION (60 min.) Comprehensive budgeting problem; activity-based costing, operating and financial budgets. 1a. Revenues Budget For the Month of June, 2018 Units Selling Price Total Revenues Regular 2,000 $120 $240,000 b. Production Budget For the Month of June, 2018 Product […]

978-0134475585 Chapter 7 Solution 1

CHAPTER 7 FLEXIBLE BUDGETS, DIRECT-COST VARIANCES, AND MANAGEMENT CONTROL 7-1 What is the relationship between management by exception and variance analysis? Management by exception is the practice of concentrating on areas not operating as expected and 7-2 What are two […]

978-0134475585 Chapter 7 Solution 2

SOLUTION (25–30 min.) Flexible-budget preparation and analysis. 1. Variance Analysis for Bank Management Printers for September 2017 Level 1 Analysis Actual Results (1) Static-Budget Variances (2) = (1) – (3) Static Budget (3) Units sold 12 ,000 3 ,000 U […]

978-0134475585 Chapter 7 Solution 3

SOLUTION (30 min.) Price and efficiency variances, journal entries. 1. Direct materials and direct manufacturing labor are analyzed in turn: Actual Costs Incurred (Actual Input Qty. × Actual Price) Actual Input Qty. × Budgeted Price Flexible Budget (Budgeted Input Qty. […]

978-0134475585 Chapter 7 Solution 4

SOLUTION (45 min.) Static and flexible budgets, service sector. 1. Static Budget Revenue (8,200 × 0.8% × $145,000) $9,512,000 Variable costs: Professional labor (8 × $45 × 8,200) 2,952,000 2. Actual results for third quarter 2017: Revenue (10,250 × 0.8% […]

978-0134475585 Chapter 7 Solution 5

SOLUTION (60 min.) Comprehensive variance analysis review Actual Results Units sold (90% × 700,000) 630,000 Selling price per unit $8.20 Direct materials purchased and used: Direct materials per unit $3.90 Total direct materials cost (630,000 × $3.90) $2,457,000 Direct manufacturing […]

978-0134475585 Chapter 7 Solution 6

SOLUTION (20–30 min.) Direct materials and manufacturing labor variances, solving unknowns. All given items are designated by an asterisk. Actual Costs Incurred (Actual Input Qty. × Actual Price) Actual Input Qty. × Budgeted Price Flexible Budget (Budgeted Input Qty. Allowed […]

978-0134475585 Chapter 7 Solution 7

SOLUTION (30 min.) Direct-cost and selling price variances. 1. Computing unit selling prices and unit costs of inputs: Actual selling price = $3,626,700 ÷ 462,000 2., 3., and 4. The actual and budgeted unit costs are: Actual Budgeted Direct materials […]

978-0134475585 Chapter 8 Solution 2

SOLUTION (30 min.) Fixed manufacturing overhead variance analysis (continuation of 8-23). 1. Budgeted standard direct manufacturing labor used = 0.02 per baguette Budgeted output = 3,100,000 baguettes Budgeted standard direct manufacturing labor-hours Budgeted fixed manufacturing overhead costs = 62,000 × […]

978-0134475585 Chapter 8 Solution 3

SOLUTION (20 min.) Activity-based costing, batch-level variance analysis 1. Static budget number of crates = Budgeted pairs shipped / Budgeted pairs per crate 2. Flexible budget number of crates = Actual pairs shipped / Budgeted pairs per crate = 180,000/15 […]

978-0134475585 Chapter 8 Solution 4

SOLUTION (20 min.) Overhead variances, service setting. 1. and 2. Variable and Fixed Technology Overhead Variance Analysis for Carlyle Capital Company for the first quarter of 2017 Actual Costs Incurred Actual Input Qty. Budgeted Rate Flexible Budget: Budgeted Input […]

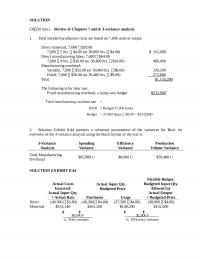

978-0134475585 Chapter 8 Solution 5

SOLUTION (3050 min.) Review of Chapters 7 and 8, 3-variance analysis. 1. Total standard production costs are based on 7,600 units of output. Direct materials, 7,600 $20.00 Direct manufacturing labor, 7,600 $64.00 7,600 4 hrs. $16.00 […]

978-0134475585 Chapter 8 Solution 6

SOLUTION (3040 min.) Straightforward coverage of manufacturing overhead, standard-costing system. 1. Solution Exhibit 8-28 shows the computations. Summary details are: Actual Flexible Budget Output units 66,500 66,500 Allocation base (machine-hours) 75,700 79,800a Allocation base per output unit 1.14b1.2 An overview […]

978-0134475585 Chapter 8 Solution 7

SOLUTION EXHIBIT 8-36 Variable Manufacturing Overhead Actual Costs Incurred (1) Actual Input Qty. × Budgeted Rate (2) Flexible Budget: Budgeted Input Qty. Allowed for Actual Output × Budgeted Rate (3) Allocated: Budgeted Input Qty. Allowed for Actual Output × Budgeted […]

978-0134475585 Chapter 9 Solution 1

CHAPTER 9 INVENTORY COSTING AND CAPACITY ANALYSIS 9-1 Differences in operating income between variable costing and absorption costing are due solely to accounting for fixed costs. Do you agree? Explain. 9-2 Why is the term direct costing a misnomer? The […]

978-0134475585 Chapter 9 Solution 2

SOLUTION (20 min.) Throughput costing (continuation of Exercise 9-21). 1. April 2017 May 2017 Direct material cost of goods sold Beginning inventory Direct materials in goods manufacturedb $ 0 3 ,350,000 $1,005,000 2 ,680,000 Cost of goods available for sale […]

978-0134475585 Chapter 9 Solution 3

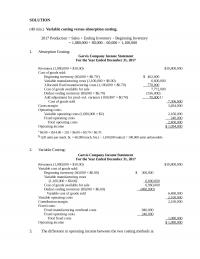

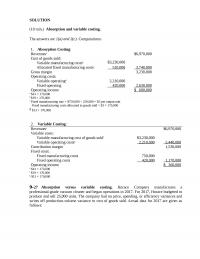

SOLUTION (40 min.) Variable costing versus absorption costing. 2017 Production = Sales + Ending Inventory – Beginning Inventory 1. Absorption Costing: Garvis Company Income Statement For the Year Ended December 31, 2017 Revenues (1,080,000 × $10.00) $10,800,000 Cost of goods […]

978-0134475585 Chapter 9 Solution 4

SOLUTION (10 min.) Absorption and variable costing. The answers are 1(a) and 2(c). Computations: 1. Absorption Costing: Revenuesa Cost of goods sold: $6,970,000 Operating costs: Variable operatingd Fixed operating Operating income 2,210,000 420 ,000 2 ,630,000 $ 600 ,000 a […]

978-0134475585 Chapter 9 Solution 5

SOLUTION (25 min.) Cost allocation, downward demand spiral. SOLUTION EXHIBIT 9-45 2017 Master Budget (1) Practical Capacity (2) 2018 Master Budget (3) Budgeted fixed cost per meal Budgeted fixed costs ¸ Denominator level ($1,533,000 1,050,000; $1,533,000 1,460,000; ¸ ¸ $1,533,000 […]

978-0134475585 Chapter 9 Solution 6

SOLUTION (60 min.) Variable and absorption costing and breakeven points 1. 2017 Variable-Costing Based Operating Income Statement Revenues (1,300 boards ´ $800 per board) Variable costs: Beginning inventory (240 boards ´ $375 per board) $ 90,000 Variable manufacturing costs (1,200 […]

978-0134475585 Chapter 9 Solution 7

SOLUTION (30–35 min.) Comparison of variable costing and absorption costing. 1. Since production volume variance is unfavorable, the budgeted fixed manufacturing overhead must be larger than the fixed manufacturing overhead allocated. = – 2. The problem provides the beginning and […]

AC 21542

The amount of productive capacity available over and above the productive capacity employed to meet customer demand in the current period is the unused capacity. The constant gross-margin percentage NRV method makes the simplifying assumption of treating the joint products […]

AC 22984

Woodruff Flowering Plants provides the following information for the month of May: What is the budgeted contribution margin per composite unit for the actual mix? (Round any intermediary calculations two decimal places.) A) $21.22 B) $21.00 C) $20.50 D) $20.20 […]

AC 39703

Manufacturing Cycle Efficiency (MCE) = Value-added Manufacturing Time divided by Manufacturing Cycle Time. Practical capacity is the level of capacity that reduces theoretical capacity by considering unavoidable operating interruptions, such as scheduled maintenance time and shutdowns for holidays. TRUE Using […]

AC 45343

Decisions regarding sources of long-term financing are best made at subunit level as the subunit has local knowledge and can leverage it in negotiations. Managers track the costs incurred in each value-chain category is to reduce costs and to improve […]

AC 51172

All of the following are factors affecting direct versus indirect cost classification except: A) materiality of the cost B) cost accuracy C) information technology’s ability to trace costs in an economically feasible way D) design of operations Which of the […]

AC 53784

A flexible-budget variance pertaining to revenues is often called a sales-volume variance. Simple regression analysis estimates the relationship between the dependent variable and one independent variable. TRUE A budget is a qualitative expression of a plan. FALSE Explanation: Explanation: A […]

AC 65013

Which of the following are true regarding long-run pricing decisions? A) they result in maximizing return on investment B) they include adjusting product mix in a competitive environment C) the price needs to be sufficient enough to break-even D) use […]

AC 69410

The following information pertains to the Ruby Corp: What is cost of goods sold? A) $1,210,000 B) $1,165,000 C) $1,157,000 D) $1,239,000 The variable overhead flexible-budget variance can be further explained by calculating the: A) price variance and the efficiency […]

AC 87139

Majestic Corporation manufactures wheel barrows and uses budgeted machine hours to allocate variable manufacturing overhead. The following information relates to the company’s manufacturing overhead data: What is the amount of the budgeted variable manufacturing overhead cost per unit? (Do not […]

Acc 10460

Jamal, Kareem, Rashid and Associates are in the process of evaluating its new client services for the business consulting division. ∙ Estate Planning, a new service, incurred $150,000 in development costs and employee training. ∙ The direct costs of providing […]

ACC 10958

Real Wood Structures Company has invested $1,040,000 in a plant to build small tool sheds. The target operating income desired from the plant is $156,000 annually. The company plans annual sales of 1200 sheds at a selling price of $1100 […]

Acc 29889

Costs of activities related to a group of units sold to a customer is termed as customer batch-level costs. All costs other than direct materials and direct manufacturing labor are classified as indirect costs. TRUE Strategy describes how an organization […]

Acc 31190

Henry Chapman Manufacturing Inc. incurred the following expenses during 2017: What will be the breakeven point in units if absorption costing is used? (Round your final answer up to the next whole unit.) A) 997 units B) 934 units C) […]

ACC 36738

Intrinsic motivation comes from being given greater responsibility, doing interesting and creative work, and having pride in doing that work. Successful implementation of a JIT production system and effective accomplishments of its goals should result in a decrease in the […]

Acc 39048

Shiffon Electronics manufactures music player. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department, the Programming department, and the Testing Department. Direct materials are added at the beginning of […]

ACC 43217

Timekeeper Inc. manufactures clocks on a highly automated assembly line. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department and the Testing Department. Direct materials are added at the […]

ACC 44547

Expert Manufacturing reported the following: What is Expert’s operating income? A) $346,400 B) $218,200 C) $204,200 D) $200,200 Which of the following is another term for required rate of return? A) hurdle rate B) total cost rate C) variance rate […]

Acc 57235

In the banking industry, depositing a customer’s check into the wrong bank account is an example of quality of design failure. With disregard to all other factors, the use of high-quality raw materials is likely to result in a favorable […]

ACC 59797

The fundamental cost objects of ABC are ________. A) activities B) cost drivers C) products D) services Which of the following is a direct manufacturing cost? A) plant maintenance B) plant rent C) fringe benefits paid to machine operators D) […]

ACC 62575

Units spoiled due to machine breakdowns and operator errors are normal spoilage. The two broad strategies that companies follow are cost leadership strategy and product differentiation strategy. TRUE U.S. tax reporting requires end-of-period reconciliation between actual and applied indirect costs […]

Acc 65827

The Big Tool Company has budgeted sales of $300,000 with the following budgeted costs: Compute the average markup percentage for setting prices as a percentage of: a. The full cost of the product b. The variable cost of the product […]

Acc 66416

ABC systems help managers to ________. A) value ending inventory more accurately B) identify new designs to reduce costs C) evaluate direct material costs more efficiently D) improve the inventory turnaround time In a perfectly competitive market, which of the […]

Acc 72699

Advocates of throughput costing argue that ________. A) fixed manufacturing costs must be included as inventoriable costs and provide less incentive than absorption costing to build-up inventory to increase profits B) direct manufacturing labor is relatively fixed and therefore should […]

ACC 73567

In the graph method of CVP analysis, the horizontal line above the x-axis represents the total cost line. The key to a company’s success is always to be the low cost producer in a particular industry. FALSE Explanation: The low […]

ACC 90369

The accuracy of the completion estimate of conversion costs depends on the care, skill, and experience of the estimator and also the nature of the conversion process. The degree of operating leverage at a specific level of sales helps the […]

Acc 92649

The accrual accounting rate-of-return method has a significant weakness for use in making capital budgeting decisions because it does NOT track cash flows and it ignores the time value of money. Under the proration approach, the sum of the amounts […]

ACC 95808

First Class, Inc., expects to sell 26,000 pool cues for $14 each. Direct materials costs are $2, direct manufacturing labor is $4, and manufacturing overhead is $0.89 per pool cue. The following inventory levels apply to 2019: On the 2019 […]

Accounting 15717

Springer Products manufactures three different product lines, Model X, Model Y, and Model Z. Considerable market demand exists for all models. The following per unit data apply: Model X Model Y Model Z Selling price $55 $69 $78 Direct materials […]

Accounting 37258

In a job-costing system the cost object is an individual unit, batch, or lot of a distinct product or service. Fluctuations in exchange rates between different countries’ currencies affect costs and pricing decisions of a company. TRUE In each period, […]

Accounting 43659

Carriage Incorporated manufactures horse carriages. The company has two divisions, Wheels and Assembly. Because of different accounting methods and inflation rates, the company is considering multiple evaluation measures. The following information is provided for 2018: ASSETS INCOME The company is […]

Accounting 45249

A locked-in cost is a(n) ________. A) opportunity cost that is fixed in the short run B) cost that can be changed in the short run C) cost that has not yet been incurred, but based on decisions that have […]

Accounting 51924

Which of the following is a measure of the balanced scorecard’s customer perspective? A) Number of client complaints B) Defect rates C) Number of process improvements D) Revenue growth Which of the following is an internal-business-process measure to study the […]

Accounting 54196

The net present value of all cash flows over the life of an investment equals the net present value of the operating incomes. Absorption costing is the required inventory method for external financial reporting in most countries. TRUE All else […]

Accounting 68745

The benefits of implementing a more-complex cost allocation system are relatively easy to quantify for application of the cost-benefit approach. The sales method for recognizing byproducts is conceptually correct because it is consistent with the matching principle. FALSE Explanation: The […]

Accounting 89456

Price dumping occurs when a domestic company is trying to get rid of out-of-style products at a substantially reduced price. The choice of the capacity level used to allocate budgeted fixed manufacturing costs to products can greatly affect the product-cost […]

Accounting 91573

Companies that overcost products risk becoming less effective on pricing and losing market share when competition utilizes more accurate cost systems. The process of preparing a budget encourages coordination and communication throughout the company. TRUE If variable costs per unit […]

ACCT 25137

Use of practical capacity results in an unrealistically small fixed manufacturing cost per unit because it is based on an idealistic and unattainable level of capacity. To evaluate overall performance, return on investment and residual income measures are more appropriate […]

ACCT 27790

Which of the following statements is true of sell-or-process-further decisions in joint costing? A) Joint costs incurred before the split-off point are relevant in deciding whether to process the product further. B) All separable costs in joint-cost allocations are incremental […]

ACCT 38931

Deducting depreciation from operating cash flows would result in counting the initial investment twice in a discounted cash flow analysis. Costs of quality (COQ) reports usually consider opportunity costs. FALSE Explanation: Costs of quality (COQ) reports usually do not consider […]

Acct 40726

Mendel Company makes the following journal entry: Which of the following statements is true of the given journal entry? A) A variable manufacturing overhead cost of $179,000 is written-off. B) An unfavorable spending variance of $57,000 is recorded. C) A […]

ACCT 45577

Which of the following is the correct mathematical expression to calculate the fixed overhead spending variance? A) Static-budget amount — Flexible-budget amount B) Actual costs incurred — Flexible-budget amount C) Static-budget amount — Fixed overhead allocated for actual output D) […]

ACCT 50172

The vertical difference, called the residual term, measures the distance between actual cost of one period and estimated cost of the next period. The theory of constraints is more useful for the long-run management of costs since it takes a […]

Acct 54318

Increasing the capacity of a bottleneck resource increases manufacturing cycle times and delays. Costs of abnormal spoilage are NOT considered to be inventoriable costs and are written off as costs of the accounting period in which the abnormal spoilage is […]

ACCT 56807

An unfavorable production-volume variance always infers that management made a bad planning decision regarding the plant capacity. The nominal rate of return is made up of a risk-free element when there is no expected inflation, a business-risk element, and an […]

Acct 58045

Which f the following methods focuses on reducing costs during the manufacturing stage? A) Target costing B) Kaizen costing C) Cost-plus pricing D) Life-cycle costing Which of the following is a component of operating budgets? A) production budget B) budgeted […]

Acct 63309

Casey Corporation produces a special line of basketball hoops. Casey Corporation produces the hoops in batches. To manufacture a batch of the basketball hoops, Casey Corporation must set up the machines and molds. Setup costs are batch-level costs because they […]

Acct 66267

Lean accounting is much simpler than traditional product costing because ________. A) it compares value stream costs against costs that include costs of all purchased materials B) it computes the cost of individual products C) calculating actual product costs by […]

ACCT 76730

The breakeven point is the activity level where ________. A) revenues equal fixed costs B) revenues equal variable costs C) contribution margin equals total costs D) revenues equal the sum of variable and fixed costs Which of the following represents […]

ACCT 76801

Springer Products manufactures three different product lines, Model X, Model Y, and Model Z. Considerable market demand exists for all models. The following per unit data apply: Model X Model Y Model Z Selling price $50 $66 $80 Direct materials […]

Acct 81726

In relevant-cost analysis, managers should not consider all variable as relevant and all fixed costs as irrelevant. For short-run product-mix decisions, managers should focus on minimizing total fixed costs. FALSE Explanation: For short-run product mix decisions, managers should focus on […]

Acct 89057

A local accounting firm employs 24 full-time professionals. The budgeted annual compensation per employee is $45,000. The average chargeable time is 420 hours per client annually. All professional labor costs are included in a single direct-cost category and are allocated […]

Acct 90214

Joint costs are incurred beyond the split-off point and are assignable to individual products. IMA’s overarching ethical principles include: Honesty, Fairness, Objectivity, and Responsibility. TRUE The constant gross-margin percentage NRV method is the only method of allocating joint costs under […]

ACCT 90663

Wilde Corporation budgeted the following costs for the production of its one and only product for the next fiscal year: Wilde has an annual target operating income of $920,000. The markup percentage for setting prices as a percentage of variable […]

ACCT 93655

A responsibility center is a part, segment, or subunit of an organization whose manager is accountable for a specified set of activities. Negotiated transfer prices are often employed when market prices are stable. FALSE Explanation: Negotiated transfer prices are often […]

Acct 96269

Following a strategy of product differentiation, Izzy’s Limited Company makes a high-end Appliance, XT15. Izzy’s Limited presents the following data for the years 2017 and 2018: Izzy’s Limited produces no defective units but it wants to reduce direct materials usage […]

ACCT 97511

Which of the following statements is true of an abnormal spoilage? A) It is a spoilage which is inherent in a particular production process. B) It arises even when the process is carried out in an efficient manner. C) It […]

Acct 97872

Feedback regarding previous actions may affect ________. A) future predictions B) implementation of the decision C) the decision model D) All of these answers are correct. The preparation of all the budgets in the master budget forces managers to think […]

ACT 27626

Chief Manufacturing is a small textile manufacturer using machine-hours as the single indirect-cost rate to allocate manufacturing overhead costs to the various jobs contracted during the year. The following estimates are provided for the coming year for the company and […]

ACT 40714

If a company is planning to reduce the selling price, they must believe that ________. A) variable costs will decline as well B) the fixed costs will cover the lower sales price C) more units will be sold D) increased […]

ACT 58426

The costs that result when a company runs out of a particular item for which there is a customer demand are ________. A) shrinkage costs B) shortage costs C) stockout costs D) EOQ estimation costs Spoilage, rework, scrap, and machine […]

ACT 67249

Francis Kenney is paid $26 an hour for straight-time and $31 an hour for overtime. One week she worked 46 hours, which included 6 hours of overtime. What is the overtime premium incurred to the company? A) $186 B) $72 […]

ACT 70959

After conducting a market research study, Magnificent Manufacturing decided to produce a new interior door to complement its exterior door line. It is estimated that the new interior door can be sold at a target price of $240. The annual […]

ACT 72881

In cost allocation, R&D costs are used to ________. A) provide information for economic decisions B) report to external parties when using generally accepted accounting principles C) calculate costs of a government contract D) calculate prime cost of a product […]

ACT 76629

Discontinuing an unprofitable customer should be solely done on the basis of profitability. If the production planners set the budgeted machine hours standards too loose, one could anticipate there would be a favorable fixed overhead efficiency variance. FALSE Explanation: There […]

ACT 82896

In comparing the three basic approaches to transfer pricing, which of the following statements would be true? A) A cost-based approach preserves subunit autonomy while negotiated transfer prices do not. B) Market-based transfer pricing motivates managers but negotiated prices do […]

ACT 90515

Which of the following true of nonfinancial measures of quality? A) They direct attention to financial processes that help managers identify the precise problem areas that need improvement. B) They focus managers’ attention on how poor quality affects operating income. […]

ACT 95601

Activity based costing system differs from traditional costing systems in the treatment of ________. A) direct labor costs B) direct material costs C) prime costs D) indirect costs Budgeted production equals ________. A) beginning finished goods inventory + budgeted unit […]

Chapter 6 Tyva Makes A Very Popular Undyed

11. Nonmanufacturing Costs Budget For the Year Ending December 31, 2018 Variable Fixed Total Marketing $21,150 $90,000 $111,150 12. Budgeted Income Statement For the Year Ending December 31, 2018 Revenue $528,000 Cost of goods sold 396,240 Gross margin 131,760 Operating […]

Chapter 8 How Do Managers Plan For Variable Overhead Costs

CHAPTER 8 FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND MANAGEMENT CONTROL 8-1 How do managers plan for variable overhead costs? Effective planning of variable overhead costs involves: 1. Planning to undertake only those variable overhead activities that add value for 8-2 […]

MET MG 26088

Under the cause and effect criterion, reasonableness is a matter of judgment rather than an operational criterion. If the sales mix shifts toward the lower-contribution-margin product, the breakeven quantity will decrease. FALSE Explanation: If the sales mix shifts toward the […]

MET MG 30065

Timekeeper Inc. manufactures clocks on a highly automated assembly line. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department and the Testing Department. Direct materials are added at the […]

MET MG 33409

A direct cost of one cost object cannot be an indirect cost of another cost object. The net realizable value (NRV) method allocates joint costs to joint products produced during the accounting period on the basis of their relative NRV—final […]

MET MG 58679

Process-costing systems using standard costs record standard direct material costs in Direct Materials Control and standard conversion costs in Conversion Costs Control. Joint costs are the costs of a production process that yields multiple products simultaneously. TRUE In the “obtain […]

MET MG 83182

Differential revenue is the difference in total revenue between two alternatives. Costs in beginning inventory are pooled with costs in the current period when determining the costs of good units under the weighted-average method of process costing. TRUE If the […]

MET MG 99895

Which of the following statements is true of contribution-margin format of the income statement? A) It is used for absorption costing. B) It distinguishes between variable and fixed costs in its format. C) It distinguishes manufacturing costs from nonmanufacturing costs. […]

SMG AC 19219

Additional insight can be gained by dividing the sales-volume variance into the sales-mix variance and the sales-quantity variance. Higher selling prices, rather than unique products or services, provide a competitive advantage for the cost leader companies. FALSE Explanation: Lower selling […]

SMG AC 27253

Greentree Incorporated manufactures rustic furniture. The cost accounting system estimates manufacturing costs to be $120 per table, consisting of 60% variable costs and 40% fixed costs. The company has surplus capacity available. It is Greentree’s policy to add a 30% […]

SMG AC 34885

A cost is a resource sacrificed or forgone to achieve a specific objective. Continuous improvement through the use of standard costs is the process of repeatedly identifying the causes of variances, taking corrective actions, and evaluating results. TRUE The tariffs […]

SMG AC 43269

For short-run product-mix decisions, maximizing contribution margin will also result in maximizing operating income. A “push-through” system, often described as a materials requirement planning system, focuses first on the forecasted amount and timing of finished goods and then determines the […]

SMG AC 70520

The top management at Amore Corp, a manufacturer of computer games, is attempting to recover from a flood that destroyed some of their accounting records. The main computer system was also severely damaged. The following information was salvaged: What were […]

SMG AC 79305

Prorated allocation of production-volume variance has the effect of approximating the allocation of fixed costs based on actual costs and actual output. In calculating the net initial investment cash flows, any increase in working capital required for the project should […]

SMG AC 82536

The weighted-average method merges unit costs from different accounting periods, obscuring period-to-period comparisons. When the dollar amount of scrap is immaterial, the simplest accounting is to record the physical quantity of scrap returned to the storeroom and to regard scrap […]

SMG AC 82835

Which of the following is required to arrive at the budgeted units to be produced in a year? A) estimated direct materials inventory required at the end of the year B) estimated finished goods inventory required at the end of […]