SOLUTION

(20 mins.) Anti-trust laws and pricing.

1. The company is not practicing price discrimination because all customers are being

offered the same prices. The offer is simply restricting the times and locations that the promotion

is available but not the individual customers to whom the promotion applies. The offer of low

2. I agree with this policy. The company is practicing peak load pricing for its flights on

Monday mornings and Friday evenings. These are the times when many business travelers fly.

Many businesses (for example, consulting businesses) require their employees to travel to their

3. As discussed in requirement 1, the company appears not to be in violation of any anti-trust

laws, but they should confirm that again. The penalties for any illegal practices could be high

enough to force an organization into bankruptcy.

Second, the company should consider the ethical implications of its price discounting policy.

Under no circumstances should its low pricing strategies compromise the quality or safety of its

operations in order to earn profits. The company should also consider the negative consequences

The company should also consider the reputational and public relations aspects of its

decision to charge more during peak hours. This may have the effect of some travelers feeling

In any event, the company should consider using value engineering to reduce any non-value

added costs and efficiency of value–added costs to increase profitability of the airline.

13-36 Ethics and pricing. Instyle Interior Designs has been requested to prepare a bid to

decorate four model homes for a new development. Winning the bid would be a big boost for

sales representative Jim Doogan, who works entirely on commission. Sara Groom, the cost

accountant for Instyle, prepares the bid based on the following cost information:

13-1

Based on the company policy of pricing at 120% of full cost, Groom gives Doogan a figure of

$165,600 to submit for the job. Doogan is very concerned. He tells Groom that at that price,

Instyle has no chance of winning the job. He confides in her that he spent $600 of company

funds to take the developer to a basketball playoff game where the developer disclosed that a bid

of $156,000 would win the job. He hadn’t planned to tell Groom because he was confident that

the bid she developed would be below that amount. Doogan reasons that the $600 he spent will

be wasted if Instyle doesn’t capitalize on this valuable information. In any case, the company

will still make money if it wins the bid at $156,000 because it is higher than the full cost of

$138,000.

Required:

1. Is the $600 spent on the basketball tickets relevant to the bid decision? Why or why not?

2. Groom suggests that if Doogan is willing to use cheaper furniture and artwork, he can

achieve a bid of $156,000. The designs have already been reviewed and accepted and cannot

be changed without additional cost, so the entire amount of reduction in cost will need to

come from furniture and artwork. What is the target cost of furniture and artwork that will

allow Doogan to submit a bid of $156,000 assuming a target markup of 20% of full cost?

3. Evaluate whether Groom’s suggestion to Doogan to use the developer’s tip is unethical.

Would it be unethical for Doogan to reduce the cost of furniture and artwork to arrive at a

lower bid? What steps should Doogan and Groom take to resolve this situation?

SOLUTION

(20 min.) Ethics and pricing.

1. The $600 spent on the basketball tickets is a sunk (past) cost and is, therefore, irrelevant to

2. If the target price is $156,000 and the markup is 20% of full cost, the target full cost is

3. It was unethical for Doogan to use the basketball tickets to get the tip out of the developer.

Knowing about Doogan’s action and suggesting a way to use it is unethical on the part of Groom.

13-2

In assessing the situation, the specific “Standards of Ethical Conduct for Management

Accountants,” described in Chapter 1 that the management accountant should consider are listed

below.

Integrity

The management accountant has a responsibility to avoid actual or apparent conflicts of interest

Credibility

The Standards of Ethical Conduct for Management Accountants require that information should

be fairly and objectively communicated and that all relevant information should be disclosed.

13-37 Value engineering, target pricing, and locked-in costs. Sylvan Creations designs,

manufactures, and sells modern wood sculptures. Sandra Johnson is an artist for the company.

Johnson has spent much of the past month working on the design of an intricate abstract piece.

Jim Chase, product development manager, likes the design. However, he wants to make sure that

the sculpture can be priced competitively. Ellen Cooper, Sylvan’s cost accountant, presents

Chase with the following cost data for the expected production of 75 sculptures:

Design cost $10,000

Direct materials 80,000

Direct manufacturing labor 27,500

Variable manufacturing overhead 10,000

Fixed manufacturing overhead 42,500

Fixed marketing costs 17,500

Required:

1. Chase thinks that Sylvan Creations can successfully market each piece for $3,000. To earn

the required return on capital, the company’s target operating income per unit is 20% of

target price. Calculate the target full cost per unit of producing the 75 sculptures. Does the

cost estimate Cooper developed meet Sylvan’s requirements? Is value engineering needed?

What is the total target operating income for the 75 sculptures?

2. Chase believes that competition will require Sylvan to reduce the price of the sculpture to

$2,800. Rather than using the highest-grade wood available, Sylvan could use standard grade

wood and lower the cost of direct materials by 25%. This redesign will require an additional

$1,500 of design cost. Will this design change allow Sylvan to earn its total target operating

income on the 75 sculptures? Is the cost of wood a locked-in cost?

13-3

3. If the price of the sculpture is $2,800, what is the total amount Sylvan can spend on direct

materials for the 75 sculptures to earn the total target operating income calculated in

requirement 1. What is the target cost per sculpture?

4. What challenges might managers at Sylvan Creations encounter in achieving the target cost

and how might they overcome these challenges?

SOLUTION

(25–30 min.) Value engineering, target pricing, and locked-in costs.

1.

Design cost $ 10,000

Direct materials 80,000

Direct manufacturing labor 27,500

The cost estimate developed by Cooper does not meet Sylvan Creations’ requirements. Value

engineering will be needed to reduce the cost per unit from $2,500 per unit to the target cost of

$2,400 per unit.

2

Total costs (requirement 1) $187,500

Less: Reduction in material costs ($80,000 × 25%) (20,000)

Students will debate whether the revised design achieves the target cost. The correct answer

is that it does not. To earn the required rate of return on investment, Sylvan needs to earn a target

13-4

operating income of $45,000 on these sculptures. This happens to be 20% of revenues of

To earn the required return on investment, Sylvan would still need to earn $45,000. It will

only earn $41,000 with the new design and so not achieve the target operating income needed to

earn the required return on investment. Some students may calculate the revised cost per unit of

The cost of materials is a locked-in cost once the design is finalized. The chosen design locks

in what the materials costs will be once manufacturing starts. Value engineering will be needed

to reduce the current cost to the target cost.

3.

New total target cost ($210,000 − $45,000) $165,000

5. The challenges that Sylvan Creations might encounter in achieving the target cost are

mostly employee related. If the employees resist the changes, or struggle with the

Sylvan Creations would also need to think about the customer and whether reducing

Try It 13-1 Solution

Gonzalo’s operating income in 2016 is as follows:

13-5

Total for

250,000 Packs

(1)

Per Unit

(2) = (1) ÷ 250,000

Revenues ($8 250,000)

Purchase cost of Packs ($6 250,000)

$2 ,000,000

1,500,000

$8.00

6.00

Try It 13-2 Solution

Price to retailers in 2017 is 95% of 2016 price = 0.95 $8 = $7.60

Cost per pack in 2017 is 96% of 2016 cost = 0.96 $6 = $5.76.

Gonzalo’s operating income in 2017 is as follows:

Total for

250,000 Packs

(1)

Per Unit

(2) = (1) ÷ 250,000

Revenues ($7.60 250,000)

Purchase cost of packs ($5.76 250,000)

$1 ,900,000

1,440,000

$7.60

5.76

Recall from Try It 13-1 that Gonzalo’s operating income in 2016 is $90,000 and target operating

Try It 13-3 Solution

Gonzalo’s operating income in 2017, if it makes changes in ordering and receiving and storage,

will be as follows:

Total for

250,000 Packs

(1)

Per Unit

(2) = (1) ÷ 250,000

Revenues ($7.60 250,000)

Purchase cost of packs ($5.76 250,000)

$1 ,900,000

1,440,000

$7.60

5.76

13-6

Through value engineering that reduces the quantity of the activity and the cost-driver rate,

Gonzalo exceeds its target operating income of $90,000 and $0.36 per pencil pack despite the

fact that its revenue per pencil pack has decreased by $0.40 ($8.00 – $7.60), while its purchase

cost per pencil pack has decreased by only $0.24 ($6.00 – $5.76).

Try It 13-4 Solution

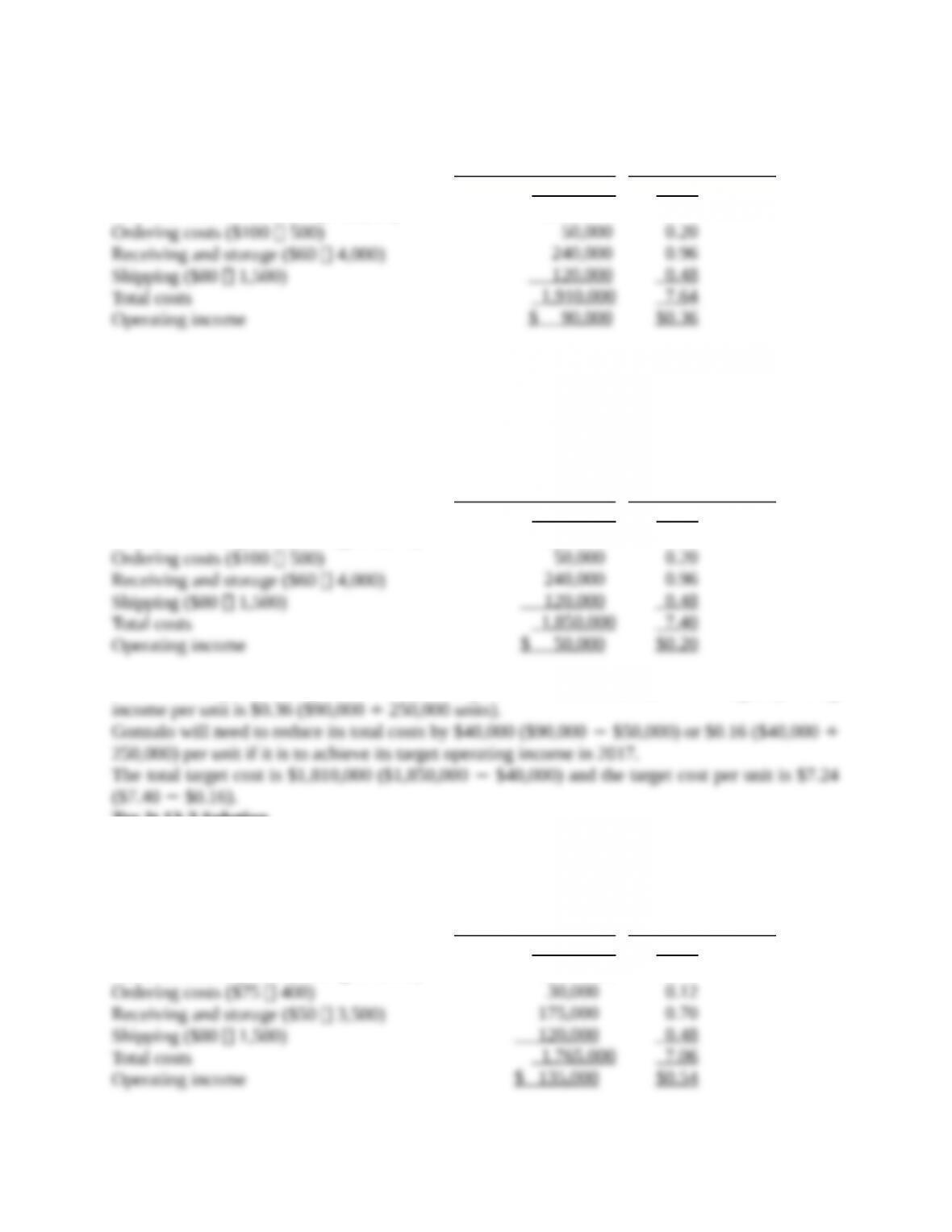

The following table shows the total costs for 250,000 packs and the cost per pack in 2017 using

Ganzalo’s activity-based costing system.

Total for

250,000 Packs

(1)

Per Unit

(2) = (1) ÷ 250,000

Purchase cost of packs ($5.76 250,000)

Ordering costs ($75 400)

$1,440,000

30,000

$5.76

0.12

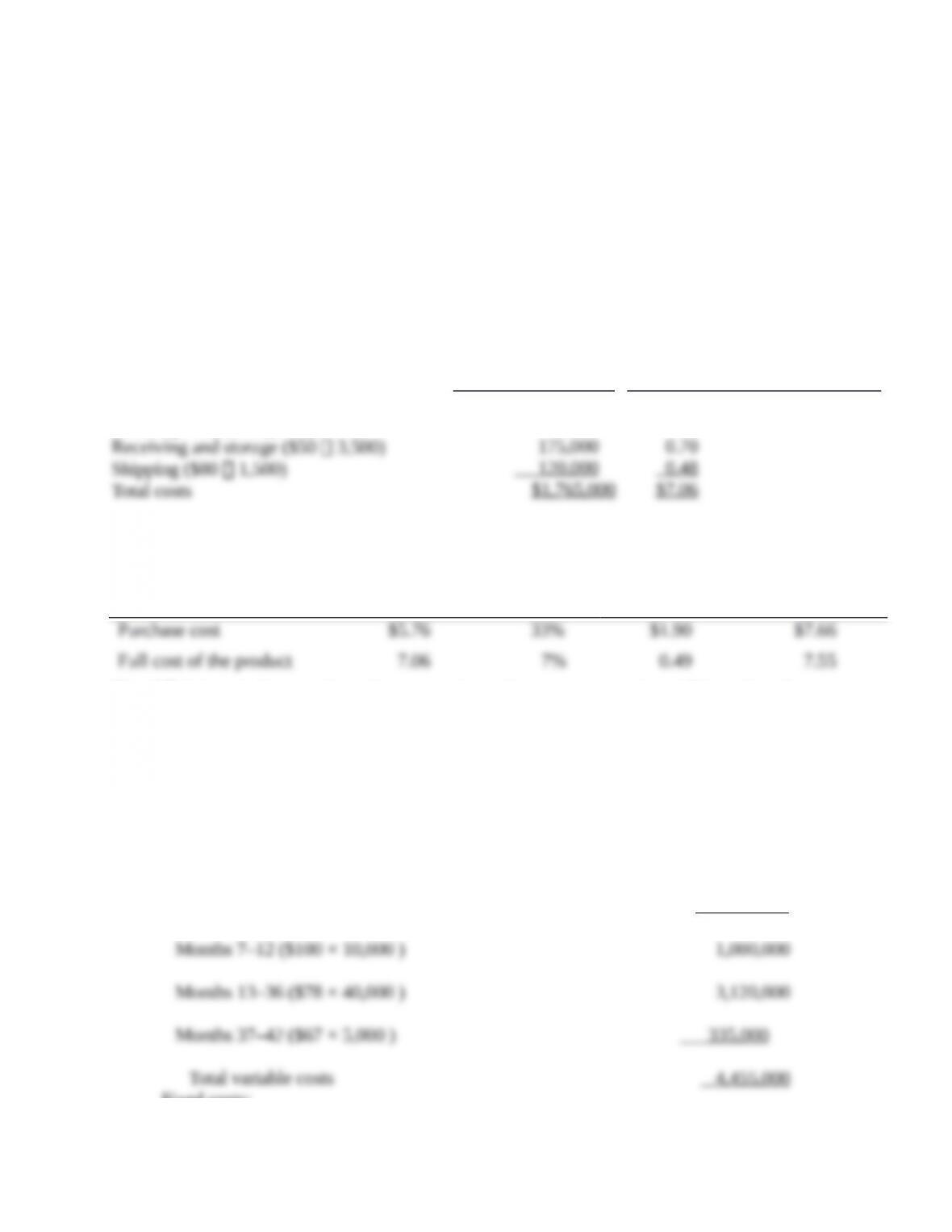

Cost Base

Estimated Cost

per Unit

(1)

Markup

Percentage

(2)

Markup

Component

(3) (1) (2)

Prospective

Selling Price

(4) (1) (3)

The different cost bases and markup percentages give two prospective selling prices that are

close to each other. The final selling price will be adjusted after taking into account customer and

competitor reactions.

Try It 13-5 Solution

1. The following table shows the operating income over the entire life cycle for the new

industrial motor.

Projected Life Cycle Income Statement

Revenues [$375 × (10,000 + 40,000 + 5,000)] $20 ,625,000

Variable costs:

Fixed costs:

13-7

Design costs 500,000

2. The following table shows the operating income over the entire life cycle for the new

industrial motor if Winchester decides to increase the price of the motor from $375 to $425 in the

first 6 months of sales.

Projected Life Cycle Income Statement

Revenues [$425 × 9,500 + $375 × (38,000 + 5,000)] $20 ,162,500

Variable costs:

Fixed costs:

Winchester earns more profit under its original plan ($3,870,000) than it does if it increases the

13-8