SOLUTION

(30 min.) Activity-based costing, service company.

1. Total indirect costs = $75,000 + $45,000 + $18,000 + $20,000 + $19,500 +

$24,000

Simple Costing System

Standard

Job

Special

Job

Cost of supplies per job $100.00 $125.00

1. Activity-based costing system

Quantity of Cost

Driver Consumed

during 2017

(see column (1))

Activity Cost Driver

Standar

d Job

Special

Job

Total

Cost of

Activity

(given)

Allocation

Rate

(1) (2) (3) (4) (5)

(6) = (5) ((3) + (4)), or

given

Machine operations

(400 jobs 10 mach.

Machine hours 4,000 2,000 $75,000 $

12.50

per machine

hour

200)

15.00

5-1

¸

´

´ ´

Total Costs

Standard

Job

Special

Job

Cost of supplies ($100 400; $125 200)

Direct labor costs ($90 400; $100 200)

Indirect costs allocated:

Machine operations ($12.50 per mach. hr. 4,000; 2,000)

Setups ($15 per setup hr. 1,600; 1,400)

Purchase orders ($20 per order 400; 500)

Marketing (0.05 $240,000; 0.05 $150,000)

Administration (0.42857 $36,000; $20,000)

Cost of each job ($189,429 400; $133,071 200)

3.

Cost per job

Standard

Job

Special

Job

Simple Costing System $525.83 $560.83

Relative to the ABC system, the simple costing system overcosts standard jobs and undercosts

special jobs. Both types of jobs need 10 machine hours per job, so in the simple system, they are

5-2

´ ´

´ ´

´

´

´

´ ´

´

¸ ¸

4. Speediprint can use the information revealed by the ABC system to change its pricing

based on the ABC costs. Under the simple system, Speediprint was making a gross margin of

12% on each standard job ([$600 – $525.83] $600) and 25% on each special job ([$750 –

Speediprint can also use the ABC information to improve its own operations. It could

examine each of the indirect cost categories and analyze whether it would be possible to deliver

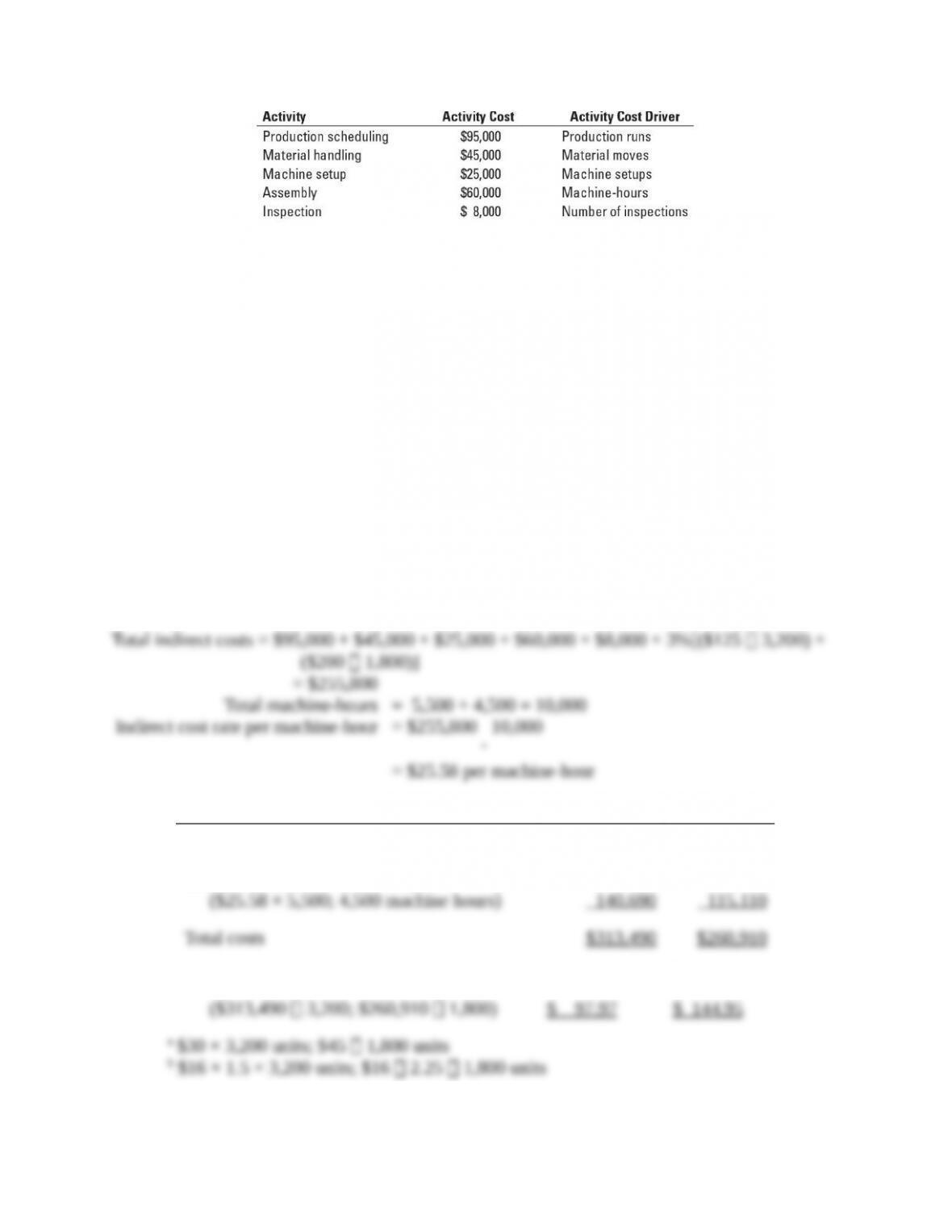

5-26 Activity-based costing, manufacturing. Decorative Doors, Inc., produces two types of

doors, interior and exterior. The company’s simple costing system has two direct-cost categories

(materials and labor) and one indirect-cost pool. The simple costing system allocates indirect

costs on the basis of machine-hours. Recently, the owners of Decorative Doors have been

concerned about a decline in the market share for their interior doors, usually their biggest seller.

Information related to Decorative Doors production for the most recent year follows:

The owners have heard of other companies in the industry that are now using an activity-based

costing system and are curious how an ABC system would affect their product costing decisions.

After analyzing the indirect-cost pool for Decorative Doors, the owners identify six activities as

generating indirect costs: production scheduling, material handling, machine setup, assembly,

inspection, and marketing. Decorative Doors collected the following data related to the

indirect-cost activities:

5-3

¸

Marketing costs were determined to be 3% of the sales revenue for each type of door.

Required

1. Calculate the cost of an interior door and an exterior door under the existing simple costing

system.

2. Calculate the cost of an interior door and an exterior door under an activity-based costing

system.

3. Compare the costs of the doors in requirements 1 and 2. Why do the simple and

activity-based costing systems differ in the cost of an interior door and an exterior door?

4. How might Decorative Doors, Inc., use the new cost information from its activity-based

costing system to address the declining market share for interior doors?

SOLUTION

(30 min.) Activity-based costing, manufacturing.

1. Simple costing system:

Simple Costing System Interior Exterior

Direct materialsa$ 96,000 $ 81,000

Direct manufacturing laborb 76,800 64,800

Indirect cost allocated to each job

Total cost per unit

5-4

2. Activity-based costing system

Activity

(1)

Total

Cost of

Activity

(2)

Cost Driver

(3)

Cost

Driver

Quantity

(4)

Allocation Rate

(5) = (2) (4)

Product

scheduling $95,000 Production runs 125c$760.00

per production

run

ABC System Interior Exterior

Direct materials $ 96,000 $ 81,000

Direct manufacturing labor 76,800 64,800

Indirect costs allocated:

´

´

´

´

´

Total cost per unit

3.

Cost per unit Interior Exterior

Simple Costing System $97.97 $144.95

5-5

4. Decorative Doors, Inc. can use the information revealed by the ABC system to change its

pricing based on the ABC costs. Under the simple system, Decorative Doors was making an

operating margin of 21.6% on each interior door ([$125 – $97.97]

¸

$125) and 27.5% on each

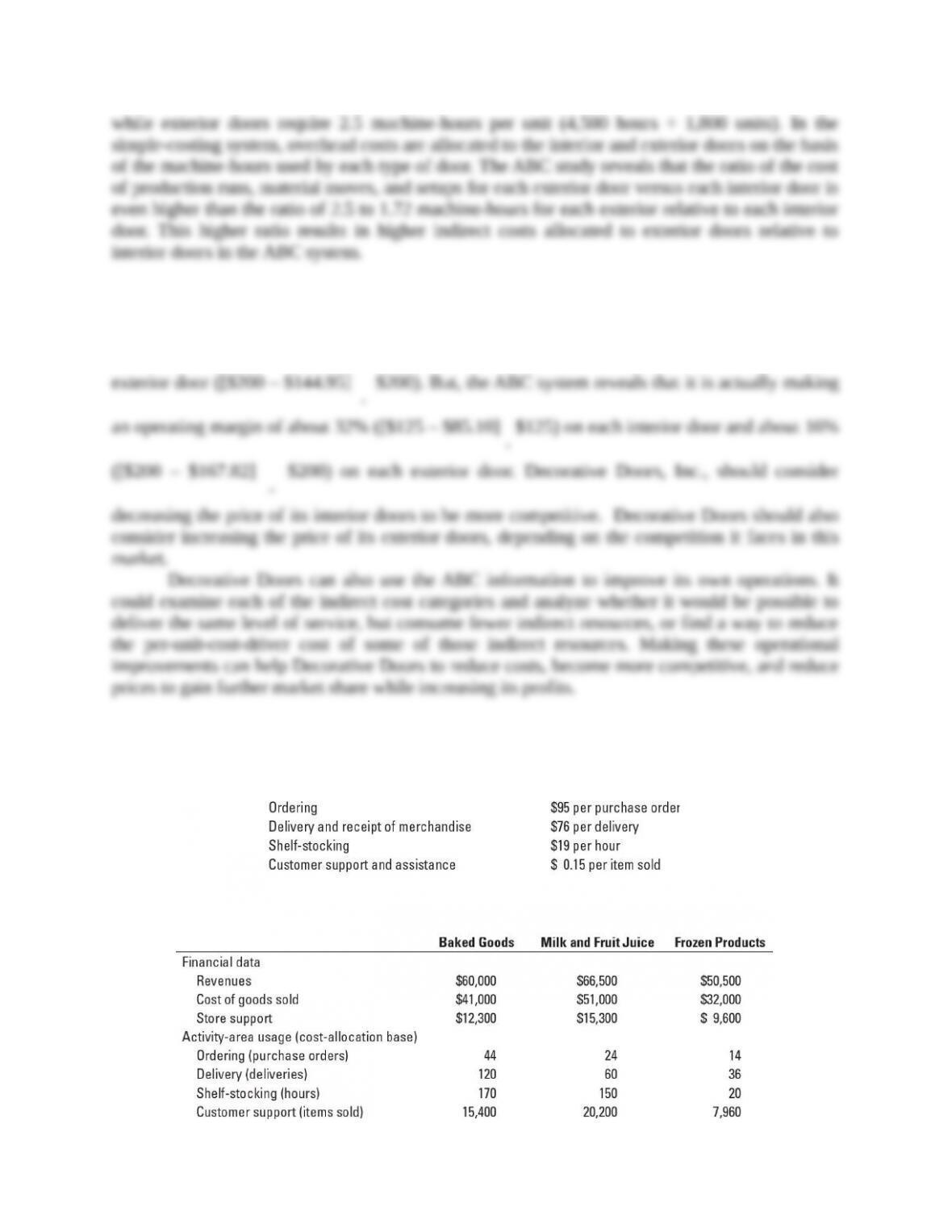

5-27 ABC, retail product-line profitability. Fitzgerald Supermarkets (FS) operates at capacity

and decides to apply ABC analysis to three product lines: baked goods, milk and fruit juice, and

frozen foods. It identifies four activities and their activity cost rates as follows:

The revenues, cost of goods sold, store support costs, activities that account for the store support

costs, and activity-area usage of the three product lines are as follows:

5-6

Under its simple costing system, FS allocated support costs to products at the rate of 30% of cost

of goods sold.

Required

1. Use the simple costing system to prepare a product-line profitability report for FS.

2. Use the ABC system to prepare a product-line profitability report for FS.

3. What new insights does the ABC system in requirement 2 provide to FS managers?

SOLUTION

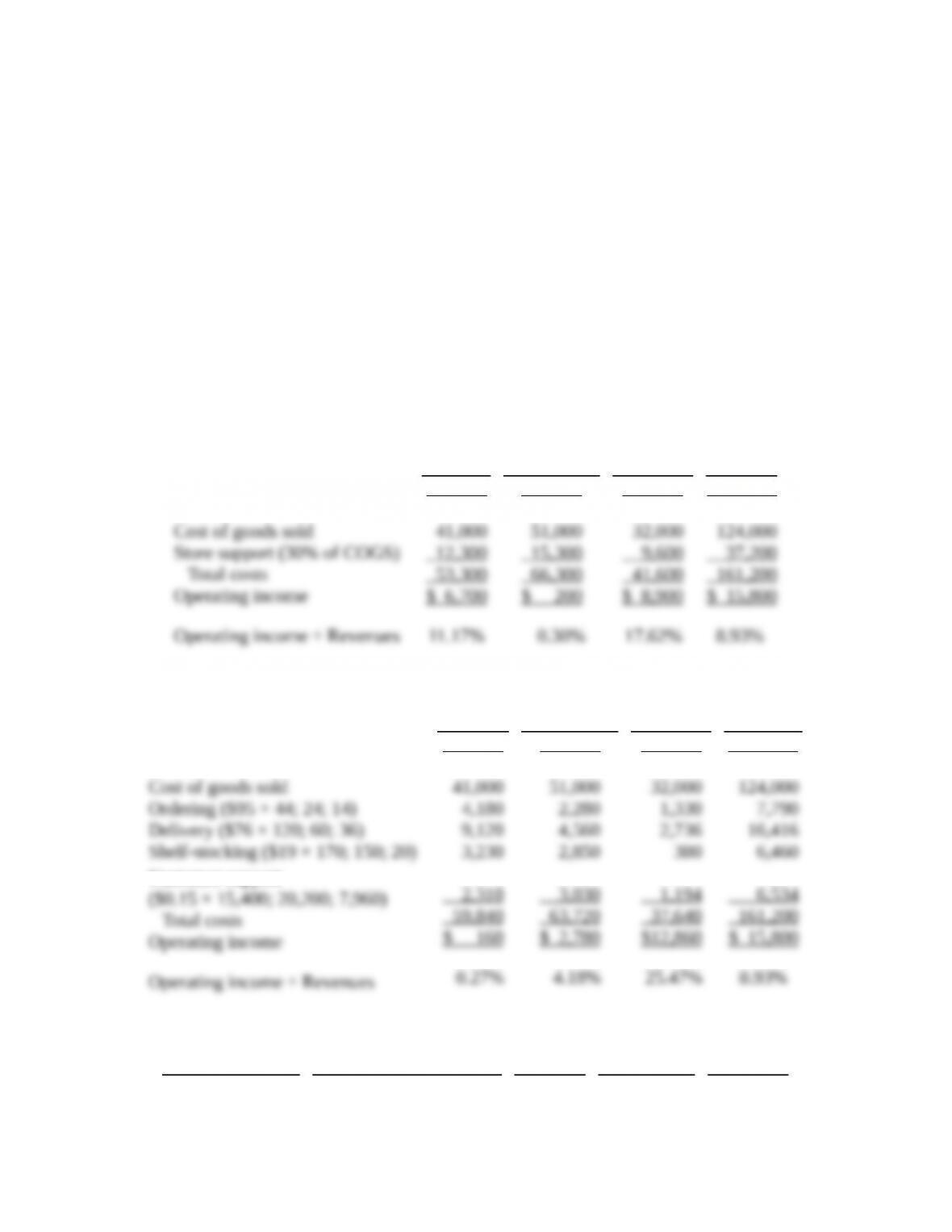

(30 min.) ABC, retail product-line profitability.

1. The simple costing system (Panel A of Solution Exhibit 5-27) reports the following:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products Total

Revenues

Costs

$60,000

$66,500

$50,500

$177,000

2. The ABC system (Panel B of Solution Exhibit 5-27) reports the following:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products Total

Revenues

Costs

Operating income ÷ Revenues

$60,000

$66,500

$50,500

$177,000

These activity costs are based on the following:

Activity Cost Allocation Rate

Baked

Goods

Milk &

Fruit Juice

Frozen

Products

5-7

3. The rankings of products in terms of relative profitability are:

Simple Costing System ABC System

1. Frozen products 17.62%

2. Baked goods 11.17

3. Milk & fruit juice 0.30

Frozen products 25.47%

Milk and fruit juice 4.18

Baked goods 0.27

The percentage revenue, COGS, and activity costs for each product line are:

Baked

Goods

Milk &

Fruit Juice

Frozen

Products Total

The baked goods line drops sizably in profitability when ABC is used. Although it constitutes

33.06% of COGS, it uses a higher percentage of total resources in each activity area, especially

Fitzgerald Supermarkets may want to explore ways to increase sales of frozen products.

It may also want to explore price increases on baked goods.

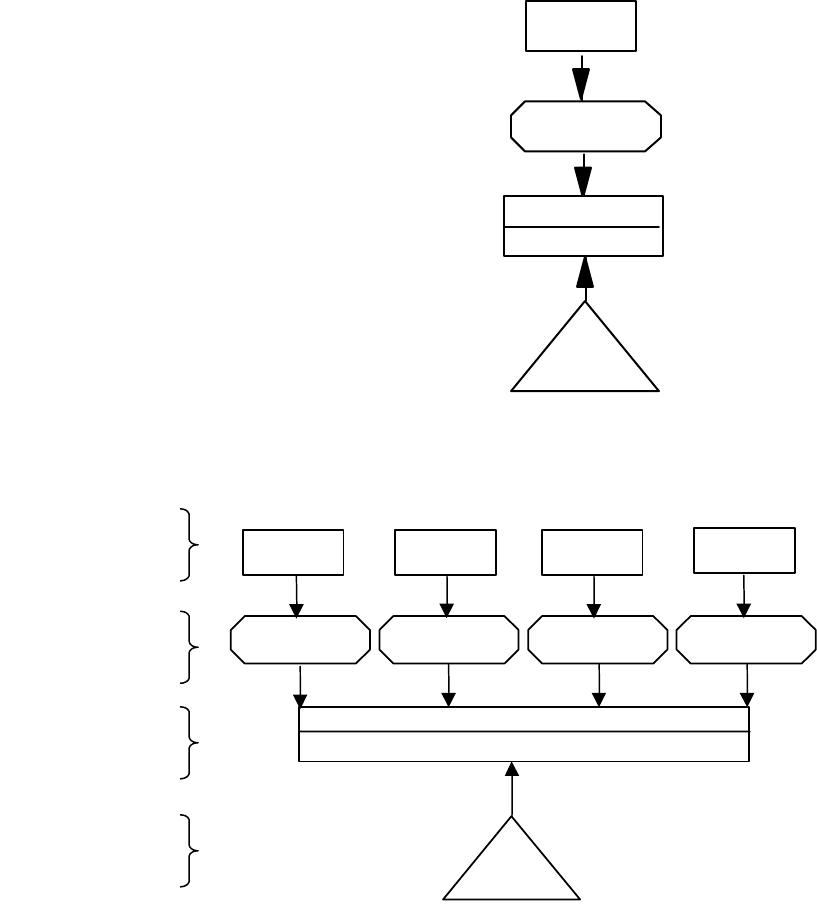

SOLUTION EXHIBIT 5-27

Product-Costing Overviews of Fitzgerald Supermarkets

PANEL A: SIMPLE COSTING SYSTEM

5-8

COST OBJECT:

PRODUCT LINE

Indirect Costs

Direct Costs

Store

Support

COGS

COGS

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

DIRECT

COST

PANEL B: ABC SYSTEM

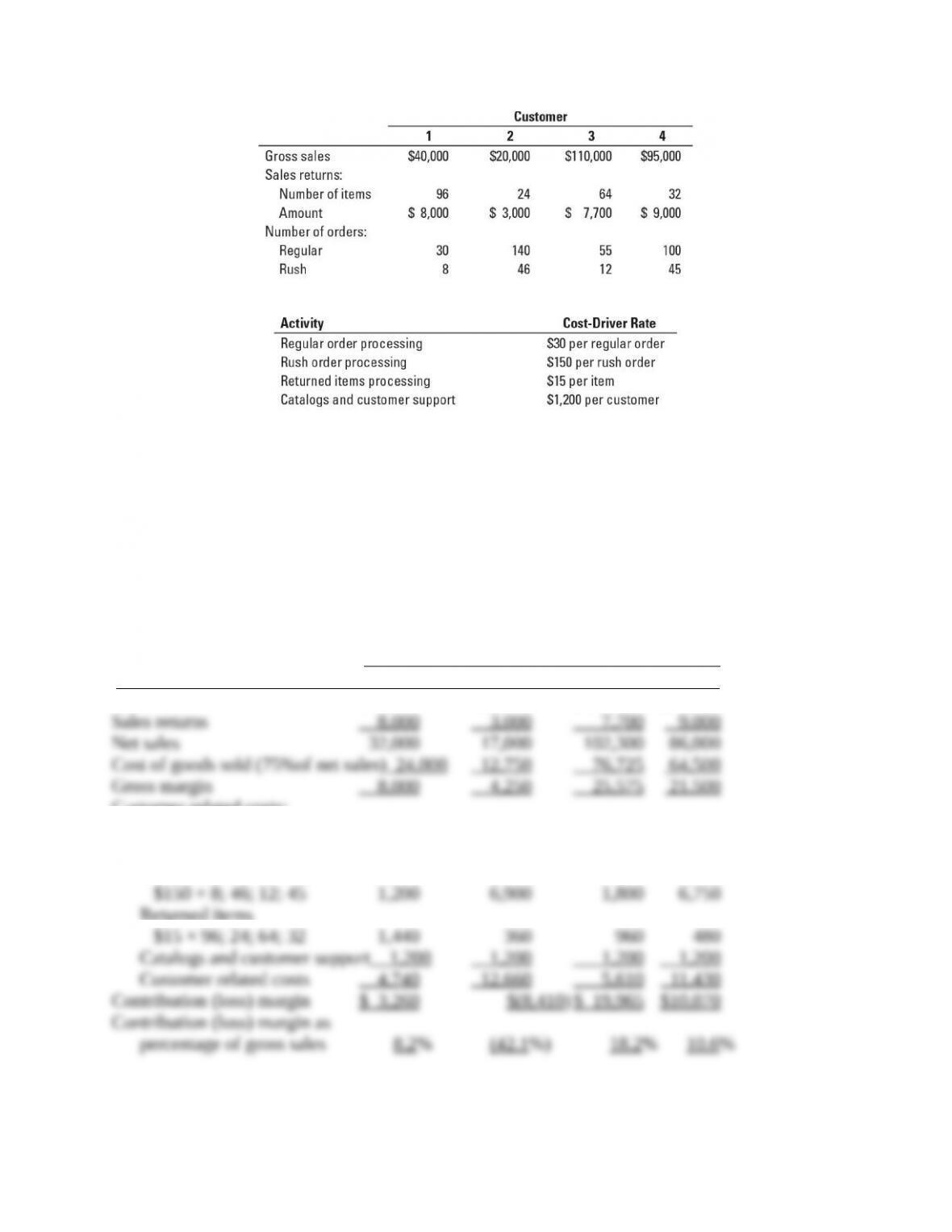

5-28 ABC, wholesale, customer profitability. Veritek Wholesalers operates at capacity and

sells furniture items to four department-store chains (customers). Mr. Veritek commented, “We

apply ABC to determine product-line profitability. The same ideas apply to customer

profitability, and we should find out our customer profitability as well.” Veritek Wholesalers

sends catalogs to corporate purchasing departments on a monthly basis. The customers are

entitled to return unsold merchandise within a six-month period from the purchase date and

receive a full purchase price refund. The following data were collected from last year’s

operations:

5-9

Ordering Delivery Shelf-

Stocking

Customer

Support

Number of

Purchase Order

Number of

Deliveries

Hours of

Shelf-Stocking

Number of

Items Sold

Indirect Costs

Direct Costs

COGS

INDIRECT

COST

POOL

COST

ALLOCATION

BASE

COST OBJECT:

PRODUCT LINE

DIRECT

COST

Veritek has calculated the following activity rates:

Required

Customers pay the transportation costs. The cost of goods sold averages 75% of sales.

Determine the contribution to profit from each customer last year. Comment on your solution.

SOLUTION

(15–20 min.) ABC, wholesale, customer profitability.

Customer

1 2 3 4

Gross sales $40,000 $20,000 $110,000 $95,000

Customer-related costs:

Regular orders

$30 × 30; 140; 55; 100 900 4,200 1,650 3,000

Rush orders

Returned items

5-10

The analysis indicates that customers’ profitability (loss) contribution varies widely from

(42.1%) to 18.2%. Immediate attention to Chain 2 is required which is currently showing a loss

Chain 1 has a disproportionate number of the items returned as well as value of sale

returns. The causes of these should be investigated so that the profitability contribution of Chain

1 could be improved.

5-29 Activity-based costing. The job-costing system at Melody’s Custom Framing has five

indirect cost pools (purchasing, material handling, machine maintenance, product inspection,

and packaging). The company is in the process of bidding on two jobs: Job 220, an order of 17

intricate personalized frames, and Job 330, an order of 5 standard personalized frames. The

controller wants you to compare overhead allocated under the current simple job-costing

system and a newly designed activity-based job-costing system. Total budgeted costs in each

indirect-cost pool and the budgeted quantity of activity driver are as follows.

Information related to Job 220 and Job 330 follows. Job 220 incurs more batch-level costs

because it uses more types of materials that need to be purchased, moved, and inspected relative

to Job 330.

Required

1. Compute the total overhead allocated to each job under a simple costing system, where

overhead is allocated based on machine-hours.

2. Compute the total overhead allocated to each job under an activity-based costing system

using the appropriate activity drivers.

3. Explain why Melody’s Custom Framing might favor the ABC job-costing system over the

5-11

simple job-costing system, especially in its bidding process.

5-12