SOLUTION EXHIBIT 17-29B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed and Units in Ending Work-in-Process Inventory;

Weighted-Average Method of Process Costing for ZanyBrainy Corporation for October 2017.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given) $ 21,000 $ 5,760 $ 14,825

Costs added in current period (given) 83,650 25,440 58,625

*Equivalent units completed and transferred out (given).

†Equivalent units in ending work in process (given).

17-30 FIFO method, assigning costs.

Required:

1. Do Exercise 17-29 using the FIFO method.

2. ZanyBrainy’s management seeks to have a more consistent cost per equivalent unit. Which

method of process costing should the company choose and why?

SOLUTION

(30 min.) FIFO method, assigning costs.

1. Solution Exhibit 17-30A calculates the equivalent units of work done in the current period.

Solution Exhibit 17-30B summarizes total costs to account for, calculates the cost per equivalent

unit of work done in the current period for direct materials and conversion costs, and assigns

these costs to units completed and transferred out and to units in ending work-in-process

inventory.

SOLUTION EXHIBIT 17-30A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing, ZanyBrainy Corporation for October 2017.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

17-B

SOLUTION EXHIBIT 17-30B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory;

FIFO Method of Process Costing, ZanyBrainy Corporation for October 2017.

Total

Production

Costs

Direct

Materials

(Step 3) Work in process, October 1 (given) $ 20,585 $ 5,760

Costs added in October (given) 84 ,065 25,440

Total costs to account for $ 104 ,650 $31,200

*Equivalent units used to complete beginning work in process from Solution Exhibit 17-30A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-30A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-30A, Step 2.

2 . Using the weighted average method will result in a greater degree of cost smoothing since

the cost of beginning inventory is mixed together with costs added each period. This will

produce a more consistent cost per equivalent unit than the FIFO method.

17-B

In the case of ZanyBrainy Corporation, note that the direct material cost per equivalent unit

went from $0.48 in the prior period ($5,760 ÷ 12,000 units) to $0.53 in October, while the

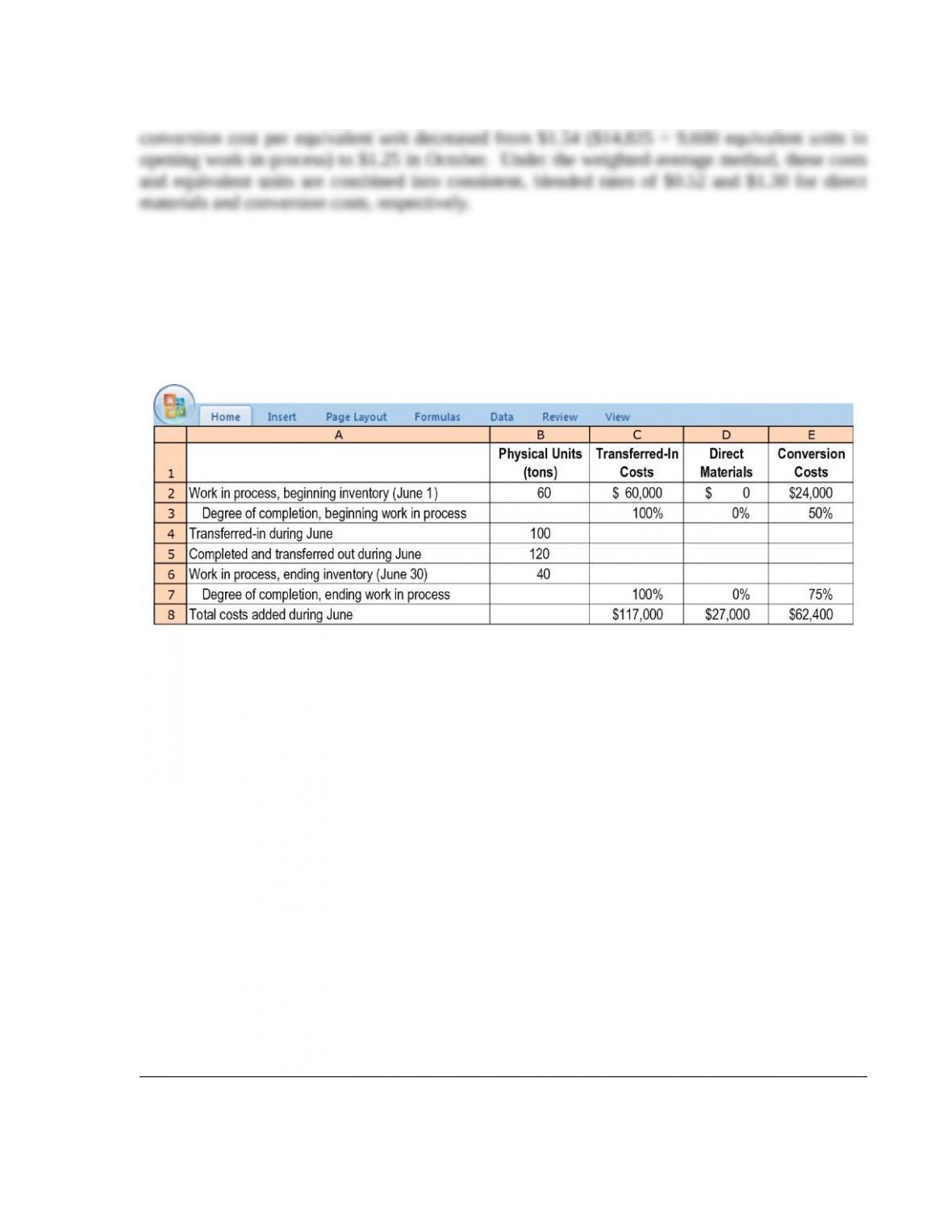

17-31 Transferred-in costs, weighted-average method. Trendy Clothing, Inc. is a

manufacturer of winter clothes. It has a knitting department and a finishing department. This

exercise focuses on the finishing department. Direct materials are added at the end of the

process. Conversion costs are added evenly during the process. Trendy uses the

weighted-average method of process costing. The following information for June 2017 is

available.

Required:

1. Calculate equivalent units of transferred-in costs, direct materials, and conversion costs.

2. Summarize the total costs to account for, and calculate the cost per equivalent unit for

transferred-in costs, direct materials, and conversion costs.

3. Assign costs to units completed (and transferred out) and to units in ending work in process.

SOLUTION

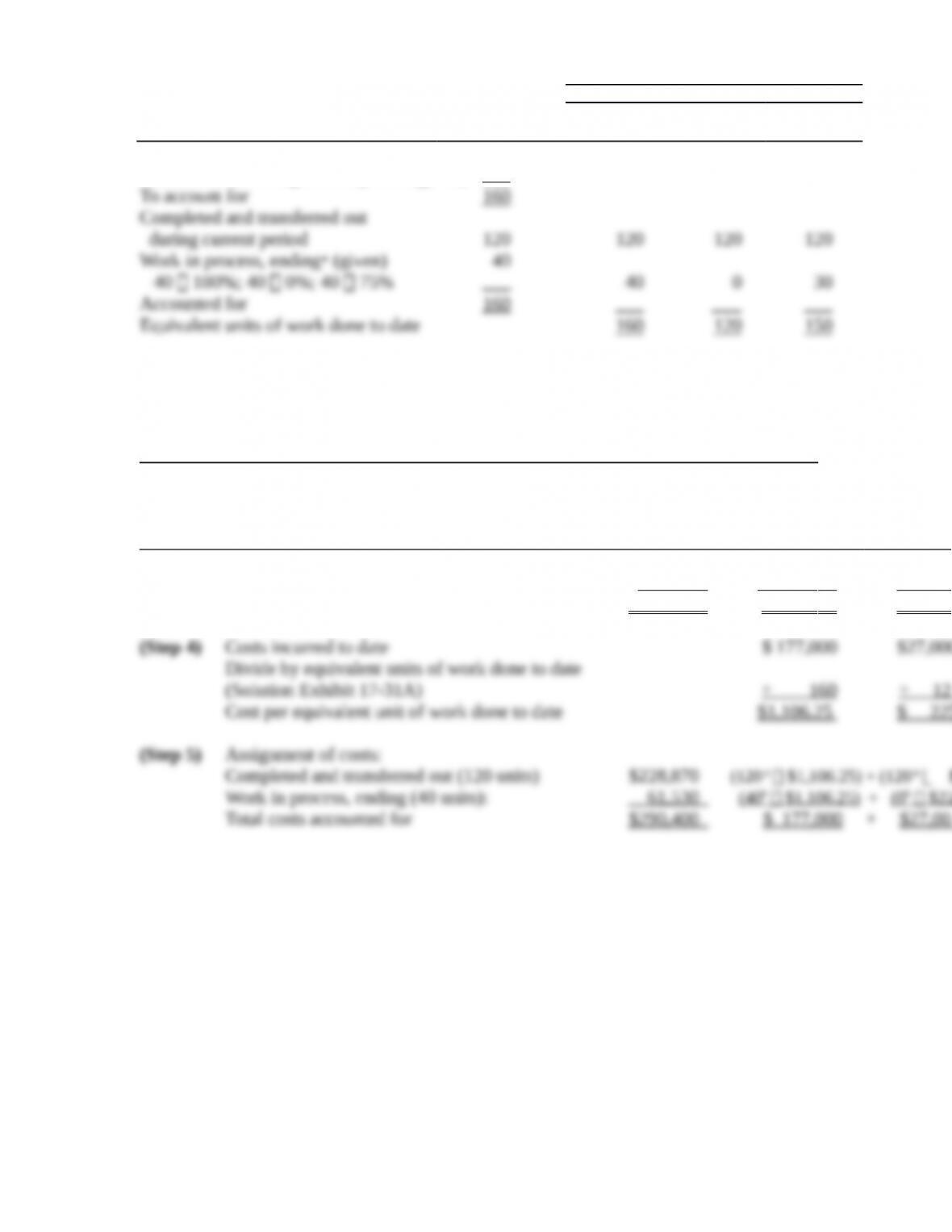

(35–40 min.) Transferred-in costs, weighted-average method.

1, 2. & 3. Solution Exhibit 17-31A calculates the equivalent units of work done to date.

Solution Exhibit 17-31B summarizes total costs to account for, calculates the cost per equivalent

unit of work done to date for transferred-in costs, direct materials, and conversion costs, and

assigns these costs to units completed and transferred out and to units in ending work-in-process

inventory.

SOLUTION EXHIBIT 17-31A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Weighted-Average Method of Process Costing,

Finishing Department of Trendy Clothing for June 2017.

(Step 1) (Step 2)

17-B

Equivalent Units

Flow of Production

Physical

Units

Transferred-

in Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given) 60

Transferred in during current period (given) 100

EXHIBIT 17-31B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory;

Weighted-Average Method of Process Costing,

Finishing Department of Trendy Clothing for June 2017.

Total

Production

Costs

Transferred-in

Costs

Direct

Materials

(Step 3) Work in process, beginning (given) $84,000 $ 60,000 $ 0

Costs added in current period (given) 206 ,400 117,0 00 27,0 00

Total costs to account for $ 290 ,400 $ 177,0 00 $ 27,0 00

a Equivalent units completed and transferred out from Sol. Exhibit 17-31A, step 2.

b Equivalent units in ending work in process from Sol. Exhibit 17-31A, step 2.

17-32 Transferred-in costs, FIFO method. Refer to the information in Exercise 17-31.

Suppose that Trendy uses the FIFO method instead of the weighted-average method in all of its

departments. The only changes to Exercise 17-31 under the FIFO method are that total

transferred-in costs of beginning work in process on June 1 are $45,000 (instead of $60,000) and

total transferred-in costs added during June are $114,000 (instead of $117,000)

Required:

Do Exercise 17-31 using the FIFO method. Note that you first need to calculate equivalent units

of work done in the current period (for transferred-in costs, direct materials, and conversion

17-B

costs) to complete beginning work in process, to start and complete new units, and to produce

ending work in process.

SOLUTION

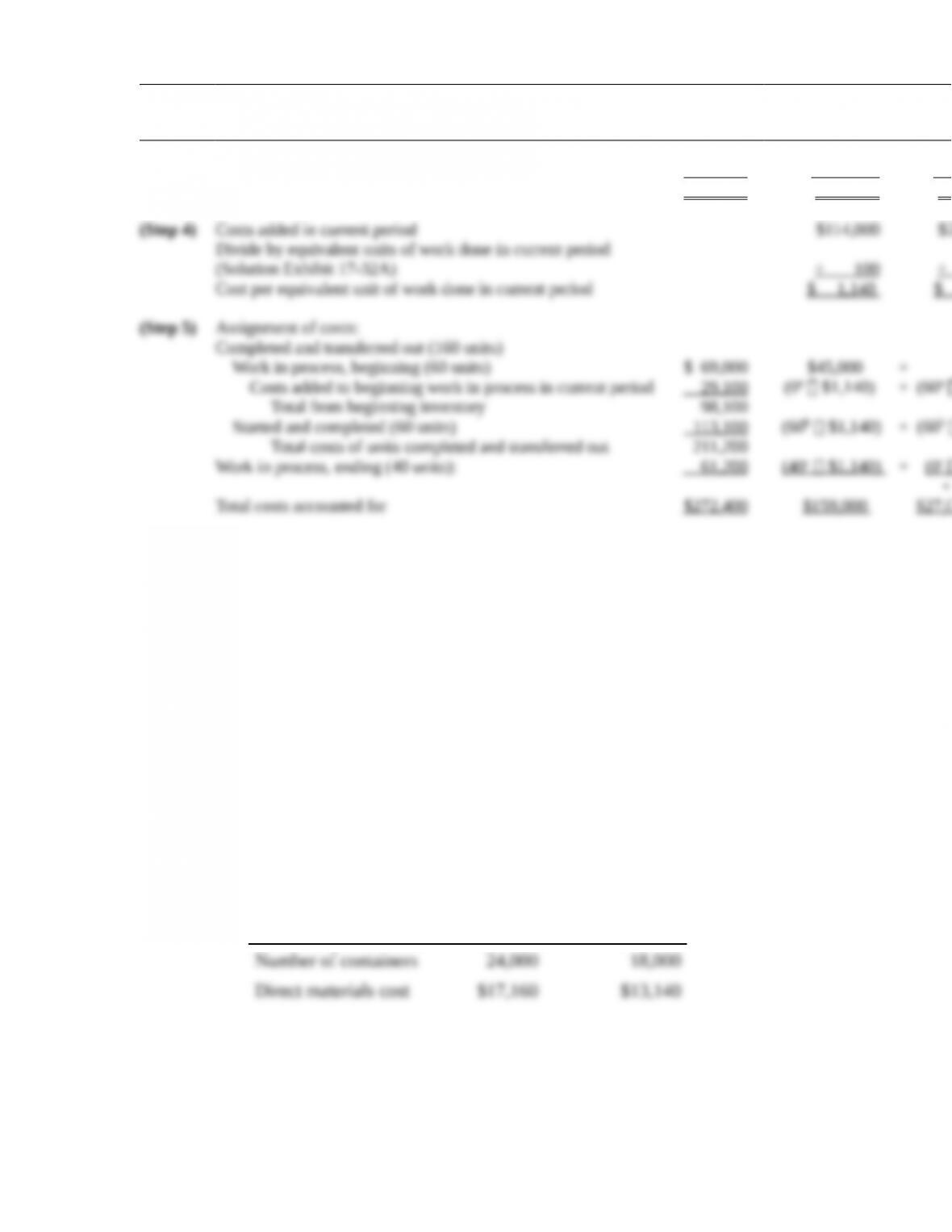

(35–40 min.) Transferred-in costs, FIFO method.

Solution Exhibit 17-32A calculates the equivalent units of work done in the current period (for

transferred-in costs, direct-materials, and conversion costs) to complete beginning

SOLUTION EXHIBIT 17-32A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

FIFO Method of Process Costing,

Finishing Department of Trendy Clothing for June 2017.

(Step 1) (Step 2)

Equivalent Units

Flow of Production

Physical

Units

Transferred-in

Costs

Direct

Materials

Conversion

Costs

Work in process, beginning (given) 60 (work done before current period)

Transferred-in during current period (given) 100

To account for 16 0

aDegree of completion in this department: Transferred-in costs, 100%; direct materials, 0%; conversion costs, 50%.

b120 physical units completed and transferred out minus 60 physical units completed and transferred out from beginning

EXHIBIT 17-32B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and

Assign Costs to the Units Completed and Units in Ending Work-in-Process Inventory;

FIFO Method of Process Costing,

Finishing Department of Trendy Clothing for June 2017.

Total

Production

Transferred-in

Costs

Direct Materials

17-B

Costs

(Step 3) Work in process, beginning (given) $ 69,000 $ 45,000 $ 0

Costs added in current period (given) 203,4 00 114,0 00 27,0

Total costs to account for $ 272,4 00 $159,000 $27,000

a Equivalent units used to complete beginning work in process from Solution Exhibit 17-32A, step 2.

b Equivalent units started and completed from Solution Exhibit 17-32A, step 2.

c Equivalent units in ending work in process from Solution Exhibit 17-32A, step 2.

-33 Operation costing. Egyptian Spa produces two different spa products: Relax and

Refresh. The company uses three operations to manufacture the products: mixing, blending, and

packaging. Because of the materials used, Relax is produced in powder form in the mixing

department, then transferred to the blending department, and finally on to packaging. Refresh

undergoes no mixing; it is produced in liquid form in the blending department and then

transferred to packaging.

Egyptian Spa applies conversion costs based on labor-hours in the mixing department. It

takes 3 minutes to mix the ingredients for a container of Relax. Conversion costs are applied

based on the number of containers in the blending departments and on the basis of

machine-hours in the packaging department. It takes 0.5 minutes of machine time to fill a

container, regardless of the product.

The budgeted number of containers and expected direct materials cost for each product are as

follows:

Relax Refresh

The budgeted conversion costs for each department for May are as follows:

17-B

Department

Allocation of

Conversion Costs

Budgeted Conversion

Cost

Required:

1. Calculate the conversion cost rates for each department.

2. Calculate the budgeted cost of goods manufactured for Relax and Refresh for the month of

May.

3. Calculate the cost per container for each product for the month of May.

17-B