CHAPTER 16

COST ALLOCATION: JOINT PRODUCTS AND BYPRODUCTS

16-1 Give two examples of industries in which joint costs are found. For each example, what

are the individual products at the splitoff point?

Exhibit 16-1 presents many examples of joint products from four different general industries.

These include:

Industry Separable Products at the Splitoff Point

Extractive:

16-2 What is a joint cost? What is a separable cost?

A joint cost is a cost of a production process that yields multiple products simultaneously. A

16-3 Distinguish between a joint product and a byproduct.

The distinction between a joint product and a byproduct is based on relative sales value. A joint

16-4 Why might the number of products in a joint-cost situation differ from the number of

outputs? Give an example.

A product is any output that has a positive sales value (or an output that enables a company to

avoid incurring costs). In some joint-cost settings, outputs can occur that do not have a positive

16-5 Provide three reasons for allocating joint costs to individual products or services.

The chapter lists the following six reasons for allocating joint costs:

1. Computation of inventoriable costs and cost of goods sold for financial accounting

purposes and reports for income tax authorities.

16-1

16-6 Why does the sales value at splitoff method use the sales value of the total production in

the accounting period and not just the revenues from the products sold?

The joint production process yields individual products that are either sold this period or held as

16-7 Describe a situation in which the sales value at splitoff method cannot be used but the

NRV method can be used for joint-cost allocation.

This situation can occur when a production process yields separable outputs at the splitoff point

16-8 Distinguish between the sales value at splitoff method and the NRV method.

Both methods use market selling-price data in allocating joint costs, but they differ in which

sales-price data they use. The sales value at splitoff method allocates joint costs to joint products

16-9 Give two limitations of the physical-measure method of joint-cost allocation.

Limitations of the physical measure method of joint-cost allocation include:

a. The physical weights used for allocating joint costs may have no relationship to the

b. The joint products may not have a common physical denominator––for example, one

16-10 How might a company simplify its use of the NRV method when final selling prices can

vary sizably in an accounting period and management frequently changes the point at which it

sells individual products?

The NRV method can be simplified by assuming (a) a standard set of post-splitoff point

16-11 Why is the constant gross-margin percentage NRV method sometimes called a

“joint-cost-allocation and a profit-allocation” method?

16-2

The constant gross-margin percentage NRV method takes account of the post-splitoff point

16-12 “Managers must decide whether a product should be sold at splitoff or processed further.

The sales value at splitoff method of joint-cost allocation is the best method for generating the

information managers need for this decision.” Do you agree? Explain.

No. Any method used to allocate joint costs to individual products that is applicable to the

problem of joint product-cost allocation should not be used for management decisions regarding

16-13 “Managers should consider only additional revenues and separable costs when making

decisions about selling at splitoff or processing further.” Do you agree? Explain.

No. The only relevant items are incremental revenues and incremental costs when making

decisions about selling products at the splitoff point or processing them further. Separable costs

16-14 Describe two major methods to account for byproducts.

Two methods to account for byproducts are:

16-15 Why might managers seeking a monthly bonus based on attaining a target operating

income prefer the sales method of accounting for byproducts rather than the production method?

The sales byproduct method enables a manager to time the sale of byproducts to affect reported

16-3

16-16 Select Manufacturing Co. produces three joint products and one organic waste byproduct.

Assuming the byproduct can be sold to an outside party, what is the correct accounting treatment

of the byproduct proceeds received by the firm?

a. Apply sale proceeds on a prorated basis to the joint products’ sales.

b. Use the sale proceeds to reduce the common costs in the joint production process.

c. Apply the sale proceeds to the firm’s miscellaneous income account.

d. Either “b” or “c” can be used.

SOLUTION

16-17 Joint costs of $8,000 are incurred to process X and Y. Upon splitoff, $4,000 and $6,000 in

costs are incurred to produce 200 units of X and 150 units of Y, respectively. In order to justify

processing further at the splitoff point, revenues for product:

a. X must exceed $12,000.

b. Y must exceed $14,000.

c. X must be greater than $60 per unit.

d. Y must be greater than $40 per unit.

SOLUTION

Choice “d” is correct. The decision at splitoff point to sell or process further will depend on the

incremental revenues versus costs beyond the splitoff point. Joint costs incurred prior to the

16-4

16-18 Hoston Corporation has two products, Astros and Texans, with the following volume

information:

Volume

Product Astros 20,000 gal

Product Texans 10,000 gal

Total 30,000 gal

The joint cost to produce the two products is $120,000. What portion of the joint cost will each

product be allocated if the allocation is performed by volume?

1. $100,000 and $0 2. $80,000 and $40,000

3. $40,000 and $80,000 4. $50,000 and $50,000

SOLUTION

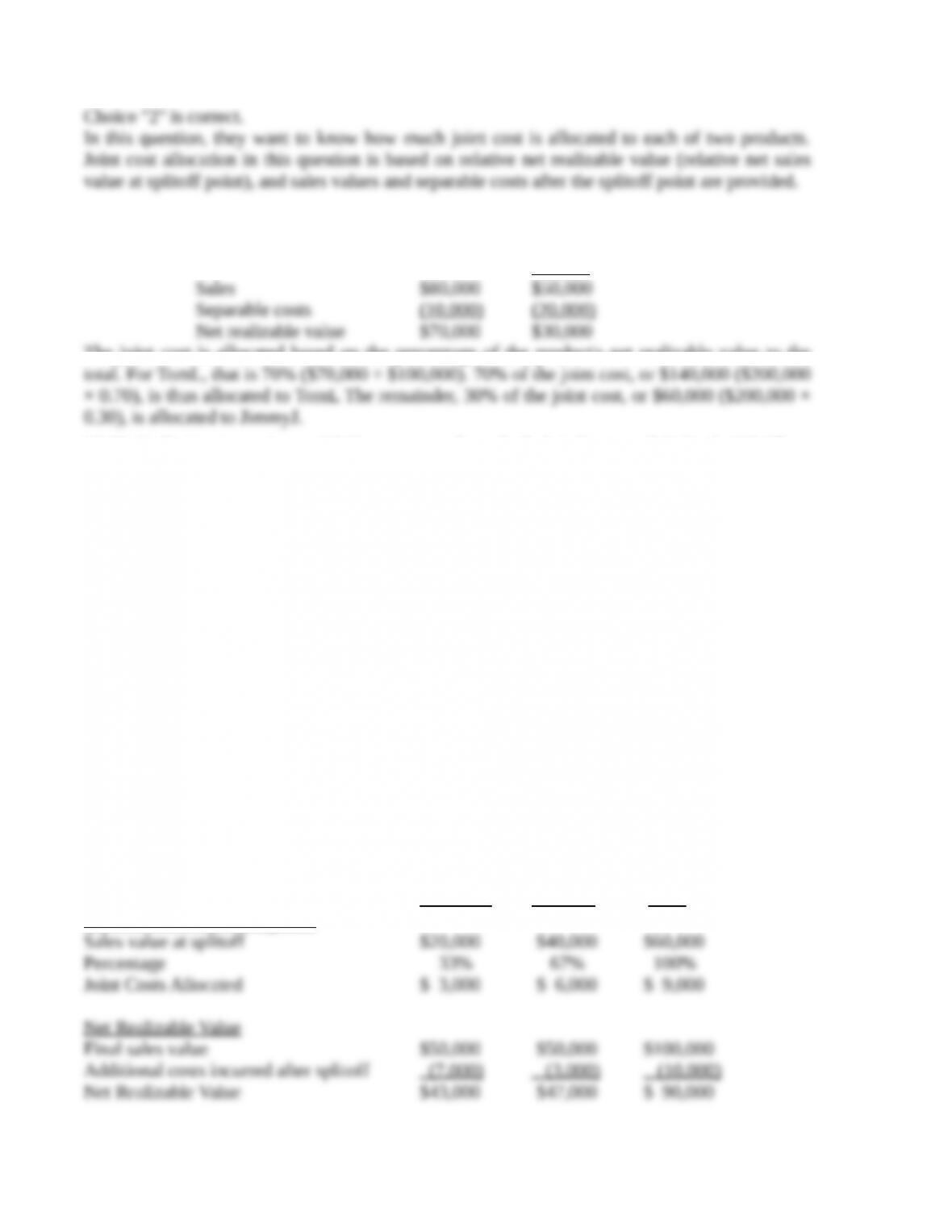

16-19 Dallas Company produces joint products, TomL and JimmyJ, each of which incurs

separable production costs after the splitoff point. Information concerning a batch produced at a

$200,000 joint cost before splitoff follows:

Product

Separable

Costs

Sales

Value

TomL $10,000 $ 80,000

JimmyJ 20,000 50,000

$30,000 $130,000

What is the joint cost assigned to TomL if costs are assigned using relative net realizable value?

1. $60,000 2. $140,000

3. $48,000 4. $200,000

SOLUTION

16-5

Using the relative net realizable value method of allocating joint costs, the net realizable value of

both products can be calculated as follows:

TomL JimmyJ

The joint cost is allocated based on the percentage of the product’s net realizable value to the

16-20 Earl’s Hurricane Lamp Oil Company produces both A-1 Fancy and B Grade Oil. There

are approximately $9,000 in joint costs that Earl may allocate using the relative sales value at

splitoff or the net realizable value approach. Before splitoff, A-1 sells for $20,000 while B grade

sells for $40,000. After an additional investment of $10,000 after splitoff, $3,000 for B grade and

$7,000 for A-1, both the products sell for $50,000. What is the difference in allocated costs for

the A-1 product assuming applications of the net realizable value and the net realizable value at

splitoff approach?

1. A-1 Fancy has $1,300 more joint costs allocated to it under the net realizable value approach

than the sales value at splitoff approach.

2. A-1 Fancy has $1,300 less joint costs allocated to it under the net realizable value approach

than the sales value at splitoff approach.

3. A-1 Fancy has $1,500 more joint costs allocated to it under the net realizable value approach

than the sales value at splitoff approach.

4. A-1 Fancy has $1,500 less joint costs allocated to it under the net realizable value approach

than the sales value at splitoff approach.

SOLUTION

Choice “1” is correct.

A comparison of the results of the net realizable value method of joint cost allocation versus the

relative sale value at splitoff approach produces a $1,300 greater allocation of joint costs to the

A-1 Product when using the net realizable value approach computed as follows:

A1 Fancy B Grade Total

Relative Sales Value at Splitoff

16-6

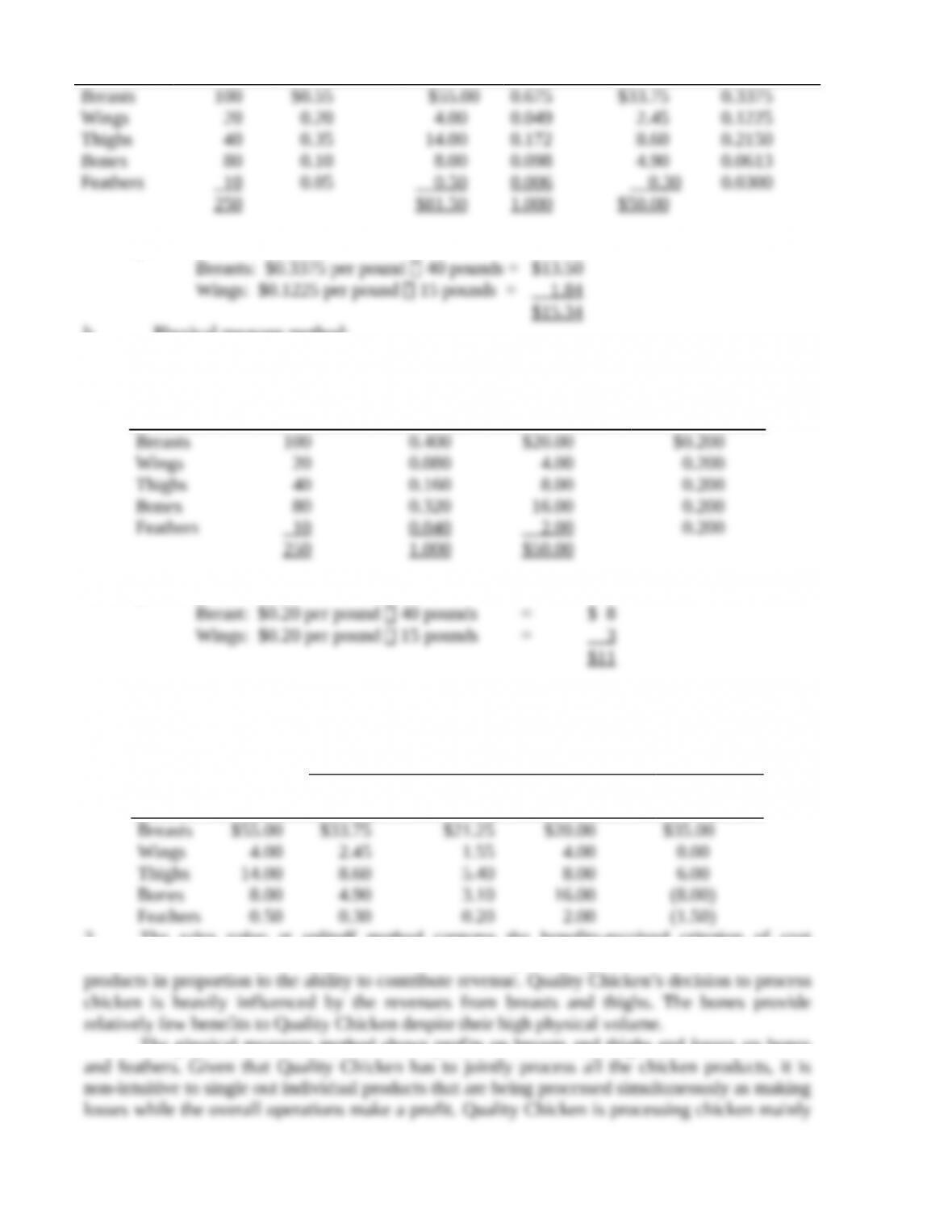

16-21 Joint-cost allocation, insurance settlement. Quality Chicken grows and processes

chickens. Each chicken is disassembled into five main parts. Information pertaining to production

in July 2017 is as follows:

Parts Pounds of Product

Wholesale Selling Price per

Pound When

Production Is Complete

Breasts 100 $0.55

Wings 20 0.20

Thighs 40 0.35

Bones 80 0.10

Feathers 10 0.05

Joint cost of production in July 2017 was $50.

A special shipment of 40 pounds of breasts and 15 pounds of wings has been destroyed in a

fire. Quality Chicken’s insurance policy provides reimbursement for the cost of the items

destroyed. The insurance company permits Quality Chicken to use a joint-cost-allocation

method. The splitoff point is assumed to be at the end of the production process.

Required:

1. Compute the cost of the special shipment destroyed using the following:

a. Sales value at splitoff method

b. Physical-measure method (pounds of finished product)

2. What joint-cost-allocation method would you recommend Quality Chicken use? Explain.

SOLUTION

(20-30 min.) Joint-cost allocation, insurance settlement.

1. (a) Sales value at splitoff method:

Pounds

of

Product

Wholesale

Selling Price

per Pound

Sales

Value

at Splitoff

Weighting:

Sales Value

at Splitoff

Joint

Costs

Allocated

Allocated

Costs per

Pound

16-7

250

$ 81.50

1.000

$ 5 0.00

Costs of Destroyed Product

b. Physical measure method:

Pounds

of

Product

Weighting:

Physical

Measures

Joint

Costs

Allocated

Allocated

Costs per

Pound

250

1.000

$ 50 .00

Costs of Destroyed Product

Note: Although not required, it is useful to highlight the individual product profitability figures:

Sales Value at

Splitoff Method

Physical

Measures Method

Product

Sales

Value

Joint Costs

Allocated

Gross

Income

Joint Costs

Allocated

Gross

Income

2 The sales value at splitoff method captures the benefits-received criterion of cost

allocation and is the preferred method. The costs of processing a chicken are allocated to

The physical measures method shows profits on breasts and thighs and losses on bones

16-8

16-22 Joint products and byproducts (continuation of 16-21). Quality Chicken is computing

the ending inventory values for its July 31, 2017, balance sheet. Ending inventory amounts on

July 31 are 15 pounds of breasts, 4 pounds of wings, 6 pounds of thighs, 5 pounds of bones, and

2 pounds of feathers.

Quality Chicken’s management wants to use the sales value at splitoff method. However,

management wants you to explore the effect on ending inventory values of classifying one or

more products as a byproduct rather than a joint product

Required:

1. Assume Quality Chicken classifies all five products as joint products. What are the ending

inventory values of each product on July 31, 2017?

2. Assume Quality Chicken uses the production method of accounting for byproducts. What are

the ending inventory values for each joint product on July 31, 2017, assuming breasts and

thighs are the joint products and wings, bones, and feathers are byproducts?

3. Comment on differences in the results in requirements 1 and 2.

SOLUTION

(10 min.) Joint products and byproducts (continuation of 16-21).

1. Ending inventory:

2.

Joint products Byproducts Net Realizable Values of

byproducts:

Joint costs to be allocated:

Pounds

of

Product

Wholesale

Selling Price

per Pound

Sales

Value

at Splitoff

Weighting:

Sales Value

at Splitoff

Joint

Costs

Allocated

Allocated

Costs Per

Pound

Ending inventory:

16-9

3. Treating all products as joint products does not require judgments as to whether a product

is a joint product or a byproduct. Joint costs are allocated in a consistent manner to all products

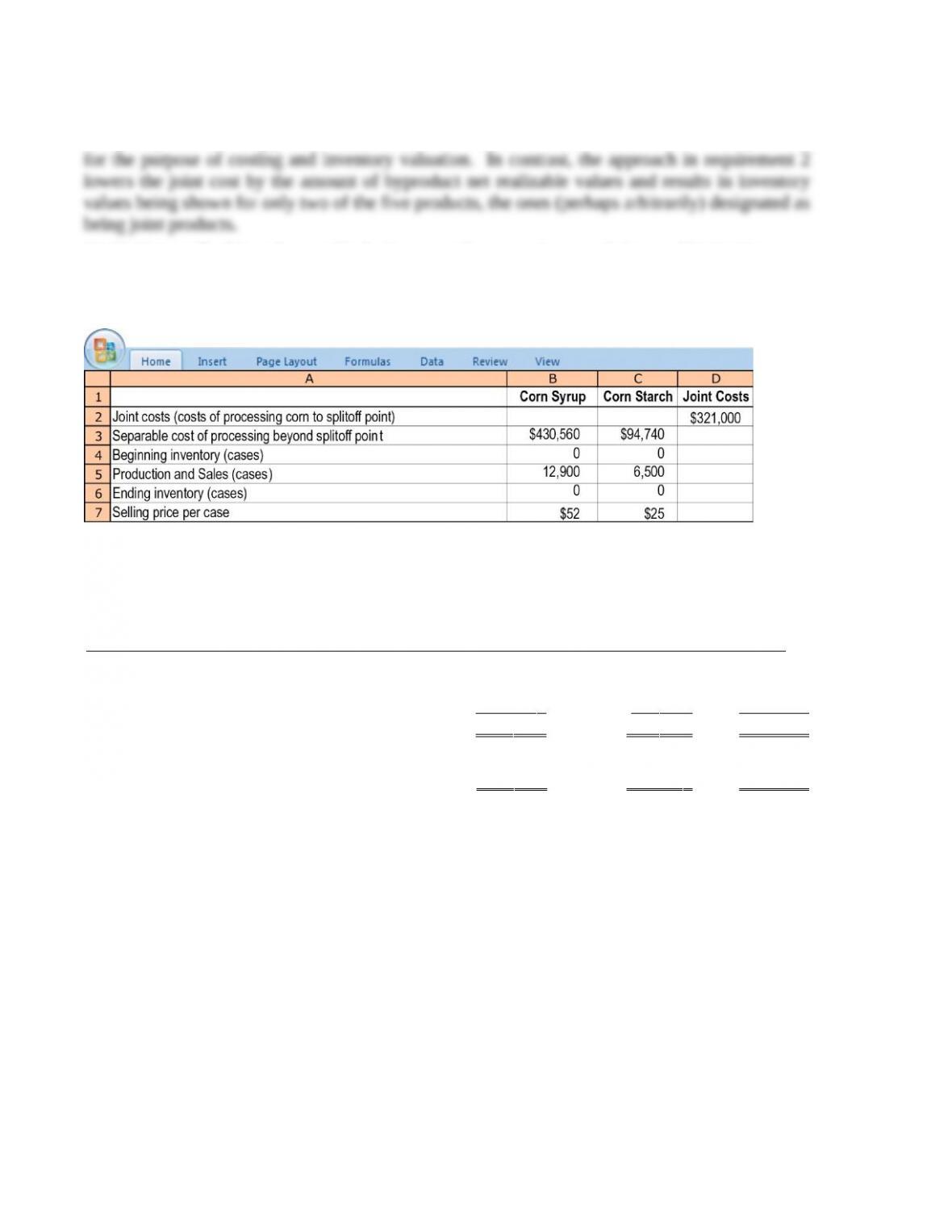

16-23 Net realizable value method. Sweeney Company is one of the world’s leading corn

refiners. It produces two joint products—corn syrup and corn starch—using a common

production process. In July 2017, Sweeney reported the following production and selling-price

information:

Required:

Allocate the $321,000 joint costs using the NRV method.

(10 min.) Net realizable value method.

A diagram of the situation is in Solution Exhibit 16-23.

Corn Syrup Corn Starch Total

Final sales value of total production,

12,900 $52; 6,500 $25 $670,800 $162,500 $833,300

Deduct separable costs 430 ,56 0 94 ,740 525 ,30 0

Net realizable value at splitoff point $240 ,240 $ 67 ,760 $ 308 ,0 00

Weighting, $240,240; $67,760

¸

$308,000 0.78 0.22 1.00

Joint costs allocated, 0.78; 0.22 $321,000 $ 250 ,380 $ 70 ,62 0 $ 321 ,000

16-10