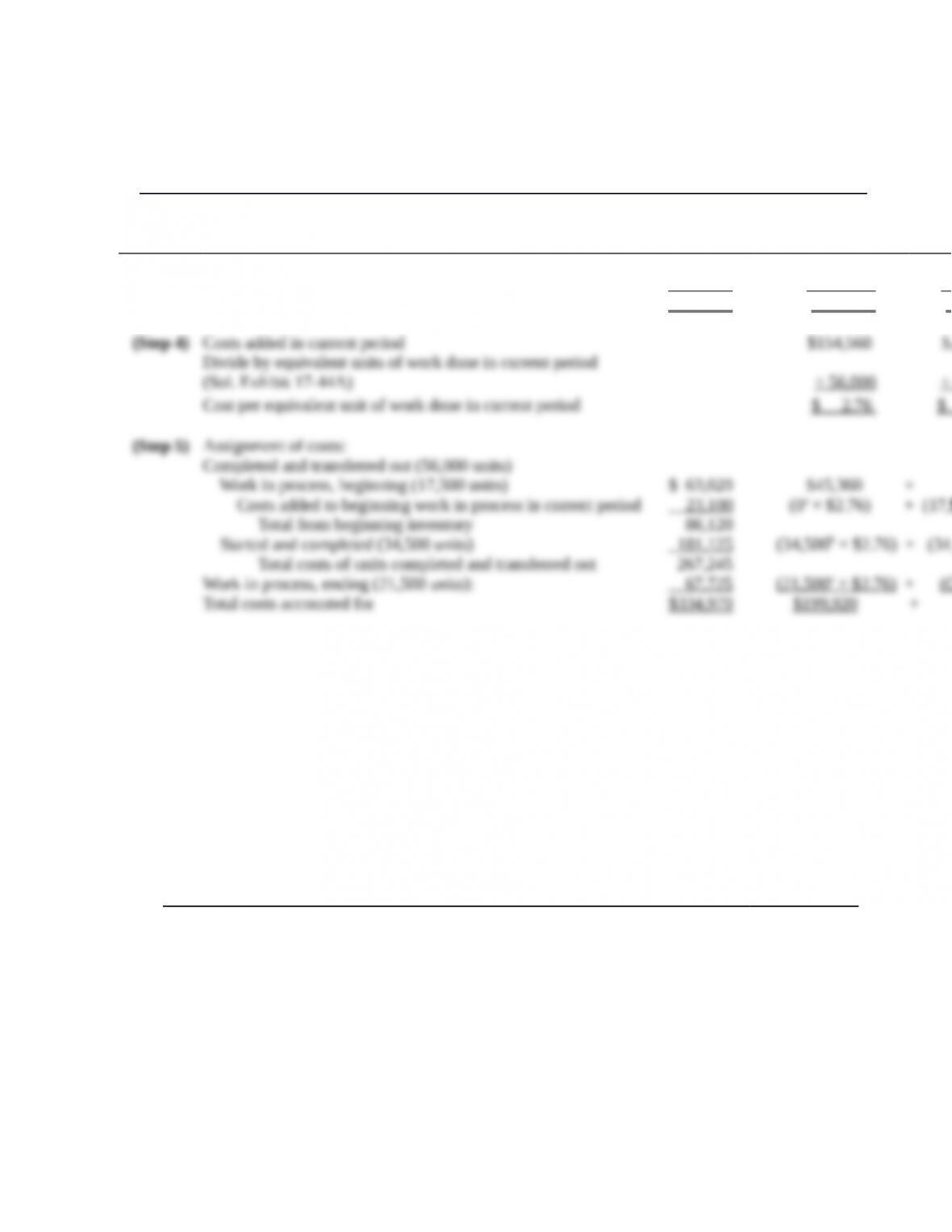

SOLUTION EXHIBIT 17-44B

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed and Units in Ending Work-in-Process Inventory;

FIFO Method of Process Costing,

Stitching Department of Spelling Sports for March 2017.

Total

Production

Costs Transferred-in Costs

Direct

Materials

(Step 3) Work in process, beginning (given) $ 63,020 $ 45,360 $ 0

Costs added in current period (given) 271,950 154,560 28,080

Total costs to account for $ 334,970 $199,920 $28,080

a Equivalent units used to complete beginning work in process from Solution Exhibit 17-44A, step 2.

b Equivalent units started and completed from Solution Exhibit 17-44A, step 2.

c Equivalent units in ending work in process from Solution Exhibit 17-44A, step 2.

17-45 Standard costing, journal entries. The Warner Company manufactures reproductions of

expensive sunglasses. Warner uses the standard-costing method of process costing to account for

the production of the sunglasses. All materials are added at the beginning of production. The

costs and output of sunglasses for May 2017 are as follows:

Physical

Units

% of Completion

for Conversion

Costs

Direct

Materials

Conversion

Costs

Work in process,

beginning

22,000 60% $ 48,400 $ 33,000

Started during May 95,000

Completed and

transferred out

87,000

Work in process, ending 30,000 75%

Standard cost per unit $ 2.20 $ 2.50

Physical

Units

% of Completion

for Conversion

Costs

Direct

Materials

Conversion

Costs

Costs added during May $207,500 $238,000

Required:

1. Compute equivalent units for direct materials and conversion costs. Show physical units in

the first column of your schedule.

2. Compute the total standard costs of sunglasses transferred out in May and the total standard

costs of the May 31 inventory of work in process.

3. Compute the total May variances for direct materials and conversion costs.

4. Prepare summarized journal entries to record both the actual costs and standard costs for

direct materials and conversion costs, including the variances for both production costs.

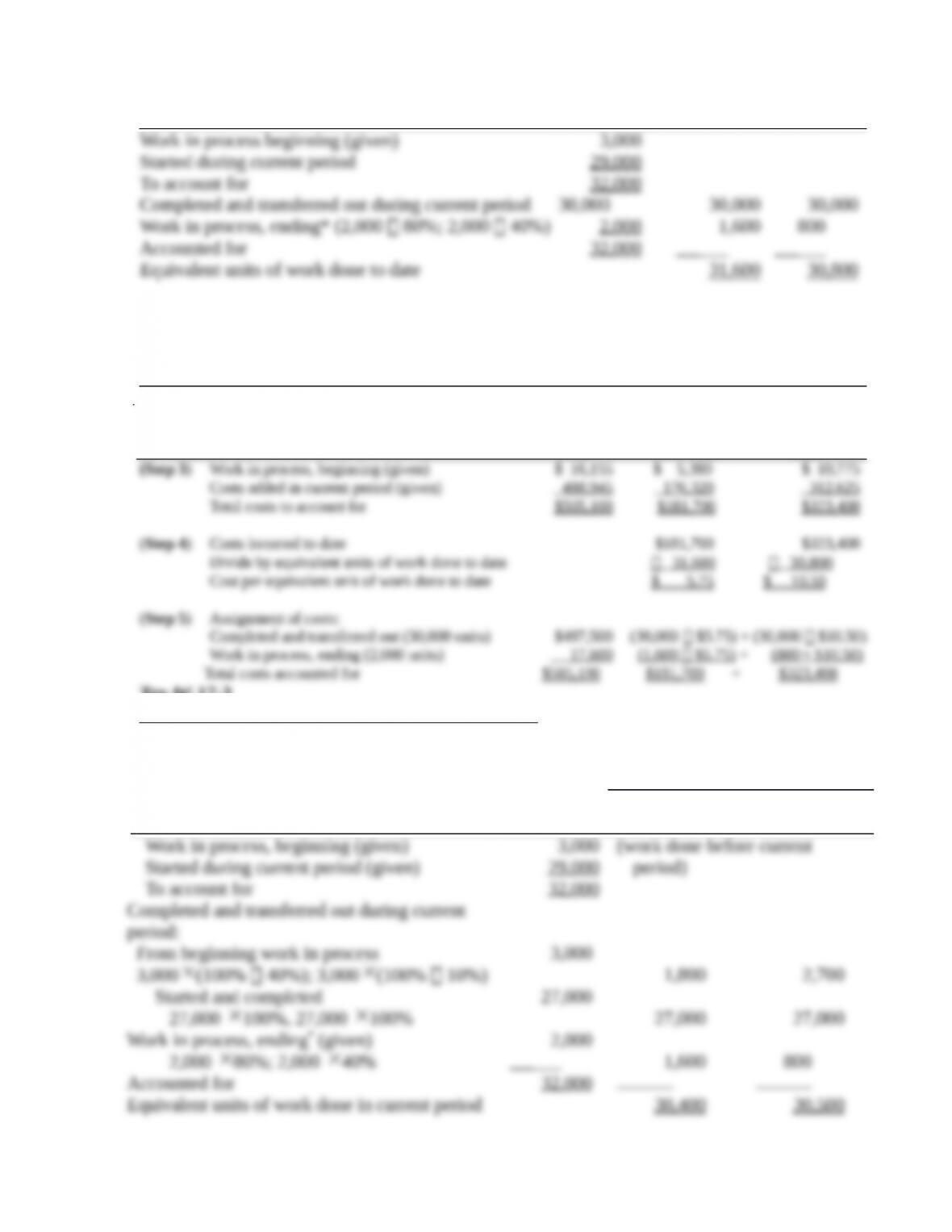

SOLUTION

(30 -35 min.) Standard costing, journal entries.

1. Solution Exhibit 17-45A computes the equivalent units of work done in May 2017 by

the Warner Company for direct materials and conversion costs.

2. and 3. Solution Exhibit 17-45B summarizes total costs of the Warner Company for May

31, 2017, and using the standard cost per equivalent unit for direct materials and conversion

costs, assigns these costs to units completed and transferred out and to units in ending work in

process. The exhibit also summarizes the cost variances for direct materials and conversion costs

for May 2017.

SOLUTION EXHIBIT 17-45A

Summarize the Flow of Physical Units and Compute Output in Equivalent Units;

Standard Costing Method of Process Costing, Warner Company for the Month Ended May 31,

2017.

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Work in process, beginning (given)

Started during current period (given)

22,000

95 ,0 00

(work done before current

period)

SOLUTION EXHIBIT 17-45B

Summarize the Total Costs to Account for, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed and Units in Ending Work-in-Process Inventory; Standard-Costing

Method of Process Costing, the Warner Company for the Month Ended May 31, 2017.

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given) $ 81,400 $ 48,400 + $ 33,000

Costs added in current period at standard costs 449 ,750 ( 95,000 $2.20) + ( 96,300 $2.50)

Total costs to account for $ 531 ,150 $257 ,400 + $273,750

(Step 4) Standard cost per equivalent unit (given) $ 2.20 $ 2.50

(Step 5) Assignment of costs at standard costs:

Completed and transferred out (87,000 units):

*Equivalent units to complete beginning work in process from Solution Exhibit 17-45A, Step 2.

†Equivalent units started and completed from Solution Exhibit 17-45A, Step 2.

#Equivalent units in ending work in process from Solution Exhibit 17-45A, Step 2.

4.

Direct Materials

Direct Materials Control ` 207,500

Accounts Payable Control 207,500

17-46 Multiple processes or operations, costing. The Sedona Company is dedicated to making

products that meet the needs of customers in a sustainable manner. Sedona is best known for its

KLN water bottle, which is a BPA-free, dishwasher-safe, bubbly glass bottle in a soft silicone

sleeve.

The production process consists of three basic operations. In the first operation, the glass is

formed by re-melting cullets (broken or refuse glass). In the second operation, the glass is

assembled with the silicone gasket and sleeve. The resulting product is finished in the final

operation with the addition of the polypropylene cap.

Consulting studies have indicated that of the total conversion costs required to complete a

finished unit, the forming operation requires 60%, the assembly 30%, and the finishing 10%.

The following data are available for March 2017 (there is no opening inventory of any kind):

Cullets purchased $67,500

Silicone purchased $24,000

Polypropylene used $ 6,000

Total conversion costs incurred $68,850

Ending inventory, cullets $ 4,500

Ending inventory, silicone $ 3,000

Number of bottles completed and transferred 12,000

Inventory in process at the end of the month:

Units formed but not assembled 4,000

Units assembled but not finished 2,000

Required:

1. What is the cost per equivalent unit for conversion costs for KLN bottles in March 2017?

2. Compute the cost per equivalent unit with respect to each of the three materials: cullets,

silicone, and polypropylene.

3. What is the cost of goods completed and transferred out?

4. What is the cost of goods formed but not assembled?

5. What is the cost of goods assembled but not finished?

SOLUTION

(25 min.) Multiple processes or operations, costing.

1. Conversion costs incurred in March = $68,850

Equivalent units of work:

2. Cost per equivalent unit for the three materials categories:

17-47 Benchmarking, ethics. Amanda McNall is the corporate controller of Scott Quarry. Scott

Quarry operates 12 rock-crushing plants in Scott County, Kentucky, that process huge chunks of

limestone rock extracted from underground mines.

Given the competitive landscape for pricing, Scott’s managers pay close attention to costs.

Each plant uses a process-costing system, and at the end of every quarter, each plant manager

submits a production report and a production-cost report. The production report includes the

plant manager’s estimate of the percentage of completion of the ending work in process as to

direct materials and conversion costs, as well as the level of processed limestone inventory.

McNall uses these estimates to compute the cost per equivalent unit of work done for each input

for the quarter. Plants are ranked from 1 to 12, and the three plants with the lowest cost per

equivalent unit for direct materials and conversion costs are each given a bonus and recognized

in the company newsletter.

McNall has been pleased with the success of her benchmarking program. However, she has

recently received anonymous e-mails that two plant managers have been manipulating their

monthly estimates of percentage of completion in an attempt to obtain the bonus.

Required:

1. Why and how might managers manipulate their monthly estimates of percentage of

completion and level of inventory?

2. McNall’s first reaction is to contact each plant controller and discuss the problem raised by

the anonymous communications. Is that a good idea?

3. Assume that each plant controller’s primary reporting responsibility is to the plant manager

and that each plant controller receives the phone call from McNall mentioned in requirement

2. What is the ethical responsibility of each plant controller (a) to Amanda McNall and (b) to

Scott Quarry in relation to the equivalent-unit and inventory information each plant provides?

4. How might McNall learn whether the data provided by particular plants are being

manipulated?

SOLUTION

(20 min.) Benchmarking, ethics.

1. The reported monthly cost per equivalent unit of either direct materials or conversion

costs is lower when the plant manager overestimates the percentage of completion of ending

2. While the plant controller has responsibility for preparing the accounting reports for the

plant, in most cases, the plant controller reports directly to the plant manager. If this reporting

3. The plant controller’s ethical responsibilities to McNall and to Scott Quarry are the same.

These include:

Competence: The plant controller is expected to have the competence to make

equivalent unit computations. This competence does not always extend to making

Objectivity: The plant controller should not allow the possibility of the plant being

4. McNall could seek evidence on possible manipulations as follows:

a. Have plant controllers report detailed breakdowns on the stages of production and

b. Examine trends in ending work in process. Divisions that report low amounts of

ending work in process relative to total production are not likely to be able to greatly

Try It! 17-1

Try It! 17-2

Weighted-Average Method of Process Costing:

Summarize the Flow of Physical Units and Compute Output in Equivalent Units:

(Step 2)

(Step 1) Equivalent Units

Physical Direct Conversion

Flow of Production Units Materials Costs

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed and Units in Ending Work-in-Process Inventory:

Total

Production

Costs

Direct

Materials

Conversion

Costs

Try It! 17-3

First-In, First-Out (FIFO) Method of Process Costing:

Summarize the Flow of Physical Units and Compute Output in Equivalent Units:

(Step 1)

(Step 2)

Equivalent Units

Flow of Production

Physical

Units

Direct

Materials

Conversion

Costs

Summarize the Total Costs to Account For, Compute the Cost per Equivalent Unit, and Assign

Costs to the Units Completed and Units in Ending Work-in-Process Inventory:

Total

Production

Costs

Direct

Materials

Conversion

Costs

(Step 3) Work in process, beginning (given) $ 16,155 $ 5,380 $ 10,775

Costs added in current period (given) 4 88 , 945 176,320 312 ,625

Try It! 17-4

1. To obtain the conversion-cost rates, divide the budgeted cost of each operation by the number

of packages that are expected to go through that operation.

Budgeted

Conversion

Cost

Budgeted

Number of

Packages

Conversion

Cost per

Package

2.

Work Order Work Order

#215 #216

Bread type: Dinner Roll Multigrain Loaves

Quantity: 2,400 2,800

Conversion costs are charged using the rates computed in part (1), taking into account the

specific operations that each type of bread actually goes through.