SOLUTION

(30–35 min.) Ethics and quality.

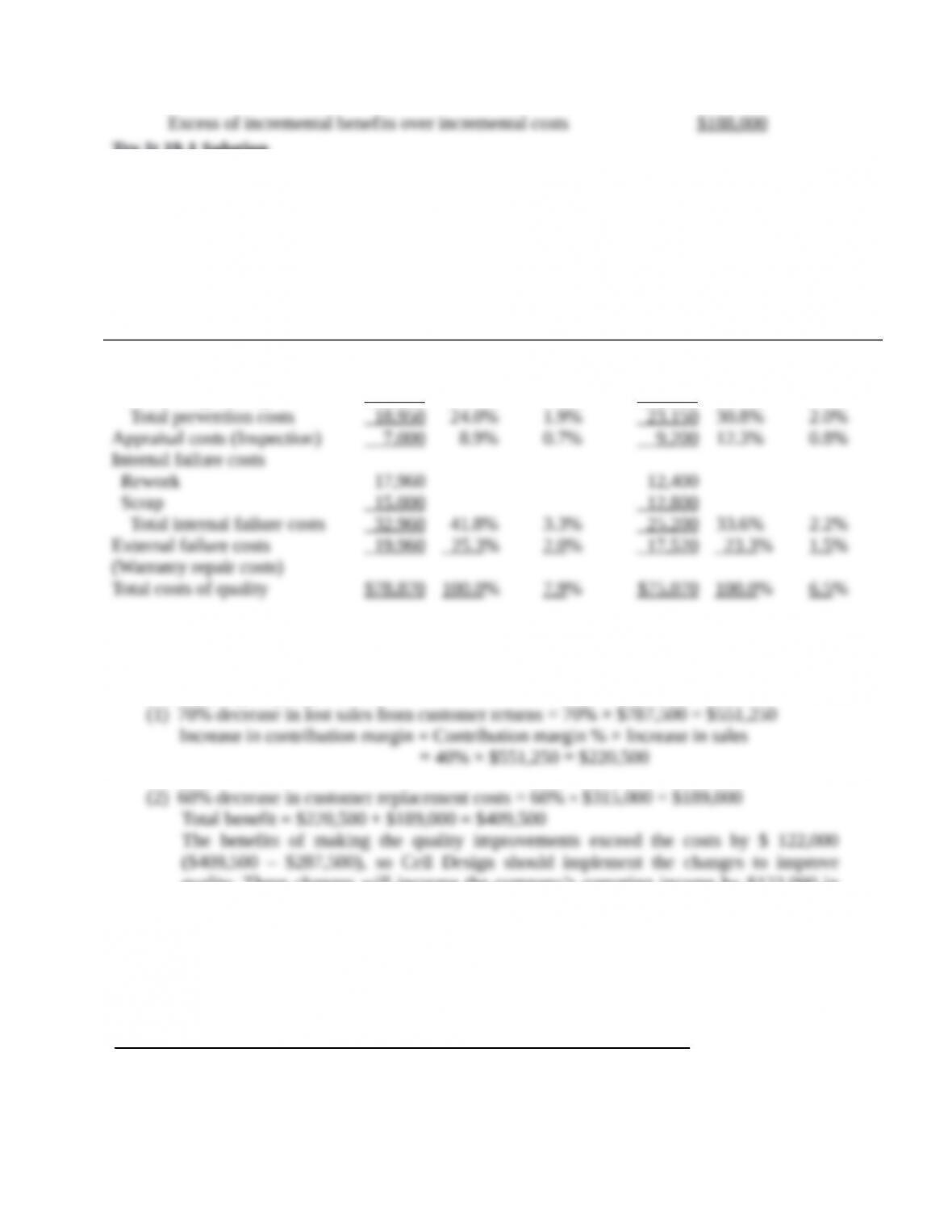

1.

Total Revenue $5,100,000

Costs of Quality Cost

Percentage of

Total Revenue

Prevention Costs

127 ,500 2.50%

Appraisal Costs

Internal Failure Costs

External Failure Costs

Total costs of quality $535 ,500 10.50%

The total costs of quality are currently more than 10% of revenue.

2.

Option 1: Reengineer the Manufacturing Process

(one-time cost of $112,500 in Year 1)

Year One Year Two*

Prevention costs ($48,000 + $7,500 + $72,000 + $112,500) $240,000 $127,500

Appraisal costs ($153,000 × 0.75) 114,750 114,750

*Reengineering cost of $112,500 is a one-time cost and is not reflected in year two costs.

Option 2: Increase Quality Control Training by $22,500 per Year

Year One Year Two

Prevention costs ($48,000 + $7,500 + $22,500 + $72,000) $150,000 $150,000

Appraisal costs ($153,000 × 0.9) 137,700 137,700

Nancy should propose Option (a) (reengineering the manufacturing process) because it decreases

quality costs by $106,800 relative to Option (b) (increasing cost-of-quality control training for

3. Nancy faces a difficult situation. On the one hand, she could argue that she is following

corporate guidelines in choosing what to report and so only reports options that satisfy it. On the

other hand, the guideline does not appear to be so strict that Nancy or Chris would not be able to

Competence

Competence states that each practitioner has a responsibility to provide decision support

Credibility

The management accountant’s standards of ethical conduct require that information should be

fairly and objectively communicated and that all relevant information that could reasonably be

expected to influence an intended user’s understanding of the reports, analyses, or

The instructor should indicate to students that ethical questions are rarely clear-cut. Even

19-38 Quality improvement. Dover Corporation makes printed cloth in two departments:

weaving and printing. Currently, all product first moves through the weaving department and

then through the printing department before it is sold to retail distributors for $2,800 per roll.

Dover provides the following information:

Dover can start only 20,000 rolls of cloth in the weaving department because of capacity

constraints of the weaving machines. Of the 20,000 rolls of cloth started in the weaving

department, 1,000 (5%) defective rolls are scrapped at zero net disposal value. The good rolls

from the weaving department (called gray cloth) are sent to the printing department. Of the

19,000 good rolls started at the printing operation, 1,900 (10%) defective rolls are scrapped at

zero net disposal value. The Dover Corporation’s total monthly sales of printed cloth equal the

printing department’s output.

Required:

1. The printing department is considering buying 10,000 additional rolls of gray cloth from an

outside supplier at $2,000 per roll, which is much higher than Dover’s cost of weaving the

roll. The printing department expects that 10% of the rolls obtained from the outside supplier

will result in defective products. Should the printing department buy the gray cloth from the

outside supplier? Show your calculations.

2. Dover’s engineers have developed a method that would lower the printing department’s rate

of defective products to 6% at the printing operation. Implementing the new method would

cost $1,400,000 per month. Should Dover implement the change? Show your calculations.

3. The design engineering team has proposed a modification that would lower the weaving

department’s rate of defective products to 3%. The modification would cost the company

$700,000 per month. Should Dover implement the change? Show your calculations.

SOLUTION

(45–50 min.) Quality improvement, theory of constraints.

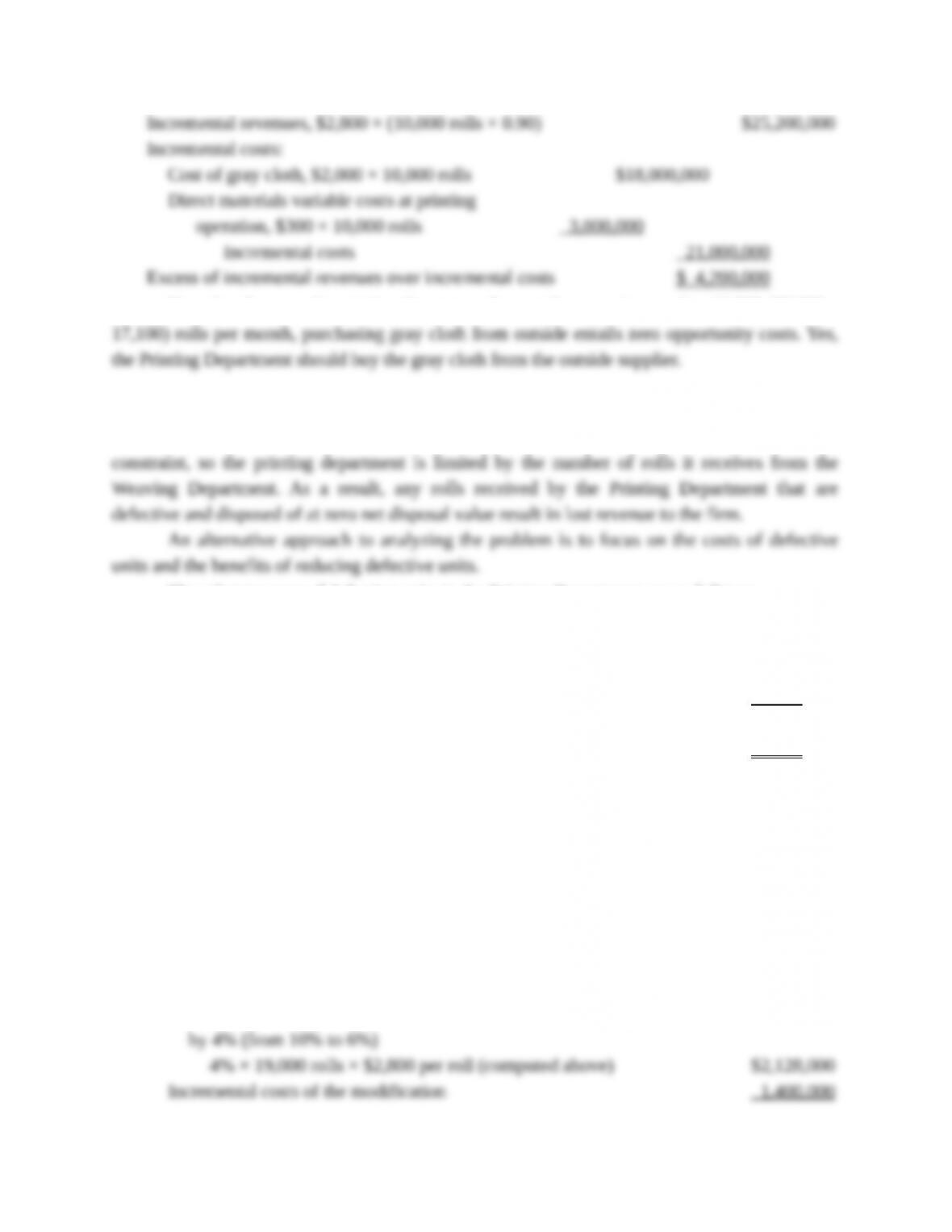

1. Consider the incremental revenues and incremental costs to Dover Corporation of

purchasing additional gray cloth from outside suppliers.

Note that, because the printing department has surplus capacity equal to 12,900 (30,000 –

2. By producing a defective roll in the Printing Department, Dover Corporation is worse off

by the entire amount of revenue forgone of $2,800 per roll. The weaving operation is a

The relevant costs of defective units in the Printing Department are as follows:

a. Direct materials variable costs in the Weaving Department $1,200

b b. Direct materials variable costs in the Printing Department 300

c. Contribution margin forgone from not selling one roll

$2,800 – $1,200 – $300 1 ,300

Amount by which Dover Corporation is worse off as a

result of a defective unit in the Printing Department $2 ,800

Note that only the variable costs of defective units of $1,500 per roll (direct materials in the

Weaving Department, $1,200 per roll: direct materials in the Printing Department, $300 per roll)

are relevant because improving quality will save these costs. Fixed costs of producing defective

units, attributable to other operating costs, are irrelevant because these costs will be incurred

whether Dover Corporation reduces defective units in the Printing Department or not. In

addition, there is an opportunity cost of contribution margin forgone as a result of producing a

defective unit in the Printing Department because it results in lost revenue.

Dover Corporation should make the proposed modifications in the Printing Department

because the incremental benefits exceed the incremental costs by $250,000 per month:

Incremental benefits of reducing defective units in the Printing Department

1. To determine how much Dover Corporation is worse off by producing a defective roll in the

Weaving Department, consider the payoff to Dover from not having a defective roll produced in

the Weaving Department. The good roll produced in the Weaving Department will be sent for

further processing in the Printing Department. The relevant costs and benefits of printing and

selling this roll follow:

By producing a defective roll in the Weaving Department, Dover Corporation is worse off by

$2,220 per roll. Note that, because the weaving operation is a constraint, any rolls that are

defective will result in lost revenue to the firm.

An alternative approach to analyzing the problem is to focus on the costs and benefits of

reducing defective units.

The relevant costs of defective units in the Weaving Department are as follows:

a. Direct materials variable costs in the Weaving Department $1,200

b. Expected unit contribution margin forgone from

not selling one roll, ($2,800 × 0.9) – $1,200 – $300 1 ,020

Amount by which Dover Corporation is worse off as a result

of producing a defective unit in the Weaving Department $2 ,220

Note that only the variable scrap costs of $1,200 per roll (direct materials in the Weaving

Department) are relevant because improving quality will save these costs. All fixed costs of

producing defective units attributable to other operating costs are irrelevant because these costs

will be incurred whether Dover Corporation reduces defective units in the Weaving Department

or not. In addition, there is an opportunity cost of contribution margin forgone as a result of

producing a defective unit in the Weaving Department because it results in lost revenue.

Dover Corporation should make the improvements proposed by the design engineering

team because the incremental benefits exceed the incremental costs by $188,000 per month:

Incremental benefits of reducing defective units in the Weaving Department

Try It 19-1 Solution

1. Prevention Costs: Design engineering, Process engineering

Appraisal Costs: Inspection

Internal Failure Costs: Rework, Scrap

External Failure Costs: Warranty repair costs

2.

2016

2016 % of

Total

COQ

2016 %

of

Revenue 2017

2017 %

of Total

COQ

2017 %

of

Revenue

Prevention costs:

Design engineering $ 8,950 $12,950

Process engineering 10 ,000 10 ,200

Try It 19-2 Solution

Cost of making quality improvements = $150,000 + $137,500 = $287,500

Benefits of quality improvements:

quality. These changes will increase the company’s operating income by $122,000 in

the current year. The quality improvements are also likely to help the company increase

operating income in the future.

Try It 19-3 Solution

1a. Average waiting time for an order of Z39

( ) ( )

( )

2

Annual average number Manufacturing time

of orders of Z39 per order of Z39

Annual machine Annual average number Manufacturing time

2

capacity of orders of Z39 per order of Z39

x

´

ù

é– ´ ú

ê

ëû

1b.

= +

2a. Average waiting time for Z39 and Y28

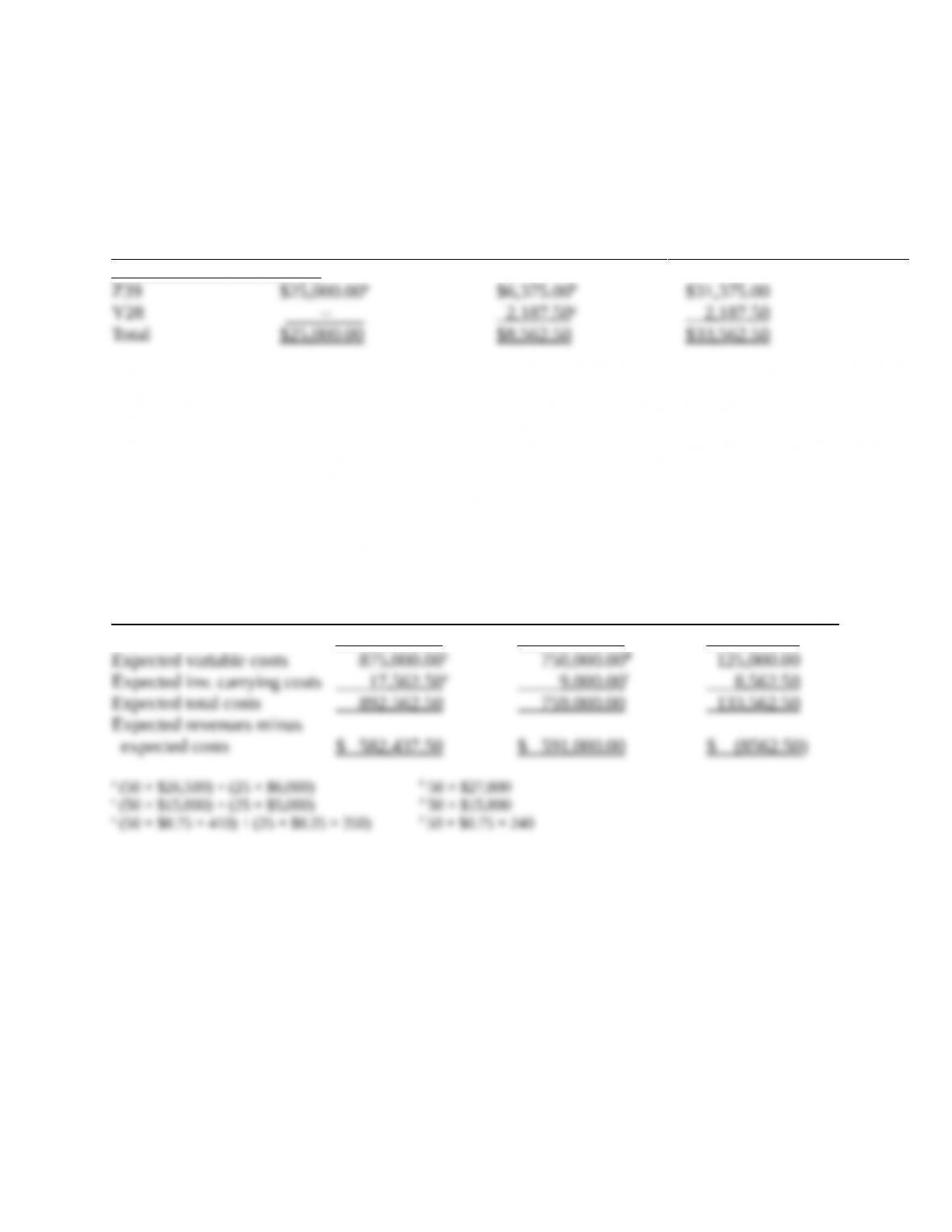

3.

Selling price per order of Y28, which has an average

manufacturing lead time of more than 320 hours $ 6,000

Expected loss in revenues and increase in costs from introducing Y28:

2

= = = =

Average manufacturing

cycle time per order for Z39

Average order

waiting time

Order manufacturing

time for Z39

2 2

Annual average Manufacturing Annual average Manufacturing

number of time per order number of time per order

orders of Z39 of Z39 orders of Y28 of Y28

é

é ù é ù

æ ö æ ö æ ö æ ö

ê

ê ú ê

ç ÷ ç ÷ ç ÷ ç ÷

´ ´ ´

ç ÷ ç ÷ ç ÷ ç ÷ê

ê ú ê

è ø è ø è ø è ø

ê

ë û ë

ë

Annual Annual average Manufacturing Annual average Manufacturing

2 machine number of time per order number of time per or

capacity orders of Z39 of Z39 orders of Y28

ù

ú

ú

ú

ú

ú

û

û

é ù

é æ ö æ ö æ ö

ê ú

ç ÷ ç ÷ ç ÷´ – ´ – ´

êç ÷ ç ÷ ç ÷

ê ú

ê

ë è ø è ø è ø

ë û

der

of Y28

ù

é ù

æ ö ú

ê ú

ç ÷

ç ÷ú

ê ú

è ø

ë û

û

2 2

a 50 orders × ($27,000 – $26,500)

b (410 hours – 240 hours) × $0.75 × 50 orders

c (350 hours – 0) × $0.25 × 25

Increase in expected contribution from Y28 of $25,000 is less than increase in expected costs of

$33,562.50 by $8,562.50. Therefore, Seawall should not introduce Y28.

Alternative calculations of incremental revenues and incremental costs of introducing Y28:

Alternative 2:

Alternative 1: Do Not Relevant Revenues

Introduce Y28 Introduce Y28 and Relevant Costs

(1) (2) (3) = (1) – (2)

Expected revenues $1,475,000.00a$1,350,000.00b$125,000.00