SOLUTION

(20–30 min.) Direct materials and manufacturing labor variances, solving unknowns.

All given items are designated by an asterisk.

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

Direct

Purchases Usage

1. 4,000 units × 0.5 hours/unit = 2,000 hours

2. Flexible budget – Efficiency variance = $40,000 – $2,200 = $37,800

3. $37,800 + Price variance, $1,890 = $39,690, the actual direct manuf. labor cost

4. Standard qty. of direct materials = 4,000 units × 3 pounds/unit = 12,000 pounds

5. Flexible budget + Dir. matls. effcy. var. = $48,000 + $2,400 = $50,400

6. Actual cost of direct materials, $55,000 – Price variance, $3,500 = $51,500

7. Actual direct materials price = $51,500 ÷ 12,875 lbs = $4.27 per lb.

7-42 Direct materials and manufacturing labor variances, journal entries. Collegiate Corn Hole is a small business that

Zach Morris developed while in college. He began building wooden corn hole game sets for friends, hand painted with college col-

ors and logos. As demand grew, he hired some workers and began to manage the operation. Collegiate Corn Hole maintains two de-

partments: construction and painting. In the construction department, the games require wood and labor. Collegiate Corn Hole has

some employees who have been with the company for a very long time and others who are new and inexperienced.

Collegiate Corn Hole uses standard costing for the game sets. Zach expects that a typical set should take 4 hours of labor in the

construction department, and the standard wage rate is $10.00 per hour. An average set uses 24 square feet of wood, allowing for a

certain amount of scrap. Because of the nature of the wood, workers must work around flaws in the materials. Zach shops around for

good deals and expects to pay $5.00 per square feet.

Zach does not store inventory, and buys the wood as he receives an order.

For the month of September, Zach’s workers produced 60 corn hole sets using 250 hours and 1,500 square feet of wood. Zach

bought wood for $7,350 (and used the entire quantity) and incurred labor costs of $2,375.

Required:

1. For the construction department, calculate the price and efficiency variances for the wood and the price and efficiency vari-

ances for direct manufacturing labor.

2. Record the journal entries for the variances incurred.

3. Discuss logical explanations for the combination of variances that the construction department of Collegiate Corn Hole ex-

perienced.

SOLUTION

(20 min.) Direct materials and manufacturing labor variances, journal entries.

1.

Direct Materials:

Actual Costs

Incurred

(Actual Input

Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

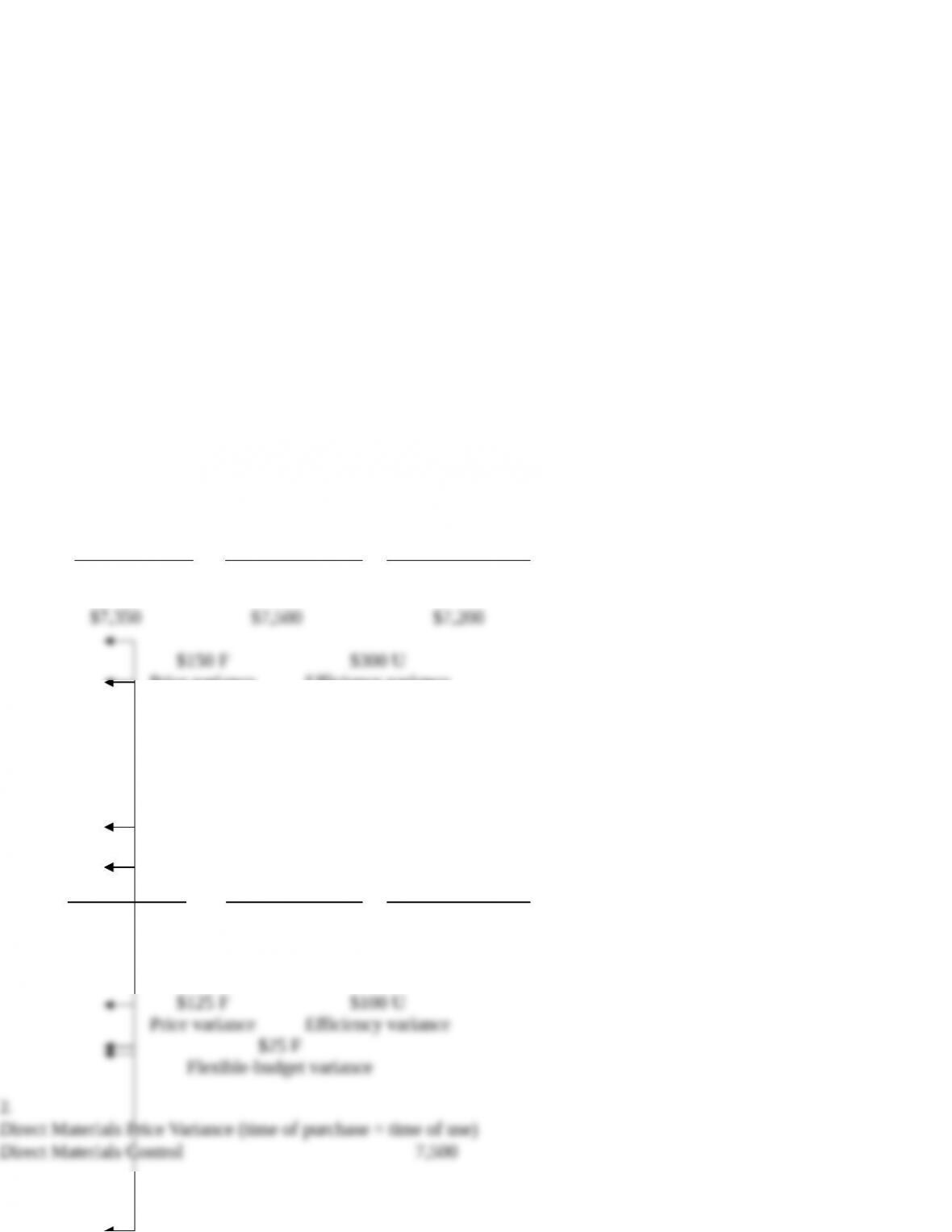

Wood (given)

1,500 $5.00

60 24 $5.00

Price variance Efficiency variance

$150 U

Flexible-budget variance

Direct Manufacturing Labor:

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

(given)

$2,375

250 $10

$2,500

60 4 $10

$2,400

Direct Materials Efficiency Variance

Direct Manufacturing Labor Variances

3. Plausible explanations for the above variances include:

7-43 Use of materials and manufacturing labor variances for benchmarking. You are a new junior accountant at In Fo-

cus Corporation, maker of lenses for eyeglasses. Your company sells generic-quality lenses for a moderate price. Your boss, the

controller, has given you the latest month’s report for the lens trade association. This report includes information related to oper-

ations for your firm and three of your competitors within the trade association. The report also includes information related to the in-

dustry benchmark for each line item in the report. You do not know which firm is which, except that you know you are Firm A.

Unit Variable Costs Member Firms for the

Month Ended September 30, 2017

Firm A Firm B Firm C Firm D Industry Benchmark

Materials input 2.15 2.00 2.20 2.60 2.15 oz. of glass

Materials price $ 5.00 $ 5.25 $ 5.10 $ 4.50 $ 5.10 per oz.

Labor-hours used 0.75 1.00 0.65 0.70 0.70 hours

Wage rate $14.50 $14.00 $14.25 $15.25 $12.50 per DLH

Variable overhead

rate

$ 9.25 $14.00 $ 7.75 $11.75 $12.25 per DLH

Required:

1. Calculate the total variable cost per unit for each firm in the trade association. Compute the percent of total for the material,

labor, and variable overhead components.

2Using the trade association’s industry benchmark, calculate direct materials and direct manufacturing labor price and effi-

ciency variances for the four firms. Calculate the percent over standard for each firm and each variance.

3. Write a brief memo to your boss outlining the advantages and disadvantages of belonging to this trade association for

benchmarking purposes. Include a few ideas to improve productivity that you want your boss to take to the department

heads’ meeting.

SOLUTION

(30 min.) Use of materials and manufacturing labor variances for benchmarking

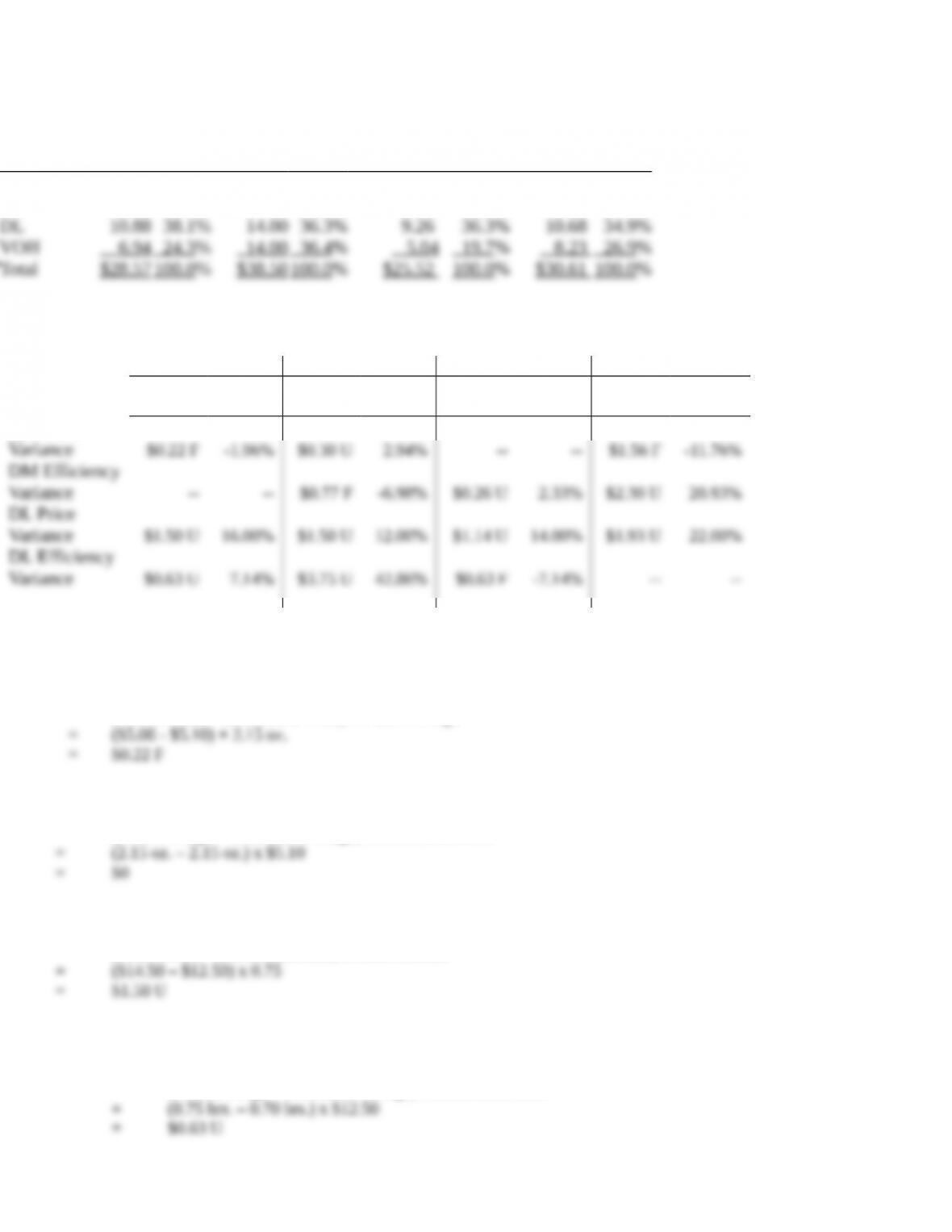

1. Unit variable cost (dollars) and component percentages for each firm:

Firm A Firm B Firm C Firm D

DM $10.75 37.6% $10.50 27.3% $11.22 44.0% $11.70 38.2%

2. Variances and percentage over/under standard for each firm relative to the Industry Benchmark:

Firm A Firm B Firm C Firm D

Variance

% over

standard Variance

% over

standard Variance

% over

standard Variance

% over

standard

DM Price

We illustrate these calculations for Firm A.

The DM Price Variance is computed as:

(Firm A Price – Benchmark Price) × Firm A Usage

The DM Efficiency Variance is computed as follows:

(Firm A Usage – Benchmark Usage) x Benchmark Price

The DL Price Variance is computed as:

(Firm A Rate – Benchmark Rate) x Firm A Hours

The DL Efficiency Variance is computed as follows:

(Firm A Usage – Benchmark Usage) x Benchmark Rate

The % over standard is the percentage difference in prices relative to the Industry Benchmark. Again using the DM Price Variance

calculation for Firm A, the % over standard is given by:

(Firm A Price – Benchmark Price)/Benchmark Price

3.

To: Controller

From: Junior Accountant

Re: Benchmarking & productivity improvements

Date: March 15, 2017

Benchmarking advantages

Benchmarking disadvantages

Areas to discuss

– we may want to find out whether we can get the same lower price for glass as Firm D

7-44 Direct manufacturing labor variances: price, efficiency, mix, and yield. Elena Martinez em-

ploys two workers in her wedding cake bakery. The first worker, Gabrielle, has been making wedding cakes for 20 years and is paid

$25 per hour. The second worker, Joseph, is less experienced and is paid $15 per hour. One wedding cake requires, on average, 6

hours of labor. The budgeted direct manufacturing labor quantities for one cake are as follows:

Quantity

Gabrielle 3 hours

Joseph 3 hours

Total 6 hours

That is, each cake is budgeted to require 6 hours of direct manufacturing labor, composed of 50% of Gabrielle’s labor and 50% of

Joseph’s, although sometimes Gabrielle works more hours on a particular cake and Joseph less, or vice versa, with no obvious

change in the quality of the cake.

During the month of May, the bakery produces 50 cakes. Actual direct manufacturing labor costs are as follows:

Gabrielle (140 hours) $ 3,500

Joseph (165 hours) 2,475

Total actual direct labor cost $ 5,975

Required:

1. What is the budgeted cost of direct manufacturing labor for 50 cakes?

2. Calculate the total direct manufacturing labor price and efficiency variances.

3. For the 50 cakes, what is the total actual amount of direct manufacturing labor used? What is the actual direct manufactur –

ing labor input mix percentage? What is the budgeted amount of Gabrielle’s and Joseph’s labor that should have been used

for the 50 cakes?

4. Calculate the total direct manufacturing labor mix and yield variances. How do these numbers relate to the total direct man-

ufacturing labor efficiency variance? What do these variances tell you?

SOLUTION

(35 min.) Direct manufacturing labor variances: price, efficiency, mix and yield

1.

Gabrielle ($25 × 3 hrs.) $ 75

2. Solution Exhibit 7-44A presents the total price variance ($0), the total efficiency variance ($25 F), and the total flexi-

ble-budget variance ($25 F).

Total direct labor price variance can also be computed as:

=

( )

Actual Budgeted

price of input price of input

–

×

Actual quantity

of input

Total direct labor efficiency variance can also be computed as:

=

( )

Actual quantity Budgeted quantity of input

of input allowed for actual output

–

×

Budgeted

price of input

Direct labor

price

variance for

Direct labor

efficiency

variance for

Total direct labor efficiency variance $ 25 F

SOLUTION EXHIBIT 7-44A

Columnar Presentation of Direct Labor Price and Efficiency Variances for Elena Martinez Wedding Cakes

Actual Costs

Incurred

(Actual Input Quantity

× Actual Price)

(1)

Actual Input Quantity

× Budgeted Price

(2)

Flexible Budget

(Budgeted Input Quantity

Allowed for Actual Output

× Budgeted Price)

(3)

Total price variance

Total flexible-budget variance

3.

Actual Quan-

tity

of Input

Actual

Mix

Budgeted Quantity

of Input for Actual Output

Budgeted

Mix

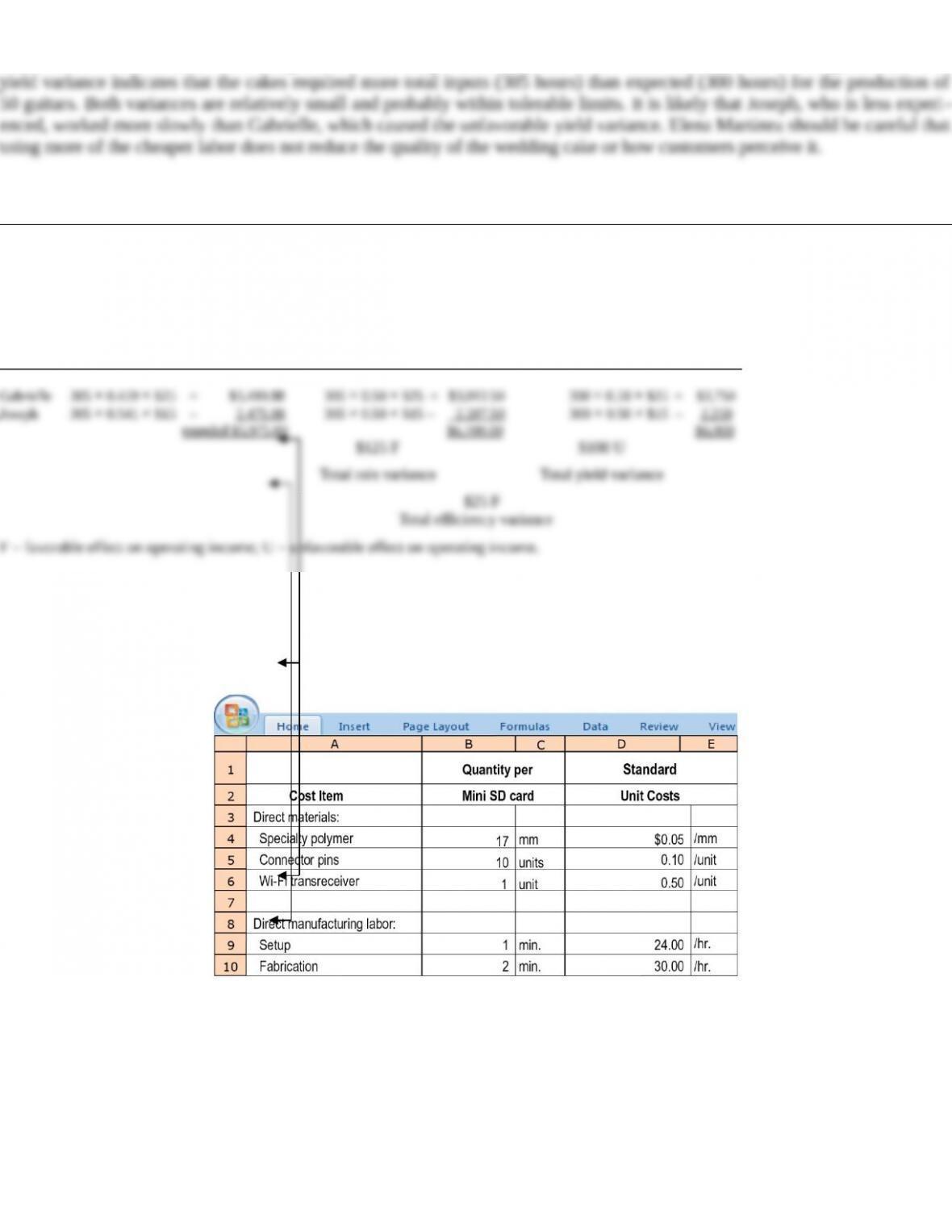

Gabrielle 140 hours 45.9% 3 hours × 50 units = 150 hours 50%

4. Solution Exhibit 7-44B presents the total direct labor yield and mix variances for Elena Martinez Wedding Cakes.

The total direct labor yield variance can also be computed as the sum of the direct labor yield variances for each input:

=×

×

The total direct labor mix variance can also be computed as the sum of the direct labor mix variances for each input:

=×

×

Direct

labor

yield

Actual

total

quantity

of all

Budgeted total

quantity of all

direct labor inputs

–

Budgeted

direct

labor input

Budgeted

price of

direct

Direct

labor

mix

Actual

direct

labor

input mix

Budgeted

direct

labor

–Actual

total

quantity of

Budgeted

price of

direct

The sum of the direct labor mix variance and the direct labor yield variance equals the direct labor efficiency variance. The fa-

vorable mix variance arises from using more of the cheaper labor (and less of the costlier labor) than the budgeted mix. The

SOLUTION EXHIBIT 7-44B

Columnar Presentation of Direct Labor Yield and Mix Variances for Elena Martinez Wedding Cakes

Actual Total Quantity

of All Inputs Used

× Actual Input Mix

× Budgeted Price

(1)

Actual Total Quantity

of All Inputs Used

× Budgeted Input Mix

× Budgeted Price

(2)

Flexible Budget:

Budgeted Total Quantity of

All Inputs Allowed for

Actual Output ×

Budgeted Input Mix

× Budgeted Price

(3)

7-45 Direct-cost and selling price variances. MicroDisk is the market leader in the Secure Digital (SD) card industry and

sells memory cards for use in portable devices such as mobile phones, tablets, and digital cameras. Its most popular card is the

Mini SD, which it sells through outlets such as Target and Walmart for an average selling price of $8. MicroDisk has a standard

monthly production level of 420,000 Mini SDs in its Taiwan facility. The standard input quantities and prices for direct-cost in-

puts are as follows:

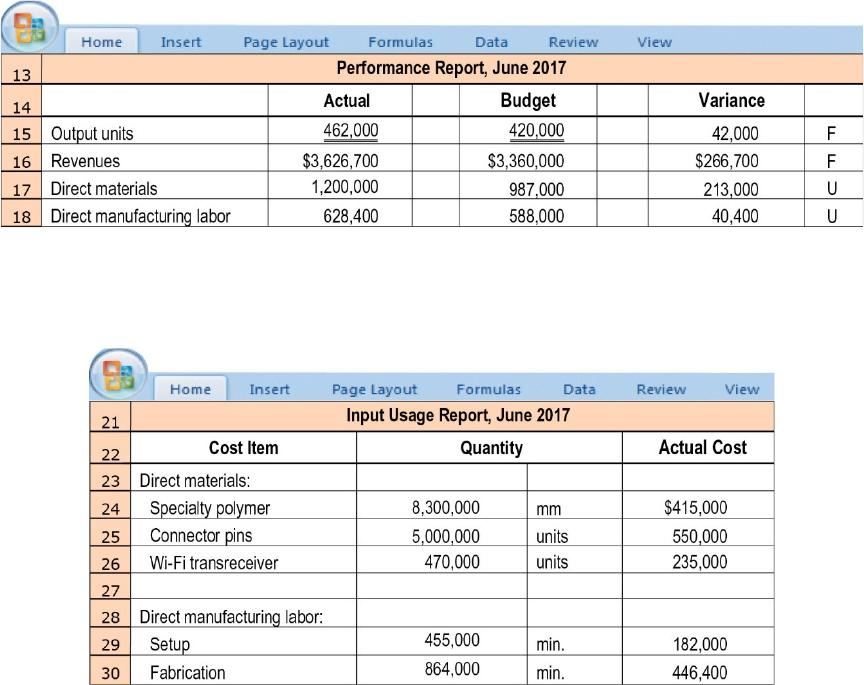

Phoebe King, the CEO, is disappointed with the results for June 2017, especially in comparison to her expectations based on

the standard cost data.

King observes that despite the significant increase in the output of Mini SDs in June, the product’s contribution to the compa-

ny’s profitability has been lower than expected. She gathers the following information to help analyze the situation:

Calculate the following variances. Comment on the variances and provide potential reasons why they might have arisen, with

particular attention to the variances that may be related to one another

Required:

1Selling-price variance

2Direct materials price variance, for each category of materials

3Direct materials efficiency variance, for each category of materials

4Direct manufacturing labor price variance, for setup and fabrication

5Direct manufacturing labor efficiency variance, for setup and fabrication