SOLUTION(40 min.) Joint-cost allocation, process further or sell.

1.

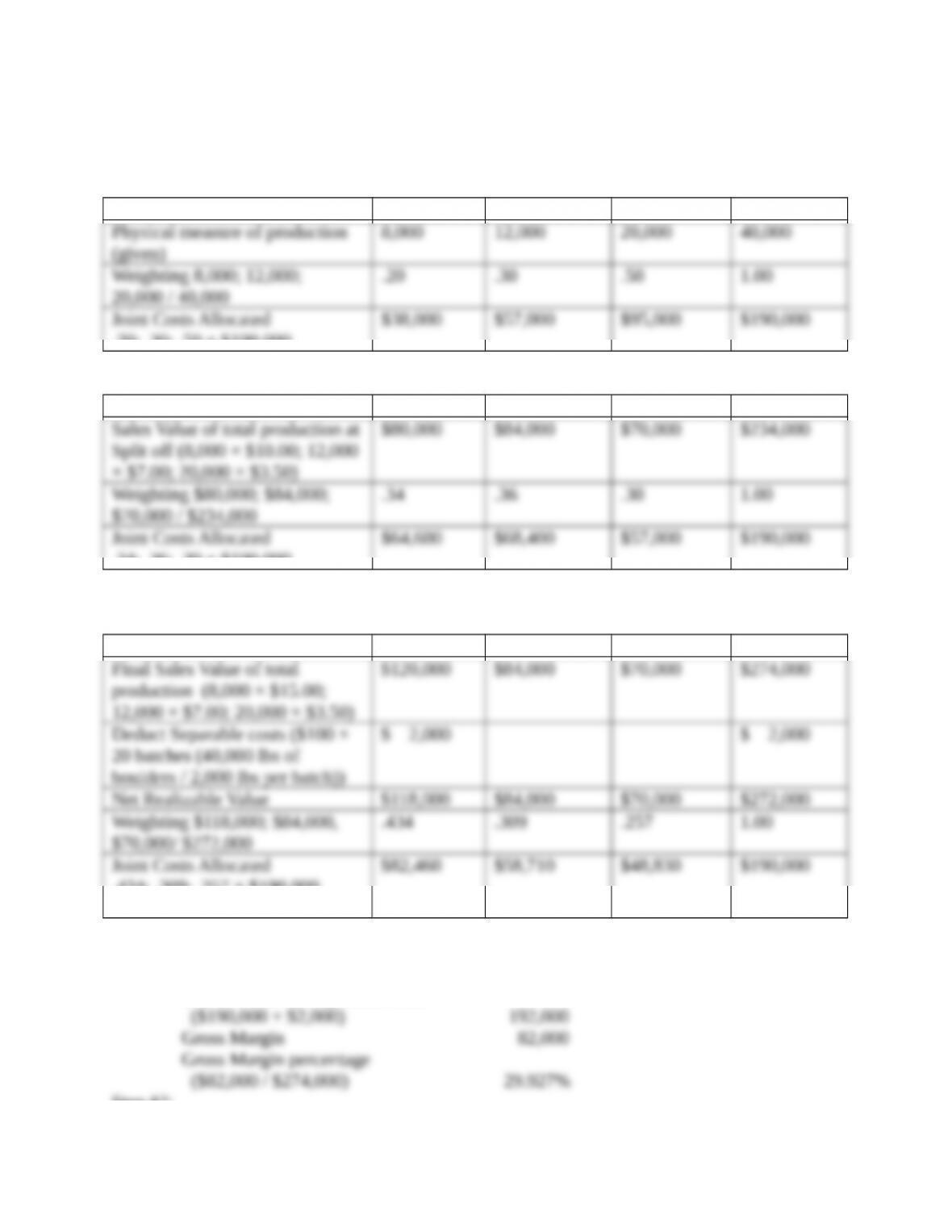

a. Physical-measure method

Red Rock White Rock Gravel Total

.20; .30; .50 × $190,000

b. Sales Value at Split off method

Red Rock White Rock Gravel Total

.34; .36; .30 × $190,000

c. Net Realizable Value method

Red Rock White Rock Gravel Total

.434; .309; .257 × $190,000

d. Constant Gross-margin Percentage NRV method Final sales value of total production

$274,000

Deduct Joint and separable costs

Step #2:

e. Summary of joint product cost allocations for Mr. Green

2. The physical measure method allocates joint costs to joint products produced during the

account period on the basis of a comparable physical measure. MCC uses the weight of the

The sales value at splitoff method is generally considered to be the preferred method.

This method allocates joint costs to joint products produced based on the relative total sales

The net realizable value method allocates the joint costs to joint products based on their

relative net realizable value. The NRV method takes into account any additional processing to

The constant gross-margin NRV method allocates joint costs to joint products produced

in a manner where each joint product is assumed to achieve an identical gross-margin percentage

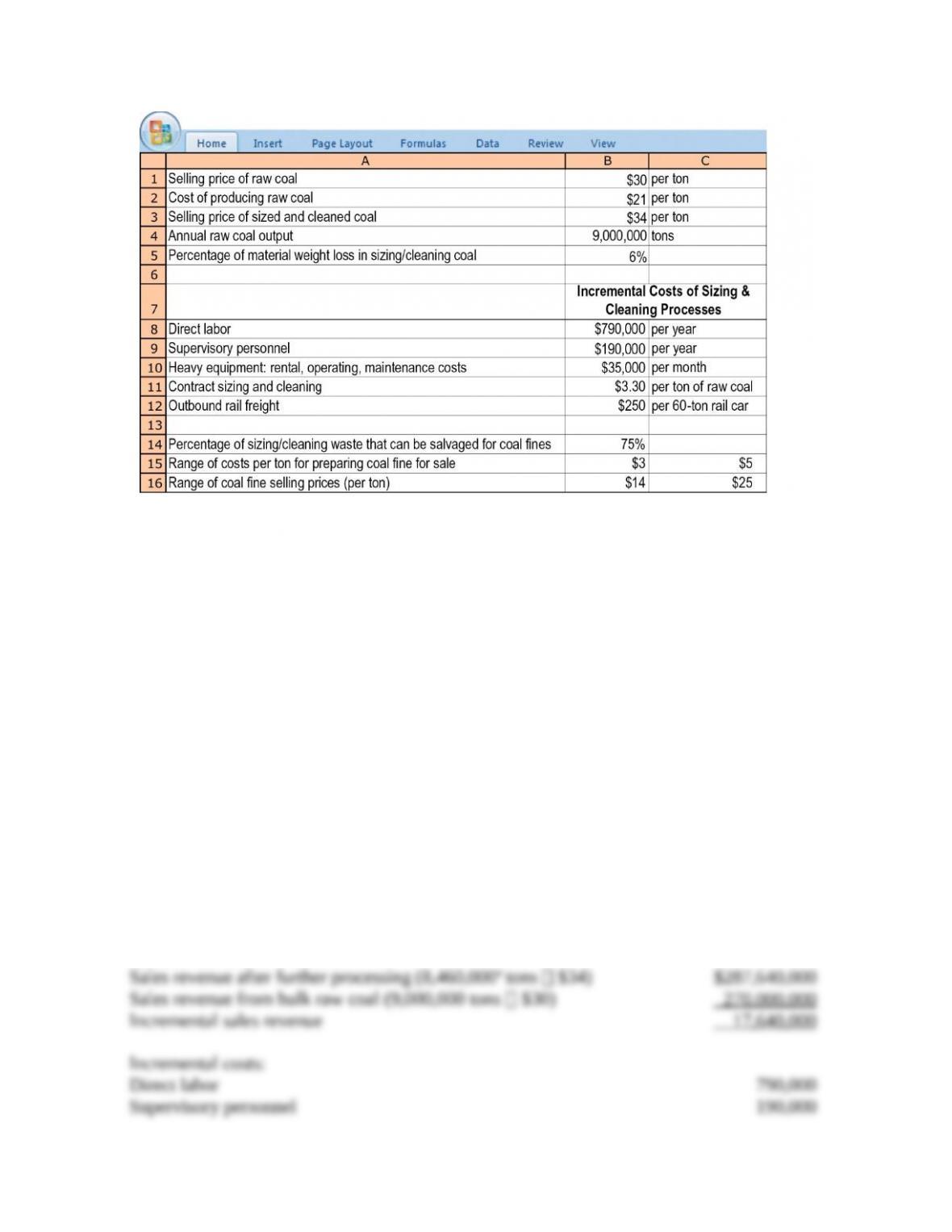

16-41 Process further or sell, byproduct. (CMA, adapted) Newcastle Mining Company

(NMC) mines coal, puts it through a one-step crushing process, and loads the bulk raw coal onto

river barges for shipment to customers.

NMC’s management is currently evaluating the possibility of further processing the raw coal

by sizing and cleaning it and selling it to an expanded set of customers at higher prices. The

option of building a new sizing and cleaning plant is ruled out as being financially infeasible.

Instead, Amy Kimbell, a mining engineer, is asked to explore outside-contracting arrangements

for the cleaning and sizing process. Kimbell puts together the following summary:

Kimbell also learns that 75% of the material loss that occurs in the cleaning and sizing process

can be salvaged as coal fines, which can be sold to steel manufacturers for their furnaces. The

sale of coal fines is erratic and NMC may need to stockpile them in a protected area for up to one

year. The selling price of coal fines ranges from $14 to $25 per ton and costs of preparing coal

fines for sale range from $3 to $5 per ton.

Required:

1. Prepare an analysis to show whether it is more profitable for NMC to continue selling raw

bulk coal or to process it further through sizing and cleaning. (Ignore coal fines in your

analysis.)

2. How would your analysis be affected if the cost of producing raw coal could be held down to

$20 per ton?

3. Now consider the potential value of the coal fines and prepare an addendum that shows how

their value affects the results of your analysis prepared in requirement 1.

SOLUTION

(40 min.) Process further or sell, byproduct.

1. The analysis shown below indicates that it would be more profitable for Newcastle Mining

Company to continue to sell bulk raw coal without further processing. This analysis ignores any

value related to coal fines. It also assumes that the costs of loading and shipping the bulk raw

coal on river barges will be the same whether Newcastle sells the bulk raw coal directly or

processes it further.

Incremental sales revenues:

a 9,000,000 tons (1– 0.06)

2. The cost of producing the raw coal is irrelevant to the decision to process further or not. As

we see from requirement 1, the cost of producing raw coal does not enter any of the calculations

3. The potential revenue from the coal fines byproduct would result in additional revenue

ranging between $5,670,000 (at a market price of $14) and $10,125,000 (at a market price of

$25).

Potential incremental income from preparing and selling the coal fines:

Minimum Maximum

The incremental loss from sizing and cleaning the raw coal is $16,985,000 as calculated

in requirement 1. Analysis indicates that relative to selling bulk raw coal, the effect of further

Stability of the current customer market for raw coal and how it compares to the

market for sized and cleaned coal.

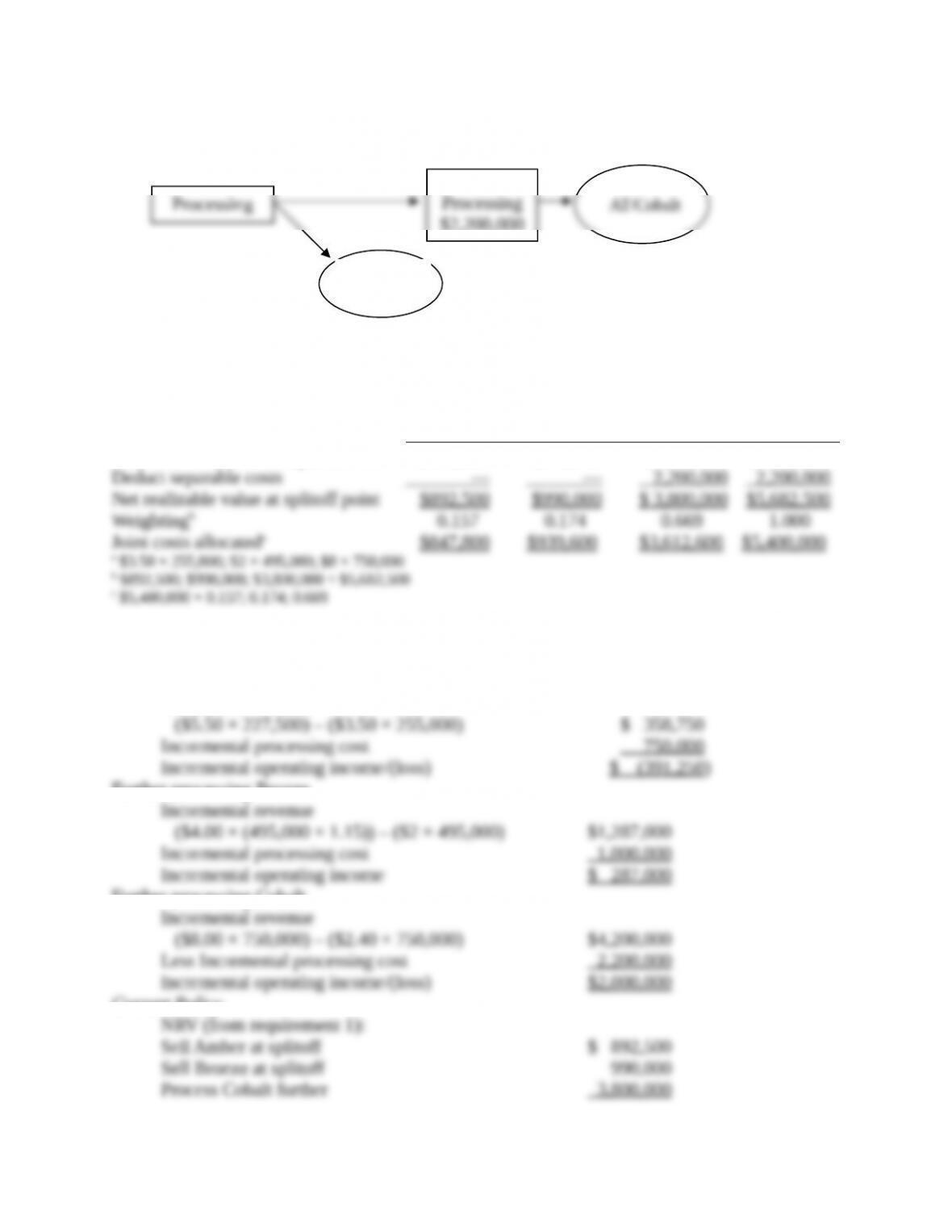

16-42 Joint-cost allocation, process further or sell. Arnold Technologies manufactures a variety

of flash memory chips at its main plant in Taiwan. Some chips are sold to makers of electronic

equipment while others are embedded into consumer products for sale under Arnold’s house label,

AT. Three of the chips that Arnold produces arise from a common production process. The first

chip, Amber, is sold to a maker of smartphones and personal computers. The second chip, Bronze,

is intended for a wireless and broadband communication firm. The third chip, Cobalt, is used to

manufacture and market a solid-state device under the AT name.

Data regarding these three products for the fiscal year ended April 30, 2017, are given below.

Amber Bronze AT with Cobalt

Units produced 255,000 495,000 750,000

Selling price per unit at

splitoff

$ 3.50 $ 2.00 —

Separable costs — — $2,200,000

Final selling price per

unit

— — $ 8.00

Arnold incurred joint product costs up to the splitoff point of $5,400,000 during the fiscal

year.

The head of Arnold, Amanda Peterson, is considering a variety of alternatives that would

potentially change the way the three products are processed and sold. Proposed changes for each

product are as follows:

■Amber chips can be incorporated into Arnold’s own memory stick. However, this additional

processing causes a loss of 27,500 units of Amber. The separable costs to further process

Amber chips are estimated to be $750,000 annually. The memory stick would sell for $5.50

per unit.

■Arnold’s R&D unit has recommended that the company process Bronze further into a 3D

vertical chip and sell it to a high-end vendor of datacenter products. The additional processing

would cost $1,000,000 annually and would result in 15% more units of product. The 3D

vertical chip sells for $4.00 per unit.

■The third chip is currently incorporated into a solid-state device under the AT name. Galaxy

Electronics has approached Arnold with an offer to purchase this chip at the splitoff point for

$2.40 per unit.

Required:

1. Allocate the $5,400,000 joint production cost to Amber, Bronze, and AT with Cobalt using the

NRV method.

2. Identify which of the three joint products Arnold should sell at the splitoff point in the future

and which of the three the company should process further to maximize operating income.

Support your decisions with appropriate computations.

SOLUTION

(30 min.) Joint-cost allocation, process further or sell.

Splitoff

Point

Amber Bronze AT/Cobalt Total

Final sales value of total productiona$892,500 $990,000 $6,000,000 $7,882,500

2.

Further processing Amber

Incremental revenue

Further processing Bronze

Further processing Cobalt

Current Policy

Processing AT/Cobalt

Amber

Bronze

Further

Processing

$2,200,000

5,682,500

Preferred Options

Arnold is $287,000 better off by changing its policy regarding Bronze – it should process it

further beyond the splitoff point.

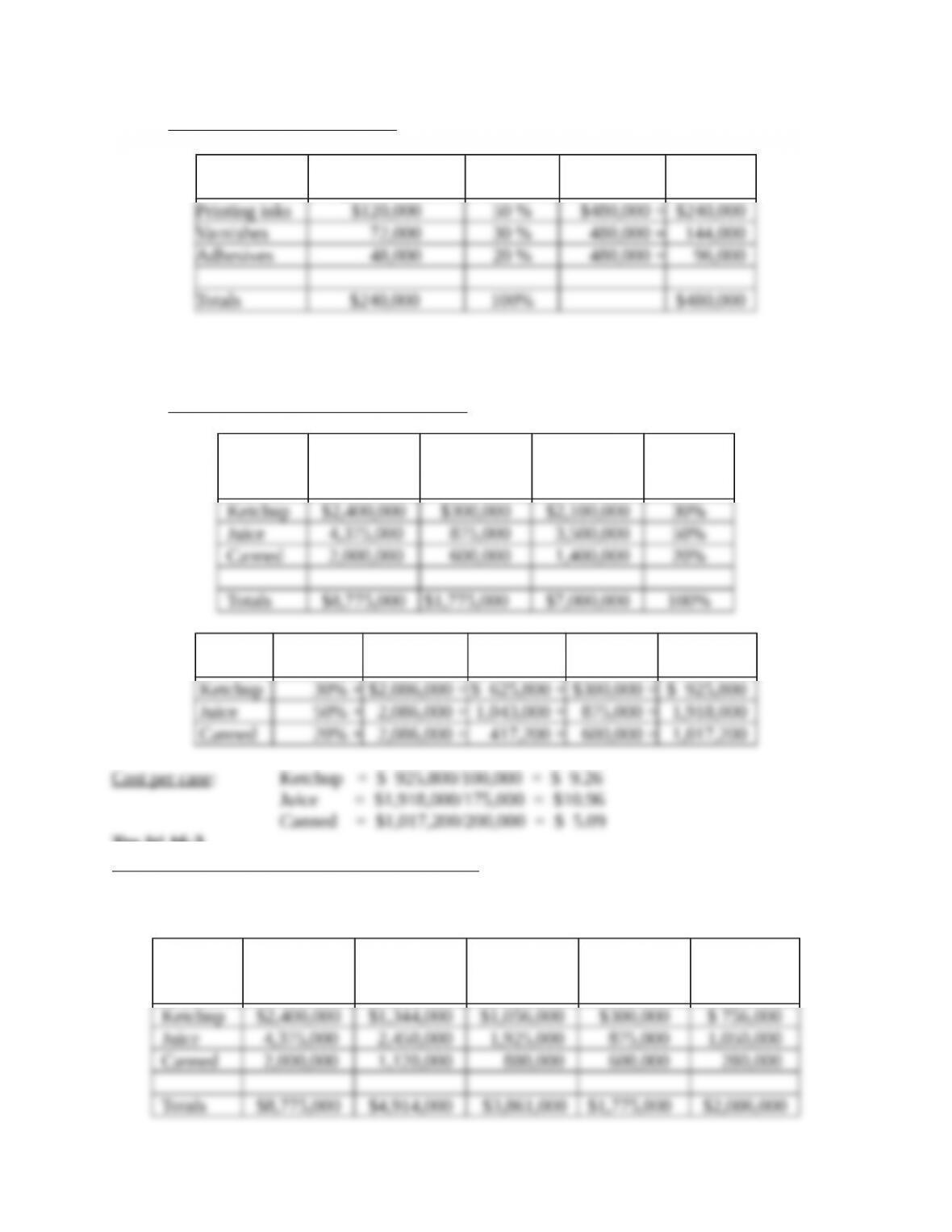

16-43 Methods of joint-cost allocation, comprehensive. Kardash Cosmetics purchases flowers

in bulk and processes them into perfume. From a certain mix of petals, the firm uses Process A to

generate Seduction, its high-grade perfume, as well as a certain residue. The residue is then further

treated, using Process B, to yield Romance, a medium-grade perfume. An ounce of residue

typically yields an ounce of Romance.

In July, the company used 25,000 pounds of petals. Costs involved in Process A, i.e.,

reducing the petals to Seduction and the residue, were:

Direct Materials – $440,000; Direct Labor – $220,000; Overhead Costs – $110,000.

The additional costs of producing Romance in Process B were:

Direct Materials – $22,000; Direct Labor – $50,000; Overhead Costs – $40,000.

During July, Process A yielded 7,000 ounces of Seduction and 49,000 ounces of residue.

From this, 5,000 ounces of Seduction were packaged and sold for $109.50 an ounce. Also,

28,000 ounces of Romance were processed in Process B and then packaged and sold for $31.50

an ounce. The other 21,000 ounces remained as residue. Packaging costs incurred were $137,500

for Seduction and $196,000 for Romance. The firm has no beginning inventory on July 1.

If it so desired, the firm could have sold unpackaged Seduction for $56 an ounce and the

residue from Process A for $24 an ounce.

Required:

1. What is the joint cost of the firm to be allocated to Seduction and Romance?

2. Under the physical measure method, how would the joint costs be allocated to Seduction and

Romance?

3. Under the sales value at splitoff method, what portion of the joint costs would be allocated to

Seduction and Romance, respectively?

4. What is the estimated net realizable value per ounce of Seduction and Romance?

5. Under the net realizable value method, what portion of the joint costs would be allocated to

Seduction and Romance, respectively?

6. What is the gross margin percentage for the firm as a whole?

7. Allocate the joint costs to Seduction and Romance under the constant gross-margin

percentage NRV method.

8. If you were the manager of Kardash Cosmetics, would you continue to process the petal

residue into Romance perfume? Explain your answer.

SOLUTION

(60 min.) Methods of joint-cost allocation, comprehensive.

1. Joint costs for Kardash include $440,000 in direct materials, $220,000 in direct labor, and

$110,000 in overhead costs, for a total of $770,000.

2. At splitoff, the relative weights of the two perfumes are 7,000 ounces of Seduction and

49,000 ounces of Romance (in the form of residue) respectively. Accordingly, the allocation of

joint costs under the physical measure method would be in the ratio of 1:7, or as follows:

7$770,000

8

æ ö´

ç ÷

è ø

3. The relative sales values of production at splitoff are as follows:

The ratio of the sales values is 392:1176, or 1:3. Accordingly, the joint costs are allocated as:

æ ö´

ç ÷

è ø

bSales Value at Splitoff Method:

Product Sales Value at

Splitoff Point Percentage Joint Costs Allocated

Try It! 16-2

Estimated Net Realizable Value Method:

Product Final Sales

Value

Separable

Costs

Net

Realizable

Value

Percentage

Product Percentage Joint Costs Allocated Separable

Costs

Product

Costs

Try It! 16-3

Constant Gross-Margin Percentage NRV Method:

The overall gross margin is the difference between the total estimated net realizable value

($7,000,000) and the joint costs ($2,086,000), or $4,914,000.

The gross margin percentage is $4,914,000/$8,775,000 = 56%.

Product Final Sales

Value

Less Gross

Margin

Total

Production

Costs

Less

Separable

Costs

Joint Costs

Allocated

Try It! 16-4

Production

Method

Sales

Method

Revenues

(4,680/26,000) × $557,500 = $100,350