CHAPTER 8

FLEXIBLE BUDGETS, OVERHEAD COST VARIANCES, AND

MANAGEMENT CONTROL

8-1 How do managers plan for variable overhead costs?

Effective planning of variable overhead costs involves:

1. Planning to undertake only those variable overhead activities that add value for

8-2 How does the planning of fixed overhead costs differ from the planning of variable

overhead costs?

At the start of an accounting period, a larger percentage of fixed overhead costs are locked-in

8-3 How does standard costing differ from actual costing?

The key differences are how direct costs are traced to a cost object and how indirect costs

are allocated to a cost object:

Actual Costing Standard Costing

Direct costs Actual prices

× Actual inputs used

Standard prices

× Standard inputs allowed for actual output

8-4 What are the steps in developing a budgeted variable overhead cost-allocation rate?

Steps in developing a budgeted variable-overhead cost rate are:

1. Choose the period to be used for the budget,

8-5 What are the factors that affect the spending variance for variable manufacturing

overhead?

Two factors affecting the spending variance for variable manufacturing overhead are:

8-6 Assume variable manufacturing overhead is allocated using machine-hours. Give three

possible reasons for a favorable variable overhead efficiency variance.

Possible reasons for a favorable variable-overhead efficiency variance are:

Workers more skillful in using machines than budgeted,

8-7 Describe the difference between a direct materials efficiency variance and a variable

manufacturing overhead efficiency variance.

A direct materials efficiency variance indicates whether more or less direct materials were used

8-8 What are the steps in developing a budgeted fixed overhead rate?

Steps in developing a budgeted fixed-overhead rate are

1. Choose the period to use for the budget,

2. Select the cost-allocation base to use in allocating fixed overhead costs to output

produced,

8-9 Why is the flexible-budget variance the same amount as the spending variance for fixed

manufacturing overhead?

The relationship for fixed-manufacturing overhead variances is:

Flexible-budget variance

(never a variance)

There is never an efficiency variance for fixed overhead because managers cannot be

8-10 Explain how the analysis of fixed manufacturing overhead costs differs for (a) planning

and control and (b) inventory costing for financial reporting.

For planning and control purposes, fixed overhead costs are a lump sum amount that is not

8-11 Provide one caveat that will affect whether a production-volume variance is a good

measure of the economic cost of unused capacity.

An important caveat is what change in selling price might have been necessary to attain the level

of sales assumed in the denominator of the fixed manufacturing overhead rate. For example, the

8-12 “The production-volume variance should always be written off to Cost of Goods Sold.”

Do you agree? Explain.

A strong case can be made for writing off an unfavorable production-volume variance to cost of

goods sold. The alternative is prorating it among inventories and cost of goods sold, but this

would “penalize” the units produced (and in inventory) for the cost of unused capacity, i.e., for

the units not produced. But, if we take the view that the denominator level is a “soft” number—

8-13 What are the variances in a 4-variance analysis?

The four variances are:

Variable manufacturing overhead costs

spending variance

Fixed manufacturing overhead costs

spending variance

8-14 “Overhead variances should be viewed as interdependent rather than independent.” Give

an example.

Interdependencies among the variances could arise for the spending and efficiency variances. For

example, if the chosen allocation base for the variable overhead efficiency variance is only one

8-15 Describe how flexible-budget variance analysis can be used in the control of costs of

activity areas.

Flexible-budget variance analysis can be used in the control of costs in an activity area by

isolating spending and efficiency variances at different levels in the cost hierarchy. For example,

an analysis of batch costs can show the price and efficiency variances from being able to use

longer production runs in each batch relative to the batch size assumed in the flexible budget.

8-16 Each of the following statements is correct regarding overhead variances except:

a. Actual overhead greater than applied overhead is unfavorable.

b. The efficiency overhead variance ignores the standard variable overhead rate.

SOLUTION

Choice “b” is the right answer, as that statement is incorrect. The efficiency variance multiplies

the standard variable overhead rate by the difference between actual and standard direct labor

hours.

8-17 Steed Co. budgets production of 150,000 units in the next year. Steed’s CFO expects that

each unit will take 8 hours to produce at an hourly wage rate of $10 per hour. If factory overhead

is applied on the basis of direct labor hours at $6 per hour, the budget for factory overhead will

total:

a. $7,200,000.

SOLUTION

Choice “a” is correct. 150,000 units at 8 hours per unit is equal to 1,200,000 hours budgeted.

Factory overhead is applied at $6 per direct labor hour, so at 1,200,000 hours, factory overhead

will be equal to $7,200,000.

8-18 As part of her annual review of her company’s budgets versus actuals, Mary Gerard

isolates unfavorable variances with the hope of getting a better understanding of what caused

them and how to avoid them next year. The variable overhead efficiency variance was the most

unfavorable over the previous year, which Gerard will specifically be able to trace to:

a. Actual overhead costs below applied overhead costs.

b. Actual production units below budgeted production units.

c. Standard direct labor hours below actual direct labor hours.

d. The standard variable overhead rate below the actual variable overhead rate.

SOLUTION

Choice “c” is correct. The variable overhead efficiency variance is calculated as the difference

between actual direct labor hours used versus standard (budgeted) direct labor hours allowed,

8-19 Culpepper Corporation had the following inventories at the beginning and end of the month

of January:

January 1 January 31

Finished goods $125,000 $117,000

Work-in-process 235,000 251,000

Direct materials 134,000 124,000

The following additional manufacturing data was available for the month of January.

Direct materials purchased $189,000

Transportation in 3,000

Direct labor 400,000

Actual factory overhead 175,000

Culpepper Corporation applies factory overhead at a rate of 40% of direct labor cost, and any

overapplied or underapplied factory overhead is deferred until the end of the year.

Culpepper’s balance in its factory overhead control account at the end of January was:

1. $15,000 overapplied.

2. $15,000 underapplied.

3. $5,000 underapplied.

4. $5,000 overapplied.

SOLUTION

Choice “2” is correct.

The question asks for the amount of overapplied or underapplied overhead at the end of a month.

8-20 Fordham Corporation produces a single product. The standard costs for one unit of its

Concourse product are as follows:

Direct materials (6 pounds at $0.50 per pound) $ 3

During November Year 2, 4,000 units of Concourse were produced. The costs associated with

November operations were as follows:

What is the variable overhead efficiency variance for Concourse for November Year 2?

1. $2,000 favorable.

2. $1,000 favorable.

3. $2,000 unfavorable.

4. $1,000 unfavorable.

SOLUTION

Choice “4” is correct.

The question asks for the variable overhead efficiency variance for a product.

8-21 Variable manufacturing overhead, variance analysis. Esquire Clothing is a

manufacturer of designer suits. The cost of each suit is the sum of three variable costs (direct

material costs, direct manufacturing labor costs, and manufacturing overhead costs) and one

fixed-cost category (manufacturing overhead costs). Variable manufacturing overhead cost is

allocated to each suit on the basis of budgeted direct manufacturing labor-hours per suit. For

June 2017, each suit is budgeted to take 4 labor-hours. Budgeted variable manufacturing

overhead cost per labor-hour is $12. The budgeted number of suits to be manufactured in June

2017 is 1,040.

Actual variable manufacturing costs in June 2017 were $52,164 for 1,080 suits started and

completed. There were no beginning or ending inventories of suits. Actual direct manufacturing

labor-hours for June were 4,536.

Required:

1. Compute the flexible-budget variance, the spending variance, and the efficiency variance for

variable manufacturing overhead.

2. Comment on the results.

SOLUTION

(20 min.) Variable manufacturing overhead, variance analysis.

1. Variable Manufacturing Overhead Variance Analysis for Esquire Clothing for June 2017

Actual Costs

Incurred

Actual Input Qty.

× Actual Rate

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

$2,268 F

$2,592 U

1 & 2.

Budgeted fixed overhead

rate per unit of

allocation base

=

4040,1

400,62$

=

160,4

400,62$

= $15 per hour

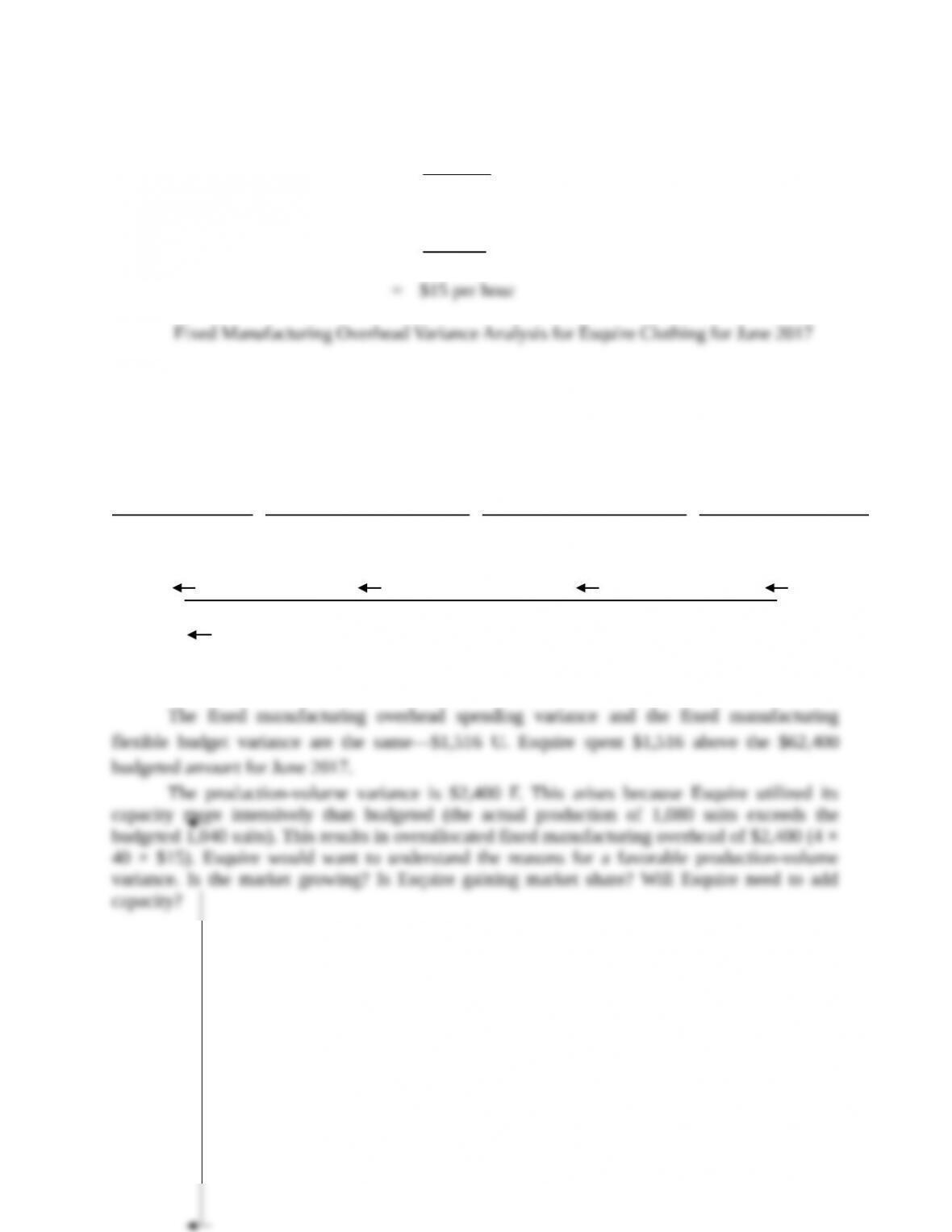

Fixed Manufacturing Overhead Variance Analysis for Esquire Clothing for June 2017

Actual Costs

Incurred

(1)

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(2)

Flexible Budget:

Same Budgeted

Lump Sum

(as in Static Budget)

Regardless of

Output Level

(3)

Allocated:

Budgeted Input Qty.

Allowed for Actual

Output

× Budgeted Rate

(4)

$63,916 $62,400 $62,400

(4 × 1,080 × $15)

$64,800

$1,516 U $2,400 F

Spending variance Never a variance Production-volume variance

$1,516 U $2,400 F

Flexible-budget variance Production-volume variance

8-23 Variable manufacturing overhead variance analysis. The Sourdough Bread Company

bakes baguettes for distribution to upscale grocery stores. The company has two direct-cost

categories: direct materials and direct manufacturing labor. Variable manufacturing overhead is

allocated to products on the basis of standard direct manufacturing labor-hours. Following is

some budget data for the Sourdough Bread Company:

Direct manufacturing labor use 0.02 hours per baguette

Variable manufacturing overhead $10.00 per direct manufacturing labor-hour

The Sourdough Bread Company provides the following additional data for the year ended

December 31, 2017:

Planned (budgeted) output 3,100,000 baguettes

Actual production 2,600,000 baguettes

Direct manufacturing labor 46,800 hours

Actual variable manufacturing overhead $617,760

Required:

1. What is the denominator level used for allocating variable manufacturing overhead? (That is,

for how many direct manufacturing labor-hours is Sourdough Bread budgeting?)

2. Prepare a variance analysis of variable manufacturing overhead. Use Exhibit 8-4 (page 304)

for reference.

3. Discuss the variances you have calculated and give possible explanations for them.

SOLUTION

(30 min.) Variable manufacturing overhead variance analysis.

1. Denominator level = (3,100,000 × 0.02 hours) = 62,000 hours

2. Actual

Results

Flexible

Budget Amounts

´

Variable Manufacturing Overhead Variance Analysis for Sourdough Bread Company for 2017:

Actual Costs

Incurred

Actual Input Qty.

× Actual Rate

(1)

Actual Input Qty.

× Budgeted Rate

(2)

Flexible Budget:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(3)

Allocated:

Budgeted Input Qty.

Allowed for

Actual Output

× Budgeted Rate

(4)

(46,800 × $13.20)

(46,800 × $10)

(52,000 × $10)

(52,000 × $10)

Spending variance

Efficiency variance Never a variance