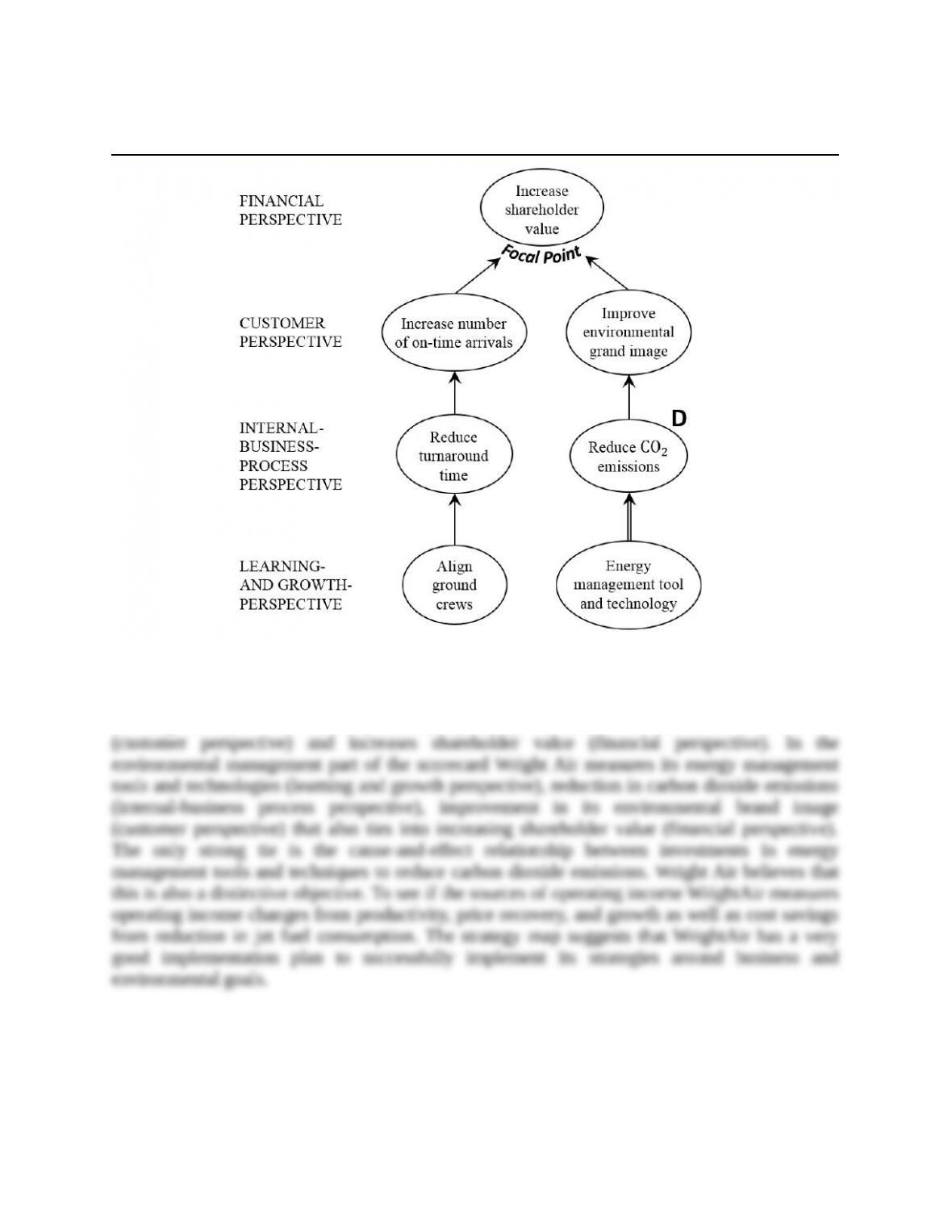

SOLUTION EXHIBIT 12-42A

Strategy Map for WrightAir

On the business side of the balanced scorecard, WrightAir measures the motivation of

ground crew (learning and growth perspective) that helps to reduce turnaround time of the planes

on the ground (internal business process perspective), increases the number of on-time arrivals

3. Normally, the price recovery component indicates that a company has been successful in

differentiating its product or service to command a price premium so that the prices of outputs

rise faster than the prices of inputs. For WrightAir, the price recovery component measures the

12-+

4. I would not have included customer-service measures in WrightAir’s customer

perspective because it is not part of WrightAir’s strategy. WrightAir does not compete with other

5. Yes, WrightAir should include some measure of employee satisfaction and employee

training in the learning and growth perspective. WrightAir’s low-cost strategy is based on

efficiency. The key to good, fast, and friendly customer service is well trained and satisfied

6. WrightAir included social and environmental performance measures in its balanced

scorecard because it believes strong environmental and social performance gives it a competitive

advantage by (1) attracting and inspiring outstanding employees, (2) enhancing its reputation

Following the concept of shared value, Smooth Air includes social and environmental

measures (together with business goals and measures) in its balanced scorecard to evaluate how

well it is doing toward achieving its social and environmental goals. The balanced scorecard

indicates that WrightAir’s social and environmental initiatives are by and large succeeding.

12-+

Not all companies believe in implementing sustainability goals, but those that do find the

12-43 Partial-productivity measurement. Gable Company manufactures wallets from fabric.

In 2016, Gable made 2,160,000 wallets using 1,600,000 yards of fabric. In 2016, Gable has

capacity to make 2,448,000 wallets and incurs a cost of $8,568,000 for this capacity. In 2017,

Gable plans to make 2,203,200 wallets, make fabric use more efficient, and reduce capacity.

Suppose that in 2017 Gable makes 2,203,200 wallets, uses 1,440,000 yards of fabric, and

reduces capacity to 2,295,000 wallets at a cost of $7,803,000.

Required:

1. Calculate the partial-productivity ratios for materials and conversion (capacity costs) for

2017, and compare them to a benchmark for 2016 calculated based on 2017 output.

2. How can Gable Company use the information from the partial-productivity calculations?

SOLUTION

(20 min.) Partial productivity measurement.

1. Gable Company’s partial productivity ratios in 2017 are as follows:

Direct materials

partial productivity

=

Quantity of output produced in 2017

Yards of direct materials used in 2017

=

2, 203, 200

1, 440, 000

=

1.53 wallets

per yard

Conversion costs

partial productivity

=

Quantity of output produced in 2017

Units of manuf. capacity in 2017

=

2, 203, 200

2, 295, 000

=

0.96 wallets

per unit of

capacity

To compare partial productivities in 2017 with partial productivities in 2016, we first calculate

the inputs that would have been used in 2016 to produce year 2017’s 2,203,200 units of output

assuming the year 2016 relationship between inputs and outputs.

Alternatively, we can calculate direct materials that would have been used in year 2016 to produce

year 2017’s 2,203,200 output as

12-+

Partial productivity calculations for 2016 based on year 2017 output (to make the partial

productivities comparable across the two years):

Direct materials

partial productivity

=

Quantity of output produced in 2017

Yards of direct materials that would

have been used in 2016 to produce

year 2017 output

=

2, 203, 200

1, 632, 000

=

1.35 wallets

per yard

Conversion costs

partial productivity

=

Quantity of output produced in 2017

Units of manufacturing capacity

that would have been used in

2016 to produce year 2017 output

=

2, 203, 200

2, 448, 000

=

0.9 wallets per

unit of capacity

The calculations indicate that Gable improved the partial productivity of direct materials and

conversion costs between 2016 and 2017 via efficiency improvements and by reducing unused

manufacturing capacity.

2. Gable Company management can use the partial productivity measures to set targets for

the next year. Partial productivity measures can easily be compared over multiple periods. For

example, they may specify bonus payments if partial productivity of direct materials increases to

12-44 Total factor productivity (continuation of 12-43). Refer to the data for Problem 12-43.

Assume the fabric costs $4.00 per yard in 2017 and $4.10 per yard in 2016.

Required:

1. Compute Gable Company’s total factor productivity (TFP) for 2017.

2. Compare TFP for 2017 with a benchmark TFP for 2016 inputs based on 2017 prices and

output.

3. What additional information does TFP provide that partial-productivity measures do not?

12-+

SOLUTION

(25 min.) Total factor productivity (continuation of 12-43).

1.

Total factor

productivity

for 2017 using

2017 prices

=

Quantity of output produced in 2017

Costs of inputs used in 2017 based on 2017 prices

=

2,203,200

(1,440,000 $4.00) + (7,803, 000)´

=

2, 203, 200 2,203,200

$5, 760,000 $7,803,000 $13,563,000

=

+

2. By itself, the 2017 TFP of 0.16244 units per dollar of input is not particularly helpful. We

need something to compare the 2017 TFP against. We use, as a benchmark, TFP calculated using

Cost of capacity in 2017 $7,803,000

2017 price of capacity = $3.40 per unit of capacity

Capacity in 2017 2,295,000 units

= =

Benchmark

TFP

=

Quantity of output produced in 2017

Costs of inputs that would have been used in 2016

to produce 2017 output at year 2017 input prices

=

2,203,200

(1,632,000 $4.00) + (2,448,000 $3.40)´ ´

=

2,203,200

$6,528,000 + $8,323,200

=

2,203,200

$14,851,200

=0.1483516 units of output per dollar of input

12-+

Using 2017 prices, total factor productivity increased 9.5% [(0.16244 0.14835)

0.14835] from 2016 to 2017.

3. Total factor productivity increased because Gable produced more output per dollar of

input in 2017 relative to 2016, measured in both years using 2017 prices. The change in partial

Partial productivities cannot be combined to indicate the overall effect on cost as a result

of these individual improvements. The TFP measure allows managers to evaluate the change in

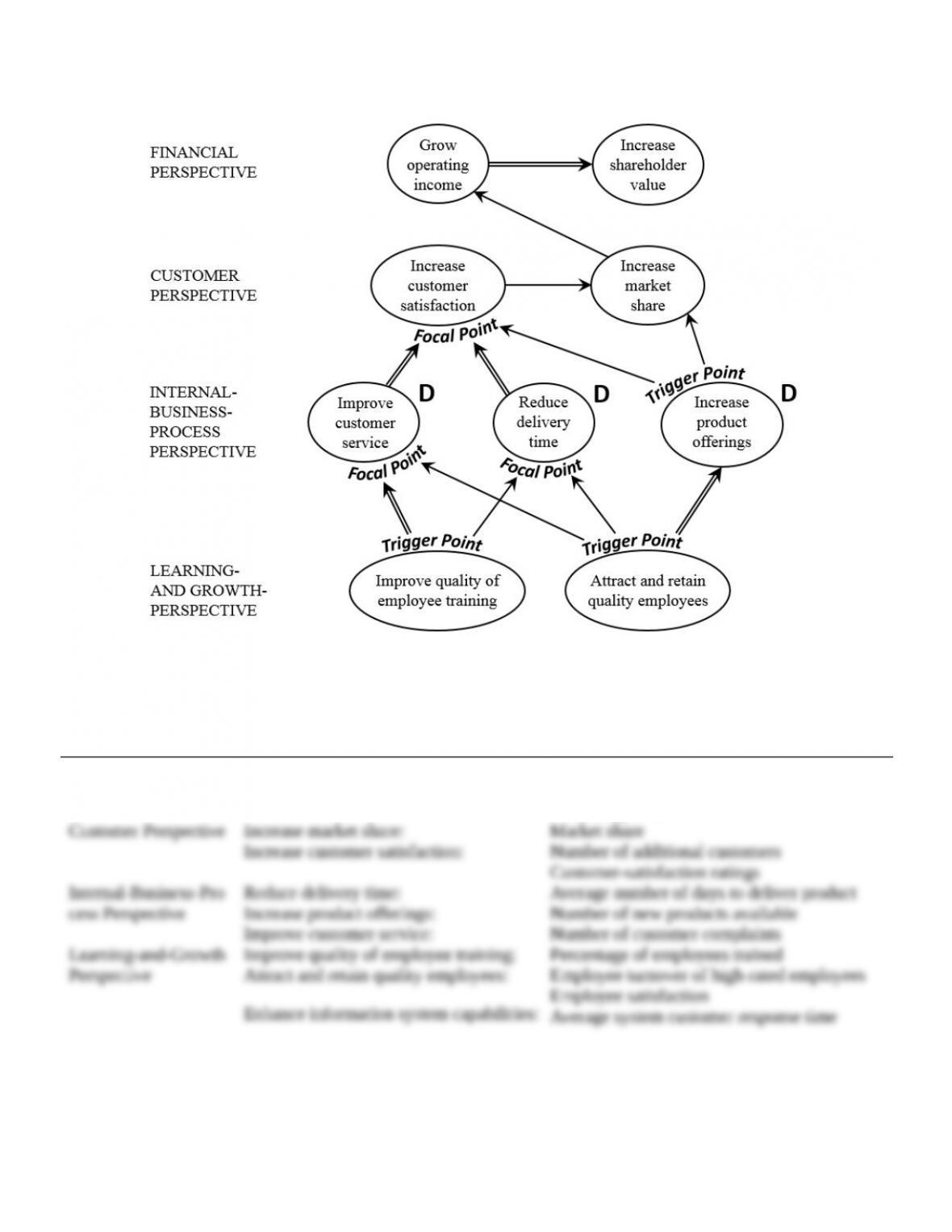

Try It 12-1 Solution

The following is Nile’s strategy map. The strong ties are indicated by bolder arrows, for example,

attracting and retaining quality employees and employee training, improving delivery time,

product offerings and customer service. Attracting and retaining quality employees and employee

training are also trigger points for improving delivery time, product offerings and customer

service. Achieving these internal business process objectives leads to higher customer

satisfaction which in turn increases market share, operating income growth and shareholder

value. The three internal business process perspectives are what make Nile distinctive. If Nile

can be better than its competitors in these perspectives, it has an excellent chance of achieving

consistent superior performance.

SOLUTION EXHIBIT TRY IT 12-1

Strategy Map for Nile Company

12-+

2. To achieve its goals, Nile includes the following measures under each perspective of the

balanced scorecard related to its strategy map:

Try It 12-2 Solution

1. Operating income for each year is as follows:

12-+

Strategic Objective Balanced Scorecard Measure

Financial Perspective Increase operating income:

Increase shareholder value:

Operating income from product differentiation

Operating income from growth

Revenue growth

2016 2017

Revenues ($3,200 400; $3,100 500) $1 ,280,000 $1 ,550,000

Costs

Engineering labor costs

The Growth Component

Revenue effect

of growth

=

Actual units Actual units of Selling

of output sold output sold price

in 2017 in 2016 in 2016

– ´

æ ö

ç ÷

ç ÷

è ø

Cost effect of

growth for

variable costs

=

Units of Actual units

input required of inputs

to produce used to

2017 output produce

in 2016 2016 ouput

–

æ ö

ç ÷

ç ÷

ç ÷

è ø

´

Input

price

in 2016

Cost effect of

growth for

fixed costs

=

Actual units of capacity in Actual

2016 because adequate units of

capacity exists to produce capacity

2017 output in 2016 in 2016

–

æ ö

ç ÷

ç ÷

è ø

×

Price per unit

of capacity

in 2016

Engineering labor-hours that would be required in 2017 to complete 500 jobs instead of the

24,000 labor-hours

500 400 jobs

jobs

æ ö

´

ç ÷

è ø

change since adequate capacity exists in 2016 to support year 2017 jobs.

The cost effects of growth component are

12-+

In summary, the net increase in operating income as a result of the growth component equals:

The Price-Recovery Component

Revenue effect of

price-recovery

()

Actual units

Selling price Selling price

= of output

in 2017 in 2016 sold in 2017

– ´

Cost effect of

price-recovery for

variable costs

=

Input Input

price in price in

2017 2016

–

æ ö

ç ÷

è ø

×

Units of input

required to

produce 2017

output in 2016

Cost effect of

price-recovery for

fixed costs

=

Price per Price per

unit of unit of

capacity capacity

in 2017 in 2016

–

æ ö

ç ÷

ç ÷

è ø

×

Actual units of capacity in

2016 because adequate

capacity exists to produce

2017 output in 2016

In summary, the net decrease in operating income as a result of the price-recovery component

equals:

The Productivity Component

Cost effect of

productivity for

variable costs

=

Actual units of Units of input

input used required to

to produce produce 2017

2017 output ouput in 2016

–

æ ö

ç ÷

ç ÷

è ø

´

Input

price

in 2017

12-+

Cost effect of

productivity for

fixed costs

=

Actual Actual units of capacity in

units of 2016 because adequate

capacity capacity exists to produce

in 2017 2017 output in 2016

–

æ ö

ç ÷

ç ÷

è ø

´

Price per

unit of

capacity

in 2017

The productivity component of cost changes are:

The change in operating income between 2016 and 2017 can be analyzed as follows:

Income

Statement

Amounts

in 2016

(1)

Revenue and

Cost Effects

of Growth

Component

in 2017

(2)

Revenue and

Cost Effects of

Price-Recovery

Component

in 2017

(3)

Cost Effect of

Productivity

Component

in 2017

(4)

Income

Statement

Amounts

in 2017

(5) =

(1) + (2) + (3) + (4)

Change in operating income

3. The analysis of operating income indicates that a significant amount of the increase in

operating income resulted from Ronaldo’s productivity improvements in 2017. The company had

Try It 12-3 Solution

Effect of industry-market-size factor on operating income

Of the 100 jobs increase in sales from 400 to 500 jobs, 10% or 40 jobs (10% 400) are due to

growth in market size, and 60 (100 40) jobs are due to an increase in market share.

The change in Ronaldo’s operating income from the industry market-size factor rather than

from specific strategic actions is:

Effect of cost leadership on operating income

12-+

The change in operating income between 2016 and 2017 can then be summarized as

Ronaldo has been very successful in implementing its cost leadership strategy. Despite the

increase in the cost of engineering labor and engineering support, Ronaldo strategically

decreased the selling price of a job by $100. That is, Ronaldo took advantage of its productivity

gains to reduce price, gain market share, and increase operating income.

Try It 12-4 Solution

1. The amount and cost of unused capacity at the beginning of year 2017 when Ronaldo makes

its capacity decisions for the year based on jobs done in year 2017 follows:

Amount of Cost of

Unused Unused

Capacity Capacity

2. Ronaldo can reduce engineering support capacity by 100 jobs from 600 jobs to 500 jobs.

Ronaldo will save 100 $320 = $32,000. This is the maximum amount of costs Ronaldo can

3. Ronaldo may have chosen not to downsize because it projects sales increases in the near term

12-+