SOLUTION

(30 min.) Price and efficiency variances, journal entries.

1. Direct materials and direct manufacturing labor are analyzed in turn:

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

Direct

Materials

(100,000 × $4.65a)

$465,000

Purchases Usage

(100,000 × $4.50) (98,055 × $4.50)

$450,000 $441,248

(9,850 × 10 × $4.50)

$443,250

2. Direct Materials Control 450,000

Direct Materials Price Variance 15,000

Accounts Payable or Cash Control 465,000

3. Some students’ comments will be immersed in conjecture about higher prices for

materials, better quality materials, higher grade labor, better efficiency in use of materials, and so

forth. A possibility is that approximately the same labor force, paid somewhat more, is taking

slightly less time with better materials and causing less waste and spoilage.

4. The purchasing point is where responsibility for price variances is found most often. The

production point is where responsibility for efficiency variances is found most often. The

7-30 Materials and manufacturing labor variances, standard costs. Dawson, Inc., is a pri-

vately held furniture manufacturer. For August 2017, Dawson had the following standards for one

of its products, a wicker chair:

Standards per Chair

Direct materials 3 square yards of input at $5.50 per square

yard

Direct manufacturing labor 0.5 hour of input at $10.50 per hour

The following data were compiled regarding actual performance: actual output units (chairs) pro-

duced, 2,200; square yards of input purchased and used, 6,200; price per square yard, $5.70; direct

manufacturing labor costs, $9,844; actual hours of input, 920; labor price per hour, $10.70.

1. Show computations of price and efficiency variances for direct materials and direct manufac-

turing labor. Give a plausible explanation of why each variance occurred.

2. Suppose 8,700 square yards of materials were purchased (at $5.70 per square yard), even

though only 6,200 square yards were used. Suppose further that variances are identified at

their most timely control point; accordingly, direct materials price variances are isolated and

traced at the time of purchase to the purchasing department rather than to the production de-

partment. Compute the price and efficiency variances under this approach.

SOLUTION

(2030 min.) Materials and manufacturing labor variances, standard costs.

1. Direct Materials

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

(6,200 sq. yds. × $5.70)

$35,340

(6,200 sq. yds. × $5.50)

$34,100

(2,200 × 3 × $5.50)

(6,600 sq. yds. × $5.50)

$36,300

The unfavorable materials price variance may be unrelated to the favorable materials

efficiency variance. For example, (a) the purchasing officer may be less skillful than assumed in

the budget, or (b) there was an unexpected increase in materials price per square yard due to

Direct Manufacturing Labor

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted Price)

(920 hrs. × $10.70)

$9,844

(920 hrs. × $10.50)

$9,660

(2,200 × 0.5 × $10.50)

(1,100 hrs. × $10.50)

$11,550

The unfavorable labor price variance may be due to, say, (a) an increase in labor rates due

to a booming economy, or (b) the standard being set without detailed analysis of labor

2.

Control

Point

Actual Costs

Incurred

(Actual Input Qty.

× Actual Price)

Actual Input Qty.

× Budgeted Price

Flexible Budget

(Budgeted Input

Qty. Allowed for

Actual Output

× Budgeted

Price)

Purchasing (8,700 sq. yds.× $5.70)

$49,590

(8,700 sq. yds. × $5.50)

$47,850

$1,740 U

7-31 Journal entries and T-accounts (continuation of 7-30). Prepare journal

entries and post them to T-accounts for all transactions in Exercise 7-30, including requirement 2.

Summarize how these journal entries differ from the normal-costing entries described in Chapter 4,

pages 120–123.

SOLUTION

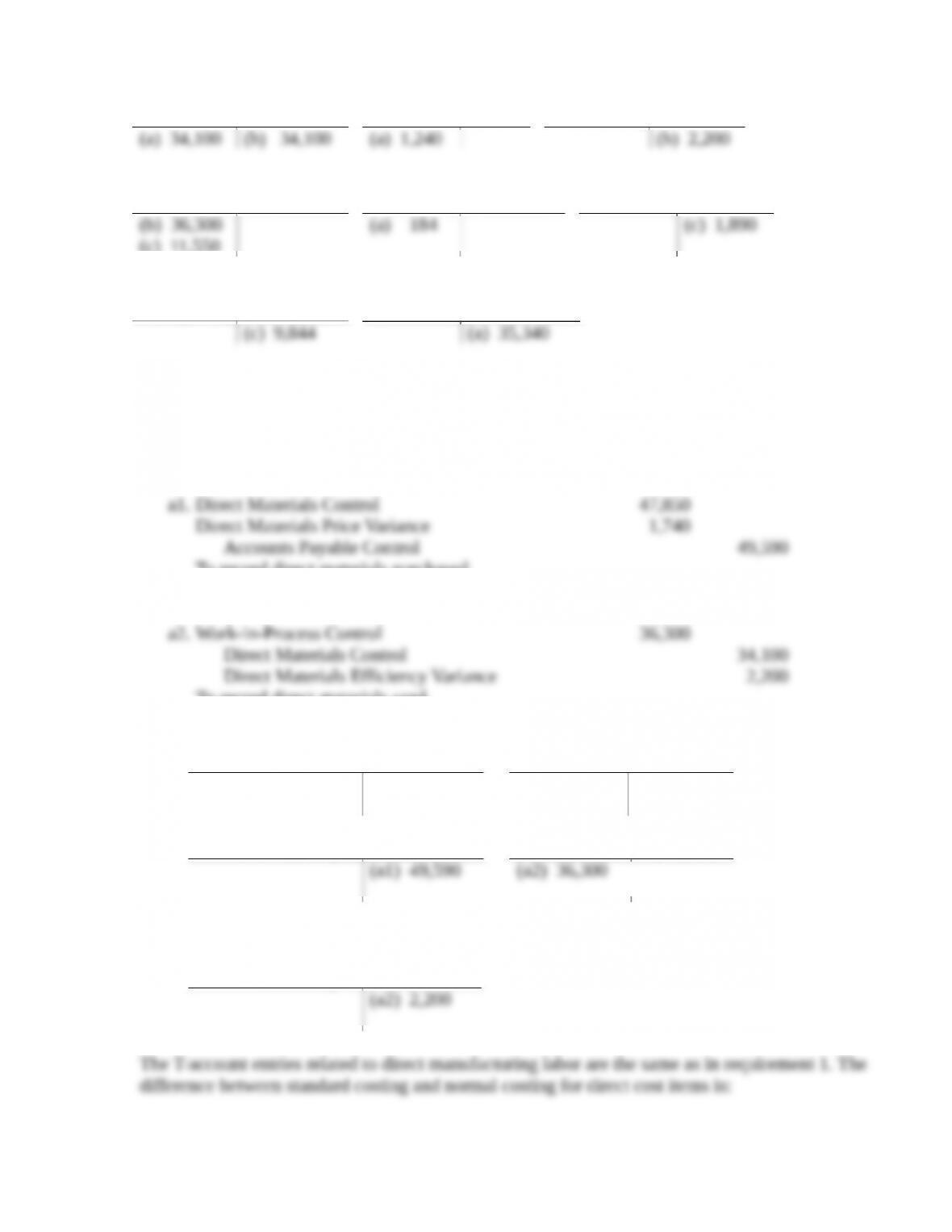

(2025 min.) Journal entries and T-accounts (continuation of 7-30).

For requirement 1 from Exercise 7-30:

a. Direct Materials Control 34,100

b. Work-in-Process Control 36,300

c. Work-in-Process Control 11,550

Direct Manufacturing Labor Price Variance 184

Direct

Materials Control

Direct Materials

Price Variance

Direct Materials

Efficiency Variance

Work-in-Process Control

Direct Manufacturing

Labor Price Variance

Direct Manuf. Labor

Efficiency Variance

(c) 11,550

Wages Payable Control Accounts Payable Control

For requirement 2 from Exercise 7-30:

The following journal entries pertain to the measurement of price and efficiency variances when

8,700 sq. yds. of direct materials are purchased:

To record direct materials purchased.

To record direct materials used.

Direct

Materials Control

Direct Materials

Price Variance

(a1) 47,850 (a2) 34,100 (a1) 1,740

Accounts Payable Control Work-in-Process Control

Direct Materials

Efficiency Variance

Standard Costs Normal Costs

Direct Costs Standard price(s)

× Standard input

Actual price(s)

× Actual input

These journal entries differ from the normal costing entries because Work-in-Process Control is

no longer carried at “actual” costs. Furthermore, Direct Materials Control is carried at standard

unit prices rather than actual unit prices. Finally, variances appear for direct materials and direct

manufacturing labor under standard costing but not under normal costing.

7-32 Price and efficiency variances, benchmarking. Nantucket Enterprises manufactures in-

sulated cold beverage cups printed with college and corporate logos, which it distributes nationally

in lots of 12 dozen cups. In June 2017, Nantucket produced 5,000 lots of its most popular line of

cups, the 24-ounce lidded tumbler, at each of its two plants, which are located in Providence and

Amherst. The production manager, Shannon Bryant, asks her assistant, Joel Hudson, to find out the

precise per-unit budgeted variable costs at the two plants and the variable costs of a competitor,

Beverage Mate, who offers similar-quality tumblers at cheaper prices. Hudson pulls together the fol-

lowing information for each lot:

Per lot Providence Plant Amherst Plant Beverage Mate

Direct materials 74 lbs. @ $3.20 per lb. 76.5 lbs. @ $3.10 per

lb.

70 lbs. @ $2.90 per lb.

Direct manufacturing

labor

2.5 hrs. @ $12.00 per

hr.

2.4 hrs. @ $12.20 per

hr.

2.4 hrs. @ $10.50 per hr.

Variable overhead $20 per lot $22 per lot $20 per lot

Required:

1. What is the budgeted variable cost per lot at the Providence Plant, the Amherst Plant, and at

Beverage Mate?

2. Using the Beverage Mate data as the standard, calculate the direct materials and direct manu-

facturing labor price and efficiency variances for the Providence and Amherst plants.

3. What advantage does Nantucket get by using Beverage Mate’s benchmark data as standards

in calculating its variances? Identify two issues that Bryant should keep in mind in using the

Beverage Mate data as the standards.

SOLUTION

(25 min.) Price and efficiency variances, benchmarking.

1.

Providence Plant

Prices and quantities Cost per lot

Direct materials 74.0 lbs @ $ 3.20 per lb $236.80

Direct labor 2.5 hrs @ $12.00 per hr 30.00

Amherst Plant

Prices and quantities Cost per lot

Direct materials 76.50 lbs @ $ 3.10 per lb $237.15

Beverage Mate

Prices and quantities Cost per lot

Direct materials 70.00 lbs @ $ 2.90 per lb $203.00

2. Providence Plant

Actual

Quantity

´

Actual Price Budgeted Efficiency

Results Variance Price Variance

(1) (2) = (1) – (3)

(4) = (3) – (5) (5)

Lots 5,000 5,000

Direct materials $1,184,000 $111,000 U $1,073,000b$58,000 U $1,015,000

´

´

Amherst Plant

Actual

Quantity

´

Actual Price Budgeted Efficiency Flexible

Results Variance Price Variance Budgeta

(1) (2) = (1) – (3)

(4) = (3) – (5) (5)

Lots 5,000 5,000

Direct Materials $1,185,750 $76,500 U $1,109,250b$8,800 U $1,015,000

´

´

3. Using an objective, external benchmark, like that of a competitor, will preempt the possibility

of any one plant feeling that the other is being favored. That this competitor, Beverage Mate, is

successful will also put positive pressure on the two plants to improve (note that all variances are

zero or unfavorable). Issues that Bryant should keep in mind include the following:

Ensure that Beverage Mate is indeed the best and most relevant standard (for exam-

ple, is there another competitor in the marketplace which should be considered?)

Ensure that the data is reliable

7-33 Static and flexible budgets, service sector. Student Finance (StuFi) is a start-up that aims

to use the power of social communities to transform the student loan market. It connects participants

through a dedicated lending pool, enabling current students to borrow from a school’s alumni com-

munity. StuFi’s revenue model is to take an upfront fee of 40 basis points (0.40%) each from the

alumni investor and the student borrower for every loan originated on its platform.

StuFi hopes to go public in the near future and is keen to ensure that its financial results are in

line with that ambition. StuFi’s budgeted and actual results for the third quarter of 2017 are presented

below.

Required:

1. Prepare StuFi’s static budget of operating income for the third quarter of 2017.

2. Prepare an analysis of variances for the third quarter of 2017 along the lines of Exhibit 7-2;

identify the sales volume and flexible budget variances for operating income.

3. Compute the professional labor price and efficiency variances for the third quarter of 2017.

4. What factors would you consider in evaluating the effectiveness of professional labor in the

third quarter of 2017?