Work in process inventory

SOLUTION

(35 min.) General ledger relationships, under- and overallocation.

The solution assumes all materials used are direct materials. A summary of the T-accounts for

Southwick Company before adjusting for under- or overallocation of overhead follows:

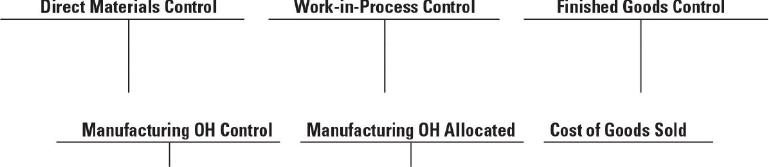

Direct Materials Control Work-in-Process Control

1-1-2017 42,000

Material used for

1-1-2017 82,000

Transferred to

Manuf. overhead

Finished Goods Control Cost of Goods Sold

1-1-2017 105,000

Cost of goods

Finished goods

Manufacturing Overhead Control Manufacturing Overhead Allocated

Manufacturing

Manufacturing

1. From Direct Materials Control T-account,

2. Direct manufacturing labor-hours =

Direct manufacturing labor costs

Direct manufacturing wage rate per hour

Manufacturing overhead

allocated

=

Direct manufacturing

labor hours

Manufacturing

overhead rate

3. From the debit entry to Finished Goods T-account,

4. From Work-in-Process T-account,

5. From the credit entry to Finished Goods Control T-account, Cost of goods sold (before

6.

Manufacturing overhead

underallocated

=

Debits to Manufacturing

Overhead Control

–

Credit to Manufacturing

Overhead Allocated

=$425,000 – $380,000

= $45,000 underallocated

7. a. Write-off to Cost of Goods Sold will increase (debit) Cost of Goods Sold by $45,000.

b. Proration based on ending balances (before proration) in Work in Process, Finished

Account balances in each account after proration follows:

Account

(1)

Account Balance

(Before Proration)

(2)

Proration of $45,000

Underallocated

Manufacturing Overhead

(3)

Account Balance

(After Proration)

(4) = (2) + (3)

Work in Process $ 190,000

(19%)

0.19 $45,000 = $ 8,550 $ 198,550

00%

8. Keezel’s operating income using write-off to Cost of Goods Sold and Proration based on

ending balances (before proration) follows:

Write-off to Proration Based

Cost of Goods Sold on Ending Balances

Revenues $1,550,000 $1,550,000

9. If the purpose is to report the most accurate inventory and cost of goods sold figures, the

preferred method is to prorate based on the manufacturing overhead allocated component in the

inventory and cost of goods sold accounts. Proration based on the balances in Work in Process,

will lead to an operating loss. Proration based on the balances in Work in Process, Finished

Goods, and Cost of Goods Sold will help Keezel avoid the loss and show an operating income.

The main merit of the write-off to Cost of Goods Sold method is its simplicity. However,

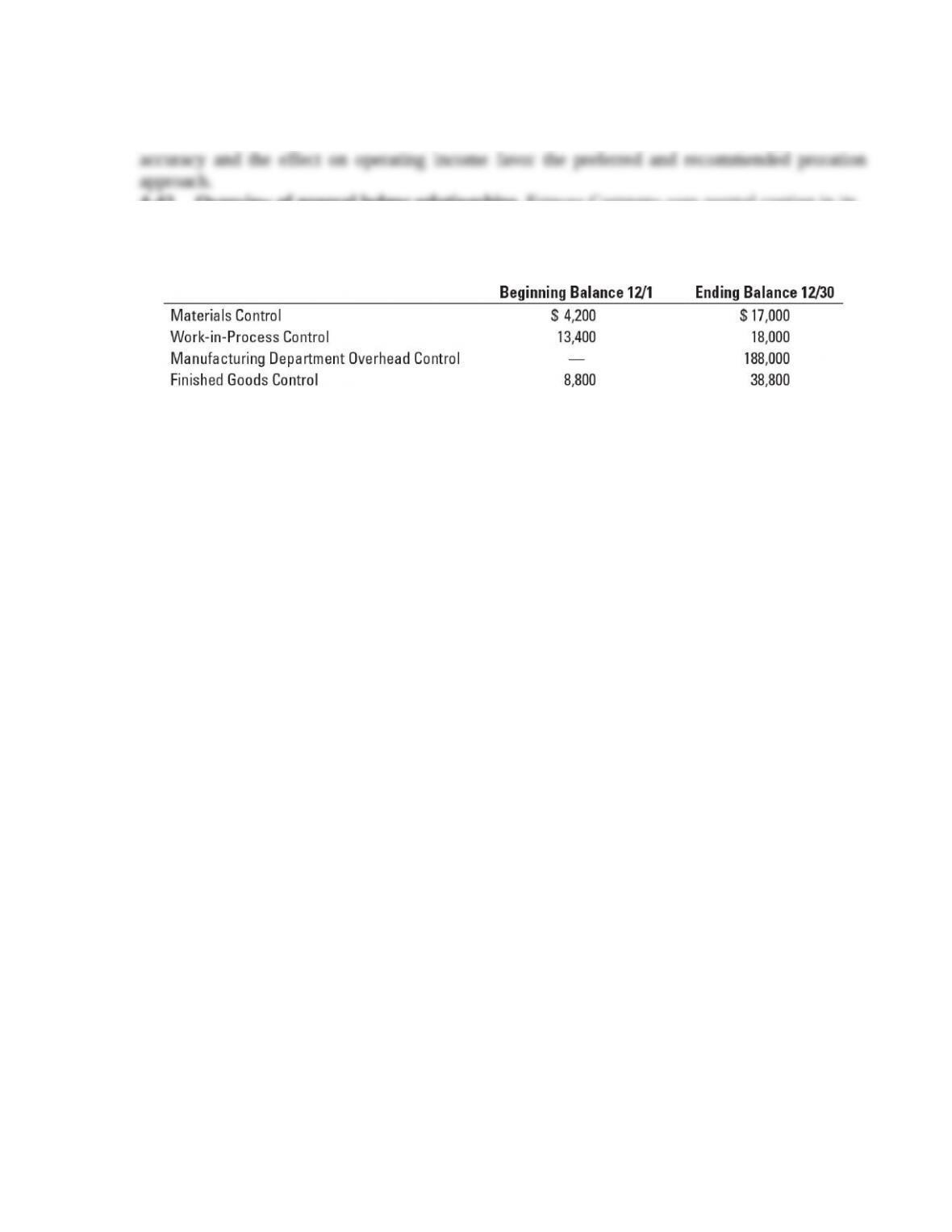

4-43 Overview of general ledger relationships. Estevez Company uses normal costing in its

job-costing system. The company produces kitchen cabinets. The beginning balances (December

1) and ending balances (as of December 30) in their inventory accounts are as follows:

Additional information follows:

a. Direct materials purchased during December were $132,600.

b. Cost of goods manufactured for December was $468,000.

c. No direct materials were returned to suppliers.

d. No units were started or completed on December 31 and no direct materials were

requisitioned on December 31.

e. The manufacturing labor costs for the December 31 working day: direct manufacturing labor,

$8,600, and indirect manufacturing labor, $2,800.

f. Manufacturing overhead has been allocated at 110% of direct manufacturing labor costs

through December 31.

Required:

1. Prepare journal entries for the December 31 payroll.

2. Use T-accounts to compute the following:

a. The total amount of materials requisitioned into work in process during December

b. The total amount of direct manufacturing labor recorded in work in process during

December (Hint: You have to solve requirements 2b and 2c simultaneously)

c. The total amount of manufacturing overhead recorded in work in process during

December

d. Ending balance in work in process, December 31

e. Cost of goods sold for December before adjustments for under- or overallocated

manufacturing overhead

3. Prepare closing journal entries related to manufacturing overhead. Assume that all under-

or overallocated manufacturing overhead is closed directly to Cost of Goods Sold.

SOLUTION

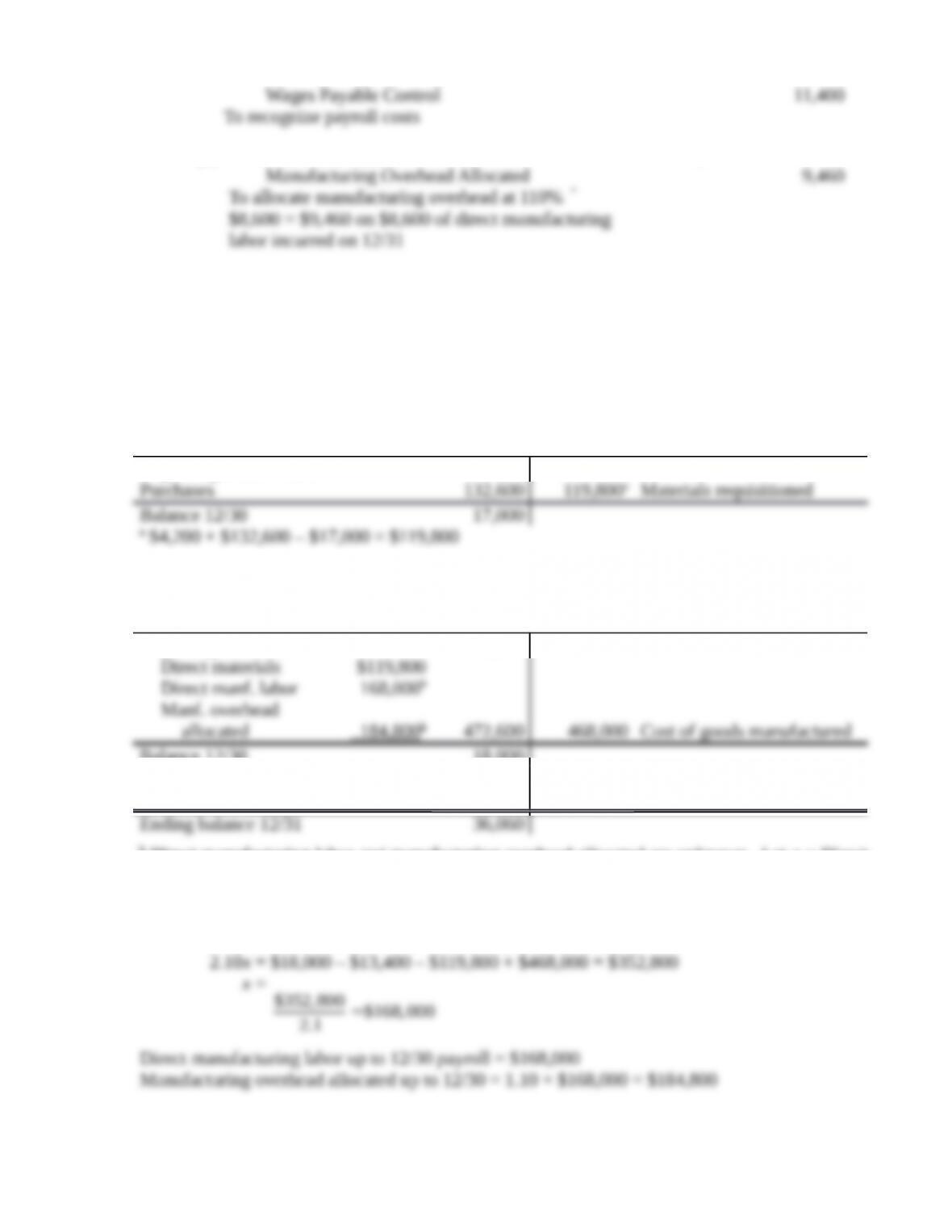

(4055 min.) Overview of general ledger relationships.

1. Adjusting entry for 12/31 payroll.

(a) Work-in-Process Control 8,600

Manufacturing Department Overhead Control 2,800

(b) Work-in-Process Control 9,460

Note: Students tend to forget entry (b) entirely. Stress that a budgeted overhead allocation

rate is used consistently throughout the year. This point is a major feature of this

problem.

2. a-e An effective approach to this problem is to draw T-accounts and insert all the known

figures. Then, working with T-account relationships, solve for the unknown figures. Entries (a)

and (b) are posted into the T-accounts that follow.

Materials Control

Beginning balance 12/1

4,200

(a) Direct materials requisitioned into work in process during December equals $119,800

because no materials are requisitioned on December 31.

Work-in-Process Control

Beginning balance 12/1

13,400

Balance 12/30 18,000

(a) Direct manuf. labor 12/31 payroll 8,600

(b) Manuf. overhead allocated 12/31 9,460c

b Direct manufacturing labor and manufacturing overhead allocated are unknown. Let x = Direct

manufacturing labor up to 12/30 payroll, then manufacturing overhead allocated up to 12/30

payroll = 1.10x

Use the T-account equation and solve for x:

$13,400 + $119,800 + x + 1.10x – $468,000 = $18,000

Total direct manufacturing labor for December = $168,000 + $8,600 (direct manufacturing labor

Total manufacturing overhead allocated for December = $184,800 + $9,460c = $194,260

labor incurred on 12/31.

(b) Total direct manufacturing labor for December = $176,600.

(c) Total manufacturing overhead allocated (recorded) in work in process equals $194,260.

(d) Ending balance in work-in-process inventory on December 31 equals $18,000 + $8,600

(direct manufacturing labor added on 12/31, requirement 1) + $9,460 (manufacturing

overhead allocated on 12/31, requirement 1) = $36,060.

An alternative approach to solving requirements 2b, 2c, and 2d is to calculate the

work-in-process inventory on December 31, recognizing that because no new units were started

or completed, no direct materials were added and the direct manufacturing labor and

manufacturing overhead allocated on December 31 were added to the work-in-process inventory

balance of December 30.

Work-in-process

inventory

=

Work-in-process

inventory on

+

Direct

manufacturin

g labor

+

Manufacturing

overhead

allocated on

We can now use the T-account equation for work-in-process inventory account from 12/1 to

12/31, as follows.

Let x = Direct manufacturing labor for December

Then 1.10x = Manufacturing overhead allocated for December

Work-in-p

rocess

inventory

on 12/1

+

Direct

materials

added in

December

+

Direct

manufacturing

labor added in

December

+

Manufacturing

overhead

allocated in

December

–

Cost of goods

manufactured

in December

=

Work-in-proce

ss inventory

on 12/31

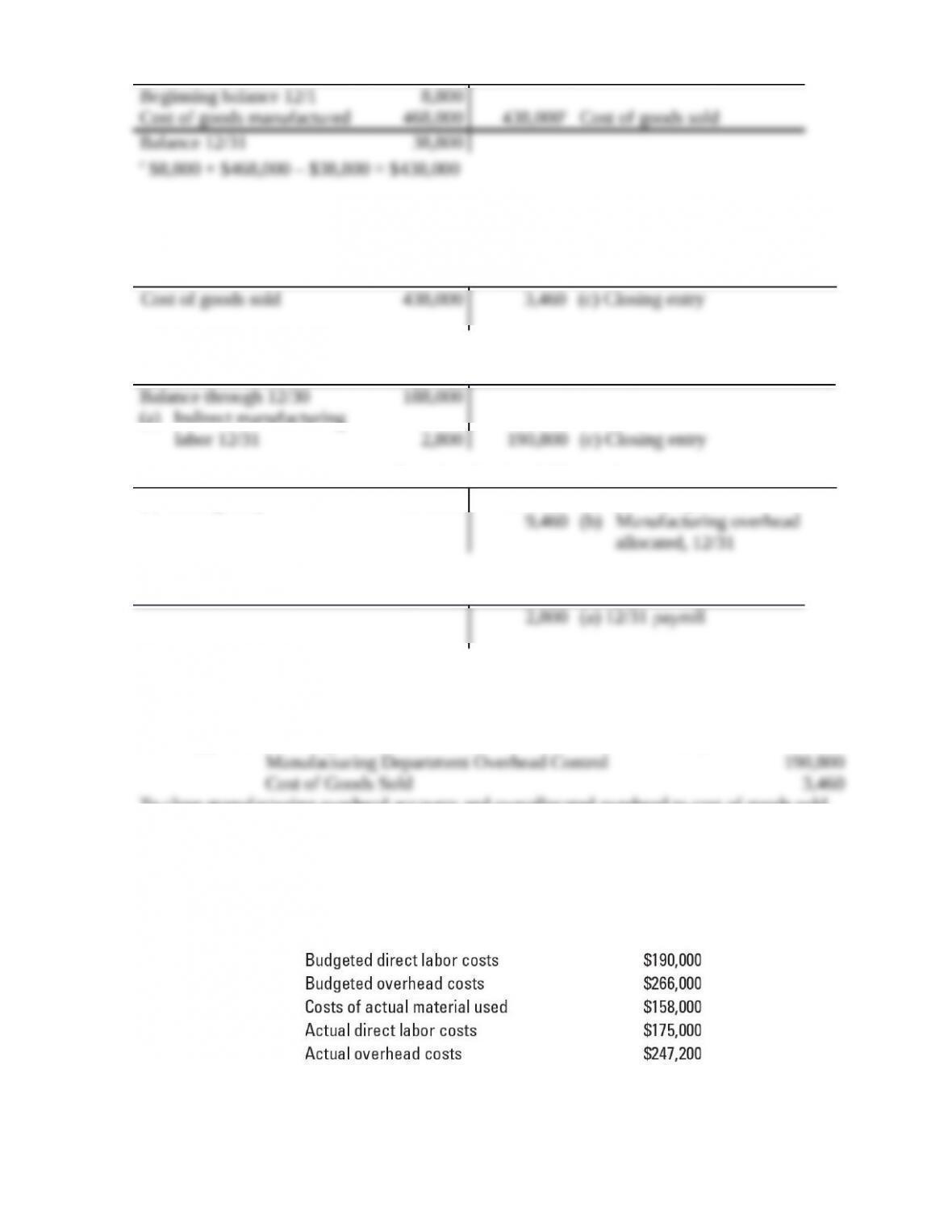

Finished Goods Control

(e) Cost of goods sold for December before adjustments for under- or overallocated overhead

equals $438,000:

Cost of Goods Sold

Manufacturing Department Overhead Control

Balance through 12/30

(a) Indirect manufacturing

188,000

Manufacturing Overhead Allocated

(c) Closing entry 194,260 184,800

Balance through 12/30

Wages Payable Control

3. Closing entries:

(c) Manufacturing Overhead Allocated 194,260

To close manufacturing overhead accounts and overallocated overhead to cost of goods sold

4-44 Allocation and proration of overhead. Resource Room prints custom training material

for corporations. The business was started January 1, 2017. The company uses a normal-costing

system. It has two direct-cost pools, materials and labor, and one indirect-cost pool, overhead.

Overhead is charged to printing jobs on the basis of direct labor cost. The following information

is available for 2017.

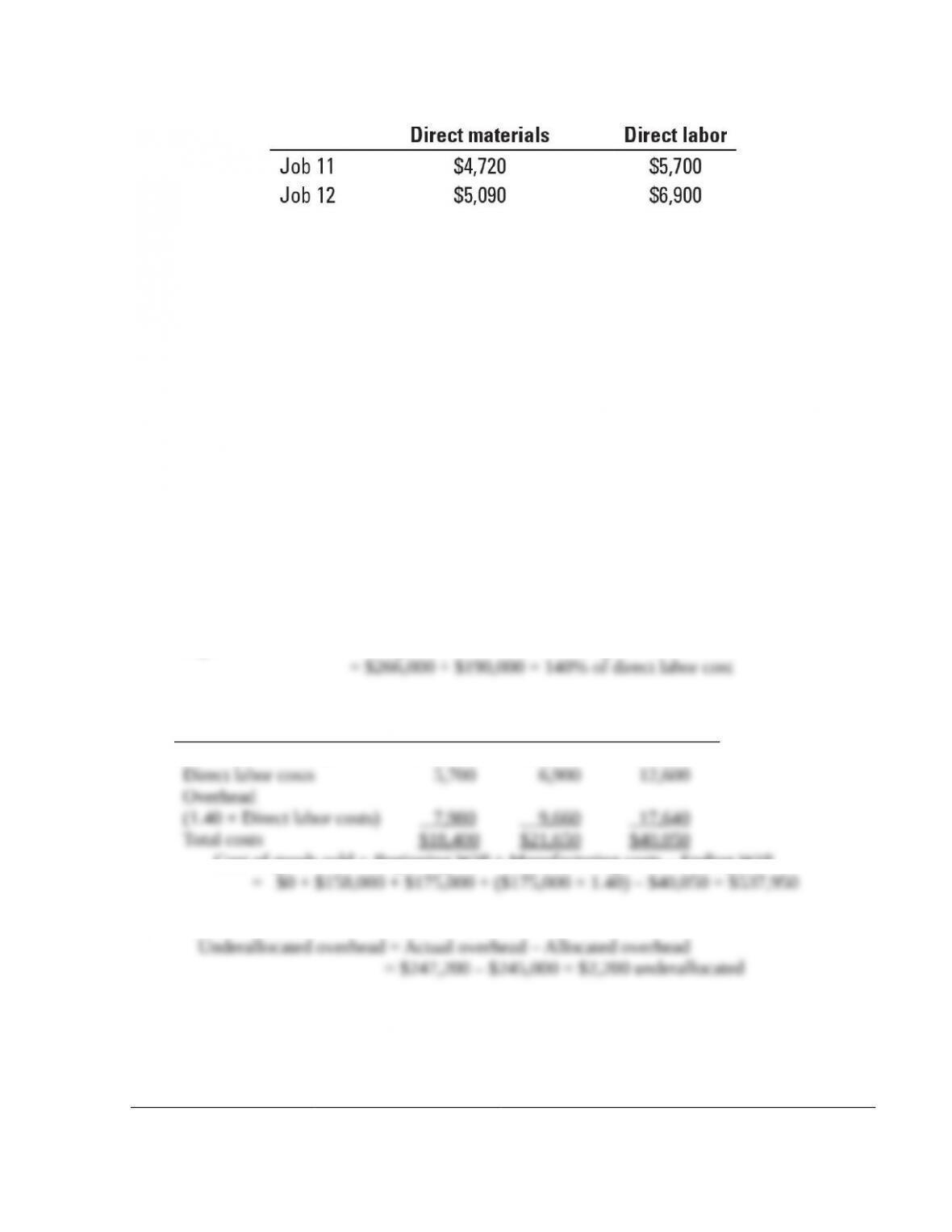

There were two jobs in process on December 31, 2017: Job 11 and Job 12. Costs added to each

job as of December 31 are as follows:

Resource Room has no finished-goods inventories because all printing jobs are transferred to

cost of goods sold when completed.

Required:

1. Compute the overhead allocation rate.

2. Calculate the balance in ending work in process and cost of goods sold before any

adjustments for under- or overallocated overhead.

3. Calculate under- or overallocated overhead.

4. Calculate the ending balances in work in process and cost of goods sold if the under- or

overallocated overhead amount is as follows:

a. Written off to cost of goods sold

b. Prorated using the overhead allocated in 2017 (before proration) in the ending balances of

cost of goods sold and work-in-process control accounts

5. Which of the methods in requirement 4 would you choose? Explain.

SOLUTION

(25 min.) Allocation and proration of overhead.

1. Budgeted overhead rate = Budgeted overhead costs ÷ Budgeted direct labor costs

2. Ending work in process

Job 11 Job 12 Total

Direct material costs $ 4,720 $ 5,090 $ 9,810

Cost of goods sold = Beginning WIP + Manufacturing costs – Ending WIP

3. Overhead allocated = 1.40 × $175,000 = $245,000

4a. All underallocated overhead is written off to cost of goods sold.

WIP inventory remains unchanged.

Account

(1)

Dec. 31, 2017

Account Balance

(Before Proration)

Write-off of $3,200

Underallocated

overhead

Dec. 31, 2017

Account Balance

(After Proration)

(2) (3) (4) = (2) + (3)

Work in Process $ 40,050 $ 0 $ 40,050

Cost of goods sold 537 ,950 2 ,200 540 ,150

4b. Underallocated overhead prorated based on overhead allocated before proration.

Account

(1)

Dec. 31, 2017

Account

Balance

(Before

Proration)

(2)

Allocated Overhead

Included in

Dec. 31, 2017

Account Balance

(Before Proration)

(3) (4)

Proration of $2,200

Underallocated

Manufacturing Overhead

(5)

Dec. 31, 2017

Account

Balance

(After

Proration)

(6) = (2) + (5)

Work in Process $ 40,050 $ 17,640a(7.2%) 0.072 $2,200 = $ 158 $ 40,208

5. Writing off all of the underallocated overhead to Cost of Goods Sold (COGS) is warranted

when COGS is large relative to Work-in-Process Inventory and Finished Goods Inventory and

the underallocated overhead is immaterial. Both these conditions apply in this case. Resource

Room should write off the $2,200 underallocated overhead to Cost of Goods Sold account.

4-45 (25–30 min.) Job costing, ethics. Joseph Underwood joined Anderson Enterprises as

controller in October 2016. Anderson Enterprises manufactures and installs home greenhouses.

The company uses a normal-costing system with two direct-cost pools, direct materials and

direct manufacturing labor, and one indirect-cost pool, manufacturing overhead. In 2016,

manufacturing overhead was allocated to jobs at 150% of direct manufacturing labor cost. At the

end of 2016, an immaterial amount of underallocated overhead was closed out to cost of goods

sold, and the company showed a small loss.

Underwood is eager to impress his new employer, and he knows that in 2017, Anderson’s

upper management is under pressure to show a profit in a challenging competitive environment

because they are hoping to be acquired by a large private equity firm sometime in 2018. At the

end of 2016, Underwood decides to adjust the manufacturing overhead rate to 160% of direct

labor cost. He explains to the company president that, because overhead was underallocated in

2016, this adjustment is necessary. Cost information for 2017 follows:

Anderson’s revenue for 2017 was $5,550,000, and the company’s selling and administrative

expenses were $2,720,000.

Required:

1. Insert the given information in the T-accounts below. Calculate the following amounts to

complete the T-accounts:

a. Direct materials control, 12/31/2017

b. Manufacturing overhead allocated, 2017

c. Cost of goods sold, 2017

2. Calculate the amount of under- or overallocated manufacturing overhead.

3. Calculate Anderson’s net operating income under the following:

a. Under- or overallocated manufacturing overhead is written off to cost of goods sold.

b. Under- or overallocated manufacturing overhead is prorated based on the ending balances

in work in process, finished goods, and cost of goods sold.

4. Underwood chooses option 3a above, stating that the amount is immaterial. Comment on the

ethical implications of his choice. Do you think that there were any ethical issues when he

established the manufacturing overhead rate for 2017 back in late 2016? Refer to the IMA

Statement of Ethical Professional Practice.